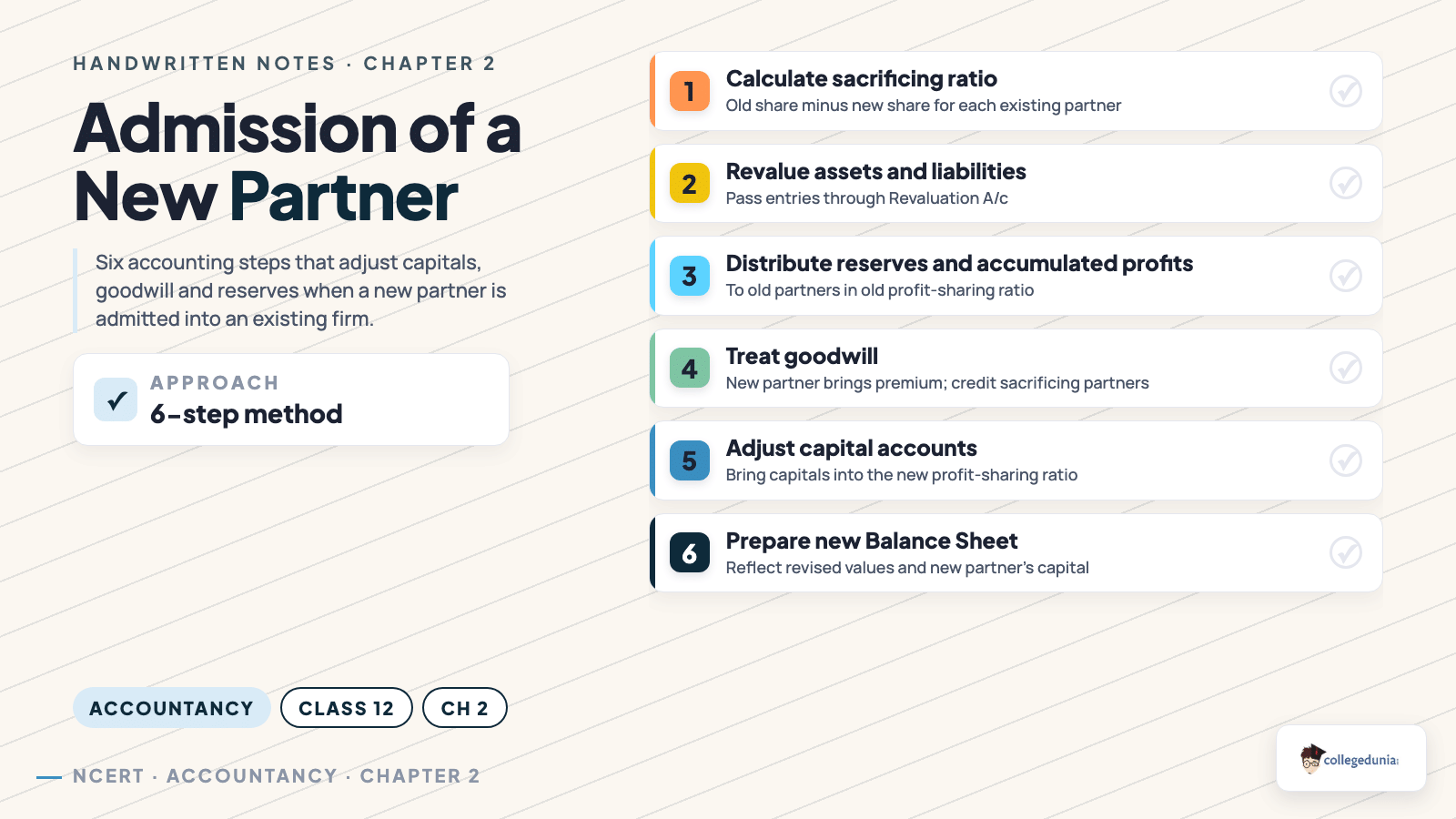

The Reconstitution of a Partnership Firm – Admission of a Partner class 12 accountancy handwritten notes below convert the longest Unit 1 chapter into a single scanned notebook, written in blue ballpoint ink on ruled paper, with the six admission adjustments boxed in the exact order a CBSE answer sheet expects: new profit-sharing ratio, sacrificing ratio, goodwill, revaluation of assets and liabilities, reserves and accumulated profits, and capital adjustment.

- CBSE Weightage: 10 to 12 marks (Unit 1: Accounting for Partnership Firms, shared across Chapters 1 to 5, with admission carrying the heaviest 8-mark numerical slot)

The PDF spans 9 ruled pages and 13 sub-topics, with hand-drawn formula boxes, a full Revaluation A/c T-account specimen, and red-ink margin arrows on the goodwill premium-method journal entries.

Curated by senior commerce educators, aligned to the 2026-27 NCERT print, and styled to mirror the rough notebook a Class 12 topper would actually carry into the board exam hall.

Also Check:

- Admission of a Partner Class 12 Notes (Typed PDF)

- Class 12 Accountancy Chapter 2 NCERT Solutions

- CBSE Class 12 Accountancy Syllabus 2026-27

Why the Admission of a Partner Chapter Decides the Accountancy Paper

Admission of a partner is the chapter examiners use to set the long 8-mark numerical. Almost every CBSE Class 12 Accountancy paper since 2018 has carried one full Revaluation A/c plus Partners' Capital A/c question from this chapter, and the marks lost here are usually the difference between a 90+ and a low-80s scorecard. The handwritten format helps because the six admission adjustments are sequential, and a ruled-paper layout fixes that sequence in visual memory.

Reconstitution of a Partnership Firm Admission of a Partner Video W...

Source: Commerce Wallah by PW on YouTube

How will Collegedunia's Admission of a Partner Handwritten Notes Help You?

Typed notes read like a textbook. Handwritten notes read like a friend's revision book, which is why the brain locates a formula faster on exam day. The Collegedunia handwritten set keeps every adjustment, every journal entry, and every account format on ruled paper so the full chapter can be flipped through in under 30 minutes the night before the paper.

- Pen-style sub-headings separate the six adjustments so the navigation spine of the chapter is visible at a glance.

- Boxed journal-entry samples for all four goodwill premium-method cases sit on one facing page, removing the need to flip back to the NCERT textbook.

- The Revaluation A/c T-account is drawn in the exact column layout CBSE examiners reward in 6-mark and 8-mark questions.

- Red-ink margin arrows flag the tricky bits, such as the sign convention on the Revaluation A/c and the implied-total formula for hidden goodwill.

Sacrificing Ratio Table and the Old Minus New Shortcut

The sacrificing ratio page presents a notebook-style table that converts the standard three sub-cases into a single line each. The shortcut to remember is Sacrificing Ratio = Old Ratio - New Ratio, applied partner by partner.

| Sub-case | What the question says | How the notes solve it |

|---|---|---|

| 1. Only new partner's share given | "C is admitted for 1/4 share" | Remaining 3/4 split among old partners in their old ratio; sacrifice in old ratio |

| 2. New ratio given for all partners | "New ratio of A, B and C is 5:3:2" | Apply Old minus New for each old partner |

| 3. New partner acquires share from specific partners | "C gets 1/8 from A and 1/8 from B" | Sacrifice is exactly the share each old partner surrenders |

The page ends with a one-line caution: a negative sacrifice means that old partner is actually a gaining partner, and the gaining partner must compensate the sacrificing partner separately.

Goodwill Premium Method: Four Journal Entry Samples

The goodwill page carries all four premium-method scenarios as handwritten journal entries, each boxed and numbered so the correct entry can be located inside the answer sheet within seconds.

- Premium brought in cash and retained: Cash A/c Dr. to Premium for Goodwill A/c; then Premium for Goodwill A/c Dr. to Sacrificing Partners' Capital A/cs in the sacrificing ratio.

- Premium brought in cash and withdrawn: add a third entry, Sacrificing Partners' Capital A/cs Dr. to Cash A/c, for the amount withdrawn.

- Premium not brought in cash: New Partner's Capital A/c Dr. to Sacrificing Partners' Capital A/cs in the sacrificing ratio.

- Existing goodwill in books: first write off, Old Partners' Capital A/cs Dr. (in old ratio) to Goodwill A/c, then post the appropriate entry from cases 1 to 3 above.

Per AS-26, self-generated goodwill is never recorded in the books, so any existing goodwill on the balance sheet must be written off first before passing the admission entry.

Revaluation Account: T-Account Layout and Seven Rules

The Revaluation A/c page is the load-bearing page of the entire chapter. It carries the T-account in handwritten form with the standard items pre-placed on the correct side, and a margin-arrow list of the seven sign rules.

| Dr. side (Particulars) | Cr. side (Particulars) |

|---|---|

| To Decrease in asset value | By Increase in asset value |

| To Increase in liability | By Decrease in liability |

| To Unrecorded liability | By Unrecorded asset |

| To Profit transferred to Old Partners' Capital A/cs (in old ratio) | By Loss transferred to Old Partners' Capital A/cs (in old ratio) |

The balancing figure is profit when the credit side is larger and loss when the debit side is larger. The profit or loss on revaluation is distributed only among old partners in the old ratio, never to the incoming partner, because the new partner has not yet shared in the firm's earlier history.

Accumulated Profits and Reserves: One-Line Shortcut

The reserves page reduces a five-line rule to a single notebook entry. Every accumulated profit, general reserve, workmen compensation reserve surplus, and investment fluctuation reserve surplus on the balance sheet at the admission date is transferred to the old partners only, in the old ratio, before passing any revaluation or capital-adjustment entry. Accumulated losses (such as a debit balance of Profit and Loss A/c) move the same way.

- Reserve / accumulated profit: Reserve A/c Dr. to Old Partners' Capital A/cs (old ratio).

- Accumulated loss: Old Partners' Capital A/cs Dr. (old ratio) to Profit & Loss A/c.

- Workmen Compensation Reserve: retain claim portion as a liability, distribute the surplus.

- Investment Fluctuation Reserve: retain the fall in investment value, distribute the surplus.

Capital Adjustment of Old Partners on the Basis of New Partner's Capital

The last formula page covers the capital adjustment step, which CBSE links to a 4-mark or 6-mark sub-question every alternate year.

- Total capital of new firm = New Partner's Capital × Reciprocal of new partner's share.

- New capital of each old partner = Total Capital × That partner's share in the new ratio.

- Adjusted closing balance in each old partner's Capital A/c, after revaluation profit/loss, reserves, and goodwill adjustments, is compared with the new capital figure from step 2.

- Shortfall: partner brings in cash. Surplus: partner withdraws cash, or the difference is transferred to that partner's Current A/c.

For hidden-goodwill questions the implied total is computed as Implied Total Capital = New Partner's Capital × Reciprocal of share, and the gap between implied total and the actual combined adjusted capital of all partners is the hidden goodwill, distributed in the sacrificing ratio.

Related Resources

- Class 12 Accountancy Chapter 2 Notes (Typed)

- Class 12 Accountancy Chapter 2 NCERT Solutions

- Class 12 Accountancy Chapter 2 NCERT Book PDF

NCERT Handwritten Notes for Class 12 Accountancy: All Chapters

| Chapter | Handwritten Notes |

|---|---|

| Chapter 1 | Accounting for Partnership: Basic Concepts Handwritten Notes |

| Chapter 3 | Reconstitution of a Partnership Firm: Retirement / Death of a Partner Handwritten Notes |

| Chapter 4 | Dissolution of Partnership Firm Handwritten Notes |

Admission of a Partner Class 12 Handwritten Notes FAQs

Ques. Are the Class 12 Accountancy Chapter 2 handwritten notes free to download?

Ans.

Yes. The complete 9-page handwritten PDF on Reconstitution of a Partnership Firm: Admission of a Partner is free to download from this page.

Ques. Do these handwritten notes cover all six admission adjustments?

Ans.

Yes. The notes carry the new profit-sharing ratio, sacrificing ratio, goodwill (with all four premium-method journal entries), Revaluation A/c, reserves and accumulated profits, and capital adjustment on the basis of the new partner's capital, including hidden goodwill.

Ques. Are the notes aligned to the 2026-27 NCERT syllabus?

Ans.

Yes. Every account format, journal entry, and formula matches the 2026-27 NCERT print and the latest CBSE Class 12 Accountancy marking scheme.

Ques. What is the difference between sacrificing ratio and new ratio in this chapter?

Ans.

The new ratio is the post-admission profit-sharing ratio of all partners including the incoming partner. The sacrificing ratio is the difference between each old partner's old ratio and new ratio, and it is the ratio in which the incoming partner's goodwill premium is distributed.

Ques. Can I rely only on the handwritten notes for board revision?

Ans.

For last-week revision, the handwritten PDF is sufficient. For first-time learning, pair it with the typed Notes PDF and the NCERT Solutions PDF linked above so the chapter-end exercises and worked numericals are covered alongside.

Comments