The ncert class 12 accountancy book pdf chapter 7 Financial Statements of a Company opens Part 2 of the Class 12 textbook and is the highest-yield single chapter in the Companies block of the CBSE 2026-27 board paper. The Reprint 2026-27 PDF contains Schedule III formats, the full Balance Sheet template, the Statement of Profit and Loss, and the Notes to Accounts that every Part B numerical sits on.

- CBSE Weightage (Part B): 8 to 10 marks in the Class 12 Accountancy board paper (Unit 3: Financial Statements of a Company)

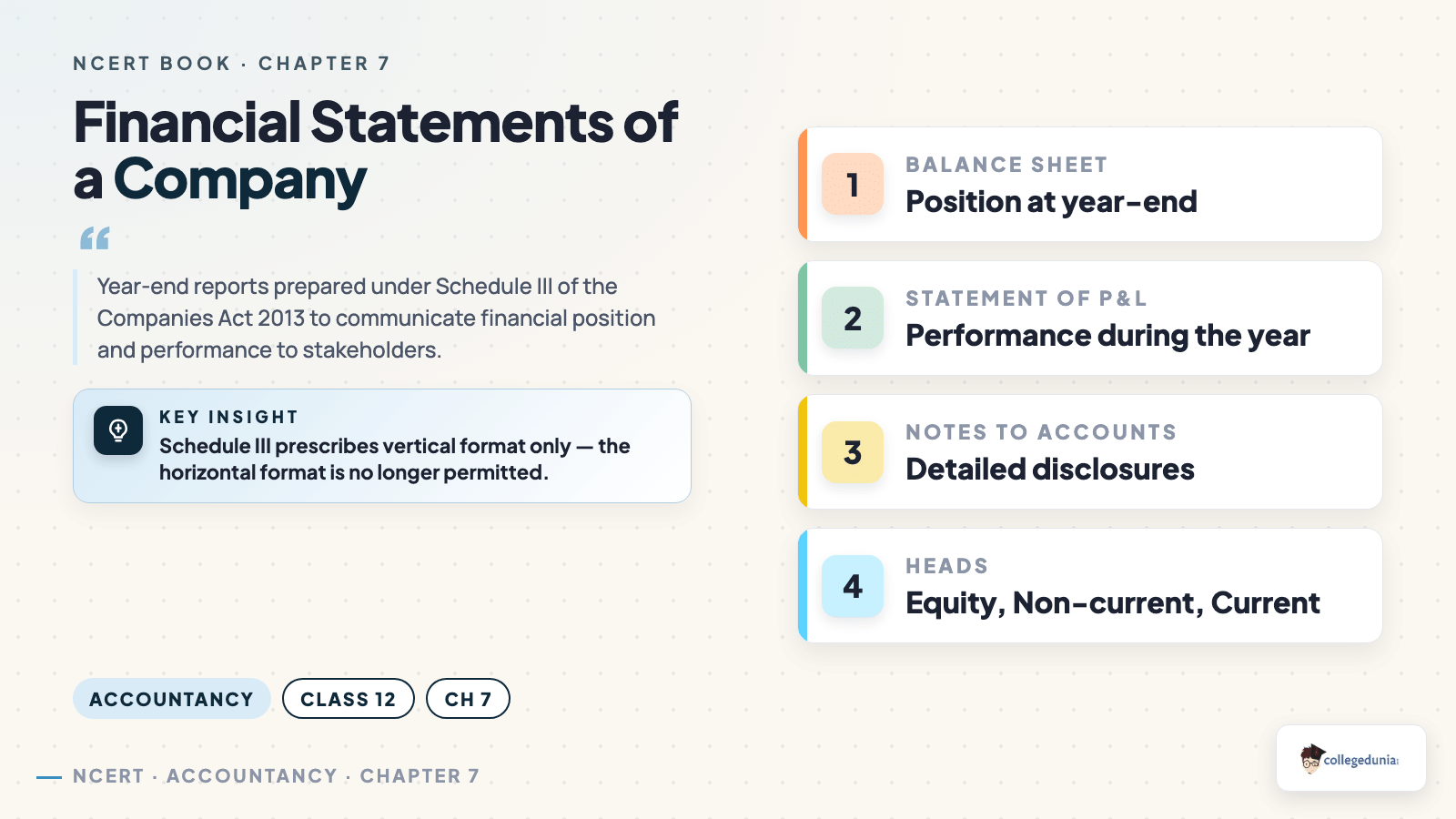

- Chapter Anchor: Schedule III, Part I (Balance Sheet) and Part II (Statement of Profit and Loss) of the Companies Act 2013

This PDF is the source the Collegedunia NCERT Solutions and Handwritten Notes refer to. Read this chapter before Part 2 Chapter 4 (Analysis of Financial Statements) and Part 2 Chapter 5 (Accounting Ratios), which both depend on the Schedule III line-item order.

Also Check:

- Financial Statements of a Company Class 12 NCERT Solutions PDF

- Financial Statements of a Company Class 12 Accountancy Notes

- Financial Statements of a Company Class 12 Handwritten Notes

How Will Collegedunia's Class 12 Accountancy Part 2 Chapter 3 NCERT Book PDF Help You?

Schedule III of the Companies Act 2013 is the single document that decides every line in the Part B paper. Reading the official NCERT chapter first builds the format in memory, so when the exam asks you to prepare a Balance Sheet from a trial balance, the line order is automatic. Collegedunia hosts the exact Reprint 2026-27 chapter the board references, along with the matching ncert class 12 accountancy book pdf chapter 7 Financial Statements of a Company resources for cross-checking.

- Page-faithful PDF: Schedule III Balance Sheet and Statement of Profit and Loss appear exactly as printed by NCERT, with original line-item numbering retained.

- Direct download: no sign-up or paywall before the file opens; print-ready for revision marking.

- Connected resources: the Solutions, Notes and Handwritten Notes on Collegedunia reference this PDF by section number, so cross-checking a Notes to Accounts entry takes one click.

Financial Statements of a Company Video Chapter Walkthrough

Source: Rajat Arora on YouTube

What the NCERT Class 12 Accountancy Part 2 Chapter 3 PDF Contains

The chapter is built around four numbered sections plus an extensive set of illustrations on the Schedule III Balance Sheet. Each section feeds directly into a board-paper question type, from line-classification multiple-choice to a full Balance Sheet preparation.

| Section | Topic | Why It Matters |

|---|---|---|

| 7.1 | Meaning of Financial Statements | Defines Balance Sheet and Statement of P&L for a company |

| 7.2 | Nature and Objectives of Financial Statements | One-mark and three-mark theory anchor |

| 7.3 | Form and Content of Balance Sheet (Schedule III Part I) | Single largest source of board marks in Part B |

| 7.4 | Statement of Profit and Loss (Schedule III Part II) | Five-head P&L format with Notes to Accounts |

| 7.x | Major Heads and Sub-heads, Notes to Accounts | Line-classification trap appears every year |

Schedule III Part I (Balance Sheet) is the source of an 8-mark numerical in 9 of the last 10 CBSE Class 12 Accountancy sessions.

Schedule III Balance Sheet Format at a Glance

The vertical Balance Sheet format printed in the chapter must be reproduced line for line in the board paper. Below is the order students should commit to memory before practising any numerical.

1. Shareholders' Funds: Share Capital, Reserves and Surplus, Money received against share warrants

2. Share Application Money pending allotment

3. Non-Current Liabilities: Long-term Borrowings, Deferred Tax Liabilities (net), Other Long-term Liabilities, Long-term Provisions

4. Current Liabilities: Short-term Borrowings, Trade Payables, Other Current Liabilities, Short-term Provisions

II. Assets

1. Non-Current Assets: Property, Plant and Equipment and Intangible Assets, Non-current Investments, Long-term Loans and Advances, Other Non-current Assets

2. Current Assets: Current Investments, Inventories, Trade Receivables, Cash and Cash Equivalents, Short-term Loans and Advances, Other Current Assets

Always cite "Note No." against any head where you have added a Note to Accounts. The CBSE marking scheme awards a separate mark for the correct Note reference even when the figure is right.

Class 12 Accountancy Part 2 Chapter 3 PYQ Trends in CBSE Board Exams

Financial Statements of a Company is a guaranteed entry in the Part B paper. The CBSE pattern alternates between a full 8-mark Balance Sheet preparation and a 3 to 4-mark line-classification or sub-head question on Schedule III.

| Year | Question Type | Marks | Sub-topic |

|---|---|---|---|

| 2025 | Long answer | 8 | Balance Sheet preparation with three Notes to Accounts |

| 2024 | Short answer | 3 | Major heads and sub-heads classification (six items) |

| 2023 | Long answer | 6 | Statement of Profit and Loss with five heads of income and expenses |

| 2022 | MCQ + Short | 1+3 | Note No. reference; current versus non-current classification |

| 2021 | Long answer | 8 | Balance Sheet from trial balance with adjustments |

Classification of an item into the correct Schedule III head is worth 1 mark each in the board marking scheme.

2026-27 Edition Notes for Part 2 Chapter 3

The current 2026-27 syllabus keeps Part 2 Chapter 3 Financial Statements of a Company unchanged from the previous reprint. Schedule III formats are intact, the Notes to Accounts illustration is retained, and no major or sub-head has been dropped. Students who used the 2024-25 or 2025-26 PDF can continue with the same problem set, but the page numbers in the new reprint shift by 1 to 2 pages because of front-matter changes.

"Money Received against Share Warrants" remains a separate line under Shareholders' Funds in the 2026-27 NCERT chapter. Some private guides have folded it into Reserves and Surplus; the official format keeps it separate, and CBSE has accepted only the NCERT order.

Five Common Mistakes Students Make in Part 2 Chapter 3

These five errors cost the most marks in Part B answer scripts year after year, according to CBSE evaluation reports.

2. Provision for Tax. Always a Short-term Provision under Current Liabilities, never under Reserves and Surplus.

3. Securities Premium. Sits under Reserves and Surplus, not under Share Capital. Mis-classification is a one-mark deduction.

4. Loose Tools. Part of Inventories under Current Assets, not Property, Plant and Equipment.

5. Public Deposits. Treated as Long-term Borrowings, even though the word "deposit" suggests an asset.

Class 12 Accountancy Chapter Weightage Snapshot

Part 2 Chapter 3 sits inside Part B (Financial Statements Analysis, 40 marks). Within Part B, the four chapters share the load as below.

| Chapter | Topic | CBSE Marks (typical) |

|---|---|---|

| Part 2 Ch 3 | Financial Statements of a Company | 8 to 10 |

| Part 2 Ch 4 | Analysis of Financial Statements | 3 to 4 |

| Part 2 Ch 5 | Accounting Ratios | 8 to 10 |

| Part 2 Ch 6 | Cash Flow Statement | 6 to 8 |

Full reference table: Class 12 Accountancy Weightage and Trend Notes

Related Resources for Part 2 Chapter 3

- Class 12 Accountancy Part 2 Chapter 3 NCERT Solutions

- Class 12 Accountancy Part 2 Chapter 3 Notes

- Class 12 Accountancy Part 2 Chapter 3 Handwritten Notes

NCERT Book PDF for Class 12 Accountancy: All Chapters

The full set of Class 12 Accountancy chapter PDFs, Part 1 and Part 2, sourced from the Reprint 2026-27 NCERT release.

| Chapter | Title |

|---|---|

| Chapter 1 | Accounting for Partnership: Basic Concepts NCERT Book PDF |

| Chapter 2 | Reconstitution: Admission of a Partner NCERT Book PDF |

| Chapter 3 | Reconstitution: Retirement / Death NCERT Book PDF |

| Chapter 4 | Dissolution of Partnership Firm NCERT Book PDF |

| Part 2 Chapter 1 | Accounting for Share Capital NCERT Book PDF |

| Part 2 Chapter 2 | Issue and Redemption of Debentures NCERT Book PDF |

| Part 2 Chapter 4 | Analysis of Financial Statements NCERT Book PDF |

| Part 2 Chapter 5 | Accounting Ratios NCERT Book PDF |

| Part 2 Chapter 6 | Cash Flow Statement NCERT Book PDF |

FAQs on Class 12 Accountancy Part 2 Chapter 3 NCERT Book PDF

FAQs on Class 12 Accountancy Part 2 Chapter 3 NCERT Book PDF

Ques. Is this the official NCERT Class 12 Accountancy Part 2 Chapter 3 PDF?

Ans.

Yes. This is the Reprint 2026-27 edition of Class 12 Accountancy Part 2, Part 2 Chapter 3 Financial Statements of a Company, sourced from ncert.nic.in and aligned to the CBSE 2026-27 syllabus.

Ques. What is Schedule III of the Companies Act 2013?

Ans.

Schedule III is the statutory format prescribed under Section 129 of the Companies Act 2013 for the presentation of a company's Balance Sheet (Part I) and Statement of Profit and Loss (Part II). The NCERT Class 12 Accountancy Part 2 Chapter 3 prints both parts verbatim, and CBSE board questions follow this format strictly.

Ques. What weightage does Part 2 Chapter 3 carry in the CBSE Class 12 Accountancy board exam?

Ans.

Part 2 Chapter 3 contributes 8 to 10 marks in the Part B paper, usually as a single 8-mark Balance Sheet preparation question plus a 3 to 4-mark line-classification question. A full Balance Sheet question has appeared in 9 of the last 10 CBSE sessions.

Ques. What is the difference between Major Heads and Sub-Heads in Schedule III?

Ans.

Major Heads are the top-level categories on the Balance Sheet (Shareholders' Funds, Non-Current Liabilities, Current Liabilities, Non-Current Assets, Current Assets). Sub-Heads sit one level below (for example, Share Capital, Reserves and Surplus, Long-term Borrowings). Each item in a numerical must be placed in both its Major Head and its correct Sub-Head to score the full mark.

Ques. Are Notes to Accounts mandatory in the Balance Sheet?

Ans.

Yes. Every line item in the Schedule III Balance Sheet that is an aggregate (such as Reserves and Surplus, Trade Payables, Property Plant and Equipment) must reference a Note No. and a supporting Note to Accounts schedule. CBSE awards a separate mark for the correct Note reference even when the aggregate figure is right.

Ques. How is Calls in Arrears shown in the company Balance Sheet?

Ans.

Calls in Arrears is shown as a deduction from Subscribed Capital under the Share Capital Sub-Head of Shareholders' Funds. It is never classified as a current asset, even though it represents money receivable from shareholders.

Comments