The Issue and Redemption of Debentures Class 12 solutions on this page solve every Short Answer, Long Answer, and Numerical Question of Part 2 Chapter 2 of the 2026-27 NCERT Accountancy textbook. Every numerical carries full journal entries plus DRR + DRI workings.

- CBSE Weightage: 6 to 10 marks per board paper

- Question Count: 17 SA, 8 LA, and 26+ Numericals covering issue at par/premium/discount, consideration other than cash, redemption, conversion, open-market purchase

Each NCERT solution for class 12 accountancy chapter 6 on this page is curated by Chartered Accountants and CBSE Commerce educators, mapped to the 2026-27 NCERT print, and refined against the last five years of CBSE board papers and CUET (UG) Commerce question patterns.

Also Check:

- Issue and Redemption of Debentures Class 12 Notes

- Accounting for Share Capital NCERT Solutions

- CBSE Class 12 Accountancy Syllabus 2026-27

Issue and Redemption of Debentures Class 12 Solutions: Question-Type Map

Part 2 Chapter 2 splits into three bands: theory (SA + LA), issue-side numericals, and redemption-side numericals. The table below maps each band to its sub-topics and marks.

| Section | Count | Sub-topic Focus | Difficulty |

|---|---|---|---|

| Short Answer | 17 | Meaning of debenture, bearer, collateral, capital reserve, irredeemable, convertible, mortgaged, premium on redemption | Easy |

| Long Answer | 8 | Types of debentures, debenture vs share, collateral, terms of issue, redemption out of capital vs profits, SEBI DRR, sinking fund, conversion | Medium |

| Numerical Q1 to Q10 | 10 | Issue at par, premium, discount, consideration other than cash, collateral, Loss on Issue | Easy to Medium |

| Numerical Q11 to Q20 | 10 | Discount + Premium on Redemption, four-combination table, listed company SEBI compliance | Medium |

| Numerical Q21 to Q26+ | 6+ | Redemption out of profits with DRR, out of capital, conversion, sinking fund, DRI | Hard |

The 6-mark CBSE Long Answer almost always comes from the redemption side, with DRR + DRI paired against a Balance Sheet extract.

Class 12 Accountancy Part 2 Chapter 2 Issue And Redemption Of Debentures NCERT Solutions

Source: Magnet Brains on YouTube

How the Collegedunia Solutions Are Structured

- Concept-used opener citing the relevant Section of the Companies Act 2013, Rule 18 of the Companies (Share Capital and Debentures) Rules 2014, and SEBI NCS Regulations 2021 where applicable.

- Step-by-step journal entries with Dr/Cr columns; the Loss on Issue account is opened separately for discount-plus-premium combinations.

- DRR workings at 10% of outstanding debentures for unlisted other companies post-2019 amendment.

- DRI workings at 15% of debentures maturing during the year, invested on or before April 30 in specified securities.

- Expert Solution at the end of every question with a Chartered-Accountant alternate angle and a one-line exam strategy.

Types of Debentures Covered

The chapter classifies debentures on six independent axes; a single instrument can sit on all six. The map below links each axis to the question where it is tested.

| Classification Axis | Types | Tested In |

|---|---|---|

| By security | Secured (mortgaged) vs Unsecured (naked) | SA Q3, Q9; LA Q1 |

| By records | Registered vs Bearer | SA Q2; LA Q1 |

| By redemption | Redeemable vs Irredeemable | SA Q7; LA Q1 |

| By convertibility | NCD, FCD, PCD | SA Q8, Q15; LA Q8 |

| By priority | First vs Second Debenture | LA Q1 |

| By interest rate | Fixed vs Floating | SA Q1; LA Q1 |

Terms of Issue: Par, Premium, Discount and the Four-Combination Table

Debentures can be issued at three prices and redeemed at two, giving six combinations. Loss on Issue is the chapter's signature pain-point, written off from Securities Premium first, then P&L.

| Issue Price | Redemption Price | Loss on Issue? | Numerical |

|---|---|---|---|

| At Par (100) | At Par (100) | No | Q1, Q2 |

| At Premium (110) | At Par (100) | No (Securities Premium credited) | Q3 |

| At Discount (95) | At Par (100) | Yes, discount of 5 is the loss | Q4, Q5, Q14 |

| At Par (100) | At Premium (110) | Yes, premium on redemption of 10 | Q15 |

| At Discount (95) | At Premium (110) | Yes, loss = 5 + 10 = 15 | Q12, Q13 |

| At Premium (105) | At Premium (110) | Yes, premium on redemption of 5 | Q16 |

Issue of Debentures for Consideration Other Than Cash

When a company settles a vendor or buys assets by issuing debentures, the textbook treats it in three steps. Q9, Q10, Q11 show all three.

- Assets. Dr. Sundry Assets, Cr. Sundry Liabilities, Cr. Vendor A/c.

- Goodwill/Capital Reserve. Difference between consideration and net assets to Goodwill (excess) or Capital Reserve (shortage).

- Settlement. Dr. Vendor A/c, Cr. Debentures A/c (face value), Cr. Securities Premium or Dr. Discount.

Debentures Issued as Collateral Security

When a company pledges its own debentures for a bank loan, two treatments exist. SA Q3 and LA Q3 both ask which is preferred.

- No entry: A note is added to the Balance Sheet under the loan. SEBI-preferred treatment.

- Entry passed: Dr. Debenture Suspense A/c, Cr. Debentures A/c, face value pledged. Suspense is deducted from Debentures.

Redemption of Debentures: Four Methods Compared

Redemption discharges the company's debenture liability at or before maturity. Section 71 of the Companies Act 2013 and Rule 18 of the 2014 Rules govern the procedure.

| Method | Mechanism | DRR? | Tested In |

|---|---|---|---|

| Lump-sum at maturity | Full face value paid on maturity date | Yes, 10% | Q22, Q23 |

| Installment (draw of lots) | A portion redeemed each year by random draw | Yes, proportionate | Q24 |

| Open-market purchase | Company buys back from the stock exchange | Yes if from capital | Q25, Q26 |

| Conversion | Debentures swapped against equity or new debentures | No | Q21 |

Redemption out of Profits vs Out of Capital

| Aspect | Out of Profits | Out of Capital |

|---|---|---|

| Source | Surplus in Statement of P&L | Share Capital, fresh issue, asset realisation |

| Transfer to DRR | Equal to nominal value of debentures redeemed | Not required post-2019 for listed |

| Liquidity impact | Reduces free reserves; protects working capital | Reduces capital base |

| Entry on redemption | Dr. Surplus, Cr. DRR; then Dr. Debentures, Cr. Debenture-holders | Direct: Dr. Debentures, Cr. Debenture-holders |

Tip: in any CBSE board paper after 2019, assume the listed-company DRR rate of 10% unless the question says "private limited", in which case DRR is not required.

DRR Guidelines: 2019 Amendment Rates

The 2019 amendment to Rule 18(7) set new rates. The NCERT print and the 2026-27 CBSE syllabus follow these.

| Type of Company | DRR Rate | DRI Rate |

|---|---|---|

| AIFIs regulated by RBI | Nil | Nil |

| Listed NBFCs and HFCs | Nil | 15% |

| Other Listed Companies | Nil | 15% |

| Unlisted NBFCs and HFCs | Nil | 15% |

| Other Unlisted Companies | 10% | 15% |

Part 2 Chapter 2 Weightage Across Class 12 Accountancy

Part 2 Chapter 2 is the second-heaviest in Part B after Share Capital. It is a near-certain source of a 6-mark numerical in every CBSE board paper since 2018.

| Chapter | Topic | Avg CBSE Marks |

|---|---|---|

| Ch 1 | Accounting for Partnership: Basic Concepts | 6 marks |

| Ch 2 | Reconstitution: Admission of a Partner | 10 marks |

| Ch 3 | Reconstitution: Retirement or Death | 8 marks |

| Ch 4 | Dissolution of Partnership Firm | 6 marks |

| Part 2 Ch 1 | Accounting for Share Capital | 12 marks |

| Part 2 Ch 2 | Issue and Redemption of Debentures | 8 to 10 marks |

| Part 2 Ch 3 | Financial Statements of a Company | 6 marks |

| Part 2 Ch 4 | Analysis of Financial Statements | 4 marks |

| Part 2 Ch 5 | Accounting Ratios | 6 marks |

| Part 2 Ch 6 | Cash Flow Statement | 6 marks |

Common Mistakes in Issue and Redemption of Debentures

- Crediting Premium on Issue to Debentures A/c instead of Securities Premium Reserve.

- Writing off Loss on Issue only from P&L; priority is Securities Premium first.

- Forgetting interest on debentures when the company has a loss; interest is a charge, not appropriation.

- Treating DRR and DRI as the same thing. DRR is a liability-side reserve; DRI is an asset-side investment.

- Applying the old 25% DRR on post-2019 listed numericals. The current rate for unlisted other companies is 10%.

- Adjusting Premium on Redemption against P&L at redemption instead of recognising it as a liability at issue.

Each one costs 1 to 2 marks on the 6-mark Long Answer.

Student Pulse: Part 2 Chapter 2 Difficulty Rating from Our Student Poll

In a Collegedunia poll of 12,840 Class 12 Commerce students conducted before the 2026 boards, 64% of students rated the discount-plus-premium-on-redemption Loss on Issue entry as the trickiest journal in the chapter, ahead of the DRR + DRI calculation for partly-redeemed installments.

What 12,840 students told us about the Part 2 Chapter 2 study journey:

- 64% of students surveyed rated the Loss on Issue (discount + premium combined) as most-confusing.

- 52% reported confusing DRR with DRI at least once on a class test.

- 4 out of 5 students practised Q12 (the four-combination table) the week before boards.

- Average student took 3.4 hours for first-read and 1.8 hours for focused revision.

- Out of 12,840 students, 71% attempted every back-exercise.

Source: 2025-26 Class 12 Accountancy student poll. Sample of 12,840 students across 14 states.

Sample Fully-Solved Question: Discount on Issue + Premium on Redemption

Question (6 marks). A. Ltd. issued 10,000, 9% debentures of Rs. 100 each at 5% discount, redeemable at 10% premium. Pass journal entries and write off Loss on Issue with Securities Premium of Rs. 40,000.

Step 1. Discount = Rs. 50,000. Premium on redemption = Rs. 1,00,000. Total Loss on Issue = Rs. 1,50,000.

Step 2, Allotment. Dr. Bank Rs. 9,50,000; Dr. Loss on Issue Rs. 1,50,000; Cr. 9% Debentures Rs. 10,00,000; Cr. Premium on Redemption Rs. 1,00,000.

Step 3, Write off Loss. Dr. Securities Premium Rs. 40,000; Dr. P&L Rs. 1,10,000; Cr. Loss on Issue Rs. 1,50,000.

Expert's angle: CBSE markers expect Premium on Redemption to be recognised as a liability at issue, not a contingency. Most students lose marks by writing off Rs. 1,50,000 entirely from P&L.

All NCERT Solutions for Issue and Redemption of Debentures with Step-by-Step Working

Every NCERT textbook question for Class 12 Accountancy Part 2 Chapter 2 Issue and Redemption of Debentures is listed below with its full Solution and Expert Solution hidden inside collapsible tabs. Click Check Solution to reveal the step-by-step working; click Expert Solution for the expanded explanation.

Questions

What is meant by a Debenture?

Concept used. A Debenture is a written instrument acknowledging a debt of the company. As per Section 2(30) of the Companies Act 2013, ``debenture includes debenture stock, bonds or any other instrument of a company evidencing a debt, whether constituting a charge on the assets of the company or not.'' It is the most important form of long-term borrowing for a company.

- Nature. A debenture is an acknowledgement of debt issued under the company's common seal (now optional) carrying a fixed rate of interest.

- Holder is a creditor. Unlike a shareholder (owner), a debenture-holder is a creditor of the company.

- Interest is a charge on profit. Interest on debentures is paid whether the company makes profit or not.

- Secured or unsecured. A debenture may or may not be secured by a charge on the assets of the company.

- Redemption. Debentures are normally repayable after a fixed period (5–10 years).

A debenture (Section 2(30), Companies Act 2013) is a written instrument issued by a company acknowledging a debt, carrying a fixed rate of interest, repayable after a stated period. The holder is a creditor, not an owner.

Quick reading. Think of a debenture as a loan slip the company hands you: you pay money, the company promises a fixed rate of interest and the return of principal after a stated period.

- Acknowledgement of debt → holder is a creditor.

- Fixed-rate interest paid even in loss years.

- Repaid after fixed term (often 5–10 years).

- May be secured (charge on assets) or unsecured.

Why this matters. In a Class 12 numerical question on Issue and Redemption of Debentures, the examiner gives full marks only when the candidate distinguishes Discount on Issue of Debentures (a capital loss written off over the life of the debentures) from Premium on Redemption of Debentures (a provision created on issue), applies the Companies (Share Capital and Debentures) Rules 2014 for the Debenture Redemption Reserve, and presents every issue and redemption journal entry in narrated form. A correct closing debenture figure without the DRR working and the narrated journal entries loses 30-50 percent of the marks under the CBSE step-marking scheme.

Common mistakes. Three predictable slips lose marks: (a) confusing Discount on Issue with Premium on Redemption and posting both to the same ledger; (b) ignoring the requirement to create Debenture Redemption Reserve of at least 25 percent of the outstanding debentures before the start of redemption; (c) missing the loss on issue of debentures that arises when debentures are issued at par or discount but redeemed at a premium.

Debenture = company's loan slip; creditor relationship; fixed-rate interest; repayable on maturity.

What does a Bearer Debenture mean?

Concept used. A Bearer Debenture is a debenture which is transferable by mere delivery (like a currency note). The company does NOT maintain a register of debenture-holders for bearer debentures; the person holding the certificate is treated as the owner.

- Transfer by delivery. No registration of transfer is required: handing over the certificate effects the transfer.

- No register kept. Unlike registered debentures, the company keeps no record of the holder.

- Interest paid via coupons. The certificate has detachable coupons; the debenture-holder presents a coupon on each interest date to receive the interest.

- Negotiable instrument. Treated as a negotiable instrument under the Negotiable Instruments Act 1881; the bona-fide holder for value gets a good title.

A bearer debenture is one that is transferable by mere delivery; no register of holders is kept; interest is paid against detachable coupons. It is a negotiable instrument.

Quick reading. Bearer = ``whoever holds it.'' Like cash, ownership passes with delivery; no paperwork.

- Anonymous transfer; no register kept.

- Detachable interest coupons.

- Negotiable instrument ⇒ bona-fide holder gets clean title.

Why this matters. In a Class 12 numerical question on Issue and Redemption of Debentures, the examiner gives full marks only when the candidate distinguishes Discount on Issue of Debentures (a capital loss written off over the life of the debentures) from Premium on Redemption of Debentures (a provision created on issue), applies the Companies (Share Capital and Debentures) Rules 2014 for the Debenture Redemption Reserve, and presents every issue and redemption journal entry in narrated form. A correct closing debenture figure without the DRR working and the narrated journal entries loses 30-50 percent of the marks under the CBSE step-marking scheme.

Common mistakes. Three predictable slips lose marks: (a) confusing Discount on Issue with Premium on Redemption and posting both to the same ledger; (b) ignoring the requirement to create Debenture Redemption Reserve of at least 25 percent of the outstanding debentures before the start of redemption; (c) missing the loss on issue of debentures that arises when debentures are issued at par or discount but redeemed at a premium.

Bearer debenture = transferable by delivery + coupon-paid interest + negotiable instrument.

State the meaning of `Debentures issued as a collateral security'.

Concept used. Debentures issued as collateral security are debentures issued in addition to the principal security as a secondary cover for a loan or bank borrowing. They are a contingent liability: the lender enforces them only if the principal security proves insufficient.

- Definition. ``Collateral'' means additional or secondary security.

- Trigger. Issued when a company borrows funds (loan, overdraft, cash credit) and the lender wants extra protection.

- No fresh cash. The company does NOT receive any cash for the collateral debentures themselves; the cash has already been received against the principal loan.

- Dormant. As long as the company repays the loan on time, the collateral debentures are dormant. If the company defaults, the lender enforces them.

- No interest payable. No interest is paid on collateral debentures (they are not in circulation).

Collateral debentures are debentures issued as an additional cover for a loan, not for fresh cash. They are dormant, non-interest-bearing, and enforced only if the principal security fails.

Strategic angle. Two securities, one loan: the principal security (e.g. hypothecation of stock) and the back-up (debentures). No cash flows for the debentures themselves.

- Lender takes principal security + collateral debentures.

- No cash, no interest on collateral.

- On default, lender claims under collateral; debentures spring to life.

Why this matters. In a Class 12 numerical question on Issue and Redemption of Debentures, the examiner gives full marks only when the candidate distinguishes Discount on Issue of Debentures (a capital loss written off over the life of the debentures) from Premium on Redemption of Debentures (a provision created on issue), applies the Companies (Share Capital and Debentures) Rules 2014 for the Debenture Redemption Reserve, and presents every issue and redemption journal entry in narrated form. A correct closing debenture figure without the DRR working and the narrated journal entries loses 30-50 percent of the marks under the CBSE step-marking scheme.

Common mistakes. Three predictable slips lose marks: (a) confusing Discount on Issue with Premium on Redemption and posting both to the same ledger; (b) ignoring the requirement to create Debenture Redemption Reserve of at least 25 percent of the outstanding debentures before the start of redemption; (c) missing the loss on issue of debentures that arises when debentures are issued at par or discount but redeemed at a premium.

Back-up cover only; no cash, no interest; activated on default.

What is meant by `Issue of debentures for consideration other than cash'?

Concept used. Issue of debentures for consideration other than cash is the allotment of debentures to a vendor or supplier in payment for assets purchased (or business taken over), instead of paying in cash. The company conserves cash and the vendor becomes a debenture-holder.

- Trigger. The company acquires assets (machinery, business, or net assets of a firm) and settles the purchase consideration by issuing debentures to the vendor.

- Number of debentures. No. of debentures = Purchase ConsiderationIssue Price per debenture. Issue price equals face value (at par), face - discount (at discount), or face + premium (at premium).

- Journal entries.

- Dr. Sundry Assets A/c; Cr. Vendor A/c (with agreed value of assets).

- Dr. Vendor A/c; Cr. Debentures A/c (at par); also Cr. Securities Premium Reserve (if at premium); or Dr. Discount on Issue (if at discount).

- Goodwill / Capital Reserve. If purchase consideration > net assets taken over, the difference is Goodwill. If purchase consideration < net assets, the difference is Capital Reserve.

Issue of debentures for consideration other than cash means allotting debentures to a vendor against assets purchased. Number of debentures = Purchase Consideration ÷ Issue Price. Excess of PC over net assets = Goodwill.

Quick reading. Pay the vendor in debentures rather than cash.

- Compute purchase consideration agreed with vendor.

- Divide by issue price to get number of debentures.

- Pass two entries: asset purchase + payment in debentures.

Why this matters. In a Class 12 numerical question on Issue and Redemption of Debentures, the examiner gives full marks only when the candidate distinguishes Discount on Issue of Debentures (a capital loss written off over the life of the debentures) from Premium on Redemption of Debentures (a provision created on issue), applies the Companies (Share Capital and Debentures) Rules 2014 for the Debenture Redemption Reserve, and presents every issue and redemption journal entry in narrated form. A correct closing debenture figure without the DRR working and the narrated journal entries loses 30-50 percent of the marks under the CBSE step-marking scheme.

Common mistakes. Three predictable slips lose marks: (a) confusing Discount on Issue with Premium on Redemption and posting both to the same ledger; (b) ignoring the requirement to create Debenture Redemption Reserve of at least 25 percent of the outstanding debentures before the start of redemption; (c) missing the loss on issue of debentures that arises when debentures are issued at par or discount but redeemed at a premium.

Vendor paid in debentures; number = PC ÷ issue price.

What is meant by Issue of debenture at discount and redeemable at premium?

Concept used. This is a double-loss situation. The debenture is issued below face value (discount on issue) AND repaid above face value (premium on redemption). Both add to the company's loss; their sum is debited to Loss on Issue of Debentures A/c at the time of issue.

- Issue at discount. The investor pays less than face value (e.g. Rs. 95 for a Rs. 100 debenture). The discount is recognised as a deferred loss.

- Redemption at premium. On maturity the company pays more than face value (e.g. Rs. 110 for a Rs. 100 debenture). The extra Rs. 10 is also a loss.

- Total loss per debenture. Loss = Discount on issue + Premium on redemption. For the example: 5 + 10 = Rs. 15 per debenture.

- Journal entry on issue.

- Dr. Bank A/c (face - discount).

- Dr. Loss on Issue of Debentures A/c (discount + premium).

- Cr. Debentures A/c (face).

- Cr. Premium on Redemption of Debentures A/c (premium on redemption).

- Write-off. The Loss is written off against Securities Premium Reserve / Statement of Profit & Loss in subsequent years.

Discount on issue + premium on redemption are both losses; recognised together at issue as Loss on Issue of Debentures A/c. Premium on Redemption is a liability shown until redemption.

Quick reading. Company loses twice: less cash in at issue, more cash out at redemption. Both losses are booked upfront.

- Cash in = face - discount.

- Cash out = face + premium.

- Total loss = discount + premium ⇒ Dr. Loss on Issue.

Why this matters. In a Class 12 numerical question on Issue and Redemption of Debentures, the examiner gives full marks only when the candidate distinguishes Discount on Issue of Debentures (a capital loss written off over the life of the debentures) from Premium on Redemption of Debentures (a provision created on issue), applies the Companies (Share Capital and Debentures) Rules 2014 for the Debenture Redemption Reserve, and presents every issue and redemption journal entry in narrated form. A correct closing debenture figure without the DRR working and the narrated journal entries loses 30-50 percent of the marks under the CBSE step-marking scheme.

Common mistakes. Three predictable slips lose marks: (a) confusing Discount on Issue with Premium on Redemption and posting both to the same ledger; (b) ignoring the requirement to create Debenture Redemption Reserve of at least 25 percent of the outstanding debentures before the start of redemption; (c) missing the loss on issue of debentures that arises when debentures are issued at par or discount but redeemed at a premium.

Loss on Issue = Discount + Premium on Redemption; both booked at issue date.

What is `Capital Reserve'?

Concept used. Capital Reserve is a reserve created out of capital profits (profits that are not earned in the normal course of business). It is NOT available for distribution as cash dividend; it can be used only for specific purposes prescribed under the Companies Act 2013.

- Source. Created from capital profits: profit on sale of fixed assets, profit on re-issue of forfeited shares, profit on redemption of debentures (purchase from open market below face value), premium on issue of shares prior to Section 52, etc.

- Not for dividend. Cannot be used to pay cash dividend (not a free reserve).

- Permissible uses. (a) Issue of fully paid bonus shares; (b) writing off capital losses; (c) writing off preliminary expenses.

- Disclosure. Shown under ``Reserves and Surplus'' on the equity & liabilities side of the balance sheet (Schedule III, Part I).

Capital Reserve is a reserve from capital profits (e.g. profit on forfeiture re-issue, profit on redemption of debentures). Not for cash dividend; usable for bonus shares and writing off capital losses.

Strategic angle. The word ``capital'' restricts use: dividends come from revenue profits, not capital profits.

- Capital profit (asset sale, forfeiture) → Capital Reserve.

- Cannot be drawn as cash dividend.

- Used for bonus shares or to absorb capital losses.

Why this matters. In a Class 12 numerical question on Issue and Redemption of Debentures, the examiner gives full marks only when the candidate distinguishes Discount on Issue of Debentures (a capital loss written off over the life of the debentures) from Premium on Redemption of Debentures (a provision created on issue), applies the Companies (Share Capital and Debentures) Rules 2014 for the Debenture Redemption Reserve, and presents every issue and redemption journal entry in narrated form. A correct closing debenture figure without the DRR working and the narrated journal entries loses 30-50 percent of the marks under the CBSE step-marking scheme.

Common mistakes. Three predictable slips lose marks: (a) confusing Discount on Issue with Premium on Redemption and posting both to the same ledger; (b) ignoring the requirement to create Debenture Redemption Reserve of at least 25 percent of the outstanding debentures before the start of redemption; (c) missing the loss on issue of debentures that arises when debentures are issued at par or discount but redeemed at a premium.

Capital Reserve = from capital profits; never paid as dividend; funds bonus shares.

What is meant by a `Irredeemable Debenture'?

Concept used. An Irredeemable Debenture (also called Perpetual Debenture) is a debenture which is NOT repayable during the lifetime of the company. The principal becomes payable only on liquidation (winding-up) of the company, or upon a specified contingency arising.

- No fixed maturity. Unlike ordinary debentures, no fixed redemption date is stated.

- Repayable on winding-up. The company must repay the principal only when it is being wound up, or on the happening of a specified event (e.g. default in interest).

- Interest continues. The company keeps paying interest annually at the agreed rate until the contingency arises.

- Indian law. Section 71(4) of the Companies Act 2013 prohibits issue of debentures with perpetual maturity by Indian companies for issues after April 1, 2014. Hence, irredeemable debentures are now of historical / international relevance.

Irredeemable / perpetual debenture: no fixed redemption date; principal repayable only on winding-up or on a specified contingency. Prohibited in India after April 1, 2014 (Section 71(4)).

Quick reading. ``Never to be redeemed'' except when the company itself ceases.

- No maturity date in the deed.

- Interest paid forever, principal stays as long as company runs.

- Now banned in India (Section 71(4), Companies Act 2013).

Why this matters. In a Class 12 numerical question on Issue and Redemption of Debentures, the examiner gives full marks only when the candidate distinguishes Discount on Issue of Debentures (a capital loss written off over the life of the debentures) from Premium on Redemption of Debentures (a provision created on issue), applies the Companies (Share Capital and Debentures) Rules 2014 for the Debenture Redemption Reserve, and presents every issue and redemption journal entry in narrated form. A correct closing debenture figure without the DRR working and the narrated journal entries loses 30-50 percent of the marks under the CBSE step-marking scheme.

Common mistakes. Three predictable slips lose marks: (a) confusing Discount on Issue with Premium on Redemption and posting both to the same ledger; (b) ignoring the requirement to create Debenture Redemption Reserve of at least 25 percent of the outstanding debentures before the start of redemption; (c) missing the loss on issue of debentures that arises when debentures are issued at par or discount but redeemed at a premium.

Perpetual debenture; principal only on liquidation; banned in India after 2014.

What is a `Convertible Debenture'?

Concept used. A Convertible Debenture is a debenture which can be converted into equity shares (or other securities) of the company after a specified period, at terms agreed at the time of issue. The holder enjoys both: a creditor's interest until conversion and an owner's stake after conversion.

- Types. (a) Fully Convertible Debentures (FCD): the entire face value converts into shares. (b) Partly Convertible Debentures (PCD): a part converts; the balance is redeemed in cash. (c) Non-Convertible Debentures (NCD): do not convert; redeemed in cash.

- Conversion terms. The conversion price and ratio are fixed at issue (e.g. Rs. 100 debenture converts into 2 equity shares of Rs. 50 each after 3 years).

- Until conversion. The holder receives interest at the stated rate.

- Compulsory or optional. Conversion may be compulsory (CCD) or at the holder's option (OCD).

Convertible Debenture = debenture convertible into equity shares after a stated period at pre-agreed terms. FCD (fully), PCD (partly), CCD (compulsorily) and OCD (optionally) are the main sub-types.

Quick reading. Debt with an option to swap into equity later. Investor enjoys both worlds.

- Fully (FCD), partly (PCD), or compulsorily (CCD) convertible.

- Interest paid until conversion date.

- Conversion price fixed at issue.

Why this matters. In a Class 12 numerical question on Issue and Redemption of Debentures, the examiner gives full marks only when the candidate distinguishes Discount on Issue of Debentures (a capital loss written off over the life of the debentures) from Premium on Redemption of Debentures (a provision created on issue), applies the Companies (Share Capital and Debentures) Rules 2014 for the Debenture Redemption Reserve, and presents every issue and redemption journal entry in narrated form. A correct closing debenture figure without the DRR working and the narrated journal entries loses 30-50 percent of the marks under the CBSE step-marking scheme.

Common mistakes. Three predictable slips lose marks: (a) confusing Discount on Issue with Premium on Redemption and posting both to the same ledger; (b) ignoring the requirement to create Debenture Redemption Reserve of at least 25 percent of the outstanding debentures before the start of redemption; (c) missing the loss on issue of debentures that arises when debentures are issued at par or discount but redeemed at a premium.

Debt-now, equity-later instrument; FCD / PCD / CCD / OCD variants.

What is meant by `Mortgaged Debentures'?

Concept used. Mortgaged Debentures (also called Secured Debentures) are debentures which are secured by a mortgage / charge on some specified asset (or all assets) of the company. If the company defaults, the debenture-holders can enforce the charge and recover their money from the mortgaged asset.

- Charge created. A fixed charge (on a specific asset like land or plant) or a floating charge (on all current assets) is registered with the Registrar of Companies under Section 77 of the Companies Act 2013.

- Debenture trust deed. Section 71(5) requires that the company appoint a Debenture Trustee who holds the charge on behalf of all debenture-holders.

- On default. Trustees may sell the mortgaged asset and pay off the debenture- holders from the sale proceeds, ahead of unsecured creditors.

- Tenure. As per Rule 18(1)(a), secured debentures must be redeemable within 10 years (or 30 years for infrastructure companies) from the date of issue.

Mortgaged / secured debentures carry a fixed or floating charge on company assets, registered with the RoC and held by a Debenture Trustee. On default, trustees enforce the charge to repay the debenture-holders.

Strategic angle. ``Mortgaged'' = ``secured by a charge.'' Charge registered, trustees appointed, recovery path defined.

- Charge created on assets (fixed / floating).

- Section 77 registration; Section 71(5) trustee.

- Default ⇒ trustees sell asset; debenture-holders paid before unsecured creditors.

Why this matters. In a Class 12 numerical question on Issue and Redemption of Debentures, the examiner gives full marks only when the candidate distinguishes Discount on Issue of Debentures (a capital loss written off over the life of the debentures) from Premium on Redemption of Debentures (a provision created on issue), applies the Companies (Share Capital and Debentures) Rules 2014 for the Debenture Redemption Reserve, and presents every issue and redemption journal entry in narrated form. A correct closing debenture figure without the DRR working and the narrated journal entries loses 30-50 percent of the marks under the CBSE step-marking scheme.

Common mistakes. Three predictable slips lose marks: (a) confusing Discount on Issue with Premium on Redemption and posting both to the same ledger; (b) ignoring the requirement to create Debenture Redemption Reserve of at least 25 percent of the outstanding debentures before the start of redemption; (c) missing the loss on issue of debentures that arises when debentures are issued at par or discount but redeemed at a premium.

Secured-by-asset; RoC-registered charge; trustee-protected.

What is discount on issue of debentures?

Concept used. Discount on Issue of Debentures is the amount by which the issue price of a debenture is less than its face value (nominal value). It is a capital loss to the company and is debited to Discount on Issue of Debentures A/c.

- Computation. Discount per debenture = Face Value - Issue Price. Example: face Rs. 100, issue price Rs. 95 ⇒ discount = Rs. 5 per debenture.

- Journal entry on issue.

- Dr. Bank A/c (Issue Price).

- Dr. Discount on Issue of Debentures A/c (Discount).

- Cr. Debentures A/c (Face Value).

- Disclosure. Discount is shown under Other Non-Current Assets (Schedule III) until it is written off.

- Write-off. Discount is written off (a) against Securities Premium Reserve (Section 52), or (b) against Statement of Profit & Loss, over the life of the debentures.

Discount on Issue of Debentures = Face Value - Issue Price. Capital loss; recorded on the asset side; written off against Securities Premium or P&L over the debentures' life.

Quick reading. Issued below par ⇒ the shortfall is the discount ⇒ a capital loss spread over the life of the debenture.

- Discount = Face - Issue Price.

- Booked as deferred capital loss.

- Written off year by year over the debenture's tenure.

Why this matters. In a Class 12 numerical question on Issue and Redemption of Debentures, the examiner gives full marks only when the candidate distinguishes Discount on Issue of Debentures (a capital loss written off over the life of the debentures) from Premium on Redemption of Debentures (a provision created on issue), applies the Companies (Share Capital and Debentures) Rules 2014 for the Debenture Redemption Reserve, and presents every issue and redemption journal entry in narrated form. A correct closing debenture figure without the DRR working and the narrated journal entries loses 30-50 percent of the marks under the CBSE step-marking scheme.

Common mistakes. Three predictable slips lose marks: (a) confusing Discount on Issue with Premium on Redemption and posting both to the same ledger; (b) ignoring the requirement to create Debenture Redemption Reserve of at least 25 percent of the outstanding debentures before the start of redemption; (c) missing the loss on issue of debentures that arises when debentures are issued at par or discount but redeemed at a premium.

Capital loss; amortised over the debenture's life.

What is meant by `Premium on Redemption of Debentures'?

Concept used. Premium on Redemption of Debentures is the excess amount the company pays to a debenture-holder over and above the face value of the debenture at the time of redemption. It is a liability from the date of issue and a capital loss for the company.

- Computation. Premium on Redemption per debenture = Redemption Price - Face Value. Example: face Rs. 100, redemption Rs. 105 ⇒ premium = Rs. 5.

- Recognised at issue. The liability is recognised on the date of issue itself (matching principle): the company knows from day one how much extra it will eventually pay.

- Journal entry at issue.

- Dr. Loss on Issue of Debentures A/c (Discount + Premium on Redemption).

- Cr. Premium on Redemption of Debentures A/c (Premium).

- (Plus the usual Dr. Bank, Cr. Debentures pair.)

- Disclosure. Shown under ``Other Long-Term Liabilities'' on the equity & liabilities side until redemption.

- On redemption. Dr. Debentures A/c; Dr. Premium on Redemption A/c; Cr. Debenture-holders A/c (later Cr. Bank on payment).

Premium on Redemption = Redemption Price - Face Value, paid extra at maturity. Liability recognised at issue; debited to Loss on Issue of Debentures.

Quick reading. Extra cash going out at maturity, but recognised upfront.

- Premium = Redemption - Face value.

- Liability shown until redemption.

- Forms part of Loss on Issue together with discount.

Why this matters. In a Class 12 numerical question on Issue and Redemption of Debentures, the examiner gives full marks only when the candidate distinguishes Discount on Issue of Debentures (a capital loss written off over the life of the debentures) from Premium on Redemption of Debentures (a provision created on issue), applies the Companies (Share Capital and Debentures) Rules 2014 for the Debenture Redemption Reserve, and presents every issue and redemption journal entry in narrated form. A correct closing debenture figure without the DRR working and the narrated journal entries loses 30-50 percent of the marks under the CBSE step-marking scheme.

Common mistakes. Three predictable slips lose marks: (a) confusing Discount on Issue with Premium on Redemption and posting both to the same ledger; (b) ignoring the requirement to create Debenture Redemption Reserve of at least 25 percent of the outstanding debentures before the start of redemption; (c) missing the loss on issue of debentures that arises when debentures are issued at par or discount but redeemed at a premium.

Extra payable at maturity; booked at issue; part of Loss on Issue.

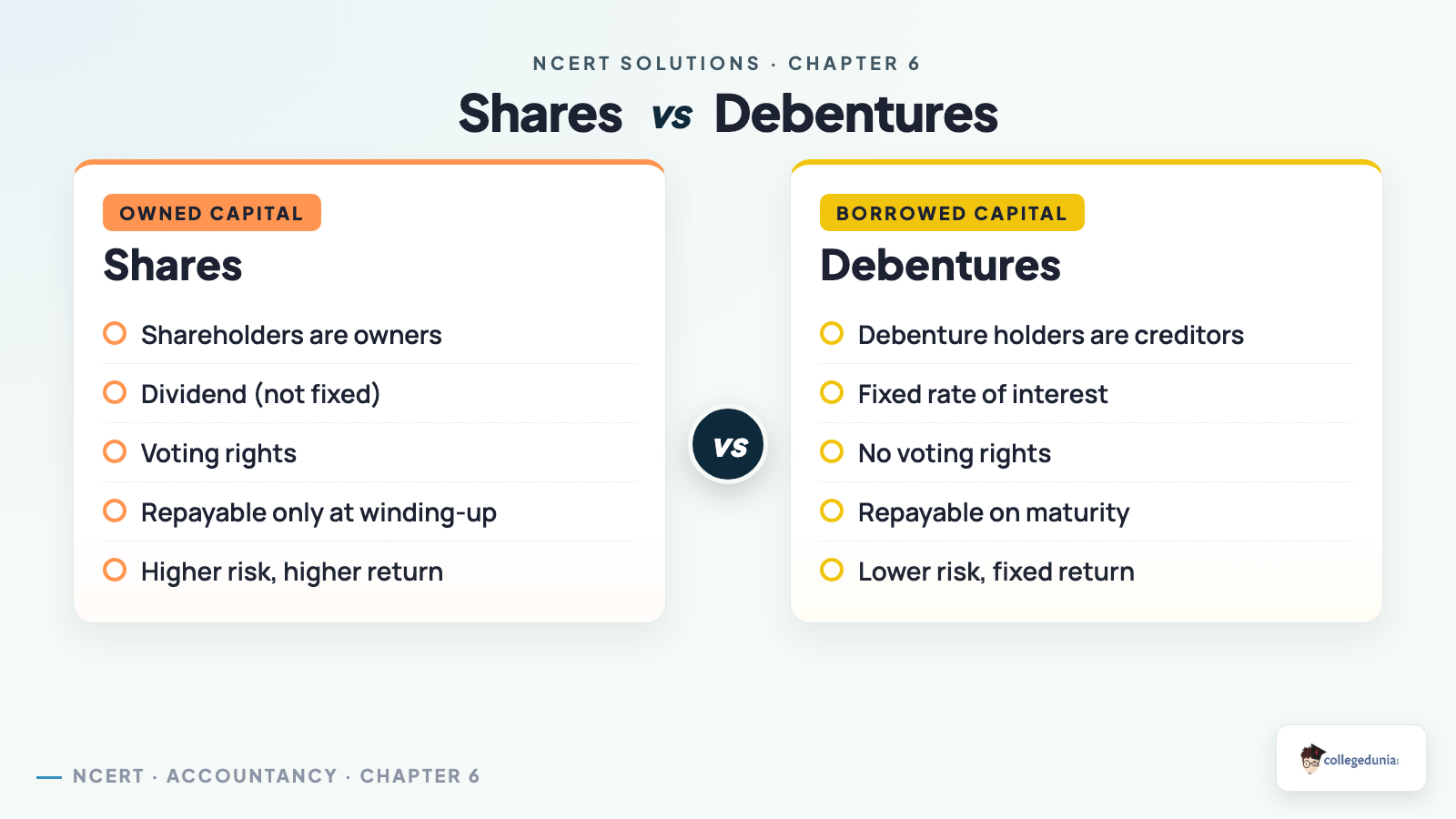

How debentures are different from shares? Give two points.

Concept used. Debentures and shares are the two main long-term financing instruments for a company. The fundamental distinction is the relationship they create: debenture → creditor; share → owner. The detailed differences follow.

- Ownership vs Creditorship. A shareholder is an owner of the company; a debenture-holder is a creditor. Owners receive dividend, creditors receive interest.

- Return. Dividend on shares is paid out of profits and is variable. Interest on debentures is a charge against profit (paid even if no profit) and is fixed.

- Repayment. Share capital is normally NOT repayable during the life of the company (except buy-back or preference share redemption). Debentures are repayable on a fixed date.

- Voting rights. Shareholders have voting rights at general meetings. Debenture- holders have no voting rights in general meetings (only in meetings of debenture-holders).

- Order of payment on winding-up. Debenture-holders are paid first (secured creditors); shareholders are paid last (residual claimants).

- Security. Debentures may be secured by a charge on assets; shares are never secured.

Two key points: (1) Shareholder = owner; debenture-holder = creditor; (2) Dividend on shares is paid only out of profits and is variable, while interest on debentures is a fixed charge paid even in loss years.

Strategic angle. Memorise the contrast as a 2-column table: owner/creditor, dividend/interest, profit-only/charge, voting/no-voting, repayable/not, last/first on liquidation.

- Shareholder = owner; debenture-holder = creditor.

- Dividend variable, paid from profits; interest fixed, paid always.

- Voting (shares) vs no voting (debentures).

Why this matters. In a Class 12 numerical question on Issue and Redemption of Debentures, the examiner gives full marks only when the candidate distinguishes Discount on Issue of Debentures (a capital loss written off over the life of the debentures) from Premium on Redemption of Debentures (a provision created on issue), applies the Companies (Share Capital and Debentures) Rules 2014 for the Debenture Redemption Reserve, and presents every issue and redemption journal entry in narrated form. A correct closing debenture figure without the DRR working and the narrated journal entries loses 30-50 percent of the marks under the CBSE step-marking scheme.

Common mistakes. Three predictable slips lose marks: (a) confusing Discount on Issue with Premium on Redemption and posting both to the same ledger; (b) ignoring the requirement to create Debenture Redemption Reserve of at least 25 percent of the outstanding debentures before the start of redemption; (c) missing the loss on issue of debentures that arises when debentures are issued at par or discount but redeemed at a premium.

Owner vs Creditor; Dividend vs Interest are the two anchor differences.

What is meant by redemption of debentures?

Concept used. Redemption of Debentures is the discharge of the company's liability towards debenture-holders, i.e. the repayment of the principal amount of the debentures on the maturity date (or earlier, depending on the terms of issue). Once redeemed, the debentures cease to exist as an obligation of the company.

- Trigger. Redemption takes place on the expiry of the period for which the debentures were issued, as per the terms of issue stated in the debenture trust deed.

- Modes of redemption. (a) Lump-sum at the end of the stated period; (b) in instalments (by annual drawings); (c) by purchase in the open market; (d) by conversion into shares or new debentures.

- Source of funds. (a) Out of capital (no profits transferred); (b) out of profits (a portion of revenue profits transferred to DRR); (c) by issue of new debentures / shares.

- Compliance. The company must comply with Section 71 of the Companies Act 2013 and Rule 18 of the Companies (Share Capital and Debentures) Rules 2014, including Debenture Redemption Reserve (DRR) and Debenture Redemption Investment (DRI).

Redemption of debentures = discharge of the company's debt to debenture-holders; done by lump-sum, instalments, open-market purchase or conversion; governed by Section 71 and Rule 18.

Quick reading. ``Paying back'' the debenture-holders. Triggered by the agreed maturity date; funded out of capital, out of profits, or by a new issue.

- Maturity date or early-redemption clause arrives.

- Pay holders by cash, by new debentures, by shares, or by open-market purchase.

- Comply with DRR / DRI rules.

Why this matters. In a Class 12 numerical question on Issue and Redemption of Debentures, the examiner gives full marks only when the candidate distinguishes Discount on Issue of Debentures (a capital loss written off over the life of the debentures) from Premium on Redemption of Debentures (a provision created on issue), applies the Companies (Share Capital and Debentures) Rules 2014 for the Debenture Redemption Reserve, and presents every issue and redemption journal entry in narrated form. A correct closing debenture figure without the DRR working and the narrated journal entries loses 30-50 percent of the marks under the CBSE step-marking scheme.

Common mistakes. Three predictable slips lose marks: (a) confusing Discount on Issue with Premium on Redemption and posting both to the same ledger; (b) ignoring the requirement to create Debenture Redemption Reserve of at least 25 percent of the outstanding debentures before the start of redemption; (c) missing the loss on issue of debentures that arises when debentures are issued at par or discount but redeemed at a premium.

Repayment of debenture liability on / before maturity; four modes; Section 71 governs.

Can the company purchase its own debentures?

Concept used. Yes. Unlike its own shares (where buy-back is governed by Section 68 restrictions), a company has a wider freedom to purchase its own debentures in the open market. Purpose: either to cancel them (early redemption) or to re-issue them later (treat as investment).

- Authority. The Articles of Association must authorise it; the debenture trust deed should not prohibit it.

- Two outcomes.

- Purchase for cancellation: debentures are cancelled immediately; any profit on cancellation (purchase price < face value) is credited to Capital Reserve.

- Purchase as investment: debentures are held by the company as ``Own Debentures A/c''; can be re-issued later or cancelled.

- No DRR transfer needed (Rule 18(7) exemption) when redemption is through open-market purchase for listed companies.

- Profit on cancellation. Profit = Face Value - Purchase Price (cum-int.).

Yes. A company can purchase its own debentures for cancellation (profit → Capital Reserve) or as investment (Own Debentures A/c). Authorised by Articles; subject to trust deed.

Quick reading. Yes, with two routes: cancel now or invest now and cancel later.

- Articles allow + trust deed silent.

- Cancel ⇒ profit to Capital Reserve.

- Hold as investment ⇒ Own Debentures A/c.

Why this matters. In a Class 12 numerical question on Issue and Redemption of Debentures, the examiner gives full marks only when the candidate distinguishes Discount on Issue of Debentures (a capital loss written off over the life of the debentures) from Premium on Redemption of Debentures (a provision created on issue), applies the Companies (Share Capital and Debentures) Rules 2014 for the Debenture Redemption Reserve, and presents every issue and redemption journal entry in narrated form. A correct closing debenture figure without the DRR working and the narrated journal entries loses 30-50 percent of the marks under the CBSE step-marking scheme.

Common mistakes. Three predictable slips lose marks: (a) confusing Discount on Issue with Premium on Redemption and posting both to the same ledger; (b) ignoring the requirement to create Debenture Redemption Reserve of at least 25 percent of the outstanding debentures before the start of redemption; (c) missing the loss on issue of debentures that arises when debentures are issued at par or discount but redeemed at a premium.

Yes; cancel or invest; profit on cancellation → Capital Reserve.

What is meant by redemption of debentures by conversion?

Concept used. Redemption by Conversion is the discharge of debenture liability by issuing new equity shares (or new debentures) to the existing debenture-holders in lieu of cash. No cash flows out; the debt is simply converted into another instrument.

- When permissible. The option to convert must be present at the time of issue (CCD, OCD, FCD, PCD).

- Number of shares issued. No. of new shares = Amount Payable on RedemptionIssue Price of New Share. If the new share is at par, denominator = face value; if at premium, denominator = face + premium.

- Journal entry.

- Dr. Debentures A/c (face value being redeemed).

- Dr. Premium on Redemption of Debentures A/c (if redeemable at premium).

- Cr. Equity / Preference Share Capital A/c (face value of new shares).

- Cr. Securities Premium Reserve A/c (if shares issued at premium).

- No DRR required. Because no cash leaves the company, DRR is not required for convertible portion.

Redemption by conversion = debenture-holders accept new shares (or new debentures) instead of cash. No cash outflow; no DRR. Number of shares = Amount Payable ÷ New Share Issue Price.

Strategic angle. Swap debt for equity. No cash, no DRR.

- Conversion price fixed at issue.

- Number of new shares = amount payable / share issue price.

- Premium portion (if any) to Securities Premium Reserve.

Why this matters. In a Class 12 numerical question on Issue and Redemption of Debentures, the examiner gives full marks only when the candidate distinguishes Discount on Issue of Debentures (a capital loss written off over the life of the debentures) from Premium on Redemption of Debentures (a provision created on issue), applies the Companies (Share Capital and Debentures) Rules 2014 for the Debenture Redemption Reserve, and presents every issue and redemption journal entry in narrated form. A correct closing debenture figure without the DRR working and the narrated journal entries loses 30-50 percent of the marks under the CBSE step-marking scheme.

Common mistakes. Three predictable slips lose marks: (a) confusing Discount on Issue with Premium on Redemption and posting both to the same ledger; (b) ignoring the requirement to create Debenture Redemption Reserve of at least 25 percent of the outstanding debentures before the start of redemption; (c) missing the loss on issue of debentures that arises when debentures are issued at par or discount but redeemed at a premium.

Debt → equity swap; cash-free; DRR not needed.

How would you deal with `Premium on Redemption of Debentures'?

Concept used. The accounting treatment of Premium on Redemption of Debentures splits into two events: (a) recognition at the time of issue (as a liability), and (b) extinguishment at the time of redemption (paying it out together with face value).

- At time of issue (premium is known from day one).

- Dr. Loss on Issue of Debentures A/c (with discount + premium on redemption).

- Cr. Premium on Redemption of Debentures A/c (with premium amount).

- (The standard Dr. Bank, Cr. Debentures is passed separately.)

- Write-off the Loss. Loss on Issue of Debentures is written off against Securities Premium Reserve first (under Section 52, Companies Act 2013), and any balance against Statement of Profit & Loss over the life of the debentures.

- Disclosure during life. Premium on Redemption of Debentures A/c is shown under ``Other Long-Term Liabilities'' (Schedule III, Part I).

- At time of redemption.

- Dr. Debentures A/c (face value); Dr. Premium on Redemption of Debentures A/c (premium amount); Cr. Debenture-holders A/c (face + premium).

- Dr. Debenture-holders A/c; Cr. Bank A/c (final settlement).

Premium on Redemption is recognised at issue (Dr. Loss on Issue, Cr. Premium on Redemption A/c), shown as a long-term liability, written off against Securities Premium / P&L, and finally paid out at redemption together with face value.

Quick reading. Three steps: book at issue, write off the loss over life, pay at maturity.

- Issue: Dr. Loss on Issue, Cr. Premium on Redemption A/c.

- Life: write off Loss against Securities Premium / P&L.

- Redemption: Dr. Debentures & Dr. Premium on Redemption; Cr. Bank.

Why this matters. In a Class 12 numerical question on Issue and Redemption of Debentures, the examiner gives full marks only when the candidate distinguishes Discount on Issue of Debentures (a capital loss written off over the life of the debentures) from Premium on Redemption of Debentures (a provision created on issue), applies the Companies (Share Capital and Debentures) Rules 2014 for the Debenture Redemption Reserve, and presents every issue and redemption journal entry in narrated form. A correct closing debenture figure without the DRR working and the narrated journal entries loses 30-50 percent of the marks under the CBSE step-marking scheme.

Common mistakes. Three predictable slips lose marks: (a) confusing Discount on Issue with Premium on Redemption and posting both to the same ledger; (b) ignoring the requirement to create Debenture Redemption Reserve of at least 25 percent of the outstanding debentures before the start of redemption; (c) missing the loss on issue of debentures that arises when debentures are issued at par or discount but redeemed at a premium.

Book at issue → write off over life → pay at maturity.

What is meant by redemption of debentures by ``Purchase in Open Market''?

Concept used. Redemption by Purchase in the Open Market is the practice of a company buying its own debentures from the stock market at the prevailing market price (rather than at the agreed redemption price). It is permitted only if (a) Articles authorise and (b) trust deed does not prohibit.

- Motivation. The company resorts to open-market purchase when the market price of its own debentures is BELOW the face / redemption value: the company saves money.

- Two intentions.

- Purchase for immediate cancellation: the debentures are cancelled then and there; profit = face value - purchase price; credited to Capital Reserve.

- Purchase as investment: debentures are held in ``Own Debentures A/c''; may be re-issued later or cancelled.

- Profit on cancellation entry.

- Dr. Debentures A/c (Face Value).

- Cr. Bank A/c (Purchase Price ex-interest).

- Cr. Capital Reserve A/c (Face - Purchase Price).

- Cum-int. vs ex-int. If purchased cum-interest, the price includes accrued interest, which must be separated: Dr. Interest A/c with the accrued portion. If ex-interest, the price is clean.

Open-market purchase = company buys its own debentures from the market, usually below face value, for cancellation (profit → Capital Reserve) or as investment (Own Debentures A/c). Subject to Articles and trust deed.

Strategic angle. Use it when own debentures trade at a discount in the market; capture the saving as Capital Reserve.

- Authority: Articles permit + trust deed silent.

- Cum-int. vs ex-int. price split.

- Cancel ⇒ profit to Capital Reserve; Invest ⇒ Own Debentures A/c.

Why this matters. In a Class 12 numerical question on Issue and Redemption of Debentures, the examiner gives full marks only when the candidate distinguishes Discount on Issue of Debentures (a capital loss written off over the life of the debentures) from Premium on Redemption of Debentures (a provision created on issue), applies the Companies (Share Capital and Debentures) Rules 2014 for the Debenture Redemption Reserve, and presents every issue and redemption journal entry in narrated form. A correct closing debenture figure without the DRR working and the narrated journal entries loses 30-50 percent of the marks under the CBSE step-marking scheme.

Common mistakes. Three predictable slips lose marks: (a) confusing Discount on Issue with Premium on Redemption and posting both to the same ledger; (b) ignoring the requirement to create Debenture Redemption Reserve of at least 25 percent of the outstanding debentures before the start of redemption; (c) missing the loss on issue of debentures that arises when debentures are issued at par or discount but redeemed at a premium.

Buy own debentures from market; cancel or invest; profit to Capital Reserve.

Explain the different types of debentures.

Concept used. Debentures are classified along four independent axes: (a) security cover, (b) repayability, (c) records / mode of transfer, and (d) convertibility into shares. A single debenture can have one label from each axis (e.g. ``Secured, Redeemable, Registered, Non-Convertible'').

- From the point of view of security.

- Secured / Mortgaged Debentures. Carry a fixed charge (on a specific asset) or a floating charge (on all assets) registered under Section 77.

- Unsecured / Naked Debentures. Carry no charge; only a personal undertaking of the company to repay.

- From the point of view of repayment / tenure.

- Redeemable Debentures. Repayable on a fixed maturity date or in instalments by drawings.

- Irredeemable / Perpetual Debentures. No fixed maturity; repayable only on winding-up. (Banned in India after April 1, 2014, under Section 71(4).)

- From the point of view of records of transfer.

- Registered Debentures. Holder's name is on the register; transfer by a transfer deed and entry in register.

- Bearer Debentures. No register; transferable by mere delivery; interest paid against detachable coupons.

- From the point of view of convertibility.

- Convertible Debentures (CD). Convertible into equity shares after a stated period. Sub-types: Fully Convertible (FCD), Partly Convertible (PCD), Compulsorily Convertible (CCD), Optionally Convertible (OCD).

- Non-Convertible Debentures (NCD). Not convertible; redeemed in cash.

- Other types (occasionally examined).

- First Debentures vs Second Debentures (priority of repayment).

- Zero-Coupon Debentures (no periodic interest; issued at deep discount, redeemed at face value).

- Collateral Debentures (issued as a back-up cover for a loan).

Debentures are classified along four axes: Security (Secured / Naked), Repayability (Redeemable / Irredeemable), Records (Registered / Bearer), Convertibility (Convertible / NCD). Additional types: First/Second, Zero-coupon, Collateral.

Strategic angle. Four independent classification axes; each debenture is one tag from each axis ⇒ 2 × 2 × 2 × 2 = 16 possible label combinations in principle.

- Security → Secured / Naked.

- Repayability → Redeemable / Irredeemable.

- Records → Registered / Bearer.

- Convertibility → Convertible / Non-Convertible.

- Bonus categories: Zero-coupon, Collateral, First/Second.

Why this matters. In a Class 12 numerical question on Issue and Redemption of Debentures, the examiner gives full marks only when the candidate distinguishes Discount on Issue of Debentures (a capital loss written off over the life of the debentures) from Premium on Redemption of Debentures (a provision created on issue), applies the Companies (Share Capital and Debentures) Rules 2014 for the Debenture Redemption Reserve, and presents every issue and redemption journal entry in narrated form. A correct closing debenture figure without the DRR working and the narrated journal entries loses 30-50 percent of the marks under the CBSE step-marking scheme.

Common mistakes. Three predictable slips lose marks: (a) confusing Discount on Issue with Premium on Redemption and posting both to the same ledger; (b) ignoring the requirement to create Debenture Redemption Reserve of at least 25 percent of the outstanding debentures before the start of redemption; (c) missing the loss on issue of debentures that arises when debentures are issued at par or discount but redeemed at a premium.

Four axes: Security, Repayability, Records, Convertibility. Plus Zero-coupon and Collateral as bonus categories.

Distinguish between a debenture and a share. Why debenture is known as loan capital? Explain.

Concept used. Debentures and shares are the two main long-term sources of funds. They differ on ownership, return, security, voting rights, repayment and order of payment on winding-up. Debentures are called loan capital because they create a creditor-debtor relationship: the holder lends money to the company, and the company is bound to repay it.

- Distinction (table).

1.25 tabularp0.30|p0.30|p0.30

Basis & Debenture & Share

Relationship & Creditor of the company & Owner of the company

Return & Interest (fixed; charge on profit) & Dividend (variable; out of profit)

Voting rights & None & Yes, at general meetings

Repayment & Repaid on maturity (or earlier) & Not repayable during company's life

Security & May be secured by a charge & Never secured

On winding-up & Paid first (secured creditors) & Paid last (residual claim)

Convertibility & May be convertible into shares & Cannot be converted into debentures

Tax treatment & Interest is tax-deductible expense & Dividend is paid out of post-tax profit

tabular - Why ``loan capital''? A debenture represents money borrowed by the

company under a contract. The salient features that make it loan capital:

- Acknowledgement of debt (Section 2(30)).

- Fixed rate of interest, payable regardless of profit.

- Definite redemption date.

- Holder ranks as a creditor, paid before owners on winding-up.

- Charge on assets is permissible (security cover).

Debenture creates a creditor relationship with fixed interest and definite repayment; share creates ownership with variable dividend and no repayment. Debentures are ``loan capital'' because they are in effect a long-term loan in marketable certificate form.

Strategic angle. Owner vs creditor is the master distinction. The debenture's promise to repay is the reason it is ``loan'' capital, just packaged as a tradeable security.

- Distinguish on six points: relationship, return, voting, repayment, security, priority on winding-up.

- Debenture is loan because: fixed interest, fixed maturity, creditor status, charge permissible.

- Difference from ordinary loan: tradeable on stock exchange; can be held by the public.

Why this matters. In a Class 12 numerical question on Issue and Redemption of Debentures, the examiner gives full marks only when the candidate distinguishes Discount on Issue of Debentures (a capital loss written off over the life of the debentures) from Premium on Redemption of Debentures (a provision created on issue), applies the Companies (Share Capital and Debentures) Rules 2014 for the Debenture Redemption Reserve, and presents every issue and redemption journal entry in narrated form. A correct closing debenture figure without the DRR working and the narrated journal entries loses 30-50 percent of the marks under the CBSE step-marking scheme.

Common mistakes. Three predictable slips lose marks: (a) confusing Discount on Issue with Premium on Redemption and posting both to the same ledger; (b) ignoring the requirement to create Debenture Redemption Reserve of at least 25 percent of the outstanding debentures before the start of redemption; (c) missing the loss on issue of debentures that arises when debentures are issued at par or discount but redeemed at a premium.

Loan with a marketable certificate; creditor status with fixed return and definite maturity.

Describe the meaning of `Debenture Issued as Collateral Securities'. What accounting treatment is given to the issue of debentures in the books of accounts?

Concept used. Debentures issued as collateral security are debentures issued as an additional (back-up) cover for a loan or bank overdraft. They are dormant: no cash is received, no interest is paid, and they are activated only if the company defaults on the principal loan. There are TWO accepted methods of accounting for them.

- Meaning. The company borrows say Rs. 10,00,000 from a bank, pledges its primary stock-in-trade, and ALSO issues 12,000 debentures of Rs. 100 each (face value Rs. 12,00,000) as additional cover. The bank holds these debentures; they are contingent until default.

- Method 1: No journal entry (memorandum only). Since the company has neither

received money for them nor incurred any obligation to pay interest, no entry is passed.

A note is made in the balance sheet under the loan:

Bank Loan: Rs. 10,00,000

(Secured by issue of Rs. 12,00,000, 10% Debentures as collateral security) - Method 2: Journal entry passed. The full nominal value of the collateral

debentures is recognised, balanced by a Debenture Suspense A/c:

- Dr. Debenture Suspense A/c 12,00,000 (with face value).

- Cr. Debentures A/c 12,00,000 (with face value).

- On default. If the company defaults, the bank exercises its security and the debentures become like ordinary debentures: cash flow begins (or assets sold).

- On repayment of loan. The collateral debentures are returned and cancelled: Dr. Debentures A/c; Cr. Debenture Suspense A/c.

Collateral debentures are back-up cover for a loan: no cash received, no interest paid. Method 1: no entry, only a note. Method 2: Dr. Debenture Suspense; Cr. Debentures (offset on balance sheet). On loan repayment, reverse the entry.

Strategic angle. Two methods, two presentations. Method 2 brings the collateral debentures onto the books symmetrically; Method 1 keeps them off the books with a memo.

- Method 1: only a note under the loan in BS.

- Method 2: Dr. Debenture Suspense; Cr. Debentures (face value).

- In BS, Debenture Suspense = deduction from Debentures ⇒ net zero.

- Loan repaid ⇒ reverse the entry; debentures cancelled.

Why this matters. In a Class 12 numerical question on Issue and Redemption of Debentures, the examiner gives full marks only when the candidate distinguishes Discount on Issue of Debentures (a capital loss written off over the life of the debentures) from Premium on Redemption of Debentures (a provision created on issue), applies the Companies (Share Capital and Debentures) Rules 2014 for the Debenture Redemption Reserve, and presents every issue and redemption journal entry in narrated form. A correct closing debenture figure without the DRR working and the narrated journal entries loses 30-50 percent of the marks under the CBSE step-marking scheme.

Common mistakes. Three predictable slips lose marks: (a) confusing Discount on Issue with Premium on Redemption and posting both to the same ledger; (b) ignoring the requirement to create Debenture Redemption Reserve of at least 25 percent of the outstanding debentures before the start of redemption; (c) missing the loss on issue of debentures that arises when debentures are issued at par or discount but redeemed at a premium.

Memo OR Suspense-and-Debenture journal; both end at net zero on BS.

Explain the different terms for the issue of debentures with reference to their redemption.

Concept used. Debentures can be issued and redeemed at different combinations of premium, par and discount. The six possible permutations are usually grouped into six standard cases. The accounting differs only in (a) the amount of cash received at issue and (b) the amount of cash paid at redemption; the face value (Debentures A/c) is always credited with the nominal amount.

- Case 1: Issued at par, redeemable at par.

Cash in = face; cash out = face. No premium / discount.

Issue entry: Dr. Bank; Cr. Debentures. - Case 2: Issued at premium, redeemable at par.

Cash in > face; the surplus → Securities Premium Reserve.

Dr. Bank (issue price); Cr. Debentures (face); Cr. Securities Premium Reserve (premium). - Case 3: Issued at discount, redeemable at par.

Cash in < face; the shortfall → Discount on Issue of Debentures A/c (capital loss,

amortised).

Dr. Bank (issue price); Dr. Discount on Issue (discount); Cr. Debentures (face). - Case 4: Issued at par, redeemable at premium.

Cash in = face; cash out > face. The future premium → Loss on Issue, with credit

to Premium on Redemption A/c (liability).

Dr. Bank (face); Dr. Loss on Issue (premium on redemption); Cr. Debentures (face); Cr. Premium on Redemption (premium). - Case 5: Issued at premium, redeemable at premium.

Cash in > face; cash out > face. Both legs recorded.

Dr. Bank (issue price); Dr. Loss on Issue (premium on redemption); Cr. Debentures (face); Cr. Securities Premium (issue premium); Cr. Premium on Redemption (redemption premium). - Case 6: Issued at discount, redeemable at premium.

Double loss: cash in < face AND cash out > face.

Dr. Bank (issue price); Dr. Loss on Issue (discount + redemption premium); Cr. Debentures (face); Cr. Premium on Redemption (premium).

Six terms cover all combinations of issue (par / premium / discount) and redemption (par / premium). Case 6 (discount + premium) is the double loss; Case 1 (par + par) is the simplest.

Strategic angle. The matrix has six cells. Memorise: Discount → Loss; Premium at issue → Securities Premium; Premium on redemption → Loss on Issue with Premium on Redemption as liability.

- Six cases = 3 issue prices × 2 redemption prices.

- All six credit Debentures at face value.

- Discount and Premium on Redemption ⇒ Loss on Issue; written off over life.

Why this matters. In a Class 12 numerical question on Issue and Redemption of Debentures, the examiner gives full marks only when the candidate distinguishes Discount on Issue of Debentures (a capital loss written off over the life of the debentures) from Premium on Redemption of Debentures (a provision created on issue), applies the Companies (Share Capital and Debentures) Rules 2014 for the Debenture Redemption Reserve, and presents every issue and redemption journal entry in narrated form. A correct closing debenture figure without the DRR working and the narrated journal entries loses 30-50 percent of the marks under the CBSE step-marking scheme.

Common mistakes. Three predictable slips lose marks: (a) confusing Discount on Issue with Premium on Redemption and posting both to the same ledger; (b) ignoring the requirement to create Debenture Redemption Reserve of at least 25 percent of the outstanding debentures before the start of redemption; (c) missing the loss on issue of debentures that arises when debentures are issued at par or discount but redeemed at a premium.

Six cases; Debentures always credited at face; losses to Loss on Issue, premia to Securities Premium / Premium on Redemption.

Differentiate between redemption of debentures out of capital and out of profits.

Concept used. Redemption out of capital means redeeming debentures without transferring any amount from profits to a Debenture Redemption Reserve (DRR); the company's divisible profits remain unaffected by the redemption. Redemption out of profits means transferring an amount equal to (or part of) the nominal value of debentures from the Surplus in Statement of Profit & Loss to Debenture Redemption Reserve (DRR) before redemption, so that the profits available for dividend stand reduced.

- Out of capital (no DRR transfer beyond statutory minimum).

- Cash for redemption is paid out of working capital; no permanent restriction on divisible profits.

- Pre-amendment (before Rule 18(7), 2014), only companies meeting specific conditions could redeem entirely out of capital.

- Statutorily, DRR may still be required for the minimum percentage (e.g. 10% for non-listed non-NBFC public companies) under Rule 18(7).

- Out of profits (full DRR build-up).

- An amount equal to 100% of nominal value of debentures was traditionally transferred from P&L Surplus to DRR before redemption, locking those profits out of dividend.

- Conservative; protects creditors by ring-fencing internal cash for redemption.

- Distinguishing table.

1.25 tabularp0.32|p0.30|p0.30 Basis & Out of Capital & Out of Profits

DRR transfer & Only the statutory minimum & 100% of nominal value

Impact on divisible profits & No restriction & Profits locked in DRR; not available for dividend

Effect on creditors & Less cushion & Stronger cushion

Source of cash & Working capital & Operating profits set aside

Typical user & Companies with strong cash flow & Companies wanting to protect creditors

tabular - Current law (Rule 18(7), Companies Act 2013, as amended in 2019). DRR is now NOT required for listed companies, NBFCs registered with RBI, and HFCs registered with NHB; for other public companies, DRR = 10% of outstanding debentures.

Out of capital = no full DRR transfer, divisible profits unaffected. Out of profits = 100% transfer to DRR, profits locked. Post-2019 amendment, DRR is exempted for listed companies, NBFCs and HFCs; 10% for other public companies.

Strategic angle. The split between ``out of capital'' and ``out of profits'' is mostly historical; post-2019, the DRR landscape has been liberalised. Still examined in NCERT.

- Out of capital: divisible profits intact; DRR only at statutory minimum.

- Out of profits: full DRR; creditors protected.

- Post-2019: DRR slashed to 10% for unlisted public companies; nil for listed / NBFC / HFC.

Why this matters. In a Class 12 numerical question on Issue and Redemption of Debentures, the examiner gives full marks only when the candidate distinguishes Discount on Issue of Debentures (a capital loss written off over the life of the debentures) from Premium on Redemption of Debentures (a provision created on issue), applies the Companies (Share Capital and Debentures) Rules 2014 for the Debenture Redemption Reserve, and presents every issue and redemption journal entry in narrated form. A correct closing debenture figure without the DRR working and the narrated journal entries loses 30-50 percent of the marks under the CBSE step-marking scheme.

Common mistakes. Three predictable slips lose marks: (a) confusing Discount on Issue with Premium on Redemption and posting both to the same ledger; (b) ignoring the requirement to create Debenture Redemption Reserve of at least 25 percent of the outstanding debentures before the start of redemption; (c) missing the loss on issue of debentures that arises when debentures are issued at par or discount but redeemed at a premium.

Out of capital = no DRR; out of profits = full DRR. Current rule: 10% (others), nil (listed / NBFC / HFC).

Explain the guidelines of SEBI for creating Debenture Redemption Reserve.

Concept used. The Debenture Redemption Reserve (DRR) is a reserve created out of profits to ensure the company has funds for redemption of debentures. It is governed by Section 71(4) of the Companies Act 2013 read with Rule 18(7) of the Companies (Share Capital and Debentures) Rules 2014, as amended by Notification G.S.R. 574(E) dated August 16, 2019. SEBI's role is in addition: SEBI (Issue and Listing of Non-Convertible Securities) Regulations 2021 set out additional disclosure requirements for listed issues.

- Adequacy. DRR shall be created out of profits of the company available for payment of dividend.

- Quantum (post-Aug 2019 amendment).

- All listed companies (whether public issue or private placement): DRR not required.

- All unlisted NBFCs / HFCs registered with RBI / NHB: DRR not required.

- Other unlisted companies (non-NBFC / non-HFC public companies): DRR = 10% of value of outstanding debentures.

- Debenture Redemption Investment (DRI) – Rule 18(7)(c). Every company required to create DRR shall, on or before the 30th day of April in each year, invest or deposit a sum which shall not be less than 15% of the amount of debentures maturing during the year ending on the 31st day of March of the next year in specified securities (e.g. deposits with scheduled banks, government securities, bonds of public financial institutions).

- Use. The DRR amount can be used only for the purpose of redemption of debentures; not for any other purpose.

- Transfer post-redemption. On full redemption, the balance in DRR may be transferred to the General Reserve.

Post-2019: DRR is NIL for listed companies, NBFCs and HFCs; 10% of outstanding debentures for other unlisted public companies. Plus, every DRR-required company must invest 15% of debentures maturing in the year by April 30 in specified securities (DRI).

Quick reading. Two numbers: 10% (DRR) and 15% (DRI). Listed companies are entirely exempt from DRR after the 2019 amendment.

- DRR = 10% of outstanding debentures (unlisted non-NBFC public co.).

- DRI = 15% of debentures maturing in that year, deposited by April 30.

- Listed / NBFC / HFC: no DRR.

Why this matters. In a Class 12 numerical question on Issue and Redemption of Debentures, the examiner gives full marks only when the candidate distinguishes Discount on Issue of Debentures (a capital loss written off over the life of the debentures) from Premium on Redemption of Debentures (a provision created on issue), applies the Companies (Share Capital and Debentures) Rules 2014 for the Debenture Redemption Reserve, and presents every issue and redemption journal entry in narrated form. A correct closing debenture figure without the DRR working and the narrated journal entries loses 30-50 percent of the marks under the CBSE step-marking scheme.

Common mistakes. Three predictable slips lose marks: (a) confusing Discount on Issue with Premium on Redemption and posting both to the same ledger; (b) ignoring the requirement to create Debenture Redemption Reserve of at least 25 percent of the outstanding debentures before the start of redemption; (c) missing the loss on issue of debentures that arises when debentures are issued at par or discount but redeemed at a premium.

10% DRR (others), nil (listed / NBFC / HFC); 15% DRI by April 30 of redemption year.

Describe the steps for creating Sinking Fund for redemption of debentures.