Commerce Mentor | B.Com (Hons) Student, SRCC | Updated on - May 25, 2026

A full Schedule III Balance Sheet appears in almost every CBSE Class 12 Accountancy paper and can carry up to 8 marks in Part B. The accountancy class 12 NCERT solutions chapter 7 Financial Statements of a Company here solve all 20 textbook questions in the exact Companies Act 2013 format examiners expect. The free 2026-27 PDF is prepared by Collegedunia's commerce desk.

CBSE Weightage

6 to 8 marks in Part B (Financial Statements of a Company)

Question Mix

20 NCERT questions: 5 Short Answer, 9 Long Answer, 6 Balance Sheet numericals

CUET (UG) Relevance

2 to 3 objective questions on Schedule III heads and disclosure

Part 2 Chapter 3 Financial Statements of a Company NCERT Solutions PDF

20 NCERT Questions | 6 Full Balance Sheets Solved | Schedule III Format · Class 12 Accountancy Part 2 Chapter 3, 2026-27 NCERT

Every numerical is solved as a vertical Schedule III Balance Sheet with Notes to Accounts attached, exactly as a CBSE answer script should look.

These solutions are reviewed by Chartered Accountants and senior CBSE Commerce educators, mapped to the 2026-27 NCERT Accountancy Part B textbook, and cross-checked against the last five years of board papers.

Financial Statements of a Company Weightage Across Class 12 Accountancy Chapters

The visual below maps the typical CBSE Part B marks distribution, averaged over the last five board papers. Part 2 Chapter 3 is the gateway to Part B because every ratio, cash flow and analysis question in later chapters reads off the Schedule III Balance Sheet you build here.

Part 2 Ch 1 Accounting for Share Capital

8 marks

Part 2 Ch 2 Issue and Redemption of Debentures

6 marks

Part 2 Ch 3 Financial Statements of a Company

8 marks

Part 2 Ch 4 Analysis of Financial Statements

6 marks

Part 2 Ch 5 Accounting Ratios

8 marks

Part 2 Ch 6 Cash Flow Statement

8 marks

Class 12 Accountancy Part 2 Chapter 3 Financial Statements Of A Company NCERT Solutions

How will Collegedunia's NCERT Solutions Help You with Financial Statements of a Company?

This chapter is less about computation and more about presentation, so the solutions train the format that earns the marks.

Schedule III Format Discipline: Every numerical is a vertical Balance Sheet with the prescribed main heads and sub-heads, so you internalise the order examiners reward.

Notes to Accounts Attached: Each Balance Sheet carries its supporting Notes to Accounts, because CBSE deducts marks when the note schedule is missing.

2026-27 NCERT Alignment: Solutions match the current 2026-27 Accountancy Part B textbook and the Companies Act 2013 Schedule III.

Theory Answers in Board Length: Short and Long Answer theory is written to the length a 3-mark or 4-mark CBSE answer expects, not compressed to one line.

NCERT Solutions Class 12 Accountancy Part 2 Chapter 3: Question-Type Distribution

The 20 NCERT questions split into a theory block and a numerical block. The theory questions are quick recall; the Balance Sheet numericals need full-format practice.

Question Type

Count

What It Tests

Typical Board Marks

Short Answer (theory)

5

Meaning, objectives, limitations, importance to users

1 to 3 marks

Long Answer (theory)

9

Nature and significance, formats explained, recorded-facts statement

4 to 6 marks

Balance Sheet numericals

6

Preparing the Balance Sheet under Schedule III with Notes to Accounts

3 to 8 marks

The numerical block is where most marks are won or lost. Six full Balance Sheet questions in the NCERT carry the weight of roughly three board questions.

Important Topics in Class 12 Accountancy Part 2 Chapter 3 Financial Statements of a Company

The chapter has a small, well-defined topic list. Cover all of it, because CBSE rotates the numerical between the same heads every year.

Nature and objectives: the recorded-facts, accounting-conventions and personal-judgement framing.

Statement of Profit and Loss format: revenue from operations, other income, expenses, profit before tax.

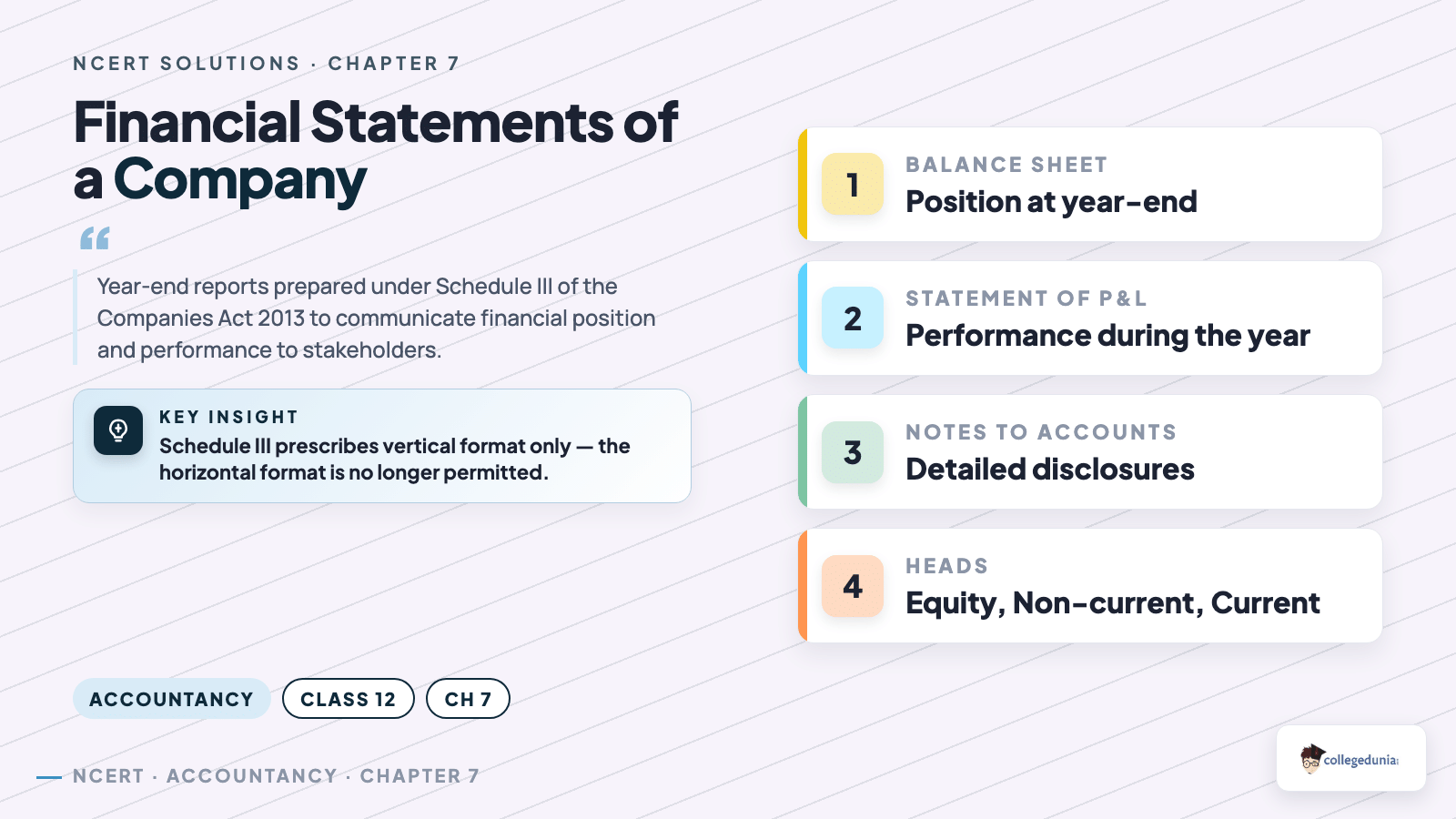

Balance Sheet under Schedule III: Equity and Liabilities then Assets, in the prescribed order.

Major heads and sub-heads: Shareholders' Funds, Non-Current and Current Liabilities, Non-Current and Current Assets.

Notes to Accounts: share capital, reserves and surplus, long-term borrowings, fixed assets.

Special items: preliminary expenses, discount on issue of debentures, contingent liabilities.

Quick Tip: Write the Schedule III five-line head skeleton on your rough sheet first, then slot each item from the question into it. This prevents the most common presentation error in the chapter.

Common Question Stems CBSE Uses for Financial Statements of a Company

CBSE phrases this chapter in a few recurring stems; the stem tells you whether the answer is theory or a full Balance Sheet.

Stem in the paper

What the examiner wants

"Under which major head and sub-head will the item be shown..."

One-line classification per item, no Balance Sheet

"Prepare the Balance Sheet of ... Ltd. as per Schedule III"

Full vertical Balance Sheet plus Notes to Accounts

"State any three limitations (or objectives) of financial statements"

Pointwise theory, one mark per valid point

"Financial statements reflect recorded facts, conventions and judgements. Explain."

Three-part explanation, one part per phrase

The classification stem and the full Balance Sheet stem together carry most of the chapter's board marks.

Financial Statements of a Company Previous Year Questions Weightage (2021 to 2026)

This chapter is a Part B fixture. The full-format Balance Sheet appears almost every year, usually with a shorter classification question. CUET (UG) tests the same heads in objective form.

Year

CBSE Board

CUET (UG)

2026

Pending (board exam in progress)

Pending (exam rescheduled)

2025

Balance Sheet under Schedule III (6 marks) + head/sub-head classification (3 marks)

2 objective questions on major heads

2024

Balance Sheet preparation with Notes to Accounts (6 marks)

3 objective questions on disclosure

2023

Classification of items under Schedule III (4 marks)

The pattern is stable: one full Balance Sheet plus one shorter theory or classification question. In four of the last five board papers, a full Schedule III Balance Sheet carried 6 marks.

Sample Solved Question: Balance Sheet of Black Swan Ltd. (NCERT Q21)

This is the full-format numerical that defines the chapter. The marks come from the correct heads, sub-heads and matching Notes to Accounts, not from arithmetic.

Question: Prepare the Balance Sheet of Black Swan Ltd. as at 31st March 2017 from balances such as Equity Share Capital, General Reserve, 10% Debentures, Trade Payables, Fixed Assets (Tangible), Inventories, Trade Receivables and Cash at Bank, as per Schedule III of the Companies Act 2013.

Step 1 - Skeleton. Write I. Equity and Liabilities (Shareholders' Funds, Non-Current, Current) then II. Assets (Non-Current, Current).

Step 2 - Place balances. Equity Share Capital and General Reserve under Shareholders' Funds; 10% Debentures as Long-Term Borrowings; Trade Payables under Current Liabilities.

Step 3 - Assets. Fixed Assets (Tangible) become Property, Plant and Equipment; Inventories, Trade Receivables and Cash at Bank are Current Assets.

Step 4 - Notes and verify. Attach numbered Notes to Accounts for each composite head, cross-reference them on the face, and confirm Equity and Liabilities equals Assets. A mismatch usually means a wrong head, not an arithmetic slip.

Quick Tip: Write the Note number on the face against the item and label the note with the same number. CBSE awards the note marks only when the cross-reference is visible.

The full working for every Balance Sheet numerical, including the complete Notes to Accounts, is in the PDF on this page.

Common Mistakes Students Make in Financial Statements of a Company

This chapter loses marks on presentation, not numbers. Avoid these errors to protect almost the entire weightage.

Watch Out: Writing the Balance Sheet in the old horizontal (T) format. Schedule III requires the vertical format only. A horizontal Balance Sheet can lose the entire presentation mark even when every figure is correct.

Skipping the Notes to Accounts: the Balance Sheet face alone is incomplete; each composite head needs its supporting note.

Wrong head for special items: preliminary expenses and discount on issue of debentures are not assets under the current treatment; classify them as the textbook directs.

Misclassifying current vs non-current: a bank loan repayable within twelve months is a current liability, not a long-term borrowing.

Listing contingent liabilities on the face: they are disclosed in the Notes, never added into the Balance Sheet total.

Wrong head order: Equity and Liabilities before Assets, and the prescribed sub-head sequence within each.

A single misclassified item can break the Balance Sheet total and cascade into lost marks on the linked Notes to Accounts.

How to Study Financial Statements of a Company for Class 12 Boards

This is a high-return chapter for a small time investment, because the format is fixed and repeats every year.

Day 1: learn the Schedule III skeleton: main heads and sub-heads for both halves. Write it from memory until it is automatic.

Day 2: solve all 6 NCERT Balance Sheet numericals with full Notes to Accounts before checking the solution.

Day 3: revise the theory questions and one classification drill.

Total time required is about 5 to 6 hours, low for a chapter that reliably returns 6 to 8 marks.

Remember: Master the Schedule III order with the mnemonic "Some Now Care, No Care" - Shareholders' Funds, Non-Current Liabilities, Current Liabilities, then Non-Current Assets, Current Assets.

All NCERT Solutions for Financial Statements of a Company with Step-by-Step Working

Every NCERT textbook question for Class 12 Accountancy Part 2 Chapter 3 Financial Statements of a Company is listed below with its full Solution and Expert Solution hidden inside collapsible tabs. Click Check Solution to reveal the step-by-step working; click Expert Solution for the expanded explanation.

Questions

Q 7.1

Question text in bold (handled automatically).

% Use

caption INSIDE the

% question text if the NCERT statement quotes a figure.

% Concept used.

%

%

...

...

>

%

% ....

% DIAGRAMS ARE REQUIRED whenever they aid understanding: see

% SKILL.md for the subject-specific list of must-draw cases.>

%

%

%

Step 1: prose + equation, every algebraic move shown.

%

Step 2: ...

%

Step 3: ...

%

%

% Final answer.

%

FS

Firstname Surname

Degree, Institution

Verified Expert

% Strategic angle. ...

%

%

%

...

%

...

%

%

% Why this matters. ...

%

% Same final answer, phrased crisply.

%

Q 7.2

State the meaning of financial statements.

Concept used.Financial statements are the end

products of the accounting process. They are the formal records that

summarise, in money terms, the financial performance and financial

position of a business for an accounting period. For a company, the

two main financial statements are the Statement of Profit

and Loss (it shows how much profit or loss the company earned during

the year) and the Balance Sheet (it shows what the company

owns and owes on the last day of the year). A Cash Flow Statement and

the Notes to Accounts go along with them.

Identify what the statements report. Financial statements

present two things: the operating results of the year

(profit or loss) and the financial position at the

year-end (assets, liabilities and capital).

State who prepares them and why. The management prepares them

at the close of the accounting year to communicate the

firm's results to owners, lenders, government and other

interested parties who cannot see the books directly.

Note the basis. They are prepared from the recorded

transactions, using accepted accounting concepts, conventions

and some personal judgement (for example, the estimate of

depreciation or doubtful debts).

Financial statements are the summarised statements of

recorded financial data, prepared at the end of an accounting period,

that show a company's profit or loss for the period and its financial

position (assets, liabilities and capital) on the closing date.

AI

Aditi Iyer

M.Sc Statistics, ISI Kolkata

Verified Expert

Quick reading. Think of financial statements as a company's

annual ``report card''. One sheet grades the year's performance

(profit or loss), the other photographs the company's wealth on the

closing date (the Balance Sheet). To define them precisely we must

pin down four things: what they report, who prepares

them, from what data they are built, and for whom.

What: operating results (profit/loss) and financial

position (assets, liabilities, capital).

Who: the company's management, at the close of every

accounting year.

From what: the recorded transactions, processed

through accepted accounting concepts and conventions.

For whom: owners and outsiders who cannot inspect the

books directly.

Fix the scope. Two questions every reader asks:

``Did the company make money this year?'' and ``How strong is

it right now?'' A financial statement is the document that

answers exactly these two questions in money terms, so the

definition must mention both performance and position.

Map each question to a statement. The Statement of

Profit and Loss answers the first by netting total revenue

against total expenses to give profit or loss. The Balance

Sheet answers the second by listing all assets on one side

and all claims (liabilities plus owners' funds) on the other,

the two totals always being equal.

State the basis. Both statements are built from

recorded data only, valued at historical cost, and shaped by

accounting concepts (going concern, accounting period) and

some personal estimates (depreciation, doubtful debts). So

the definition is incomplete unless it says ``summarised from

recorded financial data''.

Assemble the definition. Combining the scope, the

period, and the basis gives a single precise sentence (see

the boxed answer), which is exactly what an examiner expects

for a ``state the meaning'' question.

Why this matters. The definition fixes the scope: financial

statements are summaries of recorded data, not forecasts, so

they look backward, not forward. Every analysis technique in the next

two chapters takes these backward-looking summaries as its raw input.

Financial statements are period-end summaries of recorded

financial data that report a company's profitability (Statement of

Profit and Loss) and its financial position (Balance Sheet) on the

closing date.

Q 7.3

What are the limitations of financial statements?

Concept used. A limitation is a built-in weakness

that restricts how far we can rely on a financial statement. Because

financial statements mix recorded facts, accounting conventions and

personal judgement, they cannot give a perfect picture. The NCERT

text lists the following limitations.

Do not reflect current values. Statements are

prepared on the historical cost basis, so assets

are shown at their original cost, not at today's market

value. The figures can therefore be out of date.

Ignore qualitative elements. Only items that can be

expressed in money are recorded. The quality of management,

staff loyalty and customer satisfaction are valuable but do

not appear anywhere.

Affected by personal judgement. Choices such as the

depreciation method, valuation of inventory and the

provision for doubtful debts depend on the accountant's

judgement, so two firms can show different profits for the

same facts.

Based on accounting concepts and conventions. Use of

the going-concern and conservatism conventions can make the

statements depart from economic reality.

Show position at one point only. The Balance Sheet

is a snapshot on the closing date; it may not represent the

firm's position through the rest of the year.

Financial statements are limited because they use

historical cost (not current value), ignore non-money (qualitative)

items, are influenced by personal judgement, rest on accounting

conventions, and show the position at only a single date.

KM

Karan Mehta

M.Com, Delhi School of Economics

Verified Expert

Structural observation. Instead of memorising five separate

points, group the limitations by their root cause. Every limitation

in this chapter traces back to one of three roots: a

measurement-base problem, a judgement problem, or a

timing problem. Naming the root makes the answer both shorter

to recall and easier to defend in a follow-up question.

Measurement-base root: how figures are valued and what gets

measured at all.

Judgement root: where the accountant's estimate enters.

Timing root: the single date on which position is shown.

Measurement-base group. Historical cost records

assets at their original price, so it ignores price-level

(inflation) changes; this makes both the asset values and the

profit unrealistic. The same root also explains why only

money-measurable items are captured: managerial skill and

staff morale cannot be priced, so they are omitted. Thus

``does not show current value'' and ``ignores qualitative

factors'' are two faces of the one measurement-base

weakness.

Judgement group. Depreciation method, inventory

valuation and the provision for doubtful debts all rest on

the accountant's estimate. Change the depreciation method and

the reported profit changes although no transaction changed.

So reported profit is partly an opinion, not a pure fact.

Timing group. A Balance Sheet is a photograph taken

on the closing date only. A firm can repay loans just before

the date and borrow again just after (window dressing), so

the single-date position can mislead a reader who assumes it

held all year.

Combine. Listing one or two limitations from each

group gives a complete, well-organised answer that an

examiner can follow at a glance.

Why this matters. Knowing why a limitation exists

lets you adjust for it: revalue fixed assets to current cost before

comparing two firms, or read the depreciation policy note before

trusting a profit figure.

The limitations trace to three roots: a historical-cost

measurement base (no current value, no qualitative data), the heavy

reliance on personal judgement (subjective profit), and the

single-date nature of the Balance Sheet (window dressing).

Q 7.4

List any three objectives of financial statements.

Concept used. An objective of a financial

statement is the purpose it is meant to serve for the people who use

it. Financial statements are prepared to communicate useful financial

information to owners and outsiders.

To present a true and fair view of performance. The

Statement of Profit and Loss shows whether the company earned

a profit or suffered a loss during the year.

To present a true and fair view of financial

position. The Balance Sheet shows the assets the company

owns and the liabilities and capital that finance them on the

closing date.

To provide information for decision-making. Owners,

lenders, investors and government use the statements to judge

profitability, solvency and the safety of their funds.

Three objectives: (i) to show the true and fair operating

result (profit or loss), (ii) to show the true and fair financial

position, and (iii) to give useful information to users for economic

decisions.

RV

Rahul Verma

M.Com, Banaras Hindu University

Verified Expert

Quick reading. An ``objective'' question is really asking

``what reader need does this document satisfy?''. There are exactly

three reader needs, and each maps cleanly to one part of the

reporting package: ``How did we do?'' (performance), ``Where do we

stand?'' (position), ``What should I decide?'' (decision support).

Answer in that order and the three objectives write themselves.

Need 1 (performance) → Statement of Profit and Loss.

Need 2 (position) → Balance Sheet.

Need 3 (decision) → both statements plus the notes,

together.

Performance objective. The first purpose is to show

whether the year was profitable. This is met by the

Statement of Profit and Loss, which nets total revenue

against total expenses to give the profit or loss for the

year. Without this objective the owners cannot judge the

return on their capital.

Position objective. The second purpose is to show

what the firm owns and owes on the last day of the year. The

Balance Sheet meets it by setting all assets against all

claims (liabilities plus owners' funds), the two totals being

equal. This objective tells lenders whether the firm is

solvent.

Decision objective. The third purpose is to give

information that helps users take economic decisions. It is

met by reading both statements together with the Notes to

Accounts, so investors, government and creditors can judge

profitability, solvency and tax. This is the umbrella

objective the other two feed into.

Present cleanly. Stating one objective per reader

need, each tied to its statement, is the format that scores

full marks and answers any ``which statement?'' follow-up

instantly.

Why this matters. Each objective maps to a specific

statement, so an exam follow-up like ``which statement meets

objective X?'' becomes a one-word answer rather than a fresh effort.

Three objectives: show performance (Statement of Profit and

Loss), show financial position (Balance Sheet), and supply

decision-useful information to all interested parties (both

statements plus notes).

Q 7.5

State the importance of financial statements to:

(i) shareholders (ii) creditors

(iii) government (iv) investors

Concept used. Different users read financial

statements with different questions in mind. ``Importance to a user''

means the specific decision the statements help that user take.

(i) Shareholders (owners). They use the statements

to judge the safety of their investment and the return on it,

that is, the profitability and the dividend the company can

pay.

(ii) Creditors (lenders, suppliers). They use the

statements to check the company's solvency: whether

the firm has enough assets and cash to repay loans and pay

for goods supplied on credit.

(iii) Government. It uses the statements to assess

the correct tax payable, to frame industrial and economic

policy, and to compile national statistics.

(iv) Investors (prospective shareholders). They use

the statements to decide whether to buy the company's shares

by judging its earning capacity, growth and future

prospects.

Shareholders judge return and safety; creditors judge

solvency and repaying capacity; government assesses tax and frames

policy; investors judge earning capacity before investing.

SB

Sneha Banerjee

M.Com, University of Calcutta

Verified Expert

Structural observation. Pair each user with the single ratio

family they care about most: shareholders → profitability,

creditors → liquidity/solvency, government → compliance,

investors → growth.

Shareholders track earnings and dividend capacity (return on

their owned funds).

Creditors track short-term liquidity and long-term solvency

(will they be repaid on time?).

Government tracks taxable profit and statutory compliance.

Investors track trend in profits and prospects before

committing fresh money.

Why this matters. A single set of statements is

multi-purpose; the same numbers answer four different stakeholder

questions.

Each user reads the statements through a different lens:

return (shareholders), repayment safety (creditors), tax and policy

(government), and future prospects (investors).

Q 7.6

How will you disclose the following items in the Balance

Sheet of a company:

(i) Current assets, Inventory (ii) Contingent liabilities in

notes to accounts

(iii) Shareholders' Funds, Reserves and Surplus (iv) Fixed

Assets, Intangible Assets

(v) Proposed Dividend for the current year (vi) Non-Current

Liabilities

(vii) Arrears of Dividend on Cumulative Preference Shares

Concept used. Schedule III to the Companies Act, 2013

prescribes a fixed vertical Balance Sheet with two main

parts: I. Equity and Liabilities and II. Assets.

Every item must be shown under its correct major head, sub-head and

note. ``Disclosure'' means stating where the item appears (which head

or note).

(i) Inventory. Major head: Assets → Current

Assets; Sub-head: Inventories.

(ii) Contingent liabilities. A contingent liability

is a possible obligation that depends on a future uncertain

event. It is not shown on the face of the Balance

Sheet; it is disclosed only in the Notes to

Accounts (Contingent Liabilities and Commitments).

(iii) Reserves and Surplus. Major head: Equity and

Liabilities → Shareholders' Funds; Sub-head:

Reserves and Surplus.

(iv) Intangible Assets. Major head: Assets →

Non-Current Assets → Fixed Assets; Sub-head:

Intangible Assets (for example, goodwill, patents).

(v) Proposed Dividend for the current year. It is a

provision made out of profit. It is disclosed under Equity

and Liabilities → Current Liabilities →Short-term Provisions (and noted in Notes to

Accounts as a contingent item until declared, per AS-4

practice followed by NCERT).

(vi) Non-Current Liabilities. It is itself a major

head under Equity and Liabilities, with sub-heads Long-term

Borrowings, Deferred Tax Liabilities (net), Other Long-term

Liabilities and Long-term Provisions.

(vii) Arrears of dividend on cumulative preference

shares. These are unpaid past dividends on cumulative

preference shares. They are a contingent liability and are

disclosed only in the Notes to Accounts, not on the

face of the Balance Sheet.

(i) Current Assets: Inventories; (ii) Notes to Accounts

(Contingent Liabilities); (iii) Shareholders' Funds: Reserves and

Surplus; (iv) Non-Current Assets, Fixed Assets: Intangible Assets;

(v) Current Liabilities: Short-term Provisions; (vi) it is a major

head, Non-Current Liabilities; (vii) Notes to Accounts (Contingent

Liabilities).

AJ

Ankit Joshi

M.Com, Delhi School of Economics

Verified Expert

Picture-first. Sketch the two-part Schedule III skeleton

once, then drop each item into its slot. Items that are uncertain go

to the Notes drawer, not the face.

Non-Current Liabilities is a head, not an item, so it is

named as the head itself.

Note-only items: contingent liabilities and arrears of

cumulative preference dividend, because both are uncertain

future obligations.

Why this matters. The face-versus-notes split is the single

most tested idea in this chapter; mastering it makes the numerical

balance-sheet questions mechanical.

Real assets and obligations sit on the face under their

Schedule III head; uncertain items (contingent liabilities, cumulative

dividend arrears) are disclosed only in the Notes to Accounts.

Q 7.7

Explain the nature of the financial statements.

Concept used. The nature of financial statements

means the underlying character of the data they contain: where the

numbers come from and what kind of inputs shape them. The NCERT text

states that financial statements reflect a combination of three

things: recorded facts, accounting conventions

and personal judgements.

Recorded facts. The figures are based on facts

actually recorded in the books, taken at historical

cost. For example, fixed assets, cash and receivables appear

at the amounts originally recorded, not at current market

value. So facts that were never recorded (for example, the

skill of the workforce) do not appear.

Accounting conventions. Conventions such as

conservatism, consistency and materiality are applied while

preparing the statements. Because of conservatism, for

instance, stock is valued at cost or market price, whichever

is lower, which makes the statements deliberately cautious.

Postulates / concepts. Statements rest on accounting

assumptions such as going concern, money measurement and

accounting period. The going-concern assumption is the reason

assets are not shown at break-up value.

Personal judgements. Many figures depend on the

accountant's estimate: the method of depreciation, the rate

of provision for doubtful debts, the valuation of inventory.

Different judgements give different profit figures from the

same facts.

Financial statements are not pure fact: they are a blend of

recorded facts (at historical cost), accounting concepts and

conventions, and personal judgements/estimates made by the

accountant.

PD

Pranav Desai

M.Com, Banaras Hindu University

Verified Expert

Structural observation. Picture the nature of financial

statements as a spectrum running from a fully objective end to a

fully subjective end. Every ingredient the NCERT lists can be placed

somewhere on this line, and placing them is a cleaner way to

``explain the nature'' than listing four disconnected points. At the

objective end sit recorded facts and accounting concepts; the rule

layer of conventions sits in the middle; personal judgements pull

toward the subjective end.

Objective end: recorded facts, money-measurement and

going-concern assumptions.

Objective core. The bedrock is the recorded facts:

every figure comes from a documented transaction entered in

the books at historical cost, under the money-measurement and

going-concern assumptions. Because only recorded, measurable

events enter, unrecorded value (a skilled workforce) is

invisible. This is the part of the ``nature'' that is closest

to fact.

Rule layer. On top of the facts the accountant

applies conventions. Conservatism is the strongest: stock is

valued at cost or market price, whichever is lower, so the

statements are deliberately cautious. Consistency and

materiality decide how items are grouped and disclosed. The

same facts presented under different conventions look

different.

Subjective layer. Within the conventions the

accountant still estimates: the depreciation method and rate,

the provision for doubtful debts, the stock-valuation method.

Two honest accountants can report different profits from

identical facts purely because these judgements differ. This

is the end of the spectrum furthest from fact.

Combine into the answer. The ``nature'' is therefore

the blend of all three positions on the spectrum: a factual

base, filtered by conventions, fine-tuned by judgement. State

them in that order for a complete, structured answer.

Why this matters. The further a number sits toward the

judgement end, the more carefully an analyst must read its accounting

policy note before trusting it for inter-firm comparison.

Financial statements combine an objective recorded-fact core

(historical cost, going concern) with a rule layer of conventions

(conservatism, consistency) and a subjective layer of personal

estimates (depreciation, provisions); the three are inseparable in

the final figures.

Q 7.8

Explain in detail the significance of the financial

statements.

Concept used. The significance (importance) of

financial statements is the set of benefits different users derive

from them. Because many groups have a stake in a company but cannot

inspect its books, the statements act as the common channel of

financial communication.

To management. They help management measure

performance, control costs, and plan future operations

through comparison with past years and budgets.

To shareholders/owners. They show profitability and

the return earned on owners' funds, helping owners decide

whether to continue, expand or sell their holding.

To lenders and creditors. They reveal the firm's

solvency and liquidity, so banks and suppliers can judge

whether their loans and dues are safe.

To prospective investors. They show earning capacity

and growth, guiding the decision to buy the company's

securities.

To government and tax authorities. They provide the

basis for assessing tax, granting licences, and framing

economic and industrial policy.

To employees and the public. Employees judge job and

bonus security; the public judges the firm's contribution to

employment and the economy.

Financial statements are significant because they serve

management (control and planning), owners (return), creditors

(solvency), investors (prospects), government (tax and policy) and

employees/public (security and contribution), all from one common set

of figures.

IR

Ishita Rao

M.Com, University of Hyderabad

Verified Expert

Quick reading. ``Significance'' is just ``who benefits, and

for what decision''. The cleanest way to cover every beneficiary

without missing one is to first split all users into internal

(management) and external (everyone else), then split the

external group again into capital providers and

regulators/society. Three buckets, every stakeholder accounted for.

Internal: management.

External capital providers: owners, investors, lenders,

creditors.

Internal significance. Management is the only

internal user. It reads the statements to plan future

operations, control costs against budgets, and evaluate this

year's performance against past years. This is the

``stewardship'' use: those running the firm checking how well

they ran it.

Capital-provider significance. Owners and

prospective investors look at profitability and growth to

judge the return on, and safety of, their money. Lenders and

creditors look at solvency and liquidity to judge whether

loans and dues will be repaid. Both groups read the same

statements but weigh different parts.

Regulator and society significance. Government and

tax authorities use the statements to assess correct tax,

grant licences and frame economic policy. Employees judge job

and bonus security; the public judges the firm's contribution

to employment and the economy.

Tie it together. Stating the significance bucket by

bucket shows the examiner that one common set of figures

serves every interested party, which is exactly the point the

``significance'' question tests.

Why this matters. The internal-versus-external split mirrors

the next chapter, where the same statements are analysed by these

very groups for the same reasons.

One statement set, many beneficiaries: management plans and

controls with it, capital providers judge return and repayment

safety, and government/employees/public judge tax, security and

economic contribution.

Q 7.9

Explain the limitations of financial statements.

Concept used. A limitation is an inherent

shortcoming that restricts how far the statements can be relied upon

even when the books are accurate. The limitations arise directly from

the nature of the statements explained earlier.

Historical in nature. Statements record events at

historical cost; they ignore price-level (inflation)

changes, so asset values and profit can be unrealistic.

Ignore qualitative information. Only money-measurable

items are shown. Managerial efficiency, employee morale and

customer goodwill, though valuable, are excluded.

Influenced by personal judgement. Depreciation

method, stock valuation and provisions depend on the

accountant's estimate, so profit is partly subjective.

Show position at a single date. The Balance Sheet is

a snapshot on the closing date and may not reflect the

position during the rest of the year (window dressing is

possible).

Based on accounting concepts and conventions.

Going-concern and conservatism conventions can make the

statements depart from the firm's true economic worth.

Aggregate data. Statements present summarised totals;

product-wise or segment-wise detail needed for some decisions

is not visible.

Financial statements are limited by historical-cost

recording, exclusion of qualitative factors, dependence on personal

judgement, single-date presentation, the influence of conventions, and

the use of aggregated data.

DK

Dev Kapoor

M.Com, Symbiosis Pune

Verified Expert

Structural observation. A ``limitations'' answer is strongest

when it shows the examiner why each weakness exists, not just

that it exists. Bucket the six NCERT limitations into three causes

and explain each cause once: measurement (historical cost,

aggregation), omission (qualitative items), and

judgement (estimates, conventions, single date). Every

limitation then drops into exactly one bucket.

Measurement cause: how figures are valued and summarised.

Omission cause: what never enters the books at all.

Judgement cause: where opinion and timing distort the

picture.

Measurement cause. The cost basis records assets at

their original price, so it ignores inflation and shows

out-of-date values. The same cause explains aggregation:

statements present summarised totals, hiding the

product-wise or segment detail some decisions need. Both

``historical in nature'' and ``aggregate data'' flow from

how figures are measured and summarised.

Omission cause. Only money-measurable items are

recorded, so managerial efficiency, employee morale and

customer goodwill never appear, however valuable. This single

cause is the root of ``ignores qualitative information''.

Judgement cause. Depreciation method, stock

valuation and provisions rest on the accountant's estimate,

so profit is partly subjective. The going-concern and

conservatism conventions push the figures away from true

economic worth, and the single closing-date snapshot allows

window dressing. Estimates, conventions and timing together

form the judgement cause.

Present by cause. Explaining one or two limitations

under each cause produces a complete answer that an examiner

can follow as a logical argument rather than a memorised

list.

Why this matters. Naming the cause lets an analyst correct

for it: restate fixed assets to current value before inter-firm

comparison, or normalise profit for a changed depreciation policy.

Every limitation maps to one of three roots: a cost-based

measurement base (historical cost, aggregation), the omission of

non-money items, or the role of judgement and timing (estimates,

conventions, single date).

Q 7.10

Prepare the format of the Statement of Profit and Loss and

explain its items up to the ascertainment of profit before tax.

Concept used. The Statement of Profit and Loss is

prepared in the vertical form prescribed by Schedule III, Part II of

the Companies Act, 2013. It computes profit in stages: total revenue

minus total expenses gives profit before exceptional and

extraordinary items, and adjusting these gives profit before

tax.

Statement of Profit and Loss for the year ended

1.35

tabular@p1.0cmp8.8cmp1.4cmp3.0cm@

& Particulars & Note & Amount (Rs.)

I & Revenue from Operations & & xxx

II & Other Income & & xxx

III & Total Revenue (I + II) & & xxx

IV & Expenses: & &

& Cost of Materials Consumed & & xxx

& Purchases of Stock-in-Trade & & xxx

& Changes in Inventories & & xxx

& Employee Benefits Expense & & xxx

& Finance Costs & & xxx

& Depreciation & Amortisation & & xxx

& Other Expenses & & xxx

& Total Expenses & & xxx

V & Profit before Exceptional, Extra- & &

& ordinary items & Tax (III - IV) & & xxx

VI & Exceptional Items & & xxx

VII & Profit before Extraordinary items & &

& & Tax (V - VI) & & xxx

VIII & Extraordinary Items & & xxx

IX & Profit before Tax (VII - VIII) & & xxx

tabular

Revenue from Operations (I). Income from the main

business activity: sale of products and services (for a

finance company, interest and dividend earned).

Other Income (II). Income not from the main

operations, such as interest on investments, rent received

and profit on sale of assets.

Total Revenue (III). The simple sum, III = I +

II.

Expenses (IV). All operating expenses: cost of

materials consumed, purchases of stock-in-trade, change in

inventories, employee benefits, finance costs

(interest on borrowings), depreciation and other expenses.

Their total is Total Expenses.

Profit before exceptional, extraordinary items and

tax (V). Computed as V = III - IV.

Exceptional and extraordinary items (VI, VIII).

Unusual, non-recurring gains or losses; they are removed

stepwise to reach VII = V - VI and then IX = VII -

VIII.

Profit before Tax (IX). The final figure of this

part, before any income-tax provision is deducted.

Profit before tax is reached as: Total Revenue (I+II) -

Total Expenses = V; then - Exceptional items = VII; then -

Extraordinary items = Profit before Tax (IX).

YN

Yash Nair

M.Com, Christ University Bangalore

Verified Expert

Strategic angle. Do not memorise the Schedule III statement

as sixteen disconnected lines. Read it as a single subtraction chain

in three layers: start at total revenue, peel away the operating

expenses, then peel away the unusual items, and what remains is

profit before tax. Each Roman-numeral line is just one rung of that

chain.

Layer 1 builds the top: Total Revenue = I + II.

Layer 2 removes routine expenses: V = III - IV.

Layer 3 removes one-off items: IX = VII - VIII.

Layer 1: form the top line. Revenue from Operations

(I) is income from the main business: sale of products and

services. Other Income (II) is incidental income: interest on

investments, rent received, profit on sale of assets. Their

sum is Total Revenue, III = I + II. Keeping operating and

non-operating income separate here is what later lets an

analyst judge the quality of earnings.

Layer 2: subtract operating expenses. Total

Expenses (IV) gathers cost of materials consumed, purchases

of stock-in-trade, change in inventories, employee benefits,

finance costs (interest on borrowings), depreciation and

amortisation, and other expenses. Subtracting this from Total

Revenue gives the profit before exceptional and extraordinary

items: V = III - IV. Finance cost and depreciation are

expenses, not Other Income; misplacing them is the

single most common error.

Layer 3: strip the one-off items. Exceptional items

(VI) are unusual but operating; subtract them to get VII =

V - VI. Extraordinary items (VIII) are rare and outside

ordinary activity; subtract them to get IX = VII - VIII.

Removing them stepwise keeps the recurring profit visible

separately from the one-off effect.

Read off Profit before Tax. Line IX is the end of

this part: profit before any income-tax provision. Tax (X)

and the post-tax lines come after IX and are outside

what this question asks.

Why this matters. Seeing the statement as a top-down funnel

prevents the classic slip of dropping finance cost or depreciation

into ``Other Income'', which would overstate both revenue and profit.

Profit before Tax (IX) = (Revenue from Operations +

Other Income) - Total Expenses - Exceptional Items -

Extraordinary Items.

Q 7.11

Prepare the format of the Balance Sheet and explain the

various elements of the Balance Sheet.

Concept used. Schedule III, Part I prescribes a

vertical Balance Sheet with two main parts that must always

be equal: I. Equity and Liabilities and II. Assets.

Balance Sheet as at 31st March, 20

1.3

tabular@p10.8cmp1.4cmp2.6cm@

Particulars & Note & Amount (Rs.)

I. EQUITY AND LIABILITIES & &

1. Shareholders' Funds & &

(a) Share Capital & & xxx

(b) Reserves and Surplus & & xxx

(c) Money received against share warrants & & xxx

2. Share application money pending allotment & & xxx

3. Non-Current Liabilities & &

(a) Long-term Borrowings & & xxx

(b) Deferred Tax Liabilities (net) & & xxx

(c) Other Long-term Liabilities & & xxx

(d) Long-term Provisions & & xxx

4. Current Liabilities & &

(a) Short-term Borrowings & & xxx

(b) Trade Payables & & xxx

(c) Other Current Liabilities & & xxx

(d) Short-term Provisions & & xxx Total & & xxx II. ASSETS & &

1. Non-Current Assets & &

(a) Fixed Assets (Tangible/Intangible) & & xxx

(b) Non-current Investments & & xxx

(c) Deferred Tax Assets (net) & & xxx

(d) Long-term Loans and Advances & & xxx

(e) Other Non-current Assets & & xxx

2. Current Assets & &

(a) Current Investments & & xxx

(b) Inventories & & xxx

(c) Trade Receivables & & xxx

(d) Cash and Cash Equivalents & & xxx

(e) Short-term Loans and Advances & & xxx

(f) Other Current Assets & & xxx Total & & xxx

tabular

Shareholders' Funds. Owners' money in the company:

Share Capital, Reserves and Surplus, and money received

against share warrants.

Share application money pending allotment. Money

received on share applications for which shares are not yet

allotted.

Non-Current Liabilities. Obligations not due within

twelve months: long-term borrowings, deferred tax

liabilities, other long-term liabilities and long-term

provisions.

Current Liabilities. Obligations due within twelve

months: short-term borrowings, trade payables, other current

liabilities and short-term provisions.

Non-Current Assets. Assets held for long-term use:

fixed assets (tangible and intangible), non-current

investments, deferred tax assets, long-term loans and

advances, and other non-current assets.

Current Assets. Assets expected to be realised

within twelve months: current investments, inventories, trade

receivables, cash and cash equivalents, short-term loans and

advances, and other current assets.

The identity. Total Equity and Liabilities always

equals Total Assets, because every rupee of asset is financed

by either owners' funds or outside liabilities.

The Schedule III Balance Sheet has two equal parts: Equity

and Liabilities (Shareholders' Funds, Share application money,

Non-current and Current Liabilities) and Assets (Non-current and

Current Assets); Total of one always equals the Total of the other.

KP

Kavya Pillai

M.Com, Madras Christian College

Verified Expert

Picture-first. The Balance Sheet is a see-saw: claims on the

left arm, resources on the right arm, perfectly balanced.

!%

[See diagram in the PDF version]

%

Left arm: the sources. ``Equity and Liabilities''

answers who financed the firm. It has two families.

Owners' money is Shareholders' Funds: Share Capital, Reserves

and Surplus, and money received against share warrants;

Share application money pending allotment sits just below.

Outsiders' money splits by the twelve-month rule into

Non-current Liabilities (long-term borrowings, deferred tax

liabilities, other long-term liabilities, long-term

provisions) and Current Liabilities (short-term borrowings,

trade payables, other current liabilities, short-term

provisions).

Right arm: the uses. ``Assets'' answers where

the money went. Non-current Assets are long-life resources:

fixed assets (tangible and intangible), non-current

investments, deferred tax assets, long-term loans and

advances, other non-current assets. Current Assets are

short-life resources: current investments, inventories, trade

receivables, cash and cash equivalents, short-term loans and

advances, other current assets.

The pivot. The two arms are joined by the accounting

equation. Every rupee of asset must have come from either

owners or outsiders, so Total Equity and Liabilities is

always equal to Total Assets. The classification of

each item under current versus non-current uses the single

twelve-month test.

Use the picture to self-check. Draw the see-saw

before solving any numerical: if your two totals do not

balance, an item has been hung on the wrong arm or under the

wrong head, and the picture tells you to go looking for it.

Why this matters. If the two totals do not tally in a

numerical, an item has been placed on the wrong arm: the see-saw

image catches the error instantly instead of after a re-add.

Equity and Liabilities (sources: owners' funds plus

liabilities) on one side, Assets (uses: non-current plus current) on

the other, kept exactly equal by the accounting equation.

Q 7.12

Explain how financial statements are useful to the various

parties who are interested in the affairs of an undertaking.

Concept used. An interested party (stakeholder) is

anyone whose decisions are affected by the firm's results. Each party

uses the same statements for a different decision.

Owners/Shareholders. Judge profitability and the

return on their capital; decide whether to hold, buy more or

sell shares.

Management. Use the statements for planning,

controlling costs and measuring performance against past

years.

Lenders/Banks. Assess long-term solvency

before sanctioning or renewing loans.

Creditors/Suppliers. Assess short-term liquidity

before extending goods on credit.

Investors (prospective). Judge earning capacity and

growth prospects before buying securities.

Government and tax authorities. Determine taxable

profit, grant licences and frame economic policy.

Employees and trade unions. Judge job security,

bonus and wage-bargaining capacity.

Researchers and the public. Study the firm's

contribution to the economy and to employment.

Owners/investors judge return and prospects, management

plans and controls, lenders and creditors judge solvency and

liquidity, government assesses tax and policy, and

employees/public/researchers judge security and economic

contribution.

RS

Riya Sharma

M.Com, Loyola College Chennai

Verified Expert

Structural observation. A ``parties interested'' answer

loses marks when a party is forgotten. The fix is to split the eight

parties into three families and recite the families, not the loose

list: capital providers, regulators, and the

operations side. Each family shares one core concern, so the

usefulness writes itself once the family is named.

Capital providers: owners, investors, lenders, creditors.

Capital providers. Owners and prospective investors

read the statements to judge profitability and growth, that

is, the return on and prospects for their money. Lenders and

creditors read the same statements to judge solvency and

liquidity, that is, whether their loans and credit will be

repaid on time. One family, one core concern: safety of

funds against return.

Regulators. Government and tax authorities use the

statements to determine taxable profit, grant licences, and

frame economic and industrial policy. Their core concern is

compliance and the correct assessment of dues.

Operations side. Management uses the statements to

plan, control costs and measure performance against past

years. Employees and trade unions judge job security and

wage-bargaining capacity. Researchers and the public study

the firm's contribution to the economy and employment. The

shared concern is how the firm runs and what it contributes.

Recite by family. Naming three families and the one

concern of each guarantees no party is dropped and turns a

long list into a short, defensible structure.

Why this matters. A family grouping makes a long ``list''

answer easy to recall under exam pressure without missing a party,

and it directly previews the user-wise analysis of the next chapter.

Three families read the statements: capital providers

(return versus repayment safety), regulators (tax and policy), and

the operations side (planning, control, job security and economic

contribution).

Q 7.13

`Financial statements reflect a combination of recorded

facts, accounting conventions and personal judgements.' Discuss.

Concept used. This famous statement summarises the

nature of financial statements. To ``discuss'' it, we

explain each of the three ingredients and show how they combine in

the final figures.

Recorded facts. The statements use data actually

entered in the books from documented transactions, at

historical cost. Cash, sales, purchases and fixed

assets are recorded facts. Unrecorded items (the worth of a

skilled team) are excluded, which is why the statements show

only what was recorded.

Accounting conventions. Conventions such as

conservatism (provide for all losses, anticipate no

profit), consistency and materiality govern how those facts

are presented. Valuing closing stock at cost or market price,

whichever is lower, is conservatism in action.

Personal judgements. Within the conventions, the

accountant must still make estimates: the depreciation method

and rate, the provision for doubtful debts, the method of

stock valuation. These judgements directly change the

reported profit.

How they combine. A single profit figure therefore

contains all three: a factual base, shaped by conventions,

and fine-tuned by judgement. Two honest accountants can

report different profits for identical facts because the

conventions and judgements differ.

The statement is correct: every reported figure is a

recorded fact, presented through accounting conventions, and adjusted

by the accountant's personal judgement; the three are inseparable in

the final numbers.

AR

Aditya Reddy

M.Com, St. Joseph's Bangalore

Verified Expert

Strategic angle. Treat the sentence as an equation:

Statement = Facts × Conventions × Judgement. Discuss

each multiplier and the effect of changing it.

Facts term: the objective input.

Conventions term: the presentation filter.

Judgement term: the adjustable estimate.

Facts term. The recorded facts are drawn from

vouchers and ledgers at historical cost. They are the

objective input: cash, sales, purchases, fixed assets.

Nothing unrecorded (the worth of a skilled team) enters, so

this term sets the boundary of what the statements can ever

show. ``Discussing'' it means stressing that the facts are

real but incomplete.

Conventions term. Conservatism, consistency and

materiality act as a filter on those facts. Conservatism is

the most influential: provide for all losses, anticipate no

profit, value stock at the lower of cost or market. The

filter deliberately lowers reported profit and asset values,

so the same facts presented under it look more cautious than

reality.

Judgement term. Within the convention filter the

accountant still chooses: the depreciation method and rate,

the provision for doubtful debts, the stock-valuation method.

Change the depreciation method and the reported profit

changes although not a single transaction changed. This term

is the adjustable dial.

Discuss how they combine. A single profit figure

carries all three: a factual base, filtered by conventions,

fine-tuned by judgement. Because two of the three terms are

not purely factual, two honest accountants can report

different profits for identical facts, so the statement in

the question is correct.

Why this matters. Because two of the three terms are not

purely factual, reported profit must be read as a measured

opinion, not an exact truth. This single insight underlies every

caution in the analysis chapters.

The statement is correct: financial statements are jointly

produced by recorded facts, accounting conventions and personal

judgement, so reported profit is a considered estimate rather than an

absolute fact.

Q 7.14

Explain the process of preparing the income statement and

the balance sheet.

Concept used. Preparing company financial statements means

classifying every trial-balance item under the correct Schedule III

head. The income statement (Statement of Profit and Loss)

is prepared first to find profit; that profit then flows into

Reserves and Surplus on the Balance Sheet.

Start from the Trial Balance. List all ledger

balances. Separate them into revenue items (incomes and

expenses) and position items (assets, liabilities, capital).

Prepare the Statement of Profit and Loss. Put all

incomes under Revenue from Operations and Other Income to get

Total Revenue (I + II). Put all expenses under the prescribed

expense heads to get Total Expenses (IV).

Ascertain profit. Compute Profit before Tax as Total

Revenue minus Total Expenses (adjusted for exceptional and

extraordinary items). Deduct the tax provision to get

Profit/(Loss) for the period.

Carry profit to the Balance Sheet. The net profit

(after appropriations) is added to the Surplus balance under

Reserves and Surplus.

Classify the position items. Place every asset under

Non-current or Current Assets, and every liability under

Non-current or Current Liabilities, using the twelve-month

rule. Share capital and reserves go under Shareholders'

Funds.

Prepare Notes to Accounts. Break up composite heads

(Share Capital, Reserves and Surplus, Fixed Assets,

Borrowings) in numbered notes and cross-reference them on the

face.

Tally. Confirm Total Equity and Liabilities equals

Total Assets. If they differ, an item has been mis-classified.

First prepare the Statement of Profit and Loss to find

profit; transfer that profit to Reserves and Surplus; then classify

all assets and liabilities under Schedule III heads, prepare Notes to

Accounts, and ensure the two Balance Sheet totals are equal.

TB

Tara Bhat

M.Com, Fergusson College Pune

Verified Expert

Picture-first. The two statements are linked by a single

pipe: profit flows out of the income statement and into the Balance

Sheet's reserves.

!%

[See diagram in the PDF version]

%

Sort the trial balance. List every ledger balance

and label it as either a revenue item (incomes, expenses) or

a position item (assets, liabilities, capital). This sorting

is the whole battle: an item labelled wrongly here will be

mis-stated everywhere downstream.

Run the income statement. Feed the revenue items

into the Statement of Profit and Loss: incomes under Revenue

from Operations and Other Income (giving Total Revenue),

expenses under the prescribed expense heads (giving Total

Expenses). Net them, adjust exceptional and extraordinary

items, deduct the tax provision, and you have net profit for

the period.

Pipe profit into the Balance Sheet. The net profit

(after appropriations) is added to the Surplus balance under

Reserves and Surplus. This is the single link between the two

statements; the rest of the Balance Sheet is independent of

it.

Classify and tally. Place every asset under

Non-current or Current Assets and every liability under

Non-current or Current Liabilities using the twelve-month

rule, with share capital and reserves under Shareholders'

Funds. Prepare the Notes to Accounts for composite heads, and

confirm Total Equity and Liabilities equals Total Assets.

Why this matters. Remembering the profit ``pipe'' explains

why a wrong profit figure throws the Balance Sheet totals out of

balance: the error travels down the pipe into Reserves and Surplus.

Income statement first (find profit), pipe the profit into

Reserves and Surplus, classify all position items under Schedule III

using the twelve-month rule, prepare the notes, and tally the two

Balance Sheet totals.

Q 7.15

Show the following items in the Balance Sheet as per the

provisions of the Companies Act, 2013 in Schedule III:

Preliminary Expenses Rs. 2,40,000; Discount on issue of shares

Rs. 20,000; 10% Debentures Rs. 2,00,000; Stock in trade

Rs. 1,40,000; Cash at bank Rs. 1,35,000; Bills receivable

Rs. 1,20,000; Goodwill Rs. 30,000; Loose tools Rs. 12,000; Motor

vehicles Rs. 4,75,000; Provision for tax Rs. 16,000.

Concept used. Each item must be placed under its correct

Schedule III head. Preliminary expenses and discount

on issue of shares are not assets in the usual sense; they are

fictitious/deferred items shown under Other Non-current

Assets. Goodwill and loose tools are tangible/

intangible fixed assets; stock and loose tools form

Inventories; provision for tax is a

Short-term Provision.

Classify the liabilities side. 10% Debentures

Rs. 2,00,000 is a Long-term Borrowing (Non-current

Liabilities). Provision for tax Rs. 16,000 is a Short-term

Provision (Current Liabilities).

Cash and Cash Equivalents: Cash at bank

Rs. 1,35,000.

Total the liabilities side. 2,00,000 + 16,000 = 2,16,000.

Wait: this is only the borrowed and provision portion. The

balancing figure (Shareholders' Funds, not given) makes the

two sides equal. The Total of Assets is what we can

compute fully:

aligned

Total Assets &= 4,75,000 + 30,000 + 2,60,000

& + 1,52,000 + 1,20,000 + 1,35,000

&= Rs. 10,72,000.

aligned

Including only the items asked (the NCERT solution presents

the partial Balance Sheet), the assets shown total

Rs. 10,72,000; the equity-and-liabilities side carries the

balancing Shareholders' Funds plus 10% Debentures

Rs. 2,00,000 and Provision for tax Rs. 16,000.

Fictitious assets

Preliminary expenses and discount on issue of shares/debentures are

fictitious assets: they carry no resale value and are shown

under ``Other Non-current Assets'' only until written off against

profits.

Balance Sheet (extract) of the Company as per

Schedule III

Strategic angle. Ten loose items look intimidating until you

sort them into just three buckets before touching the Balance Sheet:

financed-by (liabilities), real assets, and

fictitious assets. Sorting first means each item is placed

once, correctly, with no second-guessing.

Liability bucket: how the firm is financed.

Real-asset bucket: things with genuine resale value.

Fictitious-asset bucket: expenses parked as assets until

written off.

Liability bucket. 10% Debentures Rs. 2,00,000 is a

Long-term Borrowing under Non-current Liabilities. Provision

for tax Rs. 16,000 is a Short-term Provision under Current

Liabilities. Both are placed at face value; nothing here is

netted.

Real-asset bucket. Motor vehicles Rs. 4,75,000 is a

tangible fixed asset; Goodwill Rs. 30,000 is an intangible

fixed asset. Stock in trade Rs. 1,40,000 + Loose tools

Rs. 12,000 = Rs. 1,52,000 form Inventories. Bills

receivable Rs. 1,20,000 are Trade Receivables and Cash at

bank Rs. 1,35,000 is Cash and Cash Equivalents. Real assets

total 4,75,000 + 30,000 + 1,52,000 + 1,20,000

+ 1,35,000 = Rs. 8,12,000.

Fictitious-asset bucket. Preliminary expenses

Rs. 2,40,000 + Discount on issue of shares Rs. 20,000 =

Rs. 2,60,000, shown under Other Non-current Assets until

written off against profits. These have no resale value;

treating them as ordinary assets is the single most common

slip.

Total and balance. Assets shown = 8,12,000 +

2,60,000 = Rs. 10,72,000. The equity-and-liabilities

side carries 10% Debentures Rs. 2,00,000, Provision for tax

Rs. 16,000, and the balancing Shareholders' Funds that makes

the two sides equal.

Cross-check by note totals. Re-derive the assets-shown

figure independently from the Notes to Accounts: Fixed Assets note

= 4,75,000 + 30,000 = Rs. 5,05,000; Other Non-current

Assets note = 2,40,000 + 20,000 = Rs. 2,60,000;

Inventories note = 1,40,000 + 12,000 = Rs. 1,52,000;

Trade Receivables = Rs. 1,20,000; Cash = Rs. 1,35,000.

Sum = 5,05,000 + 2,60,000 + 1,52,000 + 1,20,000 +

1,35,000 = Rs. 10,72,000, matching the face total. Two

independent routes giving the same figure is the best assurance the

classification is right.

Why this matters. Treating fictitious assets as ordinary

assets leaves the answer technically wrong even when every figure is

copied correctly, so the sorting step is not optional. The

note-level cross-check is exactly how an examiner verifies your

classification.

Real assets total Rs. 8,12,000; fictitious assets

Rs. 2,60,000; assets shown Rs. 10,72,000, balanced by 10% Debentures

Rs. 2,00,000, Provision for tax Rs. 16,000 and balancing

Shareholders' Funds.

Q 7.16

On April 1, 2017, Jumbo Ltd. issued 10,000; 12% debentures

of Rs. 100 each at a discount of 20%, redeemable after 5 years. The

company decided to write off discount on issue of such debentures on

March 31, 2018. Show the items in the Balance Sheet of the company

immediately after the issue of these debentures.

Concept used. When debentures are issued at a

discount, the company receives less than the face value but

must repay the full face value. Face value is the amount shown under

Long-term Borrowings. The total discount is a

fictitious asset (Discount/Loss on Issue of Debentures)

written off over the life of the debentures. The portion to be

written off within 12 months is a Current Asset; the rest is a

Non-current Asset.

Compute the face value of debentures. Face value = 10,000 × Rs. 100 = Rs. 10,00,000.

This full Rs. 10,00,000 is shown under Non-current

Liabilities → Long-term Borrowings, because the company

must redeem at par.

Compute the discount on issue. Discount = 20% of Rs. 10,00,000

= 20100 × 10,00,000 = Rs. 2,00,000.

Spread the discount over 5 years. The discount is

written off evenly:

Per year = 2,00,0005 = Rs. 40,000.

Split the unwritten discount on the date of issue.

Immediately after issue (before any write-off), the whole

Rs. 2,00,000 is unamortised. Of this:

the part to be written off within the next 12 months

= Rs. 40,000 ⇒Other Current

Assets;

the balance =2,00,000 - 40,000 =

Rs. 1,60,000⇒Other

Non-current Assets.

Balance Sheet of Jumbo Ltd. (extract) as at the

issue date

1.25

tabular@p8.6cmp1.2cmp3.0cm@

Particulars & Note & Amount (Rs.)

I. EQUITY AND LIABILITIES & &

Non-Current Liabilities & &

Long-term Borrowings (12% Deb.) & 1 & 10,00,000 II. ASSETS & &

Non-Current Assets & &

Other Non-current Assets & &

(Discount on issue of Deb.) & 2 & 1,60,000

Current Assets & &

Cash and Cash Equivalents & & 8,00,000

Other Current Assets & &

(Discount on issue of Deb.) & 3 & 40,000

tabular

Long-term Borrowings (12% Debentures) = Rs. 10,00,000;

Cash received = Rs. 8,00,000; Discount on issue Rs. 2,00,000 shown

as Other Non-current Assets Rs. 1,60,000 + Other Current Assets

Rs. 40,000.

SM

Siddharth Menon

M.Com, Loyola College Chennai

Verified Expert

Quick reading. Only three numbers drive this whole question:

the face value (the liability), the discount (a fictitious asset),

and the cash received (face minus discount). After that, the single

trick is slicing the discount into a one-year piece and a rest piece.

Compute the three numbers first; the Balance Sheet then fills itself

in.

Number 1: face value → Long-term Borrowing.

Number 2: discount → fictitious asset to be amortised.

Number 3: cash → Cash and Cash Equivalents.

Face value (the liability). 10,000 × Rs. 100 = Rs. 10,00,000.

The company must redeem at par, so the full Rs. 10,00,000

sits under Non-current Liabilities, untouched by the

discount.

Discount and cash. Discount = 20% × 10,00,000

= Rs. 2,00,000, Cash received = 10,00,000 - 2,00,000

= Rs. 8,00,000.

The cash goes to Cash and Cash Equivalents; the discount is a

fictitious asset, not a reduction of the liability.

Slice the discount. It is written off evenly over 5

years:

Per year = 2,00,0005 = Rs. 40,000.

Immediately after issue the whole Rs. 2,00,000 is

unamortised. The Rs. 40,000 due to be written off within 12

months is Other Current Assets; the balance

2,00,000 - 40,000 = Rs. 1,60,000 is Other

Non-current Assets.

Assemble. Long-term Borrowings Rs. 10,00,000; Cash

Rs. 8,00,000; discount split Rs. 1,60,000 non-current +

Rs. 40,000 current. The discount on both asset lines plus

cash reconcile to the face value financed.

Why this matters. The liability is always shown at

par; the discount never reduces it, it sits on the assets side

and is amortised. Confusing the two is the standard exam trap this

question is built to catch.

From the following information prepare the Balance Sheet of

Gitanjali Ltd.:

Inventories Rs. 14,00,000; Equity Share Capital Rs. 20,00,000; Plant

and Machinery Rs. 10,00,000; Preference Share Capital Rs. 12,00,000;

Debenture Redemption Reserve Rs. 6,00,000; Outstanding Expenses

Rs. 3,00,000; Proposed Dividend Rs. 5,00,000; Land and Building

Rs. 20,00,000; Current Investments Rs. 8,00,000; Cash Equivalent

Rs. 10,00,000; Short term loan from Zaveri Ltd. (a subsidiary of

Twilight Ltd.) Rs. 4,00,000; Public Deposits Rs. 12,00,000.

Concept used. Each balance is placed under its Schedule III

head. Equity and Preference Share Capital form

Share Capital; Debenture Redemption Reserve is part of

Reserves and Surplus; together they make Shareholders'

Funds. Public Deposits are Long-term Borrowings

(Non-current Liabilities). The short-term loan and

outstanding expenses and proposed dividend are

Current Liabilities.

Total Assets. 30,00,000 + 32,00,000 = Rs. 62,00,000.

Both totals equal Rs. 62,00,000, so the Balance Sheet

tallies.

Balance Sheet of Gitanjali Ltd.

1.2

tabular@p8.6cmp1.2cmp3.0cm@

Particulars & Note & Amount (Rs.)

I. EQUITY AND LIABILITIES & &

Shareholders' Funds & &

Share Capital & 1 & 32,00,000

Reserves & Surplus (DRR) & 2 & 6,00,000

Non-Current Liabilities & &

Long-term Borrowings (Public Dep.) & 3 & 12,00,000

Current Liabilities & &

Short-term Borrowings (Zaveri) & & 4,00,000

Other Current Liab. (O/s Exp.) & & 3,00,000

Short-term Provisions (Prop. Div.) & & 5,00,000 Total & & 62,00,000 II. ASSETS & &

Non-Current Assets & &

Fixed Assets (Land/Bldg + P&M) & 4 & 30,00,000

Current Assets & &

Current Investments & & 8,00,000

Inventories & & 14,00,000

Cash and Cash Equivalents & & 10,00,000 Total & & 62,00,000

tabular

Total of the Balance Sheet (Equity and Liabilities =

Assets) =Rs. 62,00,000.

AP

Ananya Pillai

M.Com, Christ University Bangalore

Verified Expert

Strategic angle. Build the liabilities side in three

deliberate layers (owners, long-term outsiders, short-term

outsiders), total it, then mirror with assets and confirm the tally.

Layer 1: owners' money.

Layer 2: long-term outside money.

Layer 3: short-term outside money.

Owners' layer. Equity Share Capital Rs. 20,00,000

+ Preference Share Capital Rs. 12,00,000 = Share Capital

Rs. 32,00,000. Add Debenture Redemption Reserve Rs. 6,00,000

(it is a reserve, part of Reserves and Surplus, never a

liability). Shareholders' Funds = 32,00,000 +

6,00,000 = Rs. 38,00,000.

Long-term outsiders. Public Deposits are borrowings

that mature after twelve months, so they are Long-term

Borrowings: Non-current Liabilities = Rs. 12,00,000.

Short-term outsiders. Short-term loan from Zaveri

Ltd. Rs. 4,00,000 (Short-term Borrowings) + Outstanding

Expenses Rs. 3,00,000 (Other Current Liabilities) +

Proposed Dividend Rs. 5,00,000 (Short-term Provisions) =

Rs. 12,00,000. The Zaveri loan is a routine borrowing despite

the subsidiary relationship.

Total and mirror with assets. Grand total =

38,00,000 + 12,00,000 + 12,00,000 =

Rs. 62,00,000. The assets side is Fixed Assets

(Land/Building Rs. 20,00,000 + Plant & Machinery

Rs. 10,00,000 = Rs. 30,00,000) + Current Assets (Current

Investments Rs. 8,00,000 + Inventories Rs. 14,00,000 +

Cash Rs. 10,00,000 = Rs. 32,00,000) = Rs. 62,00,000. The

tally confirms.

Trap audit. This question hides three classic traps; check

each before declaring done. (a) Debenture Redemption Reserve is a

reserve, not a borrowing: a Rs. 6,00,000 swing if mis-placed.

(b) Proposed Dividend is a Short-term Provision, not a reduction of

reserves. (c) The Zaveri loan, despite the subsidiary wording, is

just a Short-term Borrowing; the relationship is a distractor. Clear

all three and the Rs. 62,00,000 tally is guaranteed, not lucky.

Why this matters. Layering the liabilities side makes the

final tally a confirmation, not a surprise; if a layer is wrong the

mismatch points straight at the layer that broke.

Equity and Liabilities = Assets = Rs. 62,00,000.

Q 7.18

From the following information prepare the Balance Sheet of

Jam Ltd.:

Inventories Rs. 7,00,000; Equity Share Capital Rs. 16,00,000; Plant

and Machinery Rs. 8,00,000; 8% Preference Share Capital Rs. 6,00,000;

General Reserves Rs. 6,00,000; Bills payable Rs. 1,50,000; Provision

for taxation Rs. 2,50,000; Land and Building Rs. 16,00,000;

Non-current Investments Rs. 10,00,000; Cash at Bank Rs. 5,00,000;

Creditors Rs. 2,00,000; 12% Debentures Rs. 12,00,000.

Concept used.Equity and 8% Preference

Share Capital make Share Capital; General Reserve is

Reserves and Surplus; together they form Shareholders' Funds.

12% Debentures are Long-term Borrowings. Bills

payable and Creditors are Trade Payables; provision

for taxation is a Short-term Provision.

Total of the Balance Sheet (Equity and Liabilities =

Assets) =Rs. 46,00,000.

AC

Arjun Chatterjee

M.Com, Presidency University Kolkata

Verified Expert

Structural observation. Two items are composite and trip

students: Share Capital (equity + preference) and Trade Payables

(bills payable + creditors). Combine each correctly and the rest

slots in.

Composite head 1: Share Capital (equity + preference).