Accountancy Content Strategist | M.Com, 11 Years | Updated on - May 25, 2026

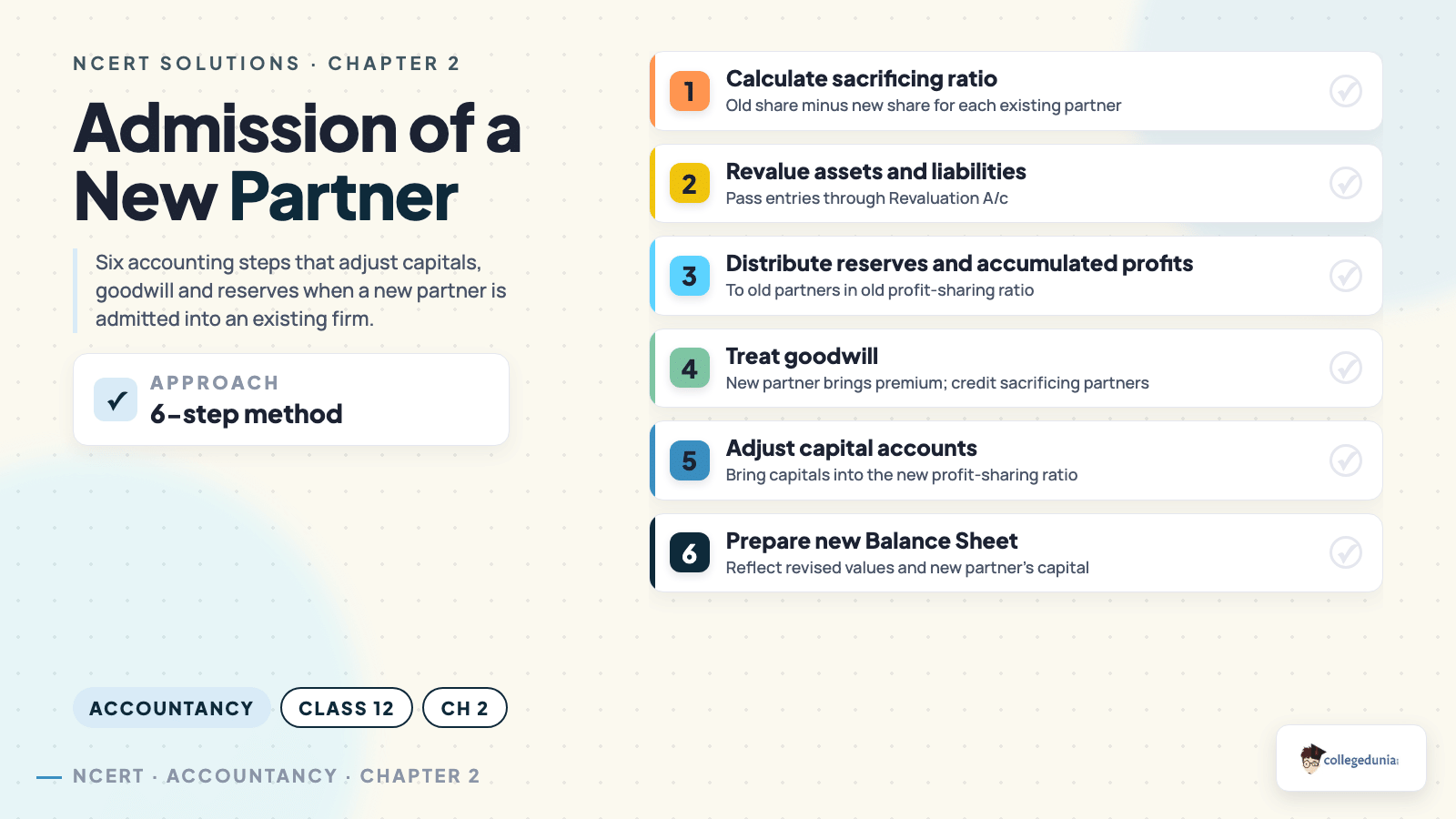

The accountancy class 12 ncert solutions chapter 2 Reconstitution of a Partnership Firm: Admission of a Partner PDF on this page solves all 49 textbook questions in the format CBSE markers reward: the six-adjustment sequence, T-format Revaluation A/c, AS-26 aligned goodwill treatment, and a balanced new firm. Every working line shows formula, substitution, and arithmetic separately so partial marks are never missed.

CBSE Weightage: 8 marks in Part A (highest single-chapter share across recent board papers)

Question Count: 6 Short Answer + 8 Long Answer + 35 Numerical = 49 solved questions

Chapter 2 Reconstitution of a Partnership Firm: Admission of a Partner NCERT Solutions PDF

The PDF below covers the new profit-sharing ratio, sacrificing ratio, three goodwill valuation methods, the four sub-cases of premium treatment, Revaluation Account, distribution of accumulated profits and reserves, and capital adjustment to the new ratio. Every numerical ends with a balanced opening Balance Sheet of the reconstituted firm.

These solutions are written by Chartered Accountants and Commerce educators, mapped to the 2026-27 NCERT, and cross-checked against the last five years of CBSE Class 12 Board papers.

Accountancy Class 12 NCERT Solutions Chapter 2 Reconstitution of a Partnership Firm: Admission of a Partner Question Map

The chapter splits cleanly into a theory block at the top of the exercise and a numerical block that scales from single-adjustment problems to full Balance Sheet questions. The numerical clusters mirror the CBSE marker's six-adjustment grid, so practising in this order is the fastest route to the 8-mark question.

Question Block

Count

Topic Focus

Typical CBSE Marks

Short Answer (Q1 to Q6)

6

Six adjustments rationale, sacrificing ratio definition, AS-26 stance on goodwill, revaluation purpose

1 to 3

Long Answer (Q1 to Q8)

8

Revaluation procedure, goodwill factors, three valuation methods, accumulated profits treatment, capital adjustment

3 to 4

Numerical Q1 to Q12

12

New PSR from default source and from specified shares, sacrificing ratio

3 to 4

Numerical Q13 to Q17

5

Goodwill valuation by Average Profit, Super Profit and Capitalisation

3 to 4

Numerical Q18 to Q26

9

Premium method, hidden goodwill, four sub-cases of payment treatment

4 to 6

Numerical Q27 to Q35

9

Full Revaluation A/c plus opening Balance Sheet of the new firm

6 to 8

The 8-mark CBSE question in every recent paper has come from the Q27 to Q35 cluster, which is why the PDF gives extra working space to those problems.

AS-26 reminder: Self-generated goodwill cannot appear on a partnership Balance Sheet. Any goodwill in the old books is first written off by debiting old partners' capitals in old PSR; only then is the new partner's premium recorded.

Reconstitution of a Partnership Firm Admission of a Partner Video W...

Three-line working on every calculation: formula on line one, substitution on line two, arithmetic on line three.

T-format Revaluation A/c for every full Balance Sheet question, with the closing transfer in old PSR.

All three goodwill valuation methods solved: Average Profit, Super Profit and Capitalisation of Average Profit.

Four sub-cases of premium treatment: retained in business, fully withdrawn, partially withdrawn, paid privately outside the books.

Hidden goodwill identification via the implied total capital method on every numerical where premium is not stated.

Expert Solution block on each numerical giving the CA-style alternate method and the common-error trap.

How Collegedunia's NCERT Solutions Help You Score the Full 8 Marks

2026-27 NCERT alignment: Question numbering and section references match the current Accountancy Part I textbook exactly.

Marker-style answer structure: Six-adjustment sequence followed in the same order CBSE evaluators expect on the 8-mark question.

Expert verification: Every Revaluation A/c, sacrificing ratio, hidden goodwill computation and capital adjustment is double-checked.

Common-error notes: AS-26 write-off, hidden goodwill, privately paid premium (no journal entry in firm books), reserves credited in old PSR, are all flagged inline.

Sample Solved Problem: New Profit-Sharing Ratio

Question. A and B share profits in 3:2. They admit C for 1/6 share, which C acquires from A and B in their old ratio. Calculate the new profit-sharing ratio.

Step 1: Default source rule. When the question is silent, the incoming partner takes from the old partners in their old profit-sharing ratio.

Step 2: Remaining share for old partners. 1 - 16 = 56

Step 3: New shares of A and B. A = 56 × 35 = 36; B = 56 × 25 = 26

Step 4: New PSR. A : B : C = 36 : 26 : 16 = 3 : 2 : 1

Top 5 Most-Tested Concepts in Admission of a Partner

Six Adjustments at Admission: The mental checklist every numerical follows, in the same order.

Sacrificing Ratio: Old Share minus New Share. Drives the credit side of the goodwill journal entry.

Goodwill Valuation: Average Profit, Super Profit, Capitalisation of Average Profit. Pick the method the question specifies.

Revaluation Account: Opens before admission. Gain or loss is transferred to old partners in old PSR.

AS-26 Write-Off: Existing goodwill on the books must be removed in old PSR before the incoming premium is recorded.

Class 12 Accountancy Chapter 2 Previous Year Question Trend

Admission of a Partner has carried 8 marks in five of the last six CBSE Class 12 Accountancy board papers, almost always as a full Balance Sheet question. The table tracks the topic mix.

Year

Marks

Topics Tested

2025

8

Full Balance Sheet on admission: revaluation, goodwill, capital adjustment

2024

8

Goodwill by super-profit method (3M) plus admission journal entries (5M)

2023

8

Revaluation A/c and Balance Sheet (6M); sacrificing ratio (2M)

2022

10

Goodwill by Capitalisation (4M); admission B/S (6M)

2021

8

Goodwill journal entries (4M); new PSR computation (4M)

2020

8

Goodwill, revaluation, opening Balance Sheet (8M)

Common Mistakes Flagged in the Solutions

Crediting reserves in new PSR. Reserves and accumulated profits belong to the old partners and are credited in old PSR.

Forgetting to write off existing goodwill. AS-26 makes the write-off compulsory before any premium entry.

Passing a journal entry for privately paid premium. If the new partner pays the premium outside the firm, no entry is recorded in the firm's books.

Hidden goodwill via wrong base. Compute total capital implied by the new partner's contribution, then deduct the combined capitals; the gap is the hidden goodwill.

Revaluation profit to all partners. Revaluation gain or loss is shared only among old partners in old PSR, never with the incoming partner.

Related Resources for Class 12 Accountancy Chapter 2

All NCERT Solutions for Reconstitution of a Partnership Firm: Admission of a Partner with Step-by-Step Working

Every NCERT textbook question for Class 12 Accountancy Chapter 2 Reconstitution of a Partnership Firm: Admission of a Partner is listed below with its full Solution and Expert Solution hidden inside collapsible tabs. Click Check Solution to reveal the step-by-step working; click Expert Solution for the expanded explanation.

Short Answer Questions

Q 2.1

Identify various matters that need adjustments at the time of admission of a new partner.

Concept used. On admission of a new partner the firm undergoes a

reconstitution, existing relations among partners change. Six

specific matters must be adjusted in the books before the new firm

starts trading.

New Profit-Sharing Ratio. Re-state the new ratio in

which the new partner and old partners will share future

profits.

Sacrificing Ratio. Compute the ratio in which old

partners surrender share for the new partner; this drives the

goodwill compensation.

Treatment of Goodwill. Value the firm's goodwill, then

adjust it through partners' capital accounts (premium method,

revaluation method, or hidden-goodwill method depending on the

deed).

Revaluation of Assets and Liabilities. Open a

Revaluation A/c; transfer net gain/loss to old partners

in their old PSR.

Distribution of Reserves and Accumulated Profits or

Losses. Transfer existing balances (general reserve, P&L

Cr. balance, workmen compensation reserve, etc.) to old

partners in their old PSR before the admission entry.

Adjustment of Capitals. If the deed requires, adjust

the capitals of all partners in the new PSR by introducing /

withdrawing cash, or by routing through current accounts.

Six adjustments: (1) new PSR, (2) sacrificing ratio, (3)

goodwill treatment, (4) revaluation of assets and liabilities, (5)

distribution of reserves and accumulated P&L, and (6) adjustment of

capitals to new ratio.

CR

CA Rohit Mehra

B.Com (H), FCA, Associate Member ICAI

Verified Expert

Strategic angle. Group the six adjustments under three

buckets: (a) ratio (new PSR, sacrificing ratio), (b) value

(goodwill, revaluation, reserves), (c) capital (final capital

adjustment).

Ratio adjustments first, compute the new PSR and the

sacrificing ratio.

Value adjustments next, goodwill, revaluation, reserves

(all three in old PSR).

Capital adjustment last (if deed requires).

Why this matters. Every numerical question in this chapter

follows this exact sequence. Train yourself to ask ``which of the six

adjustments does this part of the question want?''

Common mistakes. Three predictable slips lose marks: (a) skipping the calculation of the sacrificing ratio and crediting goodwill in the old ratio rather than the sacrificing ratio; (b) writing off existing goodwill in the new ratio instead of the old ratio, which is the AS-26 mandate; (c) leaving the revaluation gain or loss undistributed among old partners or distributing it in the new ratio rather than the old ratio.

Six adjustments grouped as ratio (PSR, sacrificing),

value (goodwill, revaluation, reserves) and capital.

Q 2.2

Why is it necessary to ascertain new profit-sharing ratio even for old partners when a new partner is admitted?

Concept used. When a new partner is admitted, the share of

profit currently going to the old partners must be reduced (in

some agreed proportion) to make room for the new partner's share.

Therefore the old partners' new profit-sharing ratio is not

their old ratio; it has to be recomputed.

Share given up. The total share given up by old

partners exactly equals the new partner's share.

Reduction in old shares. Each old partner's new

share = old share - his sacrifice.

Why this matters financially. Future profits will be

distributed in the new ratio; for any year's P&L App A/c we

need the new PSR. The new ratio also determines:

[leftmargin=18pt,topsep=2pt,itemsep=1pt]

the partners' capital proportion (if capitals are to

be in the new ratio);

the share of revaluation gain / loss (in old

ratio, but new ratio is needed for the cross-check);

how goodwill premium received from the new partner is

divided among the sacrificing old partners.

The new PSR for old partners is needed because their old

shares are no longer accurate after admission; every future profit,

capital adjustment and goodwill calculation depends on the new ratio.

PS

Priya Singhal

M.Com, NET-JRF, Commerce Faculty

Verified Expert

Strategic angle. Frame it as ``addition forces subtraction''

, adding a new partner to a fixed-sum profit pool forces each old

partner's share to fall.

The total share is always 1 (or 100%).

Once the new partner takes a slice, the rest must fit into

1 - new partner's share.

The way old partners redistribute that residue defines their

new ratio.

Why this matters. Without a clear new PSR for old partners,

the P&L App A/c becomes impossible to prepare for any subsequent year.

Common mistakes. Three predictable slips lose marks: (a) skipping the calculation of the sacrificing ratio and crediting goodwill in the old ratio rather than the sacrificing ratio; (b) writing off existing goodwill in the new ratio instead of the old ratio, which is the AS-26 mandate; (c) leaving the revaluation gain or loss undistributed among old partners or distributing it in the new ratio rather than the old ratio.

New PSR for old partners ensures clean future profit

distribution, capital adjustment and goodwill allocation.

Q 2.3

What is sacrificing ratio? Why is it calculated?

Concept used.Sacrificing ratio is the ratio in which

the old partners surrender (sacrifice) parts of their old share

in favour of the new partner.

Sacrifice of a partner = Old Share - New Share.

Definition. For each old partner, the sacrifice is

positive (he loses share). The set of sacrifices, taken in

order, defines the sacrificing ratio.

Why it is calculated.

[leftmargin=18pt,topsep=2pt,itemsep=1pt]

To distribute the goodwill premium brought in

by the new partner among the old partners in the

proportion in which they have surrendered share.

If the new partner does not bring his share of

goodwill in cash, an adjustment journal entry passes

debit to the new partner's capital and credit to the

sacrificing partners' capitals in the sacrificing

ratio.

Sacrificing ratio is also used to compute the

gaining ratio on a future change in PSR (it is

the mirror image).

Sacrificing ratio = Old Share - New Share, computed for

each old partner. It is needed to distribute the new partner's

goodwill premium and to pass goodwill-adjustment entries.

RG

Rekha Gokhale

PhD Commerce, Presidency Kolkata

Verified Expert

Strategic angle. Memorise the dual question: sacrificing

ratio at admission = gaining ratio at retirement. Same formula, mirror

direction.

Sacrifice = Old - New (positive for sacrificing partner).

Express the sacrifices as a single ratio (e.g. 3:2).

Use this ratio to allocate goodwill premium.

Why this matters. CBSE often gives the new PSR and old PSR

and asks for the sacrificing ratio in a one-mark sub-question

embedded inside a larger 6-mark question.

Common mistakes. Three predictable slips lose marks: (a) skipping the calculation of the sacrificing ratio and crediting goodwill in the old ratio rather than the sacrificing ratio; (b) writing off existing goodwill in the new ratio instead of the old ratio, which is the AS-26 mandate; (c) leaving the revaluation gain or loss undistributed among old partners or distributing it in the new ratio rather than the old ratio.

Sacrificing ratio = Old - New; needed for distributing

goodwill premium and passing goodwill-adjustment entries.

Q 2.4

On what occasions sacrificing ratio is used?

Concept used. The sacrificing ratio is used in any

reconstitution event where one or more old partners give up share in

favour of another partner.

Admission of a new partner. Goodwill premium brought

in by the new partner is credited to the sacrificing partners

in the sacrificing ratio.

Change in profit-sharing ratio among existing

partners. When one partner gains and another sacrifices, the

gaining partner compensates the sacrificing partner for his

share of goodwill, in the sacrificing ratio (= gain ratio,

mirrored).

Conversion of a partnership into a company (advanced

topic, beyond Class 12 syllabus but commonly tested in B.Com

first year).

Sacrificing ratio is used (i) on admission of a new partner

to distribute goodwill premium; (ii) on a change in PSR among

existing partners to record the goodwill compensation entry; and

(iii) in conversion of a firm into a company.

ML

Manish Luthra

PhD Economics, IIM Kozhikode

Verified Expert

Strategic angle. The sacrificing ratio appears whenever

one partner pays another for surrendered profit share.

Admission of new partner, new partner pays old partners.

Change in PSR, gaining partner pays sacrificing partner.

Both cases use the sacrificing ratio (or its mirror, the

gaining ratio).

Why this matters. Sacrificing-ratio computations earn easy

marks in every reconstitution numerical.

Common mistakes. Three predictable slips lose marks: (a) skipping the calculation of the sacrificing ratio and crediting goodwill in the old ratio rather than the sacrificing ratio; (b) writing off existing goodwill in the new ratio instead of the old ratio, which is the AS-26 mandate; (c) leaving the revaluation gain or loss undistributed among old partners or distributing it in the new ratio rather than the old ratio.

Three occasions: admission of new partner, change in PSR

among existing partners, conversion of firm into a company.

Q 2.5

If some goodwill already exists in the books and the new partner brings in his share of goodwill in cash, how will you deal with the existing amount of goodwill?

Concept used. As per AS-26 (Accounting Standard 26)

issued by the ICAI, self-generated goodwill cannot be shown

on the balance sheet. Hence any goodwill already appearing in the

books of the old firm must be written off before the new

partner's admission.

Write off existing goodwill. The goodwill currently

shown in the books is debited to the old partners' capital

accounts in their old profit-sharing ratio, and the

Goodwill A/c is credited.

tabularlrr

& Dr. (Rs.) & Cr. (Rs.)

Old Partners' Capital A/c Dr. (in old PSR) & xxx &

To Goodwill A/c & & xxx

3l(Existing goodwill written off)

tabular

Record incoming goodwill premium. Cash brought in by

the new partner for his share of goodwill is credited to the

sacrificing partners in the sacrificing ratio.

tabularlrr

& Dr. (Rs.) & Cr. (Rs.)

Cash / Bank A/c Dr. & xxx &

To Sacrificing Partners' Capital A/cs & & xxx

3l(Goodwill premium brought by new partner)

tabular

Existing goodwill is first written off to old partners'

capital A/cs in the old PSR; then the new partner's incoming

goodwill premium is credited to the sacrificing partners in the

sacrificing ratio.

GO

Geeta Ojha

PhD Accounting, ICAI Kolkata

Verified Expert

Strategic angle. Two journal entries in sequence: (a) wipe

old goodwill from the books in old PSR; (b) credit incoming premium

to sacrificing partners in sacrificing ratio.

Existing goodwill is fictitious from an accounting-standards

perspective; remove it.

Incoming goodwill premium is real cash; credit it correctly.

Why this matters. CBSE has tested this exact two-step

sequence in 2020, 2022 and 2024. Forgetting the AS-26 write-off costs

half the marks of the question.

Common mistakes. Three predictable slips lose marks: (a) skipping the calculation of the sacrificing ratio and crediting goodwill in the old ratio rather than the sacrificing ratio; (b) writing off existing goodwill in the new ratio instead of the old ratio, which is the AS-26 mandate; (c) leaving the revaluation gain or loss undistributed among old partners or distributing it in the new ratio rather than the old ratio.

(i) Write off existing goodwill to old partners' capitals

in old PSR; (ii) Credit incoming premium to sacrificing partners in

sacrificing ratio.

Q 2.6

Why is there a need for the revaluation of assets and liabilities on the admission of a partner?

Concept used. At the date of admission of a new partner, the

firm's assets and liabilities may be carrying book values that

no longer reflect fair values. The new partner should neither

benefit from undisclosed appreciation nor suffer hidden depreciation;

similarly, the gain or loss on revaluation must accrue to the

old partners (in their old PSR), not to the incoming partner.

Fairness to incoming partner. If the building is

worth Rs. 12,00,000 but shown at Rs. 10,00,000, the

unrecognised gain belongs to the old partners. Without

revaluation, the new partner would automatically acquire a

share of that hidden gain, which would be unfair.

Fairness to old partners. Hidden depreciation

(e.g. outdated machinery, bad debts not provided for) must

be absorbed by old partners, not foisted on the new partner.

Accounting accuracy. The Balance Sheet of the new

firm must show assets and liabilities at fair value, in line

with the prudence concept.

Mechanics. A Revaluation A/c (also called Profit &

Loss Adjustment A/c) is opened. Increase in asset / decrease

in liability is credited; decrease in asset / increase in

liability is debited. The net balance is transferred to old

partners' capital A/cs in old PSR.

Revaluation is needed so that any hidden gain or loss at

the date of admission accrues only to the old partners, in their old

PSR, and not to the new partner; this maintains fairness and ensures

the new firm's Balance Sheet shows fair values.

DR

Deepak Ranjan

MCom NET, Madras Christian College

Verified Expert

Strategic angle. Three motivations to remember: fairness,

accuracy, accountability.

Fairness, gains/losses till admission date belong to old

partners in old PSR.

Accuracy, new firm's Balance Sheet should show fair

values.

Accountability, the Revaluation A/c is the single document

that records who got what.

Why this matters. Numerical Q27–Q35 of this chapter test the

Revaluation A/c. Mastering its rules unlocks half the chapter's

marks.

Common mistakes. Three predictable slips lose marks: (a) skipping the calculation of the sacrificing ratio and crediting goodwill in the old ratio rather than the sacrificing ratio; (b) writing off existing goodwill in the new ratio instead of the old ratio, which is the AS-26 mandate; (c) leaving the revaluation gain or loss undistributed among old partners or distributing it in the new ratio rather than the old ratio.

Revaluation ensures hidden gain/loss accrues to old

partners (in old PSR), maintains fair values on the new firm's

Balance Sheet, and provides an audit trail.

Long Answer Questions

Q 2.7

Do you advise that assets and liabilities must be revalued at the time of admission of a partner? If so, why? Also describe how it is treated in the books of account.

Concept used. Yes, assets and liabilities must be

revalued at the time of admission of a partner. The reasoning has

three pillars: fairness, accounting accuracy, and statutory

compliance. The mechanics of revaluation go through a Revaluation

A/c (or Profit & Loss Adjustment A/c).

Why revalue?

[leftmargin=18pt,topsep=2pt,itemsep=1pt]

Any unrecognised appreciation belongs to the old

partners (they earned it before admission).

Any unrecognised depreciation should be borne by old

partners (it occurred during their tenure).

The new firm's Balance Sheet should disclose

fair values.

Statutory compliance with AS-10 (Property, Plant and

Equipment) and AS-29 (Provisions, Contingent

Liabilities).

Open a Revaluation A/c.

Credits (gains):

[leftmargin=18pt,topsep=2pt,itemsep=1pt]

Increase in value of asset.

Decrease in value of liability.

Unrecorded asset brought in.

Debits (losses):

[leftmargin=18pt,topsep=2pt,itemsep=1pt]

Decrease in value of asset.

Increase in value of liability.

Unrecorded liability brought in.

New provision for doubtful debts.

Journal entries.

tabularlrr

& Dr. & Cr.

Asset A/c Dr. (increase) & xxx &

To Revaluation A/c & & xxx

Revaluation A/c Dr. (decrease) & xxx &

To Asset A/c & & xxx

Liability A/c Dr. (decrease) & xxx &

To Revaluation A/c & & xxx

Revaluation A/c Dr. (increase in liab) & xxx &

To Liability A/c & & xxx

tabular

Transfer net balance to Old Partners' Capital A/cs.

If credit side (gains) > debit side (losses), it is a

gain on revaluation, credited to old partners'

capitals in the old PSR. Otherwise it is a

loss, debited similarly.

tabularlrr

& Dr. & Cr.

Revaluation A/c (Gain) Dr. & xxx &

To Old Partners' Capitals (Old PSR) & & xxx

Old Partners' Capitals (Old PSR) Dr. (Loss) & xxx &

To Revaluation A/c & & xxx

tabular

Yes, revaluation is necessary. It is recorded in a

Revaluation A/c: gains (asset increase, liability decrease) are

credited; losses (asset decrease, liability increase, new provisions)

are debited; the net balance is transferred to old partners' capital

accounts in their old PSR.

SK

Sangeeta Kulkarni

MA Economics, IIM Shillong

Verified Expert

Strategic angle. The Revaluation A/c is a temporary nominal

account. It exists for one purpose: to compute the net adjustment

that belongs to the old partners.

List every asset/liability change one by one.

Post each to the correct side of the Revaluation A/c.

Net balance to old partners in old PSR.

Why this matters. The Revaluation A/c is the second-most-

tested item in admission numericals (after capital adjustment).

A clean four-step procedure earns method marks even if the final

balance is wrong.

Common mistakes. Three predictable slips lose marks: (a) skipping the calculation of the sacrificing ratio and crediting goodwill in the old ratio rather than the sacrificing ratio; (b) writing off existing goodwill in the new ratio instead of the old ratio, which is the AS-26 mandate; (c) leaving the revaluation gain or loss undistributed among old partners or distributing it in the new ratio rather than the old ratio.

Open Revaluation A/c; credit asset increases and liability

decreases; debit the opposites; transfer net gain/loss to old

partners in old PSR.

Q 2.8

What is goodwill? What factors affect goodwill?

Concept used.Goodwill is the present value of a

firm's future earnings in excess of normal earnings on its capital

employed, in other words, the value of the firm's reputation,

customer relations, brand, and other intangible advantages that

enable it to earn super profits.

Formal definition.Goodwill is an intangible

asset representing the excess of the purchase consideration

of a business over the fair value of its identifiable net

assets.

Two kinds of goodwill.

[leftmargin=18pt,topsep=2pt,itemsep=1pt]

Purchased goodwill, paid for when one firm

buys another; shown as an asset (AS-26 permits).

Self-generated goodwill, built up over

years through reputation; cannot be shown on the

balance sheet (AS-26 prohibits).

Factors affecting goodwill.

[leftmargin=18pt,topsep=2pt,itemsep=1pt]

Quality and reputation of the product /

service. Higher quality ⇒ stronger

customer loyalty ⇒ higher goodwill.

Efficient management. Skilled,

forward-looking management adds to goodwill.

Favourable location. Prime commercial

location boosts goodwill.

Strong customer base. Repeat customers

signal goodwill.

Time factor. The longer a firm has been in

business, the more goodwill it builds, ceteris

paribus.

Capital required. A capital-light business

can deliver high returns on small capital, raising

goodwill.

Future prospects. Goodwill is forward-

looking; a firm in a growth industry commands higher

goodwill than one in decline.

Goodwill = present value of a firm's super-earning capacity.

Factors affecting goodwill: product/service quality, efficient

management, location, customer base, risk profile, age of the firm,

capital required, and future prospects.

PB

Pankaj Bhardwaj

MCom CA, IIM Bangalore

Verified Expert

Strategic angle. Define goodwill as the value of

super-earning capacity, then list 6–8 factors. CBSE allots 1 mark

per factor.

Goodwill = capitalised value of expected super-profits.

AS-26 allows only purchased goodwill on books.

Eight standard factors as memorised above.

Why this matters. Numerical Q13–Q17 of this chapter rely on

goodwill valuation methods that all derive from the underlying

definition, super-profit-based pricing of intangible advantages.

Common mistakes. Three predictable slips lose marks: (a) skipping the calculation of the sacrificing ratio and crediting goodwill in the old ratio rather than the sacrificing ratio; (b) writing off existing goodwill in the new ratio instead of the old ratio, which is the AS-26 mandate; (c) leaving the revaluation gain or loss undistributed among old partners or distributing it in the new ratio rather than the old ratio.

Goodwill = value of super-earning capacity. Factors:

quality, management, location, customers, risk, age, capital, future

prospects.

Q 2.9

Explain various methods of valuation of goodwill.

Concept used. Three principal methods are prescribed in the

NCERT for valuing goodwill at admission, retirement or change in

PSR.

Average Profit Method.

Goodwill = Average Profit × Number of years' purchase.

Average profit is computed over the last 3–5 years.

``Years' purchase'' is the multiplier (typically 2 to 4).

Example: Average profit Rs. 50,000; 4 years'

purchase ⇒ Goodwill = 50,000 × 4 =

Rs. 2,00,000.

Super Profit Method.

First, define Super Profit and Normal Profit:

Super Profit = Actual Avg Profit - Normal Profit.

Normal Profit equals capital employed multiplied by normal rate divided by 100.

Then the goodwill is computed as:

Goodwill = Super Profit × Years' Purchase.

Example: Avg profit Rs. 1,00,000; capital

Rs. 5,00,000; normal rate 12%. Normal profit

= 60,000; super profit = 40,000. Goodwill (3 years'

purchase) = 40,000 × 3 = Rs. 1,20,000.

Capitalisation Method. Two sub-methods.

Capitalisation of Average Profit:

Goodwill = (Avg Profit × 100 ÷ Normal Rate) - Capital Employed.

Capitalisation of Super Profit:

Goodwill = Super Profit × 100 ÷ Normal Rate.

Example: Avg profit Rs. 1,00,000; normal rate

10%; capital Rs. 8,20,000.

Capitalised value = 100 × 1,00,000 / 10 =

10,00,000. Goodwill = 10,00,000 - 8,20,000 =

Rs. 1,80,000.

Weighted Average Profit Method (advanced, a

refinement of Average Profit Method). Assign higher weights

to more recent years.

Weighted Avg = ∑ (Profit × Weight)∑ Weight.

Three primary methods: (i) Average Profit (Avg ×

years' purchase); (ii) Super Profit (Super Profit × years'

purchase, where Super = Actual - Normal); (iii) Capitalisation

(either of Avg Profit minus Capital Employed, or Super Profit divided

by Normal Rate). The Weighted Average method is a refinement.

SC

Sunita Chatterjee

MBA Banking, Symbiosis Pune

Verified Expert

Strategic angle. Choose the method to match the data given.

Given only past profits + a multiplier ⇒ Average

Profit method.

Given profits + capital + normal rate ⇒ Super

Profit method.

Given profits + capital + normal rate + asked for

capitalised value ⇒ Capitalisation method.

Why this matters. CBSE awards full marks for any of the

three methods provided the working matches the data given. Knowing

which method best fits saves time.

Common mistakes. Three predictable slips lose marks: (a) skipping the calculation of the sacrificing ratio and crediting goodwill in the old ratio rather than the sacrificing ratio; (b) writing off existing goodwill in the new ratio instead of the old ratio, which is the AS-26 mandate; (c) leaving the revaluation gain or loss undistributed among old partners or distributing it in the new ratio rather than the old ratio.

Average Profit, Super Profit, and Capitalisation are the

three NCERT methods. Choose based on the data given.

Q 2.10

If it is agreed that the capital of all the partners should be proportionate to the new profit-sharing ratio, how will you work out the new capital of each partner? Give examples and state how necessary adjustments will be made.

Concept used.Proportionate capital adjustment on

admission means that, after the new partner is admitted, each partner's

capital must stand in the same ratio as the new profit-sharing

ratio. The base for the new total capital is normally the capital

brought in by the new partner (since his share of profits is known).

Identify the new partner's capital and share. Suppose

C is admitted for 14 share and brings in Rs. 1,00,000.

Compute total new capital of the firm.

Total capital = New partner's capitalNew partner's share

= 1,00,0001/4 = Rs. 4,00,000.

Compute each old partner's new capital in the new PSR.

If A and B were in 3:2 and now sit in 9:6:5 with C,

aligned

A's new capital &= 4,00,000 × 920 = Rs. 1,80,000, B's new capital &= 4,00,000 × 620 = Rs. 1,20,000, C's capital &= 4,00,000 × 520 = Rs. 1,00,000.

aligned

Adjust each old partner's existing capital.

If existing capital < new capital, partner brings in cash;

if existing capital > new capital, excess is paid back in

cash or transferred to a Current A/c.

Total new capital = New partner's capital ÷ his share.

Allocate to each partner in the new PSR; adjust by cash or current

account.

KI

Karan Iyer

M.Com, Bombay University

Verified Expert

Strategic angle. Two flavours: (a) base on new partner's

capital, (b) base on combined capital of old partners. Read carefully.

Total firm capital = new partner's capital ÷ his share.

Multiply by each partner's new share.

Compare with existing balance; bring in or withdraw cash.

Why this matters. CBSE asks this in 4–6 mark questions; the

key is converting ``proportionate to PSR'' into clear arithmetic.

Common mistakes. Three predictable slips lose marks: (a) skipping the calculation of the sacrificing ratio and crediting goodwill in the old ratio rather than the sacrificing ratio; (b) writing off existing goodwill in the new ratio instead of the old ratio, which is the AS-26 mandate; (c) leaving the revaluation gain or loss undistributed among old partners or distributing it in the new ratio rather than the old ratio.

New total capital = partner's capital ÷ share; allocate in

new PSR; adjust by cash/current A/c.

Q 2.11

Explain how will you deal with goodwill when the new partner is not in a position to bring his share of goodwill in cash.

Concept used. When the incoming partner cannot pay his share

of goodwill in cash, his share is adjusted by a debit to his

Capital A/c and a credit to the old partners' Capital A/cs in

their sacrificing ratio. The premium is never recorded in a

Goodwill A/c (AS-26 prohibits creating self-generated goodwill).

Value goodwill using any standard method (Avg Profit,

Super Profit, Capitalisation).

Compute new partner's share of goodwill= Total goodwill × his share.

Pass the adjustment entry:

tabularlrr

Particulars & Dr. (Rs.) & Cr. (Rs.)

New partner's Capital A/c & xxxx &

1emTo Old partners' Capital A/cs (sacrificing ratio) & & xxxx

3l(Being new partner's share of goodwill credited

3lto old partners in their sacrificing ratio)

tabular

Why not raise a Goodwill A/c? AS-26 disallows

capitalising self-generated goodwill; the adjustment must run

through Capital A/cs.

Debit new partner's Capital with his share of goodwill; credit

old partners' Capital in sacrificing ratio. No Goodwill A/c is raised.

DR

Diya Reddy

M.Com, NET, Commerce Faculty

Verified Expert

Strategic angle. Memorise: new partner's Capital Dr. to old

partners' Capital (sacrificing ratio).

Value goodwill; find new partner's share.

Debit his Capital; credit old partners' in sacrificing ratio.

Why this matters. Quoting AS-26 in 4-mark theory earns the

``conceptual clarity'' mark.

Common mistakes. Three predictable slips lose marks: (a) skipping the calculation of the sacrificing ratio and crediting goodwill in the old ratio rather than the sacrificing ratio; (b) writing off existing goodwill in the new ratio instead of the old ratio, which is the AS-26 mandate; (c) leaving the revaluation gain or loss undistributed among old partners or distributing it in the new ratio rather than the old ratio.

Capital adjustment entry: new partner Dr. old partners Cr. in

sacrificing ratio.

Q 2.12

Explain various methods for the treatment of goodwill on the admission of a new partner.

Concept used. Four standard scenarios (only the first three

are AS-26 compliant; the fourth handles inferred figures):

Premium Method (cash brought). New partner brings his

share of goodwill in cash. Cash debited; old partners' Capital

A/cs credited in sacrificing ratio.

tabularlrr

Cash A/c & Dr. xxxx &

1emTo Premium for Goodwill A/c & & xxxx

Premium for Goodwill A/c & Dr. xxxx &

1emTo Old partners' Capital A/cs & & xxxx

tabular

When new partner cannot bring cash.

New partner's Capital A/c Dr.; old partners' Capital A/cs

Cr. in sacrificing ratio.

When goodwill already appears in books. Write off old

goodwill first by debiting old partners' Capital A/cs in

old ratio, then apply Method 1 or 2.

Hidden goodwill (inferred). If the new partner's

capital is given but total firm capital implies a higher

figure, the difference is hidden goodwill:

Hidden Goodwill = New partner's capitalhis share

- Total adjusted capital.

Then apply Method 2.

Four sub-cases: cash premium, no-cash via Capital A/c,

existing goodwill written off, hidden goodwill computed. All AS-26

compliant.

VM

Vipin Malhotra

MBA Finance, IMI Delhi

Verified Expert

Strategic angle. Identify the sub-case first.

Cash premium ⇒ Cash Dr. + Premium for Goodwill A/c.

No cash ⇒ New partner's Capital Dr.

Existing goodwill ⇒ write off in old ratio first.

Hidden goodwill ⇒ compute via capital comparison.

Why this matters. A typical 6-mark CBSE question gives one

scenario but expects you to name the sub-case, write the label at

the top of your answer for a method mark.

Common mistakes. Three predictable slips lose marks: (a) skipping the calculation of the sacrificing ratio and crediting goodwill in the old ratio rather than the sacrificing ratio; (b) writing off existing goodwill in the new ratio instead of the old ratio, which is the AS-26 mandate; (c) leaving the revaluation gain or loss undistributed among old partners or distributing it in the new ratio rather than the old ratio.

Premium, no-cash, existing-goodwill-write-off, hidden-goodwill,

identify, then apply.

Q 2.13

How will you deal with accumulated profits and losses and reserves on the admission of a new partner?

Concept used. Accumulated profits, reserves, P&L

(Cr. balance), and accumulated losses, P&L (Dr. balance), all belong

to the old partners and must be distributed in the old

profit-sharing ratio before the new partner is admitted.

For accumulated profits / General Reserve / P&L (Cr.)

, distribute to old partners' Capital A/cs in old PSR.

tabularlrr

Reserve / Profit A/c & Dr. xxxx &

1emTo Old partners' Capital A/cs & & xxxx

3l(in old profit-sharing ratio)

tabular

For accumulated losses / P&L (Dr.), charge to old

partners' Capital A/cs in old PSR.

tabularlrr

Old partners' Capital A/cs & Dr. xxxx &

1emTo P&L A/c (Dr. balance) & & xxxx

tabular

Why old PSR? These items accrued when only the old

partners existed; the new partner has no claim.

Accumulated profits credit old partners' Capital; accumulated

losses debit them. Always in old profit-sharing ratio.

Reserves and Cr. P&L → Cr. old partners' Capital in old PSR.

Dr. P&L → Dr. old partners' Capital in old PSR.

Why this matters. The CBSE 8-mark question typically combines

this with revaluation; the order is revalue → reserves

→ goodwill → admit.

Common mistakes. Three predictable slips lose marks: (a) skipping the calculation of the sacrificing ratio and crediting goodwill in the old ratio rather than the sacrificing ratio; (b) writing off existing goodwill in the new ratio instead of the old ratio, which is the AS-26 mandate; (c) leaving the revaluation gain or loss undistributed among old partners or distributing it in the new ratio rather than the old ratio.

Old PSR; Cr. items boost old capitals, Dr. items reduce them.

Q 2.14

At what figures do the values of assets and liabilities appear in the books of the firm after revaluation has been done? Show with the help of an imaginary balance sheet.

Concept used. After revaluation, every asset and liability is

recorded at its revalued amount. The net gain or loss on

revaluation is distributed among the old partners in the old PSR via

the Revaluation A/c.

Net Revaluation gain = 1,00,000 - 5,000 + 4,000

= Rs. 99,000, credited to old partners' Capitals in

old PSR.

All assets and liabilities are shown at their revalued (new)

figures. The Revaluation A/c's net balance is transferred to old

partners' Capitals in old PSR.

AG

Anil Garg

MCom CFA, FMS BHU Varanasi

Verified Expert

Strategic angle. Treat each B/S line as a comparison: book

value vs. new figure; the difference flows to Revaluation A/c.

Rewrite each item at its revalued amount.

Build the Revaluation A/c; net gain/loss to old partners.

Carry revalued figures into the new B/S.

Why this matters. CBSE often asks for ``Balance Sheet after

revaluation'' as a 6-mark sub-question, remembering that ALL items

appear at the new figures saves marks.

Common mistakes. Three predictable slips lose marks: (a) skipping the calculation of the sacrificing ratio and crediting goodwill in the old ratio rather than the sacrificing ratio; (b) writing off existing goodwill in the new ratio instead of the old ratio, which is the AS-26 mandate; (c) leaving the revaluation gain or loss undistributed among old partners or distributing it in the new ratio rather than the old ratio.

Revalued figures in the new B/S; Revaluation gain/loss to old

partners' Capitals in old PSR.

Numerical Questions

Q 2.15

A and B were partners in a firm sharing profits and losses in the ratio of 3:2. They admit C into the partnership with 1/6 share in the profits. Calculate the new profit-sharing ratio.

Concept used. When the question does not specify how the new

partner acquires his share, the default assumption is that the new

partner acquires his share from the old partners in their

old profit-sharing ratio. The old partners' new shares are

their old shares scaled down by (1 - new share).

Total share that remains for old partners.

1 - 16 = 56.

Old partners' new shares (in old ratio 3:2):

A: 56 × 35 = 36 = 12B: 56 × 25 = 26 = 13

Express in LCM. Common denominator 6:

A: 36, B: 26, C: 16.

New profit-sharing ratio.A:B:C = 3:2:1.

New profit-sharing ratio A:B:C = 3:2:1.

SM

Shweta Mehta

MCom ICWA, Welingkar Mumbai

Verified Expert

Strategic angle. Whenever the new partner's source is

unspecified, default to old PSR.

Remaining share = 1 - new share = 5/6.

Scale old shares: A = 3/5 × 5/6 = 3/6; B = 2/6;

C = 1/6.

Why this matters. This default rule appears in nearly every

admission question. Memorise it.

Common mistakes. Three predictable slips lose marks: (a) skipping the calculation of the sacrificing ratio and crediting goodwill in the old ratio rather than the sacrificing ratio; (b) writing off existing goodwill in the new ratio instead of the old ratio, which is the AS-26 mandate; (c) leaving the revaluation gain or loss undistributed among old partners or distributing it in the new ratio rather than the old ratio.

3:2:1.

Q 2.16

A, B and C were partners sharing profits 3:2:1. They admitted D for 10% profits. Calculate the new PSR.

Concept used. When the new partner's share is acquired equally

from all old partners, each old partner sacrifices in their old PSR; the new

PSR follows directly.

D's share = 10% = 110.

Remaining 910 split among A, B, C in 3:2:1.

aligned

A &= 910 × 36 = 2760 = 920. B &= 910 × 26 = 1860 = 620. C &= 910 × 16 = 960 = 320.

aligned

D = 110 = 220. New PSR = 9:6:3:2.

New PSR =9:6:3:2.

NP

Naveen Pillai

MCom NET-JRF, SP Jain Mumbai

Verified Expert

Strategic angle. Compute remaining share; split in old PSR; bring to

common denominator.

Remaining = 9/10 in 3:2:1.

Convert to common denominator 20.

Why this matters. 1-mark direct question.

Common mistakes. Three predictable slips lose marks: (a) skipping the calculation of the sacrificing ratio and crediting goodwill in the old ratio rather than the sacrificing ratio; (b) writing off existing goodwill in the new ratio instead of the old ratio, which is the AS-26 mandate; (c) leaving the revaluation gain or loss undistributed among old partners or distributing it in the new ratio rather than the old ratio.

9:6:3:2.

Q 2.17

X and Y are partners sharing profits 5:3. Admitted Z for 1/10 share which he acquired equally from X and Y. Calculate new PSR.

Concept used. New partner takes equally from each old partner.

Z's share = 110; each old partner sacrifices 120.

aligned

X new &= 58 - 120 = 5080 - 480 = 4680 = 2340. Y new &= 38 - 120 = 3080 - 480 = 2680 = 1340. Z &= 110 = 440.

aligned

New PSR X:Y:Z =23:13:4.

BP

Bhavya Pandey

MCom CA-Inter, IIM Calcutta

Verified Expert

Strategic angle. Equal sacrifice ⇒ split Z's share in half between X and Y.

Each old sacrifices 120.

Common denominator 40.

Why this matters. Tests the ``equally acquired'' phrase.

Common mistakes. Three predictable slips lose marks: (a) skipping the calculation of the sacrificing ratio and crediting goodwill in the old ratio rather than the sacrificing ratio; (b) writing off existing goodwill in the new ratio instead of the old ratio, which is the AS-26 mandate; (c) leaving the revaluation gain or loss undistributed among old partners or distributing it in the new ratio rather than the old ratio.

23:13:4.

Q 2.18

A, B and C share profits 2:2:1. Admitted D for 1/8 share acquired entirely from A. Calculate new PSR.

Concept used. New partner's share is acquired from one specific

old partner; only that partner's share is reduced.

A new share = 25 - 18 = 1640 - 540 = 1140.

B new = 25 = 1640 (unchanged).

C new = 15 = 840 (unchanged).

D = 18 = 540.

New PSR A:B:C:D =11:16:8:5.

RK

Ramesh Kaur

BCom FCA, K.J. Somaiya Mumbai

Verified Expert

Strategic angle. ``Entirely from A'' ⇒ only A's

share decreases.

Subtract D's share from A only.

Common denominator 40.

Why this matters. Distinguishes ``from all'' vs. ``from one''.

Common mistakes. Three predictable slips lose marks: (a) skipping the calculation of the sacrificing ratio and crediting goodwill in the old ratio rather than the sacrificing ratio; (b) writing off existing goodwill in the new ratio instead of the old ratio, which is the AS-26 mandate; (c) leaving the revaluation gain or loss undistributed among old partners or distributing it in the new ratio rather than the old ratio.

11:16:8:5.

Q 2.19

P and Q share profits 2:1. Admitted R for 1/5 share acquired from P and Q in 1:2 ratio. Calculate new PSR.

Concept used. R's share is acquired from old partners in a

specified ratio (1:2), so P's sacrifice = 13 × 15

and Q's sacrifice = 23 × 15.

Sacrifices: P = 115; Q = 215.

P new = 23 - 115 = 1015 - 115 = 915 = 35.

Q new = 13 - 215 = 515 - 215 = 315 = 15.

R = 15.

New PSR P:Q:R =3:1:1.

KD

Kirti Dutta

BCom CMA, Delhi University

Verified Expert

Strategic angle. Split new partner's share in the agreed

sacrifice ratio.

P sacrifices Rs. 115; Q sacrifices 215.

Why this matters. Explicit sacrifice ratio is the most common

admission variant.

Common mistakes. Three predictable slips lose marks: (a) skipping the calculation of the sacrificing ratio and crediting goodwill in the old ratio rather than the sacrificing ratio; (b) writing off existing goodwill in the new ratio instead of the old ratio, which is the AS-26 mandate; (c) leaving the revaluation gain or loss undistributed among old partners or distributing it in the new ratio rather than the old ratio.

3:1:1.

Q 2.20

A, B and C share profits 3:2:2. Admitted D for 1/5 share acquired from A, B, C in 2:2:1 ratio. Calculate new PSR.

Concept used. D's share split per specified sacrifice ratio.

D's 15 split 2:2:1 (total 5):

A sacrifices 225; B 225; C 125.

Compute new shares (over 175 to find common denominator).

aligned

A new &= 37 - 225 = 75 - 14175 = 61175. B new &= 27 - 225 = 50 - 14175 = 36175. C new &= 27 - 125 = 50 - 7175 = 43175. D &= 15 = 35175.

aligned

New PSR A:B:C:D =61:36:43:35.

MK

Mahesh Kashyap

BCom (H) FCA, ISB Hyderabad

Verified Expert

Strategic angle. Two-step LCM (7 and 25) to find common denominator.

Compute each sacrifice.

Common denominator 175.

Why this matters. Higher-LCM problems test arithmetic precision.

Common mistakes. Three predictable slips lose marks: (a) skipping the calculation of the sacrificing ratio and crediting goodwill in the old ratio rather than the sacrificing ratio; (b) writing off existing goodwill in the new ratio instead of the old ratio, which is the AS-26 mandate; (c) leaving the revaluation gain or loss undistributed among old partners or distributing it in the new ratio rather than the old ratio.

61:36:43:35.

Q 2.21

A and B share profits 3:2. Admitted C for 3/7 share, taking 2/7 from A and 1/7 from B. Calculate new PSR.

Concept used. Specified sacrifice from each partner separately.

A new = 35 - 27 = 21 - 1035 = 1135.

B new = 25 - 17 = 14 - 535 = 935.

C = 37 = 1535.

New PSR A:B:C =11:9:15.

NP

Nidhi Patil

PhD Finance, IIM Ahmedabad

Verified Expert

Strategic angle. Direct subtraction; common denominator 35.

Sacrifices specified.

Why this matters. Multi-source sacrifice ratio.

Common mistakes. Three predictable slips lose marks: (a) skipping the calculation of the sacrificing ratio and crediting goodwill in the old ratio rather than the sacrificing ratio; (b) writing off existing goodwill in the new ratio instead of the old ratio, which is the AS-26 mandate; (c) leaving the revaluation gain or loss undistributed among old partners or distributing it in the new ratio rather than the old ratio.

11:9:15.

Q 2.22

A, B and C share profits 3:3:2. Admitted D for 4/7 profit. D acquired 2/7 from A, 1/7 from B and 1/7 from C. Calculate new PSR.

Concept used. Specified per-partner sacrifices.

A new = 38 - 27 = 21 - 1656 = 556.

B new = 38 - 17 = 21 - 856 = 1356.

C new = 28 - 17 = 14 - 856 = 656.

D = 47 = 3256.

New PSR A:B:C:D =5:13:6:32.

PT

Prakash Tandon

MSc Statistics, ICAI Chandigarh

Verified Expert

Strategic angle. Common denominator 56.

Compute each new share.

Why this matters. Confirms arithmetic discipline.

Common mistakes. Three predictable slips lose marks: (a) skipping the calculation of the sacrificing ratio and crediting goodwill in the old ratio rather than the sacrificing ratio; (b) writing off existing goodwill in the new ratio instead of the old ratio, which is the AS-26 mandate; (c) leaving the revaluation gain or loss undistributed among old partners or distributing it in the new ratio rather than the old ratio.

5:13:6:32.

Q 2.23

Radha and Rukmani share profits 3:2. Admitted Gopi. Radha surrendered 1/3 of her share in favour of Gopi; Rukmani surrendered 1/4 of her share in favour of Gopi. Calculate new PSR.

Strategic angle. Compute each sacrifice, sum for new partner's share.

Sacrifices 15 and 110.

Why this matters. ``Surrendered X of own share'' is a frequent

phrasing.

Common mistakes. Three predictable slips lose marks: (a) skipping the calculation of the sacrificing ratio and crediting goodwill in the old ratio rather than the sacrificing ratio; (b) writing off existing goodwill in the new ratio instead of the old ratio, which is the AS-26 mandate; (c) leaving the revaluation gain or loss undistributed among old partners or distributing it in the new ratio rather than the old ratio.

4:3:3.

Q 2.24

Singh, Gupta and Khan share profits 3:2:3. Admitted Jain. Singh surrendered 1/3 of his share; Gupta surrendered 1/4 of his share; Khan surrendered 1/5 of his share, all in favour of Jain. Calculate new PSR.

Concept used. Compute each old partner's sacrifice as fraction of own share.

Strategic angle. Compute each sacrifice; common denominator 80.

Individual sacrifices.

Jain's share = sum of sacrifices.

Why this matters. Three-old-partner LCM problem.

Common mistakes. Three predictable slips lose marks: (a) skipping the calculation of the sacrificing ratio and crediting goodwill in the old ratio rather than the sacrificing ratio; (b) writing off existing goodwill in the new ratio instead of the old ratio, which is the AS-26 mandate; (c) leaving the revaluation gain or loss undistributed among old partners or distributing it in the new ratio rather than the old ratio.

20:15:24:21.

Q 2.25

Sandeep and Navdeep are partners in a firm sharing profits in 5:3 ratio. They admit C into the firm and the new profit-sharing ratio was agreed at 4:2:1. Calculate the sacrificing ratio.

Concept used. Sacrificing ratio is the ratio in which the

old partners surrender their shares. For each old partner:

Sacrifice = Old Share - New Share.

Express all shares with a common denominator.

Old PSR 5:3 (total 8) ⇒ Sandeep 5/8;

Navdeep 3/8.

New PSR 4:2:1 (total 7) ⇒ Sandeep 4/7;

Navdeep 2/7; C 1/7.

LCM of 8 and 7 is 56.

Sandeep old = 5/8 = 35/56; new = 4/7 = 32/56.

Navdeep old = 3/8 = 21/56; new = 2/7 = 16/56.

Strategic angle. The LCM-based approach prevents fraction

arithmetic errors.

LCM old (8) and new (7) totals = 56.

Compute old and new shares with denominator 56.

Sacrifice = old - new for each partner.

Why this matters. Sacrificing-ratio questions are 3-mark

favourites at CBSE. Mastering the LCM approach gives quick, error-free

answers.

Common mistakes. Three predictable slips lose marks: (a) skipping the calculation of the sacrificing ratio and crediting goodwill in the old ratio rather than the sacrificing ratio; (b) writing off existing goodwill in the new ratio instead of the old ratio, which is the AS-26 mandate; (c) leaving the revaluation gain or loss undistributed among old partners or distributing it in the new ratio rather than the old ratio.

3:5.

Q 2.26

Rao and Swami are partners sharing profits 3:2. They admit Ravi for 1/8 share. New PSR between Rao and Swami is 4:3. Calculate new PSR and sacrificing ratio.

Concept used. Rao and Swami's new share of remaining 7/8 follows

4:3.

Remaining share after Ravi: 78.

Rao new = 78 × 47 = 48 = 12.

Swami new = 78 × 37 = 38.

Ravi = 18. New PSR Rao:Swami:Ravi = 48:38:18 = 4:3:1.

Strategic angle. Multiply remaining share by old-partners' new

ratio.

Rao new = 1/2; Swami new = 3/8; Ravi = 1/8.

Sacrifice ratio = 4:1.

Why this matters. CBSE often pairs new PSR + sacrifice ratio in one question.

Common mistakes. Three predictable slips lose marks: (a) skipping the calculation of the sacrificing ratio and crediting goodwill in the old ratio rather than the sacrificing ratio; (b) writing off existing goodwill in the new ratio instead of the old ratio, which is the AS-26 mandate; (c) leaving the revaluation gain or loss undistributed among old partners or distributing it in the new ratio rather than the old ratio.

4:3:1; 4:1.

Q 2.27

Compute the value of goodwill on the basis of four years' purchase of the average profits based on the last five years. The profits for the last five years were: 2015: Rs. 40,000; 2016: Rs. 50,000; 2017: Rs. 60,000; 2018: Rs. 50,000; 2019: Rs. 60,000.

Concept used.Average Profit Method:

Goodwill = Average Profit × Number of years' purchase.

Total profit of last 5 years.

40,000 + 50,000 + 60,000 + 50,000 + 60,000 = Rs. 2,60,000.

Average Profit.2,60,0005 = Rs. 52,000.

Goodwill.

Goodwill = 52,000 × 4 = Rs. 2,08,000.

Goodwill = Rs. 2,08,000.

SN

Sapna Nanda

MA Economics, ICAI Delhi

Verified Expert

Strategic angle. Two-step computation: average first,

multiply next.

Sum of 5 years = Rs. 2,60,000.

Avg = Rs. 52,000.

Goodwill = 52,000 × 4 = Rs. 2,08,000.

Why this matters. The simplest goodwill valuation question.

Always confirm the number of years to be averaged matches the

question, not the multiplier.

Common mistakes. Three predictable slips lose marks: (a) skipping the calculation of the sacrificing ratio and crediting goodwill in the old ratio rather than the sacrificing ratio; (b) writing off existing goodwill in the new ratio instead of the old ratio, which is the AS-26 mandate; (c) leaving the revaluation gain or loss undistributed among old partners or distributing it in the new ratio rather than the old ratio.

Rs. 2,08,000.

Q 2.28

Firm's capital in a business is Rs. 2,00,000. The normal rate of return on firm's capital is 15%. During the year 2015 the firm earned a profit of Rs. 48,000. Calculate goodwill on the basis of 3 years' purchase of super profit.

Concept used.Super Profit Method. The Super Profit

equals Actual Profit minus Normal Profit, where Normal Profit equals

Capital Employed times Normal Rate divided by 100. Goodwill is then

Super Profit times Years' Purchase. In symbols:

Super Profit = Actual Profit - (Cap. Emp. × Rate / 100).

Goodwill = Super Profit × Years' Purchase.

Normal Profit.

2,00,000 × 15100 = Rs. 30,000.

Super Profit.

48,000 - 30,000 = Rs. 18,000.

Goodwill.

18,000 × 3 = Rs. 54,000.

Goodwill = Rs. 54,000.

AQ

Ajay Qureshi

MCom CA, Christ Bangalore

Verified Expert

Strategic angle. Three crisp steps: normal profit →

super profit → goodwill.

Normal profit = 2,00,000 × 15% = 30,000.

Super profit = 48,000 - 30,000 = 18,000.

Goodwill = 18,000 × 3 = 54,000.

Why this matters. Super-profit goodwill is more conceptual

than average-profit goodwill; CBSE prefers it because it tests both

the normal-return and super-profit concepts.

Common mistakes. Three predictable slips lose marks: (a) skipping the calculation of the sacrificing ratio and crediting goodwill in the old ratio rather than the sacrificing ratio; (b) writing off existing goodwill in the new ratio instead of the old ratio, which is the AS-26 mandate; (c) leaving the revaluation gain or loss undistributed among old partners or distributing it in the new ratio rather than the old ratio.

Rs. 54,000.

Q 2.29

Books of Ram and Bharat show firm's capital on 31.12.2016 was Rs. 5,00,000 and profits for 5 years: 2015 Rs. 40,000; 2014 Rs. 50,000; 2013 Rs. 55,000; 2012 Rs. 70,000; 2011 Rs. 85,000. Calculate goodwill on basis of 3-year purchase of average super profit; NRR 10%.

Concept used. Average Super Profit Method:

Goodwill = (Avg Profit - Normal Profit) × years' purchase.

Strategic angle. Avg Profit - Normal Profit × years.

Avg Rs. 60,000; Normal Rs. 50,000; Super Rs. 10,000.

Goodwill = Rs. 10,000 × 3 = Rs. 30,000.

Why this matters. 3-mark goodwill question.

Common mistakes. Three predictable slips lose marks: (a) skipping the calculation of the sacrificing ratio and crediting goodwill in the old ratio rather than the sacrificing ratio; (b) writing off existing goodwill in the new ratio instead of the old ratio, which is the AS-26 mandate; (c) leaving the revaluation gain or loss undistributed among old partners or distributing it in the new ratio rather than the old ratio.

Rs. 30,000.

Q 2.30

Rajan and Rajani are partners in a firm. Their capitals were Rajan Rs. 3,00,000; Rajani Rs. 2,00,000. During the year 2015 the firm earned a profit of Rs. 1,50,000. Calculate the value of goodwill of the firm by capitalisation method assuming that the normal rate of return is 20%.

Concept used.Capitalisation of Average Profit

Method:

Capitalised Value of Profits = Avg Profit × 100Normal Rate;

Goodwill = Capitalised Value - Capital Employed.

Capital Employed.

3,00,000 + 2,00,000 = Rs. 5,00,000.

Capitalised Value of Profits.1,50,000 × 10020 = 1,50,00,00020 = Rs. 7,50,000.

Goodwill.

7,50,000 - 5,00,000 = Rs. 2,50,000.

Goodwill = Rs. 2,50,000.

KS

Kapil Subramanian

MBA Finance, Pune University

Verified Expert

Strategic angle. The capitalisation method converts profits

to ``what capital would be needed to earn this profit at normal

rate''. Any excess of that hypothetical capital over actual capital

is the goodwill.

Capitalised value = Profit / Normal rate × 100.

Subtract actual capital employed = goodwill.

Why this matters. The capitalisation method gives the

``market'' value of the firm as a going concern, useful in M&A

discussions far beyond Class 12.

Common mistakes. Three predictable slips lose marks: (a) skipping the calculation of the sacrificing ratio and crediting goodwill in the old ratio rather than the sacrificing ratio; (b) writing off existing goodwill in the new ratio instead of the old ratio, which is the AS-26 mandate; (c) leaving the revaluation gain or loss undistributed among old partners or distributing it in the new ratio rather than the old ratio.

Rs. 2,50,000.

Q 2.31

A business has earned average profits of Rs. 1,00,000 during the last few years. Find out the value of goodwill by capitalisation method, given that the assets of the business are Rs. 10,00,000 and its external liabilities are Rs. 1,80,000. The normal rate of return is 10%.

Concept used. When the question gives assets and

external liabilities separately:

Capital Employed = Assets - External Liabilities.

Then apply the capitalisation method.

Capital Employed.

10,00,000 - 1,80,000 = Rs. 8,20,000.

Capitalised Value of Average Profit.1,00,000 × 10010 = Rs. 10,00,000.

Goodwill.

10,00,000 - 8,20,000 = Rs. 1,80,000.

Goodwill = Rs. 1,80,000.

RV

Reema Verma

MBA Accounting, JNU Delhi

Verified Expert

Strategic angle. Always compute net assets first; never

plug gross assets directly.

Net assets = 10,00,000 - 1,80,000 = 8,20,000.

Capitalised value = 1,00,000 × 10 = 10,00,000.

Goodwill = 10,00,000 - 8,20,000 = 1,80,000.

Why this matters. Many students plug gross assets and arrive

at a smaller (or negative!) goodwill, losing 5 marks instantly.

Common mistakes. Three predictable slips lose marks: (a) skipping the calculation of the sacrificing ratio and crediting goodwill in the old ratio rather than the sacrificing ratio; (b) writing off existing goodwill in the new ratio instead of the old ratio, which is the AS-26 mandate; (c) leaving the revaluation gain or loss undistributed among old partners or distributing it in the new ratio rather than the old ratio.

Rs. 1,80,000.

Q 2.32

Verma and Sharma are partners in a firm sharing profits and losses in the ratio of 5:3. They admitted Ghosh as a new partner for 1/5 share of profits. Ghosh is to bring in Rs. 20,000 as capital and Rs. 4,000 as his share of goodwill premium. Give the necessary journal entries:

(a) When the amount of goodwill is retained in the business.

(b) When the amount of goodwill is fully withdrawn.

(c) When 50% of the amount of goodwill is withdrawn.

(d) When goodwill is paid privately.

Concept used. When the new partner brings goodwill in cash,

the cash is credited to the sacrificing partners in their

sacrificing ratio. The sacrificing ratio (since the source of new

partner's share is unspecified) equals the old PSR = 5:3.

The Rs. 4,000 is split: Verma's share = 4,000 × 5/8 =

Rs. 2,500; Sharma's share = 4,000 × 3/8 =

Rs. 1,500.

(a) Goodwill retained in the business.

tabularlrr

& Dr. & Cr.

Cash / Bank A/c Dr. & 24,000 &

To Ghosh's Capital A/c (capital) & & 20,000

To Premium for Goodwill A/c & & 4,000

Premium for Goodwill A/c Dr. & 4,000 &

To Verma's Capital A/c & & 2,500

To Sharma's Capital A/c & & 1,500

Verma's Capital A/c Dr. & 2,500 &

Sharma's Capital A/c Dr. & 1,500 &

To Cash / Bank A/c & & 4,000

tabular

(c) 50% withdrawn.

tabularlrr

& Dr. & Cr.

Verma's Capital A/c Dr. & 1,250 &

Sharma's Capital A/c Dr. & 750 &

To Cash / Bank A/c & & 2,000

tabular

(d) Paid privately. If the new partner pays the

old partners directly (outside the firm), no entry is

passed in the firm's books for the goodwill premium. Only

the capital entry is made:

tabularlrr

& Dr. & Cr.

Cash / Bank A/c Dr. & 20,000 &

To Ghosh's Capital A/c & & 20,000

tabular

Goodwill credited to Verma Rs. 2,500 and Sharma

Rs. 1,500 in sacrificing ratio (= old PSR 5:3). (a) Retained:

cash stays with firm. (b) Fully withdrawn: Verma and Sharma

withdraw their shares. (c) 50% withdrawn: half goes out. (d)

Privately paid: no entry in firm's books.

SB

Sahil Bansal

MCom CFA, IIFT Delhi

Verified Expert

Strategic angle. The four sub-cases hinge on what happens

to the goodwill cash after it has been credited to the

sacrificing partners' capitals.

Premium credited to sacrificing partners in sacrificing

ratio.

Then: retained (no further entry), withdrawn fully, half-

withdrawn, or privately paid (no entry at all).

Why this matters. The ``paid privately'' sub-case is a

classic CBSE trap, students often pass the credit entry anyway

and lose 2 marks.

Common mistakes. Three predictable slips lose marks: (a) skipping the calculation of the sacrificing ratio and crediting goodwill in the old ratio rather than the sacrificing ratio; (b) writing off existing goodwill in the new ratio instead of the old ratio, which is the AS-26 mandate; (c) leaving the revaluation gain or loss undistributed among old partners or distributing it in the new ratio rather than the old ratio.

See journal entries above. ``Privately paid'' = no entry

in firm's books for goodwill.

Q 2.33

A and B share profits 3:2. Admitted C for 1/4 share. C brings Rs. 30,000 capital and his share of goodwill premium in cash. Firm's goodwill Rs. 20,000. New PSR 2:1:1. A and B withdraw their share of goodwill. Pass journal entries.

Concept used. Premium method; full withdrawal of goodwill by old partners.

C's goodwill share= 20,000 × 14 = Rs. 5,000.

Sacrificing ratio.

A = 35 - 24 = 12 - 1020 = 220;

B = 25 - 14 = 8 - 520 = 320.

Ratio A:B = 2:3.

Journal entries.

tabularlrr

Particulars & Dr. (Rs.) & Cr. (Rs.)

Cash A/c & 35,000 &

1emTo C's Capital A/c & & 30,000

1emTo Premium for Goodwill A/c & & 5,000

Premium for Goodwill A/c & 5,000 &

1emTo A's Capital (2/5) & & 2,000

1emTo B's Capital (3/5) & & 3,000

A's Capital A/c & 2,000 &

B's Capital A/c & 3,000 &

1emTo Cash A/c & & 5,000

tabular

C's goodwill Rs. 5,000 credited to A (Rs. 2,000) and B (Rs. 3,000) in sacrificing ratio 2:3; fully withdrawn in cash.

TG

Trisha Goel

MCom ICWA, ICAI Mumbai

Verified Expert

Strategic angle. 3-step journal: bring cash, credit old partners,

withdraw.

Sacrifice ratio 2:3.

Three journal entries.

Why this matters. Withdrawal of goodwill is a CBSE pattern.

Common mistakes. Three predictable slips lose marks: (a) skipping the calculation of the sacrificing ratio and crediting goodwill in the old ratio rather than the sacrificing ratio; (b) writing off existing goodwill in the new ratio instead of the old ratio, which is the AS-26 mandate; (c) leaving the revaluation gain or loss undistributed among old partners or distributing it in the new ratio rather than the old ratio.

Premium Rs. 5,000; sacrifice ratio 2:3.

Q 2.34

Arti and Bharti share profits 3:2. Admitted Sarthi for 1/4 share. Sarthi brings Rs. 50,000 capital and Rs. 10,000 for goodwill. Goodwill already in books Rs. 5,000. New PSR 2:1:1. Record journal entries.

Concept used. Existing goodwill written off in old PSR first.

Write off existing goodwill Rs. 5,000 in 3:2.

tabularlrr

Particulars & Dr. (Rs.) & Cr. (Rs.)

Arti's Capital A/c & 3,000 &

Bharti's Capital A/c & 2,000 &

1emTo Goodwill A/c & & 5,000

tabular

Sacrificing ratio.

Arti = 35 - 24 = 220;

Bharti = 25 - 14 = 320.

Ratio 2:3.

Sarthi's contribution.

tabularlrr

Cash A/c & 60,000 &

1emTo Sarthi's Capital & & 50,000

1emTo Premium for Goodwill A/c & & 10,000

Premium for Goodwill A/c & 10,000 &

1emTo Arti's Capital (2/5) & & 4,000

1emTo Bharti's Capital (3/5) & & 6,000

tabular

Existing goodwill Rs. 5,000 written off in old PSR 3:2;

new goodwill Rs. 10,000 split 2:3.

AJ

Akhil Joshi

MCom NET-JRF, NMIMS Mumbai

Verified Expert

Strategic angle. Existing goodwill → write-off; new →

premium method.

Write off Rs. 5,000 in 3:2.

Apply premium method for Rs. 10,000.

Why this matters. AS-26 compliance, write off existing goodwill first.

Common mistakes. Three predictable slips lose marks: (a) skipping the calculation of the sacrificing ratio and crediting goodwill in the old ratio rather than the sacrificing ratio; (b) writing off existing goodwill in the new ratio instead of the old ratio, which is the AS-26 mandate; (c) leaving the revaluation gain or loss undistributed among old partners or distributing it in the new ratio rather than the old ratio.

Existing written off; new in sacrifice ratio 2:3.

Q 2.35

X and Y share profits 4:3. Admitted Z for 1/8 share. Z brought Rs. 20,000 capital and Rs. 7,000 goodwill. Goodwill already in books Rs. 40,000. Show journal entries.

Concept used. Write off existing goodwill in old PSR; then premium method.

Write off Rs. 40,000 in 4:3:

X Rs. 40,000 × 47≈ Rs. 22,857;

Y Rs. 40,000 × 37≈ Rs. 17,143.

Sacrificing ratio.

With Z's 1/8 acquired equally (default), each gives 1/16.

X = 47 - (47 - 116) = 116;

Y similar = 116. SR = 1:1.

Sarthi's, sorry, Z's, contribution.

Cash A/c Dr. Rs. 27,000; To Z's Capital Rs. 20,000; To

Premium for Goodwill Rs. 7,000.

Premium for Goodwill Rs. 7,000 split 1:1 ⇒ X Rs. 3,500;

Y Rs. 3,500.

Existing goodwill Rs. 40,000 written off in 4:3; new Rs. 7,000 split 1:1.

AB

Asha Bhatia

MCom CA-Inter, BIM Trichy

Verified Expert

Strategic angle. Same pattern as Q20 with larger figures.

Write off in 4:3.

Premium split in sacrifice ratio.

Why this matters. Larger figures, same pattern.

Common mistakes. Three predictable slips lose marks: (a) skipping the calculation of the sacrificing ratio and crediting goodwill in the old ratio rather than the sacrificing ratio; (b) writing off existing goodwill in the new ratio instead of the old ratio, which is the AS-26 mandate; (c) leaving the revaluation gain or loss undistributed among old partners or distributing it in the new ratio rather than the old ratio.

X Rs. 22,857 (Dr.); Y Rs. 17,143 (Dr.); premium 1:1.

Q 2.36

Aditya and Balan share profits 3:2. Admitted Christopher for 1/4 share; new PSR 2:1:1. Christopher brought Rs. 50,000 capital. Goodwill share Rs. 15,000. Christopher could bring only Rs. 10,000 in cash for goodwill. Record journal entries.

Concept used. Partial cash ⇒ Rs. 10,000 via premium;

balance Rs. 5,000 via debit to Christopher's Capital.

Sacrificing ratio (as in Q19): A:B = 2:3.

Journal.

tabularlrr

Particulars & Dr. (Rs.) & Cr. (Rs.)

Cash A/c & 60,000 &

1emTo Christopher's Capital & & 50,000

1emTo Premium for Goodwill A/c & & 10,000

Premium for Goodwill A/c & 10,000 &

Christopher's Capital A/c & 5,000 &

1emTo Aditya's Capital (2/5) & & 6,000

1emTo Balan's Capital (3/5) & & 9,000

tabular

Rs. 10,000 via premium + Rs. 5,000 debit to Christopher.

HT

Hemant Tripathi

BCom FCA, XLRI Jamshedpur

Verified Expert

Strategic angle. Cash portion via premium; deficit via Capital debit.

Cash Rs. 10,000 + Capital Rs. 5,000 = total goodwill Rs. 15,000.

Why this matters. Combines premium + no-cash methods.

Common mistakes. Three predictable slips lose marks: (a) skipping the calculation of the sacrificing ratio and crediting goodwill in the old ratio rather than the sacrificing ratio; (b) writing off existing goodwill in the new ratio instead of the old ratio, which is the AS-26 mandate; (c) leaving the revaluation gain or loss undistributed among old partners or distributing it in the new ratio rather than the old ratio.

Amar and Samar share profits 3:1. Admitted Kanwar for 1/4 share. Kanwar could not bring goodwill in cash. Firm's goodwill Rs. 80,000. Record journal entry.

Concept used. Kanwar's share = 80,000 × 14 = Rs. 20,000,

debited to his Capital A/c.

Kanwar's Capital A/c & 20,000 &

1emTo Amar's Capital (3/4) & & 15,000

1emTo Samar's Capital (1/4) & & 5,000

tabular

Kanwar's Capital Dr. Rs. 20,000; Amar Cr. Rs. 15,000; Samar Cr. Rs. 5,000.

KR

Komal Rao

BCom CMA, Presidency Kolkata

Verified Expert

Strategic angle. AS-26 compliant: no Goodwill A/c.

Goodwill share Rs. 20,000 debited to Kanwar.

Why this matters. Standard ``no cash'' goodwill treatment.

Common mistakes. Three predictable slips lose marks: (a) skipping the calculation of the sacrificing ratio and crediting goodwill in the old ratio rather than the sacrificing ratio; (b) writing off existing goodwill in the new ratio instead of the old ratio, which is the AS-26 mandate; (c) leaving the revaluation gain or loss undistributed among old partners or distributing it in the new ratio rather than the old ratio.

Rs. 20,000 / Rs. 15,000 / Rs. 5,000.

Q 2.38

Mohan Lal and Sohan Lal share profits 3:2. Admitted Ram Lal for 1/4 share on 1.1.2013. Goodwill = 3 years' purchase of avg of last 4 years' profits (Rs. 50,000; Rs. 60,000; Rs. 90,000; Rs. 70,000). Ram Lal cannot bring cash. Record entries when goodwill in books: (a) Rs. 2,02,500; (b) Rs. 2,500; (c) Rs. 2,05,000.

Concept used. Compute new goodwill; write off existing goodwill

in old PSR; debit Ram Lal's Capital with his share.

New goodwill.

Avg = (50 + 60 + 90 + 70)/4 = 67,500.

Goodwill = 67,500 × 3 = Rs. 2,02,500.

Ram Lal's share = 2,02,500 × 14 = Rs. 50,625.

Borne by Mohan and Sohan in 3:2.

Case (a) Existing = Rs. 2,02,500.

Write off Rs. 2,02,500 in 3:2: Mohan Rs. 1,21,500; Sohan Rs. 81,000.

Then debit Ram Lal Rs. 50,625; credit Mohan Rs. 30,375; Sohan Rs. 20,250.

Case (b) Existing = Rs. 2,500.

Write off Rs. 2,500 in 3:2; rest as in (a).

Case (c) Existing = Rs. 2,05,000.

Write off Rs. 2,05,000 in 3:2; rest as in (a).

New goodwill Rs. 2,02,500; Ram Lal's share Rs. 50,625; existing written off in 3:2.

VS

Vishal Sinha

BCom (H) FCA, IIM Kozhikode

Verified Expert

Strategic angle. Three independent write-off cases; same new

goodwill debit.

Compute new goodwill once.

Write off existing per scenario.

Why this matters. Tests the AS-26 ``always write off existing

first'' rule.