The NCERT Class 10 Economics Book PDF Chapter 3 Money and Credit brings together every definition, case study and credit term that the CBSE Class 10 Social Science board paper actually tests.

The chapter sits in Understanding Economic Development and runs to about 16 printed pages in the 2026-27 reprint, with the Salim and Swapna credit stories, two pie-chart graphs and the Grameen Bank example.

- Board Weightage: 5 to 6 marks in the Class 10 Social Science (Economics unit) paper, usually one short answer plus one source-based question on credit

- What's Inside: money as a medium of exchange, modern forms of money, loan activities of banks, terms of credit, formal and informal credit, Self-Help Groups and Grameen Bank

This NCERT class 10 economics book pdf chapter 3 Money and Credit is the original NCERT print, hosted unmodified by Collegedunia, mapped to the 2026-27 syllabus and checked against the last five years of CBSE board papers.

What the Money and Credit Class 10 Chapter 3 PDF Covers

The chapter opens by asking why we use money, then explains modern forms of money, how banks lend, and what makes credit help or hurt a borrower. It ends with how the poor get loans through Self-Help Groups and the Grameen Bank.

- Money: double coincidence of wants, currency and demand deposits, cheque payments

- Credit: the Salim and Swapna stories, plus the four terms of credit

- Credit sources: formal lenders (banks, cooperatives) versus informal lenders (moneylenders, traders), and how the RBI supervises the formal sector

- Help for the poor: Self-Help Groups and the Grameen Bank case study

Money as a Medium of Exchange and the Double Coincidence of Wants

Why do we trade in money instead of swapping goods directly? Money removes a hard condition called the double coincidence of wants. This is the most common opening question of the chapter.

- Barter system: goods are swapped directly, so a shoe maker must find a wheat farmer who also wants shoes.

- Double coincidence of wants: what one person wants to sell is exactly what the other wants to buy.

- Money as a medium of exchange: the shoe maker can sell shoes for money and then buy wheat from anyone.

So money removes the need for a double coincidence of wants, a favourite three-mark board question.

Money and Credit Class 10 Explained in Simple Language

Source: Magnet Brains on YouTube

Modern Forms of Money: Currency and Demand Deposits in Chapter 3

Modern money is no longer made of gold or grain. The chapter splits it into two forms, both linked to the banking system.

- Currency: paper notes and coins. In India only the Reserve Bank of India issues currency notes on behalf of the central government, and no one can refuse a payment in rupees.

- Demand deposits: money in bank accounts, withdrawn on demand and earning interest.

- Cheque payments: a cheque tells the bank to pay a set amount from the payer's account, so payments settle without cash.

So currency and demand deposits together make up modern money, both depending on the banking system.

Loan Activities of Banks and How Banks Earn Income

Banks hold only a small share of deposits as cash and lend out the rest. This mediation between depositors and borrowers is the engine of the chapter.

- Banks in India keep only about 5 per cent of deposits as cash, ready for depositors who withdraw.

- The major portion of deposits is given out as loans.

- Banks charge more interest on loans than they pay on deposits. This difference is the main source of bank income.

So the gap between interest charged and interest paid is the bank's main income.

Two Credit Situations: Salim's Festival Order and Swapna's Debt-Trap

Credit means a loan: the lender gives money or goods against a promise of future payment. The chapter uses two stories to show credit can help in one case and hurt in another, the most-asked part of the chapter.

| Borrower | Why credit was taken | Outcome |

|---|---|---|

| Salim (shoe manufacturer) | To meet working-capital needs for a festival-season order | Delivered the order, made a good profit and repaid the loan. Credit helped. |

| Swapna (small farmer) | To meet the cost of growing groundnut | The crop failed, the debt grew, and she had to sell part of her land. Credit pushed her into a debt-trap. |

So whether credit helps depends on the risk in the situation. Credit in a risky situation can push a borrower into a debt-trap, as it did for Swapna.

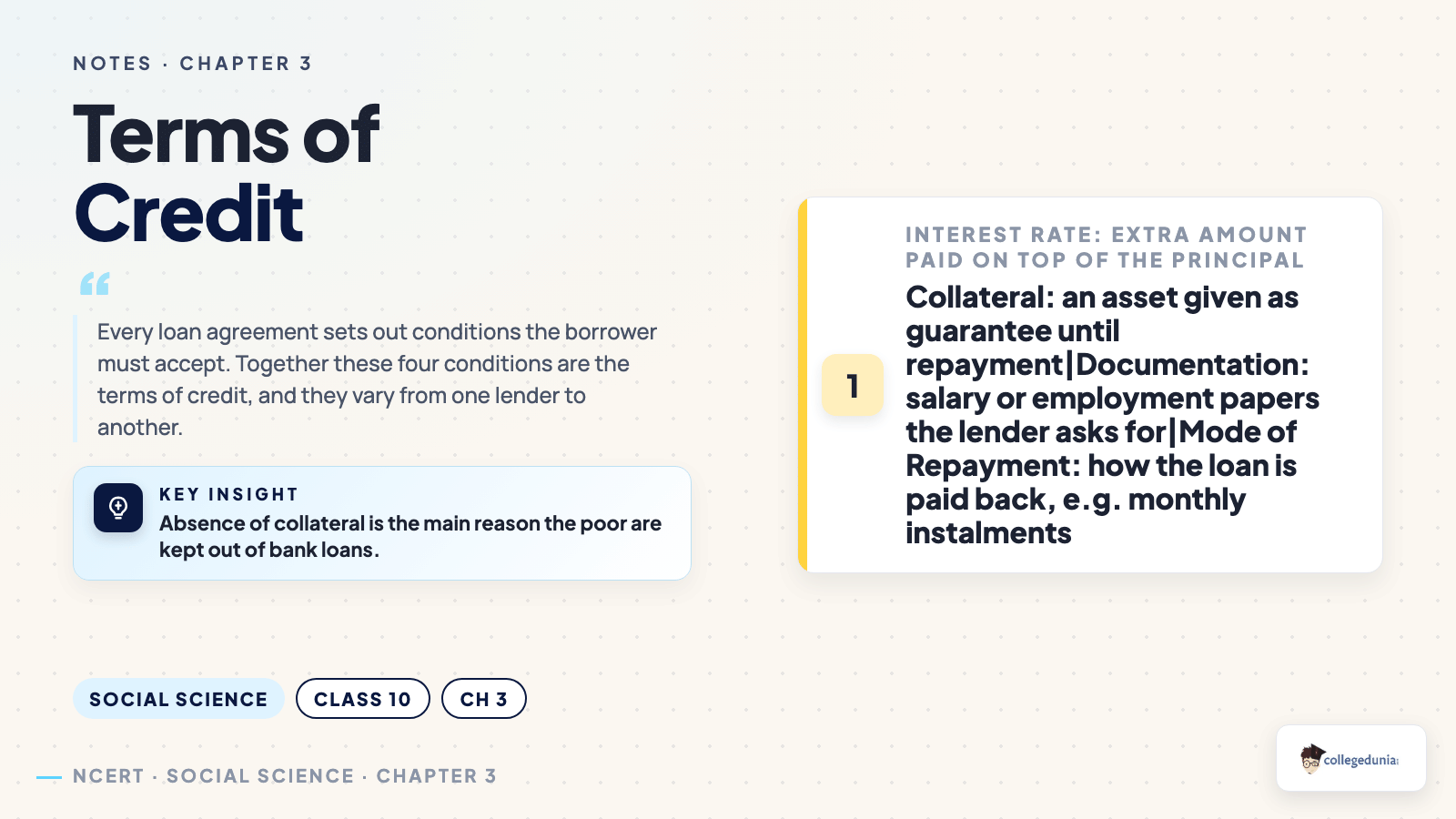

Terms of Credit: Interest Rate, Collateral, Documentation and Repayment

Every loan agreement sets out four conditions called the terms of credit, which change from one lender to another. This is a frequent 3-mark question.

- Interest rate: the extra amount the borrower pays on top of the principal.

- Collateral: an asset (land, building, vehicle, deposits) given as a guarantee until the loan is repaid. If the borrower fails to repay, the lender can sell it.

- Documentation: papers like salary or employment records the lender asks for before lending.

- Mode of repayment: how the loan is paid back, such as monthly instalments.

Tip: Absence of collateral is the main reason the poor are kept out of bank loans, which leads into the next section.

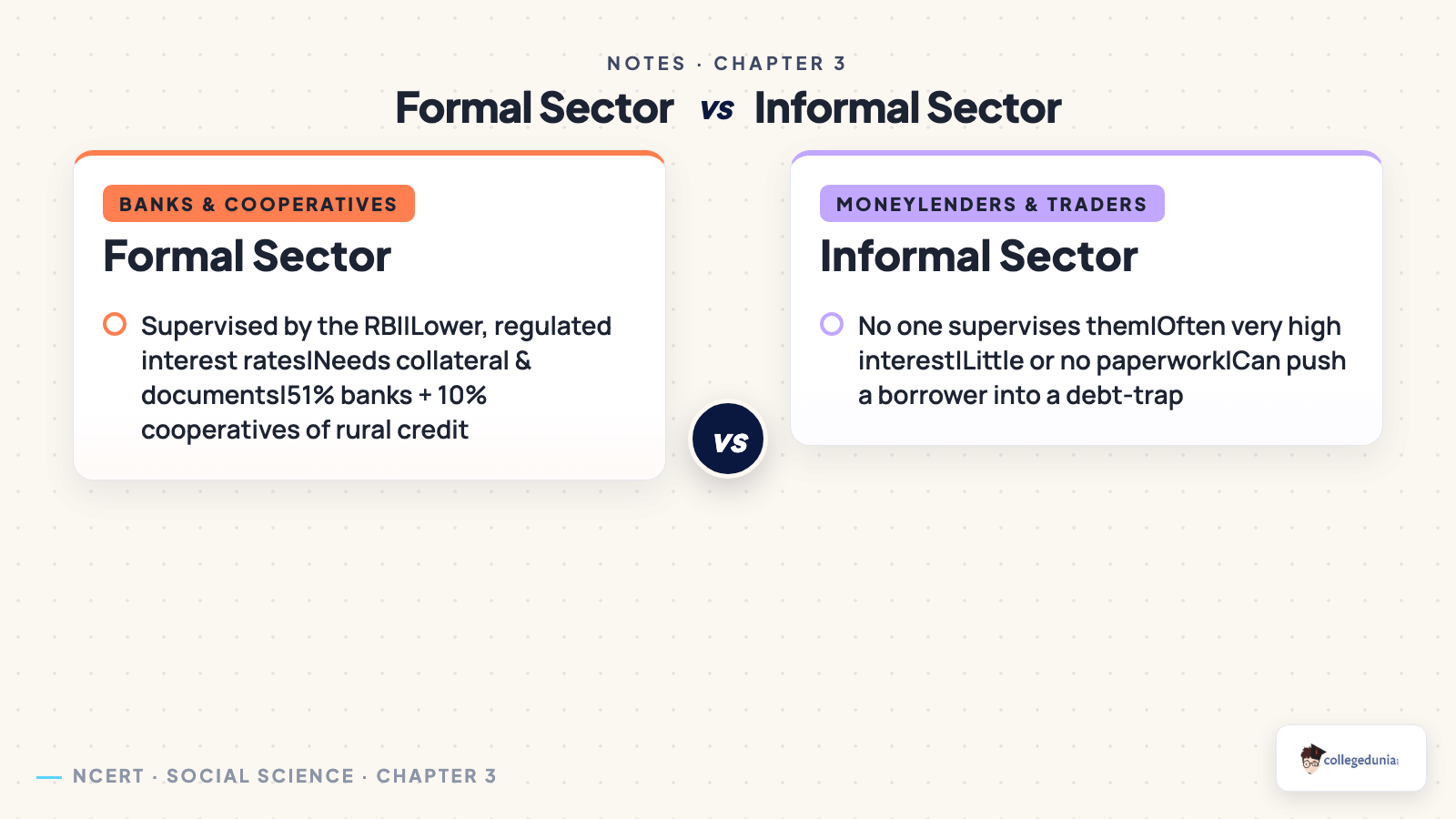

Formal and Informal Sources of Credit in India

Loans come from two groups of lenders. Graph 1 shows how much credit each source gives rural households, and why the formal sector is cheaper and safer. This split is the spine of the second half.

| Feature | Formal Sector | Informal Sector |

|---|---|---|

| Lenders | Banks and cooperatives | Moneylenders, traders, employers, relatives, friends |

| Supervision | Supervised by the Reserve Bank of India | No organisation supervises them |

| Interest rate | Lower, regulated rates | Often very high rates, set freely |

| Effect on borrower | Cheap credit supports earnings and development | High cost can lead to a debt-trap |

From Graph 1, commercial banks give 51 per cent and cooperatives 10 per cent of rural credit, while moneylenders give about 23 per cent. The RBI checks that banks keep the minimum cash balance and lend to small borrowers too. The formal sector still meets only about half the credit needs of rural households.

Self-Help Groups and the Grameen Bank: Credit for the Poor

The poor often cannot get bank loans because they have no collateral and no proper papers. The chapter shows two ways to give them cheap credit instead of depending on moneylenders.

- Self-Help Groups (SHGs): 15 to 20 members, usually women, who meet and save regularly and take small loans from the pooled savings at a fair rate.

- SHGs and banks: after saving for a year or two, the group becomes eligible for a bank loan even without collateral, because the group is responsible for repayment.

- Grameen Bank of Bangladesh: started by Professor Muhammad Yunus, it lends to poor women and proved they are reliable borrowers.

So SHGs help poor women borrow without collateral and become self-reliant, which is why the chapter calls affordable credit crucial for development.

Class 10 Economics Chapter 3 Exam Weightage and Question Trends

Money and Credit is one of the most scoring chapters in the Economics unit, appearing in nearly every paper over the last five cycles, mostly as a short answer plus a source-based question.

| Year | Question Type Asked | Approx. Marks |

|---|---|---|

| 2025 | Difference between formal and informal sources of credit | 3 |

| 2024 | Terms of credit with the role of collateral | 3 |

| 2023 | Source-based question on Self-Help Groups | 4 |

| 2022 | How money solves the double coincidence of wants | 5 |

| 2021 | Loan activities of banks and how banks earn income | 3 |

Credit terms, the two credit situations and the formal-informal split cover most of the marks. Revise the comparison tables first.

Student Feedback on the Money and Credit Chapter

In a Collegedunia poll of 14,860 Class 10 students conducted before the 2026 boards, 71% of students rated the four terms of credit as the part they revise most. Most students said the Salim and Swapna comparison was the easiest way to remember when credit helps or hurts.

Source: 2026-27 Class 10 Economics student poll. Sample of 14,860 students from CBSE schools across 14 states.

Common Mistakes Students Make in the Money and Credit Chapter

- Writing that the RBI prints currency for itself. The RBI issues notes on behalf of the central government.

- Mixing up collateral (an asset given as guarantee) with the interest rate. They are two separate terms of credit.

- Saying credit always helps. It helped Salim but pushed Swapna into a debt-trap, so the outcome depends on the risk.

- Calling cooperatives an informal source. Banks and cooperatives are both formal sources of credit.

Key Features of the Official NCERT Class 10 Economics Book PDF

- Reprint Edition: 2026-27, aligned to the current CBSE syllabus

- Publisher: NCERT, New Delhi

- Book: Understanding Economic Development, Class 10 Economics

- File Type: searchable text PDF, mobile-readable and print-ready

Related Resources for Money and Credit Class 10

| Resource | Link |

|---|---|

| NCERT Solutions | Money and Credit Class 10 NCERT Solutions |

| Notes | Money and Credit Class 10 Notes |

| Handwritten Notes | Money and Credit Class 10 Handwritten Notes |

NCERT Book PDF for Class 10 Economics: All Chapters

All five chapters of Understanding Economic Development are available on Collegedunia. Use the table below to download any chapter PDF directly.

| Chapter | NCERT Book PDF |

|---|---|

| Chapter 1 | Development NCERT Book PDF |

| Chapter 2 | Sectors of the Indian Economy NCERT Book PDF |

| Chapter 4 | Globalisation and the Indian Economy NCERT Book PDF |

| Chapter 5 | Consumer Rights NCERT Book PDF |

Money and Credit Class 10 NCERT Book PDF Frequently Asked Questions

Ques. Is this the official NCERT Class 10 Economics Chapter 3 textbook PDF?

Ans. Yes. The file is the original NCERT Class 10 Economics Chapter 3 Money and Credit from Understanding Economic Development, 2026-27 reprint, hosted unmodified for free student download.

Ques. How many pages is the Money and Credit Class 10 chapter?

Ans. The chapter runs to about 16 pages in the 2026-27 NCERT reprint, including the money section, the two credit situations, the terms of credit, the formal and informal credit graphs and the end-of-chapter exercises.

Ques. What is the board weightage of Class 10 Economics Chapter 3?

Ans. Money and Credit carries roughly 5 to 6 marks in the CBSE Class 10 Social Science board paper, usually as one short answer plus one source-based question on credit, Self-Help Groups or the terms of credit.

Ques. What is the double coincidence of wants in this chapter?

Ans. Double coincidence of wants means what one person wants to sell is exactly what the other wants to buy. It is needed in a barter system, and money removes this condition by acting as a medium of exchange.

Ques. What are the terms of credit in Class 10 Economics?

Ans. The terms of credit are the interest rate, collateral, documentation and the mode of repayment. Together these conditions make up every loan agreement, and they vary from one lender to another.

Ques. Where can I get the ncert solutions for Class 10 Economics Chapter 3?

Ans. The Money and Credit Class 10 NCERT Solutions page linked above works through every textbook exercise question with step-by-step answers, mapped to the 2026-27 syllabus.

Ques. Is the NCERT Class 10 Economics book PDF free to download?

Ans. Yes. NCERT textbooks are open educational resources published by the Government of India and are free to download and use for study.

Ques. What is the difference between formal and informal sources of credit?

Ans. Formal sources are banks and cooperatives, supervised by the Reserve Bank of India and charging lower rates. Informal sources are moneylenders, traders and employers, who are not supervised and often charge very high interest.

Comments