The NCERT Class 12 Accountancy Book PDF Chapter 2 Reconstitution of a Partnership Firm: Admission of a Partner runs to 89 pages, making it the longest chapter in the Class 12 Accountancy Part A syllabus. It is also the highest-scoring topic in the CBSE board paper, with at least one 6-mark or 8-mark journal-entry problem appearing every single session since 2018. This page hosts the original NCERT Reprint 2026-27 chapter PDF for free download.

- CBSE Weightage: 8 to 10 marks (Part A: Accounting for Partnership Firms and Companies)

Chapter 2 spans sections 2.1 to 2.7, packs in 23 solved illustrations, and closes with 6 Short Answer, 8 Long Answer and 35 Numerical Questions for Practice.

The PDF is the unmodified NCERT chapter file, aligned to the 2026-27 academic session and reprinted in April 2025 by the National Council of Educational Research and Training.

Also Check:

- Class 12 Accountancy Chapter 2 NCERT Solutions

- Class 12 Accountancy Chapter 2 NCERT Notes

- Chapter 3 NCERT Book PDF: Retirement or Death of a Partner

Chapter 2 Quick Stats: What the PDF Contains

The table below summarises the structural shape of the chapter so you know what you are downloading. Numbers are taken directly from the printed 2026-27 reprint.

| Element | Count or Detail |

|---|---|

| Total pages | 89 |

| Main sections (2.1 to 2.7) | 7 |

| Solved illustrations | 23 |

| Short Answer Questions | 6 |

| Long Answer Questions | 8 |

| Numerical Questions for Practice | 35 |

| Test Your Understanding boxes | 2 (I and II) |

| Goodwill valuation methods covered | 3 (Average Profit, Super Profit, Capitalisation) |

| Standard referenced | AS-26 (Intangible Assets) |

Reconstitution of a Partnership Firm Admission of a Partner Video C...

Source: Commerce Wallah by PW on YouTube

Class 12 Accountancy Chapter 2 Topics: Section by Section

Chapter 2 is built around five accounting consequences that follow when a new partner is admitted. Every CBSE question on this chapter tests at least one of them.

- Section 2.1 Modes of Reconstitution: change in profit-sharing ratio, admission, retirement or death, and dissolution. Reconstitution preserves the firm; dissolution ends it.

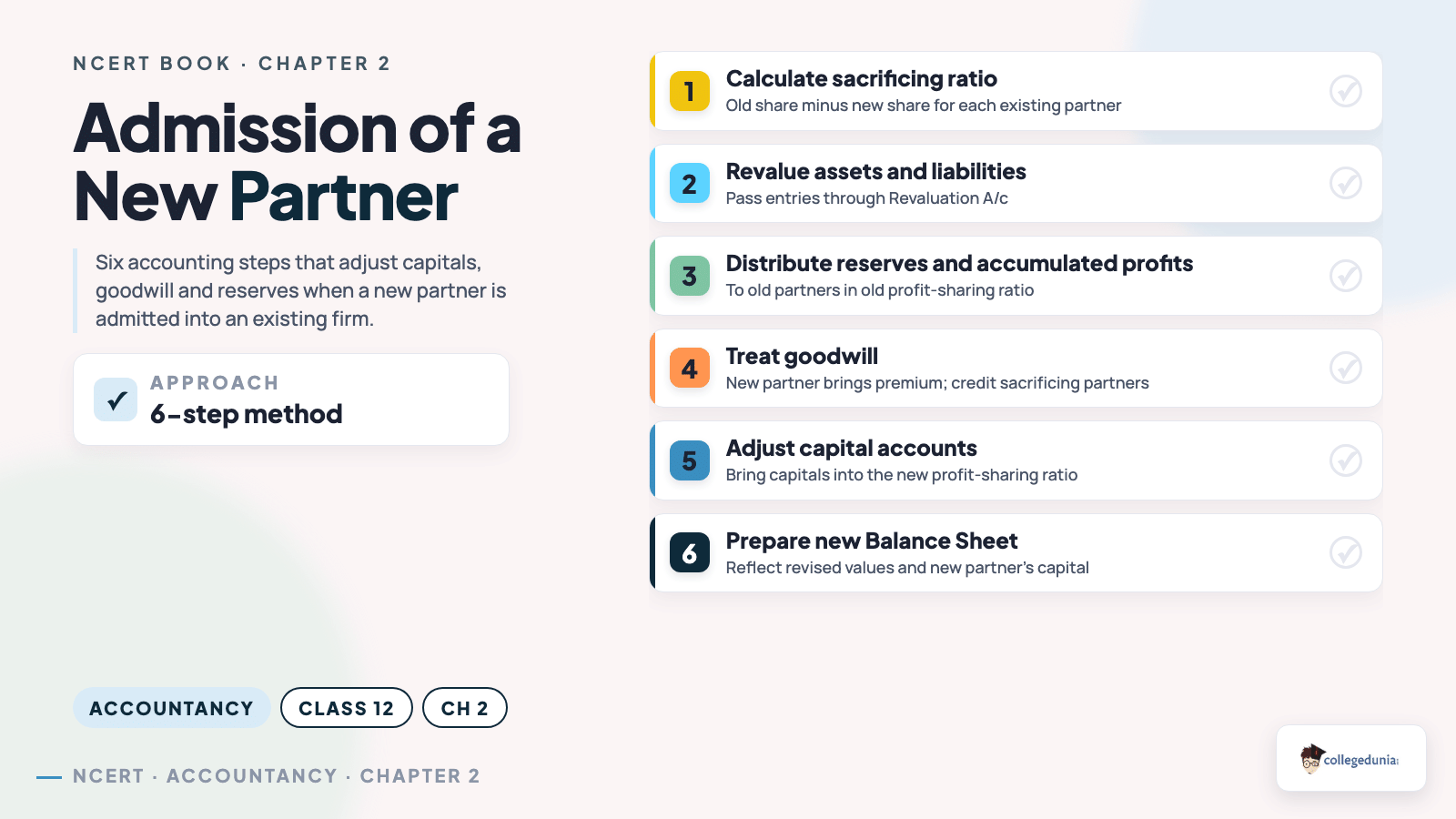

- Section 2.2 Admission of a New Partner: the five matters needing adjustment, new ratio, sacrificing ratio, goodwill, revaluation, accumulated reserves, and capital adjustment.

- Section 2.3 New Profit Sharing Ratio and Sacrificing Ratio: the formula Sacrificing Ratio = Old Ratio − New Ratio with five worked variants.

- Section 2.4 Goodwill: Nature and Valuation: AS-26 treatment, factors affecting goodwill, and the three valuation methods.

- Section 2.5 Treatment of Goodwill on Admission: premium method, hidden goodwill, and writing off any existing goodwill before admission.

- Section 2.6 Revaluation of Assets and Reassessment of Liabilities: Revaluation A/c format and the rule that revaluation profit or loss belongs to old partners only.

- Section 2.7 Adjustment of Capitals: two routes, capitals on the basis of the new partner's capital, or new partner's capital on the basis of old capitals.

How Will Collegedunia's Class 12 Accountancy Chapter 2 Resources Help You?

Collegedunia hosts the official NCERT PDF plus a stack of derived study material aimed at the CBSE Class 12 board paper. The PDF on this page is the textbook itself; the linked Solutions and Notes pages take the textbook content forward.

- Verbatim NCERT print: the same file CBSE schools issue, with no paraphrasing or layout changes.

- 2026-27 reprint: the April 2025 reprint, so the AS-26 reference and the rationalisation note are current.

- Pairs with Solutions and Notes: read the chapter here, then jump to the worked solutions for the 35 numerical questions, then revise from the chapter notes before the exam.

Goodwill Valuation Methods: A Snapshot from Chapter 2

Section 2.4 is the most examined area of Chapter 2. The table lists the three valuation formulas exactly as the textbook prints them.

| Method | Formula | When the Question Uses It |

|---|---|---|

| Average Profit | Goodwill = Average Profit × Number of years' purchase | Default method when only past profits are given. |

| Super Profit | Goodwill = Super Profit × Number of years' purchase, where Super Profit = Actual Average Profit − Normal Profit | Used when normal rate of return is given. |

| Capitalisation | Goodwill = Capitalised Value of Average Profit − Net Assets, OR Goodwill = Super Profit × (100 / Normal Rate) | Used when the question gives the normal rate and the capital employed. |

Full formula sheet: Class 12 Accountancy Chapter 2 Formula Sheet.

Class 12 Accountancy Chapter 2 PYQ Trends in CBSE Board Exams

Admission of a Partner has carried a multi-part numerical in every CBSE Class 12 Accountancy paper for the last six years. The table tracks the dominant sub-topic per session.

| Year | Dominant Sub-Topic | Marks |

|---|---|---|

| 2025 | Goodwill, premium method + Revaluation A/c | 8 |

| 2024 | Sacrificing ratio + capital adjustment | 6 |

| 2023 | Hidden goodwill | 6 |

| 2022 | Revaluation A/c + reserves treatment | 8 |

| 2021 | Admission with goodwill premium | 6 |

Admission and Retirement together account for nearly one-third of the CBSE Class 12 Accountancy paper.

Key Features of the Official NCERT Reprint 2026-27

- CBSE board authority: every Class 12 Accountancy board question is set from this textbook.

- Stream coverage: the chapter is also the foundational reading for CA Foundation, CMA Foundation and B.Com first year.

- AS-26 alignment: the goodwill section explicitly references Accounting Standard 26 on Intangible Assets, the version examiners expect students to quote.

- Free and public domain: the file is published under NCERT's open educational licence.

Related Resources

- Class 12 Accountancy Chapter 2 NCERT Solutions

- Class 12 Accountancy Chapter 2 NCERT Notes

- Class 12 Accountancy Chapter 2 Formula Sheet

- Class 12 Accountancy Chapter 2 Handwritten Notes

NCERT Book PDF for Class 12 Accountancy: All Chapters

The Class 12 Accountancy syllabus is split across two parts. Part A covers partnership and company accounts; Part B covers analysis of financial statements. The table below routes you to every chapter PDF.

| Chapter | NCERT Book PDF |

|---|---|

| Chapter 1 | Accounting for Partnership: Basic Concepts NCERT Book PDF |

| Chapter 3 | Retirement or Death of a Partner NCERT Book PDF |

| Chapter 4 | Dissolution of Partnership Firm NCERT Book PDF |

| Chapter 5 | Accounting for Share Capital NCERT Book PDF |

| Chapter 6 | Issue and Redemption of Debentures NCERT Book PDF |

| Chapter 7 | Financial Statements of a Company NCERT Book PDF |

| Chapter 8 | Analysis of Financial Statements NCERT Book PDF |

| Chapter 9 | Accounting Ratios NCERT Book PDF |

| Chapter 10 | Cash Flow Statement NCERT Book PDF |

Frequently Asked Questions

Ques. How many pages is NCERT Class 12 Accountancy Chapter 2 Admission of a Partner?

Ans.

The chapter runs to 89 pages in the NCERT Reprint 2026-27, making it the longest chapter in the Class 12 Accountancy Part A syllabus.

Ques. Is this the official NCERT Class 12 Accountancy textbook PDF?

Ans.

Yes. The file on this page is the unmodified NCERT Class 12 Accountancy Part A Chapter 2, Reprint 2026-27, published by NCERT and released for free public download.

Ques. What topics are covered in Chapter 2 Admission of a Partner?

Ans.

Sections 2.1 to 2.7 cover modes of reconstitution, the five adjustments on admission, new and sacrificing ratio, goodwill (AS-26, three valuation methods), Revaluation A/c, treatment of accumulated reserves, and capital adjustment.

Ques. How many illustrations and practice questions are in the chapter?

Ans.

The chapter has 23 solved illustrations, 6 Short Answer questions, 8 Long Answer questions, and 35 Numerical Questions for Practice. Solved answers are available on the Collegedunia NCERT Solutions page linked above.

Ques. What is the CBSE weightage of Chapter 2 in the Class 12 Accountancy board exam?

Ans.

Admission of a Partner carries 8 to 10 marks in the CBSE Class 12 Accountancy board paper and has appeared as a major numerical (6 to 8 marks) in every session from 2018 to 2025.

Ques. Which goodwill valuation methods are in the chapter?

Ans.

Three methods: Average Profit, Super Profit, and Capitalisation (capitalised value of average profit, and capitalisation of super profit). The Weighted Average variant of the Average Profit method is also briefly noted.

Comments