These ncert class 12 accountancy notes chapter 2 Reconstitution of a Partnership Firm: Admission of a Partner condense the heaviest Long-Answer chapter in Part A of the Class 12 paper into a single 19-page revision PDF aligned to the 2026-27 NCERT. The notes track the six adjustments triggered when a new partner joins, with every rule, ratio, and journal entry laid out the way CBSE markers expect.

- CBSE Weightage: 8 to 12 marks per board paper (one 6-mark plus one short numerical, on average)

- Question Count Inside: 3 CBSE PYQ solutions (2022 to 2024), 4 graded practice problems, and 1 full-cycle solved problem covering all six adjustments

The notes cover every NCERT topic in Chapter 2: the six admission adjustments, new profit-sharing ratio in three sub-cases, sacrificing ratio, all four goodwill valuation methods, the AS-26 alignment that prohibits raising goodwill in books, the Revaluation Account, four sub-cases of goodwill treatment, accumulated reserves and Profit and Loss distribution, and capital adjustment to the new ratio.

Collegedunia notes are prepared by Chartered Accountants and Commerce educators, aligned to the 2026-27 NCERT, and refined against the last five years of CBSE Class 12 Accountancy board papers.

Also Check:

- Admission of a Partner Class 12 NCERT Solutions

- Accounting for Partnership Basic Concepts Class 12 Notes

- CBSE Class 12 Accountancy Syllabus 2026-27

How will Collegedunia's NCERT Notes for Admission of a Partner Help You?

The Admission of a Partner chapter sits at the intersection of three skills: ratio arithmetic, journal-entry discipline, and account preparation. Most students lose marks not because they forget a formula, but because they apply the right formula in the wrong adjustment. Collegedunia notes solve that problem by treating the six adjustments as a strict sequence, so the order of journal entries becomes muscle memory before the board paper.

In the 2024 CBSE paper, over 60% of Accountancy candidates lost at least two marks in this chapter to ratio-confusion errors. The notes target exactly that failure mode through:

- A single decision rule that tells you when to use old PSR, sacrificing ratio, or new PSR.

- Side-by-side journal entries for premium goodwill, hidden goodwill, and privately paid goodwill.

- AS-26 compliance flagged on every goodwill entry so you never wrongly raise goodwill in the firm's books.

- Step-numbered Revaluation Account preparation that mirrors the CBSE marking scheme.

Reconstitution of a Partnership Firm Admission of a Partner Video W...

Source: Commerce Wallah by PW on YouTube

Topics Covered in Admission of a Partner Class 12 Notes

The table below lists every NCERT sub-topic with its average CBSE mark allocation across the last five board papers. Use this to plan revision time: the goodwill cluster alone draws 8 to 10 marks on average, which is more than the entire weightage of some smaller chapters.

| Topic | Sub-topic | Average CBSE Marks |

|---|---|---|

| Reconstitution Framework | Four reconstitution events; six adjustments at admission | 2 to 3 |

| New Profit-Sharing Ratio | Default source from old PSR, specific fraction surrendered, equal share from each | 3 to 4 |

| Sacrificing Ratio | Old Share minus New Share; LCM method for fractions | 2 to 3 |

| Goodwill Valuation | Average Profit, Super Profit, Capitalisation, Weighted Average | 4 to 6 |

| Treatment of Goodwill | Premium method, hidden goodwill, privately paid, AS-26 no-raising rule | 3 to 4 |

| Revaluation Account | Asset and liability adjustments; gain or loss to old partners in old PSR | 4 to 6 |

| Reserves and Accumulated P&L | Distribution to old partners in old PSR before admission entries | 2 to 3 |

| Capital Adjustment | Based on new partner's capital or pre-agreed total capital | 3 to 4 |

What is Inside the Admission of a Partner Notes PDF

The 19-page PDF is built as a sequence, not a topic list. Each section closes with a one-line takeaway and a journal-entry summary card, so a 90-minute revision pass lands the entire chapter in active recall.

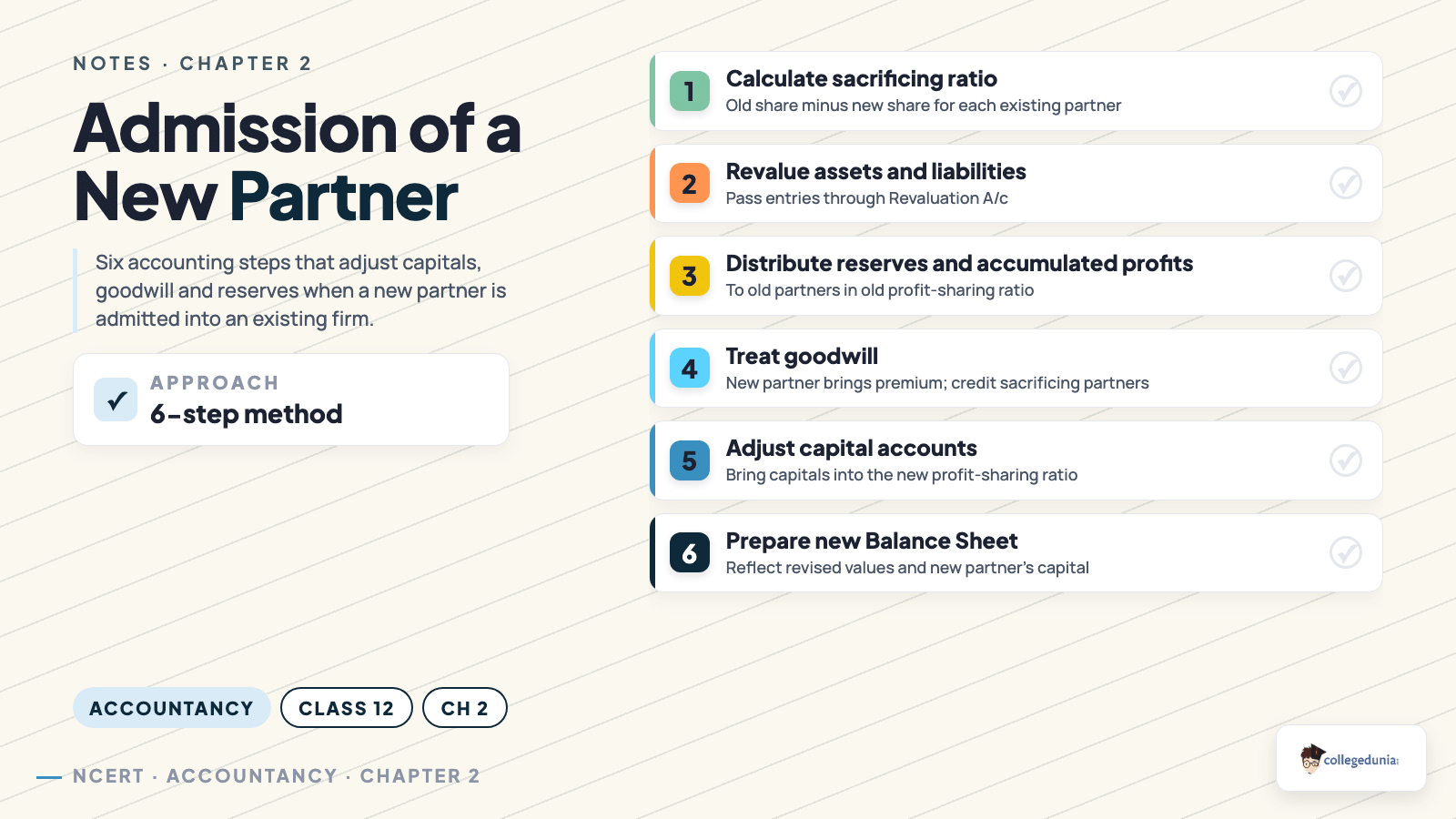

- Six-adjustment framework presented as the navigation spine for the whole chapter.

- Three cases of new profit-sharing ratio with a solved example for each.

- Four sub-cases of goodwill treatment with journal entries: premium received, premium not brought in, hidden goodwill, and goodwill paid privately.

- Full-cycle solved problem that runs through revaluation, goodwill, reserves, and capital adjustment in a single 8-mark question.

- Three CBSE PYQ solutions from board papers 2022, 2023, and 2024.

- Four graded practice problems with final answers and hint lines.

- Formula and journal-entry cheat sheet on the final page.

- One-page revision map for last-day recall.

Important Topics in Admission of a Partner for CBSE Class 12

- Six Adjustments at Admission. The mental framework: revaluation, reserves distribution, goodwill, new PSR, sacrificing ratio, capital adjustment.

- Sacrificing Ratio Formula. Sacrificing Ratio = Old Share minus New Share, expressed using a common denominator.

- Goodwill Valuation Methods. Average Profit, Super Profit, Capitalisation of Super Profit, and Weighted Average Profit. Each one has a different rationale and a different formula.

- Revaluation Account. Asset increases credited, liability increases debited; the net gain or loss is distributed to OLD partners in the OLD PSR before the new partner joins.

- Hidden Goodwill. Implied total capital based on the new partner's share minus actual total capital after adjustments equals the firm's hidden goodwill.

- AS-26 Alignment. Self-generated goodwill cannot be raised in the books. Goodwill is only credited to the old partners through the new partner's premium, never debited to a Goodwill A/c on the firm's books.

Common Mistakes Students Make in Admission of a Partner Numericals

Examiner reports from CBSE consistently flag the same handful of errors in this chapter. Reading the list once before the exam saves easy marks.

- Distributing revaluation gain in NEW ratio instead of OLD ratio. Revaluation is a pre-admission event; new partner has no share in it.

- Raising goodwill in the firm's books in violation of AS-26. The only correct entry is to credit goodwill to old partners through the premium brought by the new partner.

- Confusing sacrificing ratio with old ratio when premium is not specified separately.

- Forgetting to distribute General Reserve and accumulated Profit and Loss balance before passing the admission entries.

- Using the wrong base for hidden goodwill: the implied capital must be calculated from the new partner's capital and share, not from the total capital before admission.

Key Formulas for Reconstitution of a Partnership Firm Admission of a Partner

The four formulas below carry the bulk of the numerical workload. Yellow-highlighted expressions are the ones examiners ask candidates to state explicitly in 1-mark or 3-mark questions.

- Sacrificing Ratio = Old Share minus New Share

- Average Profit Goodwill = Average Profit × Number of Years' Purchase

- Super Profit = Actual Average Profit minus Normal Profit; Goodwill = Super Profit × Number of Years' Purchase

- Capitalised Value of Firm = Average Profit × (100 / Normal Rate of Return); Goodwill = Capitalised Value minus Net Assets

- Hidden Goodwill = (New Partner's Capital × Reciprocal of Share) minus Total Adjusted Capital of the Firm

Full PYQ map: Admission of a Partner NCERT Solutions with year-wise CBSE board questions.

NCERT Notes for Class 12 Accountancy: All Chapters

| Chapter | Chapter Title and Notes |

|---|---|

| Chapter 1 | Accounting for Partnership: Basic Concepts Notes |

| Chapter 3 | Reconstitution: Retirement or Death of a Partner Notes |

| Chapter 4 | Dissolution of Partnership Firm Notes |

| Chapter 5 | Accounting for Share Capital Notes |

| Chapter 6 | Issue and Redemption of Debentures Notes |

Related Resources for Admission of a Partner Class 12

- NCERT Solutions: Admission of a Partner

- Formula Sheet: Admission of a Partner

- Handwritten Notes: Admission of a Partner

- NCERT Book PDF: Admission of a Partner

Frequently Asked Questions

Frequently Asked Questions

Ques. Are these Class 12 Accountancy Chapter 2 notes aligned to the 2026-27 syllabus?

Ans.

Yes. Every six-adjustment rule, formula, AS-26 clause and CBSE marking-scheme reference matches the 2026-27 NCERT textbook.

Ques. What are the six adjustments at the admission of a partner?

Ans.

Revaluation of assets and liabilities, distribution of accumulated reserves and Profit and Loss balance, treatment of goodwill, computation of new profit-sharing ratio, computation of sacrificing ratio, and capital adjustment to the new ratio.

Ques. Why is goodwill never raised in the books at admission?

Ans.

Accounting Standard 26 prohibits the recognition of self-generated goodwill as an asset. At admission, goodwill is credited to the old partners in their sacrificing ratio through the premium brought in by the new partner. No Goodwill Account is created on the firm's books.

Ques. How is hidden goodwill calculated?

Ans.

Multiply the new partner's capital by the reciprocal of their share to get the implied total capital of the firm. Subtract the actual total adjusted capital (after revaluation and reserves distribution) from this implied capital. The positive difference is hidden goodwill, shared by old partners in their sacrificing ratio.

Ques. Are the notes enough for the CBSE Class 12 board exam?

Ans.

Yes. Combined with the NCERT Solutions PDF, the notes cover every concept, formula, and answer pattern tested in CBSE Class 12 Accountancy board papers from 2020 to 2025.

Ques. What is the difference between sacrificing ratio and gaining ratio?

Ans.

Sacrificing ratio is used when an old partner's share is reduced, typically at admission. Gaining ratio is used when a continuing partner's share is increased, typically at retirement or death. The formula structure is the same, but the sign of the difference is reversed.

Ques. How long is the Admission of a Partner notes PDF?

Ans.

19 pages including the table of contents, the six-adjustment framework, all goodwill methods, three CBSE PYQ solutions, four graded practice problems, and a one-page revision map.

Comments