These class 10 economics notes chapter 3 Money and Credit bring together every definition, comparison table, and example that the CBSE board paper actually tests in 2026-27.

Chapter3MoneyandCreditNotes.pdf?page=1&dpi=150)

Chapter3MoneyandCreditNotes.pdf?page=2&dpi=150)

Chapter3MoneyandCreditNotes.pdf?page=3&dpi=150)

Chapter3MoneyandCreditNotes.pdf?page=4&dpi=150)

Chapter3MoneyandCreditNotes.pdf?page=5&dpi=150)

Chapter3MoneyandCreditNotes.pdf?page=6&dpi=150)

Chapter3MoneyandCreditNotes.pdf?page=7&dpi=150)

Chapter3MoneyandCreditNotes.pdf?page=8&dpi=150)

Chapter3MoneyandCreditNotes.pdf?page=9&dpi=150)

Chapter3MoneyandCreditNotes.pdf?page=10&dpi=150)

Chapter3MoneyandCreditNotes.pdf?page=11&dpi=150)

Chapter3MoneyandCreditNotes.pdf?page=12&dpi=150)

Chapter3MoneyandCreditNotes.pdf?page=13&dpi=150)

Chapter3MoneyandCreditNotes.pdf?page=14&dpi=150)

Chapter3MoneyandCreditNotes.pdf?page=15&dpi=150)

Chapter3MoneyandCreditNotes.pdf?page=16&dpi=150)

Chapter3MoneyandCreditNotes.pdf?page=17&dpi=150)

Chapter3MoneyandCreditNotes.pdf?page=18&dpi=150)

Chapter3MoneyandCreditNotes.pdf?page=19&dpi=150)

Chapter3MoneyandCreditNotes.pdf?page=20&dpi=150)

Chapter3MoneyandCreditNotes.pdf?page=21&dpi=150)

The notes cover money as a medium of exchange, modern forms of money, how banks lend, the terms of credit, the formal and informal sectors, and Self Help Groups, all according to the latest 2026-27 NCERT Understanding Economic Development textbook.

- This chapter usually carries 5 to 6 marks across one short answer and one long answer.

- Most-tested ideas: double coincidence of wants, terms of credit, and formal versus informal sources.

- The Salim and Swapna credit examples and the Self Help Group idea appear almost every year.

Each set of money and credit class 10 notes in this Collegedunia compilation is curated by subject experts, mapped to the 2026-27 NCERT, and refined against the last five years of CBSE board papers.

Student Feedback: What 13,420 students told us about the Money and Credit chapter

81% of Class 10 students surveyed rated the difference between the formal and informal sources of credit as the part they found hardest. Most students said the Salim and Swapna comparison made the idea of a debt trap click in one read.

Source: 2026-27 Class 10 Economics student poll. Sample of 13,420 students from CBSE schools across 15 states.

What Money and Credit Means in Class 10 Economics

Money is anything widely accepted as a means of payment. Before money, people swapped goods directly, which was slow and difficult. The chapter starts from this problem before moving to banks and credit.

- Money acts as a medium of exchange, so people no longer need to swap one good for another.

- Credit means a loan, where one side gets money now and promises to pay back later.

- Credit can help a person grow, or it can pull a person into debt, depending on the situation.

Money makes buying and selling easy because both sides accept it. Money removes the need to match what two people want at the same time. This single idea is the base of the whole chapter and a common one-mark recall point.

The Barter System and the Double Coincidence of Wants

Before money, people used the barter system, exchanging goods directly. This worked only when both sides wanted what the other had, which made trade hard.

| System | How an Exchange Happens |

|---|---|

| Barter (no money) | A shoe-maker who wants wheat must find a wheat-grower who also wants shoes |

| Money used | The shoe-maker sells shoes for money, then buys wheat with that money |

In barter, both people must want each other's goods at the same time. This is called the double coincidence of wants. Money is the intermediate step that ends the double coincidence of wants. A person sells goods for money, then uses that money to buy what they need, so the two halves of a deal are split.

Watch the Full Money and Credit Chapter Explained for Class 10

Source: Magnet Brains on YouTube

Modern Forms of Money: Currency, Deposits and Cheques

Modern money is not gold or silver. It takes the form of currency, bank deposits and cheques, defined below.

| Form of Money | What It Means in the Chapter |

|---|---|

| Currency (notes and coins) | The Reserve Bank of India issues currency on behalf of the central government |

| Legal tender | No one in India can refuse a payment made in rupees, as the law backs it |

| Demand deposits | Money kept in a bank account that can be withdrawn on demand |

| Cheque | A paper that tells the bank to pay a sum from the writer's account, with no cash needed |

Indian notes carry no value of their own, yet everyone accepts them. A rupee note is accepted because the RBI issues it and the law makes it legal tender. A bank deposit also counts as money, since you can withdraw it or pay by cheque any time.

Loan Activities of Banks and How Banks Earn

Banks keep a small part of deposits as a reserve and lend out the rest, earning income from the gap:

- Banks keep only about 15% of deposits as cash to pay people who come to withdraw money.

- The rest is given out as loans to people who need credit for farming, trade, or business.

- Banks charge a higher interest from borrowers than the interest they pay to depositors.

- This difference between the two interest rates is the bank's main source of income.

Banks earn from the gap between interest charged to borrowers and interest paid to depositors. A frequent three-mark board question, so learn the 15% reserve idea and the interest gap.

Two Sides of Credit: Salim and Swapna

Credit can help one person and harm another. The NCERT uses two short stories to compare the good and bad outcomes of a loan.

| Case | What Happens | Outcome |

|---|---|---|

| Salim (festival shoes) | Takes credit to finish a large shoe order in the festival season and delivers on time | Credit helps; he earns a profit and repays easily |

| Swapna (cotton farmer) | Borrows to grow cotton, but the crop fails due to pests and she cannot repay | Credit harms; she falls into a debt trap and must sell her land |

The same tool, credit, gives two very different results. Credit helps when income rises after the loan, but harms when income fails and the debt grows. A common board question asks you to explain, with examples, when credit is useful and when it is harmful.

Terms of Credit and What Collateral Means

Every loan comes with conditions called the terms of credit, which decide how easy or hard a loan is for the borrower.

| Term of Credit | What It Means |

|---|---|

| Interest rate | The extra amount the borrower pays on top of the borrowed sum |

| Collateral | An asset like land, a building, a vehicle, or deposits, pledged as a guarantee until the loan is repaid |

| Documentation | The papers a lender asks for, such as proof of income or land records |

| Mode of repayment | How and when the loan must be paid back, in cash or in instalments |

Collateral is an asset the borrower owns and pledges to the lender as a guarantee for the loan. If a borrower fails to repay, the lender can sell it. Easy terms mean low interest and little collateral; tough terms mean high interest and heavy collateral.

Variety of Credit: The Sonpur Village Example

People borrow from many sources, not banks alone. The NCERT uses Sonpur village to show this variety:

- Formal sources: banks and cooperatives that follow government rules.

- Informal sources: moneylenders, traders, employers and relatives, with no outside control.

- A small farmer may borrow from a moneylender at a very high rate when a bank loan is hard to get; a richer farmer gets a cheaper bank loan because he owns land to pledge.

Formal sources charge low, controlled interest, while informal sources can charge very high interest. The source of a loan matters as much as the loan itself.

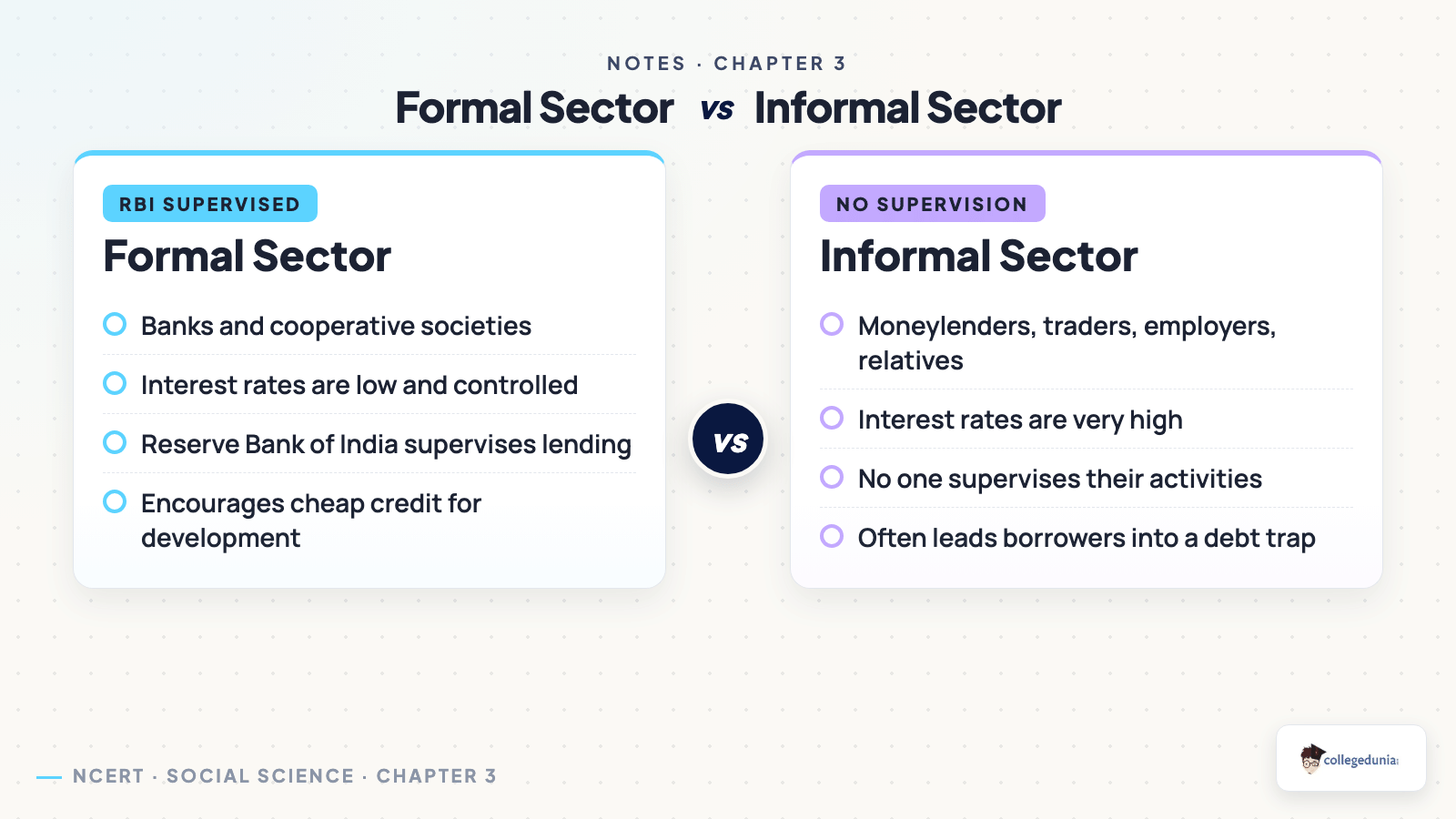

Formal Versus Informal Sources of Credit

The divide between formal and informal sectors decides who watches the lender and how much interest a borrower pays.

| Point | Formal Sector | Informal Sector |

|---|---|---|

| Examples | Banks and cooperative societies | Moneylenders, traders, employers, relatives |

| Who supervises | The Reserve Bank of India supervises and checks them | No one supervises the lender or the rate charged |

| Interest rate | Low and reasonable | Very high, which can cause a debt trap |

The RBI checks that formal lenders give loans fairly and do not charge too much. In rural India, about 85% of poor households depend on informal sources of credit. Cheap and affordable credit is crucial for the country's development, so India needs to expand formal credit and reduce its reliance on costly informal loans.

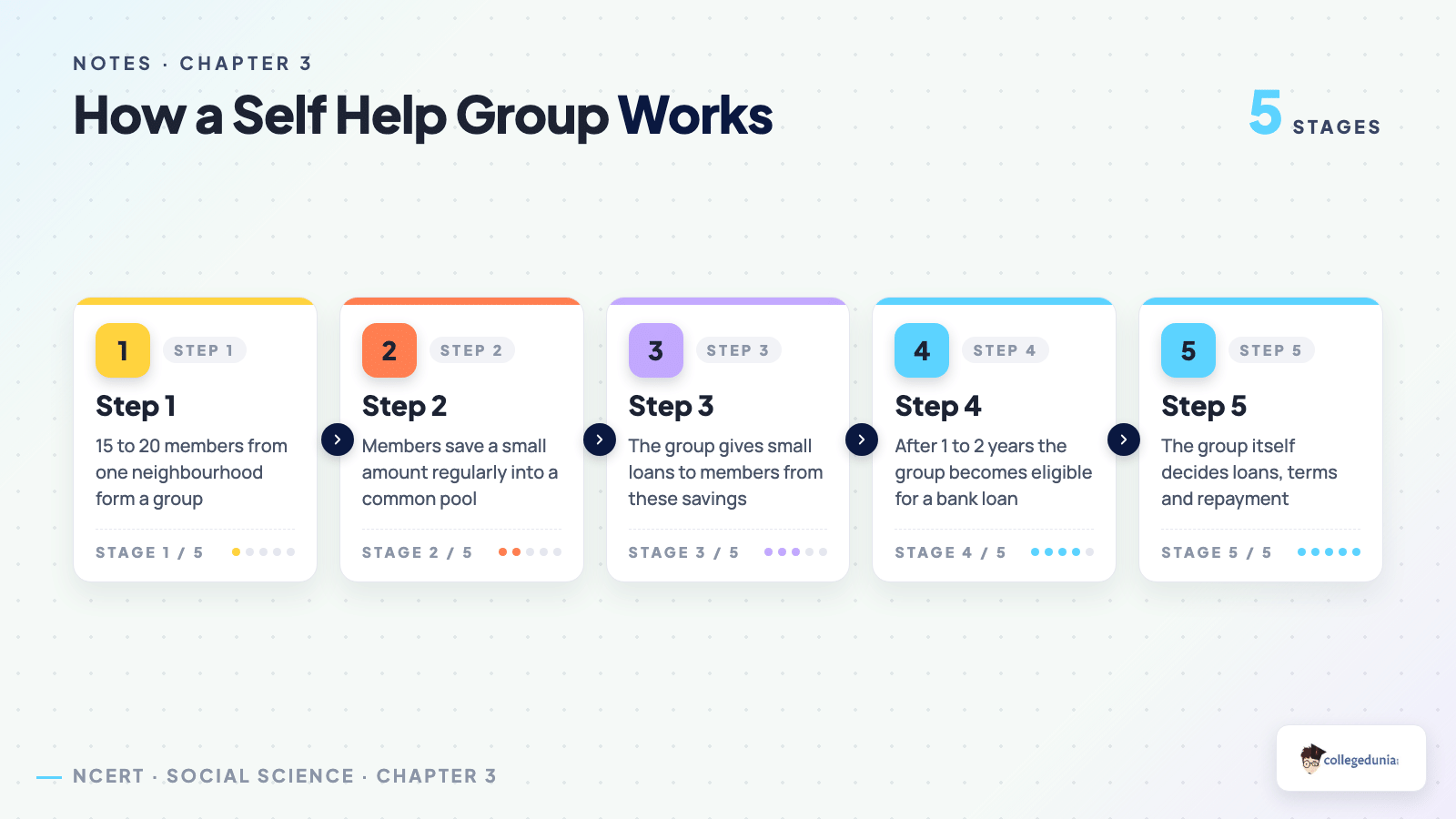

Self Help Groups and the Grameen Bank Idea

Poor people often cannot get bank loans because they have no collateral. Self Help Groups (SHGs) solve this by turning small savings into bank credit.

- An SHG usually has 15 to 20 members from one neighbourhood who meet and save a little money every month.

- Members can take small loans from the group's pooled savings at a fair rate.

- After the group saves for a year or two, a bank gives the SHG a loan against its savings.

- Group responsibility means every member helps ensure the loan is repaid, which replaces collateral.

The idea grew from the Grameen Bank of Bangladesh, started by Muhammad Yunus, which lends to the poor without collateral. An SHG gives the poor access to credit and frees them from high-cost moneylenders, and helps women take part in village decisions.

Important Questions and Previous Year Trends

The board tests this chapter through definitions, comparisons, and reasoning questions:

- One-mark: define double coincidence of wants; what is collateral; who issues currency in India.

- Three-mark: how do banks earn their income; explain any three terms of credit.

- Five-mark: compare formal and informal sources of credit; explain how a Self Help Group works.

Revise the formal versus informal table and the four terms of credit as your priority. That covers about 80% of what the chapter asks in the 2026-27 session.

How These Notes Pair with NCERT Solutions and the Book PDF

These notes give you the concept base. To score full marks, pair them with the other resources for the same chapter. Read the table below and follow the links to the matching resource type.

| Resource | Best For | Open |

|---|---|---|

| NCERT Solutions | Model answers to every back-exercise question | NCERT Solutions for Money and Credit |

| Handwritten Notes | Quick one-shot revision before the exam | Handwritten Notes for Money and Credit |

| NCERT Book PDF | Reading the original chapter text | NCERT Book PDF for Money and Credit |

All Chapters Notes for Class 10 Economics Understanding Economic Development

Once this chapter is done, move to the other chapters of the book. Each link below opens the Notes page for that chapter in the same subject.

| Chapter | Topic | Notes Link |

|---|---|---|

| Chapter 1 | Development | Development Class 10 Notes |

| Chapter 2 | Sectors of the Indian Economy | Sectors of the Indian Economy Class 10 Notes |

| Chapter 4 | Globalisation and the Indian Economy | Globalisation and the Indian Economy Class 10 Notes |

| Chapter 5 | Consumer Rights | Consumer Rights Class 10 Notes |

Ques. What is the double coincidence of wants in money and credit class 10?

Ans. The double coincidence of wants means both people in a barter exchange must want what the other has at the same time. A shoe-maker who wants wheat must find a wheat-grower who also wants shoes. Money removes this problem by acting as an intermediate step in any deal.

Ques. Why is money called a medium of exchange?

Ans. Money is called a medium of exchange because a person can sell goods for money and then use that money to buy other goods. The two halves of a deal no longer need to match, so trade becomes quick and easy.

Ques. What are the modern forms of money?

Ans. The modern forms of money are currency, which means the notes and coins issued by the Reserve Bank of India, and deposits kept in banks. People can also pay through a cheque, which tells the bank to pay a sum from the account without using cash.

Ques. How do banks earn their income in the class 10 economics chapter 3 notes?

Ans. Banks keep about 15% of deposits as cash and lend the rest as loans. They charge a higher interest from borrowers than the interest they pay to depositors. The difference between these two interest rates is the bank's main income.

Ques. What is collateral in money and credit notes class 10?

Ans. Collateral is an asset that a borrower owns and pledges to the lender as a guarantee for a loan. It can be land, a building, a vehicle, or bank deposits. If the borrower fails to repay, the lender can sell the collateral to recover the money.

Ques. What is the difference between formal and informal sources of credit?

Ans. Formal sources are banks and cooperatives that the Reserve Bank of India supervises, and they charge low interest. Informal sources are moneylenders, traders, employers, and relatives, who are not supervised and can charge very high interest, which may lead to a debt trap.

Ques. How does a Self Help Group work?

Ans. A Self Help Group has 15 to 20 members who save a small amount every month. Members take small loans from the pooled savings, and after a year or two a bank gives the group a loan. Group responsibility replaces collateral and ensures the loan is repaid.

Ques. How much weightage do the money and credit class 10 notes carry in the board exam?

Ans. The chapter usually carries about 5 to 6 marks in the CBSE board paper for the 2026-27 session, split across a short answer and a long answer on the terms of credit, the formal versus informal sectors, or Self Help Groups.

Comments