These ncert class 12 accountancy notes chapter 5 Accounting for Share Capital compress 38 NCERT pages and 24 distinct journal-entry patterns into a single revision file covering the issue, allotment, calls, forfeiture, and re-issue cycle of equity shares in a public limited company. The notes are aligned to the 2026-27 NCERT Part B Reprint and the Companies Act, 2013, so every entry, every disclosure heading, and every Schedule III tag is current.

- CBSE Weightage: 8 to 10 marks (Part B, Company Accounts unit, Section A)

- Notes Length: 22-page revision PDF with two fully worked numericals and a Schedule III balance-sheet extract

| NCERT pages condensed | 38 pages into a 22-page revision file |

| Journal-entry patterns covered | 24 across issue, calls, forfeiture, re-issue |

| Solved numericals inside | 2 long-form plus 6 short scenario blocks |

These Notes are reviewed by Chartered Accountants and senior Commerce educators, mapped to the current 2026-27 NCERT Accountancy Part B textbook, and cross-checked against the last five years of CBSE Class 12 Board papers (2021 to 2025).

Also Check:

- Accounting for Share Capital Class 12 NCERT Solutions

- Dissolution of Partnership Firm Class 12 Accountancy Notes

- CBSE Class 12 Accountancy Syllabus 2026-27

Why Share Capital Accounting Matters in Class 12 Commerce

Part 2 Chapter 1 is the entry point to Company Accounts and the first time Class 12 students touch the Companies Act, 2013. CUET (UG) Accountancy, B.Com Corporate Accounting, and CA Foundation Accounts all open with this same skeleton: authorised, issued, called-up, and paid-up capital. Lock the four layers down here and the rest of the company-accounts syllabus reads as variations on one balance sheet.

Across 2021 to 2025 CBSE Boards, share-capital questions appeared in every Class 12 Accountancy paper, with an average yield of 8 to 10 marks. That makes it the highest-yield Part B chapter, ahead of Debentures and Financial Statements.

Class 12 Accountancy Part 2 Chapter 1 Accounting For Share Capital Notes

Source: Next Toppers - 12th Commerce on YouTube

How Will Collegedunia's NCERT Notes Help You Score the Full 8 to 10 Marks?

The Collegedunia revision file is built around the four-layer capital structure and the seven-stage life-cycle of a share. Each stage gets its own journal-entry skeleton, its own Schedule III disclosure tag, and one solved numerical built on a real CBSE prompt.

- One-page capital-layer diagram showing authorised, issued, subscribed, called-up, and paid-up capital with their inter-relationships and Schedule III line numbers.

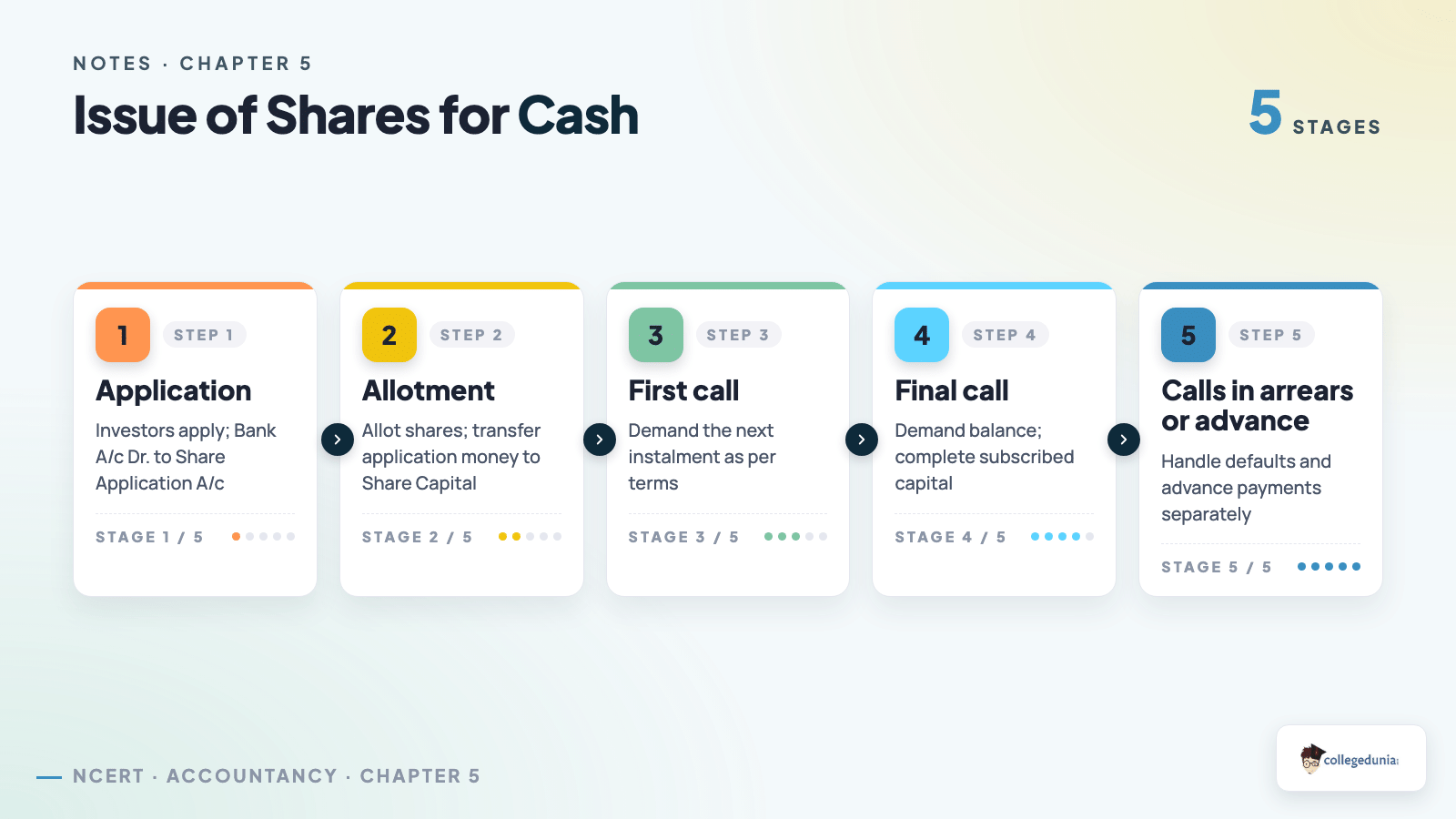

- Eight journal-entry skeletons for the standard issue cycle (application, allotment, first call, final call) with full / under / over-subscription handling.

- Forfeiture and re-issue workflow on one A4 spread, including the maximum-discount-on-reissue rule and the Capital Reserve transfer.

- Schedule III balance-sheet extract with the exact line-item wording the CBSE marker looks for.

The Four-Layer Capital Structure of a Company

The hardest 1-mark MCQ on this chapter is the difference between subscribed and called-up capital. The four-layer chain below is the answer key for every such question.

| Layer | Definition | Schedule III Disclosure |

|---|---|---|

| 1. Authorised Capital | Maximum capital a company can issue, fixed in the Memorandum of Association | Disclosed as a note, not added to the balance sheet total |

| 2. Issued Capital | Portion of authorised capital actually offered to the public | Disclosed as a note |

| 3. Subscribed Capital | Portion of issued capital that the public has applied for | Subscribed and Fully Paid-Up plus Subscribed but Not Fully Paid-Up |

| 4. Called-Up and Paid-Up Capital | Amount the company has called and actually received | The figure that flows into Equity and Liabilities, Note 1 |

Reserve Capital sits outside the four layers. It is the portion of uncalled capital that a company resolves (by special resolution) to call only at the time of winding up. Schedule III does not require it on the balance sheet face; it appears only in the notes.

Accounting for Share Capital Topic-wise Weightage for CBSE Boards

The table below shows how the 8 to 10 marks of this chapter typically split across sub-topics in the CBSE Class 12 Accountancy paper. The weightage tier is based on a five-year rolling count of board-paper appearances (2021 to 2025).

| Sub-Topic | Typical Marks | Weightage Tier |

|---|---|---|

| Forfeiture and Re-issue of Shares | 3 to 4 | High |

| Over-Subscription with Pro-Rata Allotment | 3 to 6 | High |

| Issue at Premium (Securities Premium Reserve) | 1 to 3 | High |

| Calls in Advance and Calls in Arrears | 1 to 3 | Medium |

| Issue of Shares for Consideration Other Than Cash | 3 | Medium |

| Private Placement and ESOP (theory) | 1 | Low |

| Sweat Equity Shares (theory) | 1 | Low |

Accounting for Share Capital: Topic-by-Topic Summary

Issue of Shares at Par, at Premium, and at Consideration Other Than Cash

Share money flows in three instalments: application, allotment, and one or more calls. The journal skeleton is the same at par or at premium: Bank A/c Dr. to Share Application A/c, then transfer to Share Capital A/c plus Securities Premium Reserve A/c on allotment. Section 52 of the Companies Act, 2013 restricts Securities Premium use to five purposes. For non-cash consideration (vendors, promoters), the entry is Sundry Assets A/c Dr. to Share Capital A/c, with any excess to Securities Premium Reserve.

Over-Subscription and Pro-Rata Allotment

Over-subscription means applications received exceed shares issued. Directors handle the excess in three ways: outright rejection, pro-rata allotment, or a mix. In pro-rata, the excess application money is adjusted against allotment first, then against calls. The allotment ratio = applications received / shares allotted, and excess money flows down the call schedule on the same ratio. CBSE typically sets a mix where some applicants get full allotment, some pro-rata, and some are refused.

Calls in Advance and Calls in Arrears

Calls in Advance is money a shareholder pays before the call is due. It is shown as a current liability under Other Current Liabilities and carries interest at 12% per annum under Table F of the Companies Act, 2013. Calls in Arrears is the reverse: money called but not received. It is shown as a deduction from Subscribed but Not Fully Paid-Up Capital and carries interest receivable at 10% per annum. Both are common 3-mark questions.

Forfeiture and Re-issue of Forfeited Shares

If a shareholder defaults on an allotment or call, the company can forfeit the shares after a statutory 14-day notice. Forfeiture cancels the called-up amount on the capital side and credits the amount already received to Share Forfeiture A/c. The maximum discount on re-issue is the balance in Share Forfeiture A/c for those shares; any further discount is illegal. The residual balance after re-issue is a capital profit transferred to Capital Reserve, the most-missed step in CBSE answers.

Private Placement, ESOP, and Sweat Equity Shares

These three surface as 1-mark MCQs or short parts of 3-mark questions. Private Placement is an offer to a select group (not the public) under Section 42. ESOP gives employees the right to buy shares at a pre-decided price under Section 62(1)(b). Sweat Equity Shares are issued at a discount or for non-cash consideration to directors or employees under Section 54. CBSE typically tests the section number and definition, not the journal entries.

Important Journal Entries Box for Accounting for Share Capital

The eight skeleton entries below cover roughly 90% of the CBSE Long Answer mark scheme on this chapter. Memorise the pattern, not the numbers; the numbers change every year, the pattern does not.

- Application money received: Bank A/c Dr. to Share Application A/c

- Application money transferred: Share Application A/c Dr. to Share Capital A/c (and to Securities Premium Reserve A/c if premium is charged on application)

- Allotment due: Share Allotment A/c Dr. to Share Capital A/c (plus Securities Premium Reserve A/c)

- Allotment received: Bank A/c Dr. to Share Allotment A/c

- Calls due: Share First Call A/c Dr. to Share Capital A/c

- Calls received: Bank A/c Dr. to Share First Call A/c

- Forfeiture: Share Capital A/c Dr. (called-up amount) to Share Forfeiture A/c (amount received) and to Share Allotment / Call A/c (amount due but not received)

- Re-issue and transfer to Capital Reserve: Bank A/c plus Share Forfeiture A/c Dr. to Share Capital A/c; then Share Forfeiture A/c Dr. to Capital Reserve A/c

Common Mistakes Students Make in Accounting for Share Capital

The four mistakes below cost more marks in CBSE Class 12 Accountancy than any other Part B chapter, according to the CBSE answer-key bulletins and our markers' debrief notes.

- Calling the credit side of forfeiture "Share Capital". The credit is to Share Forfeiture A/c. Share Capital is debited, not credited, on forfeiture. This single mistake costs 2 marks in a 6-mark Long Answer.

- Forgetting the Capital Reserve transfer after re-issue. The marker is waiting for the second entry that transfers the residual Share Forfeiture balance to Capital Reserve.

- Confusing Securities Premium Reserve with Capital Reserve. Securities Premium is collected on issue at premium; Capital Reserve is the residual profit on re-issue. Both sit under Reserves and Surplus, but they are different line items with different uses.

- Treating Calls in Advance as part of Share Capital. It is a current liability shown under Other Current Liabilities, not capital. Only the called-up amount is capital.

Most Repeated Accounting for Share Capital Board Questions

The four CBSE-style prompts below appeared in at least two of the five most recent Class 12 Accountancy Boards (2021 to 2025) in some form. Practise the pattern, not the exact wording.

| Prompt Pattern | Marks | Last Seen |

|---|---|---|

| Pass journal entries for issue of shares with pro-rata allotment, calls, forfeiture, and re-issue | 6 | 2025, 2023, 2021 |

| Distinguish between Reserve Capital and Capital Reserve | 3 | 2024, 2022 |

| Calculate the amount transferred to Capital Reserve after re-issue of forfeited shares | 3 | 2025, 2023 |

| Show Share Capital in the Schedule III balance sheet of a company | 4 | 2024, 2022, 2021 |

Real-World Applications of Share Capital Accounting

The same four-layer capital chain appears on every listed Indian company's annual report. Reading one alongside these notes will make the Schedule III line items click.

- Reliance Industries bonus issue of 1:1 in 2024 used the Securities Premium Reserve under Section 52, exactly the way the NCERT example shows.

- Tata Consultancy Services reports authorised, issued, and subscribed capital separately in its FY 2024-25 annual report Note 18, matching the four-layer chain in this chapter.

- Hyundai Motor India IPO 2024 prospectus carries the same application, allotment, and call structure the chapter describes, scaled to thousands of crores.

Previous Year CBSE Question Mapping for Part 2 Chapter 1

The Solutions page carries the full year-wise PYQ map with every question, options, and step-mark answer. The mini-table below is a five-year highlight strip of the most repeated question types in CBSE Class 12 Accountancy Board papers, with the latest year first.

| Year | Question Type Seen | Marks |

|---|---|---|

| 2025 | Issue with pro-rata, forfeiture, and re-issue Long Answer | 6 |

| 2024 | Reserve Capital vs Capital Reserve theory plus Schedule III extract | 3 + 4 |

| 2023 | Forfeiture of partly-paid shares with computation of Capital Reserve | 6 |

| 2022 | Issue at premium with non-cash consideration to vendors | 3 |

| 2021 | Calls in Advance and Calls in Arrears journal entries | 3 |

Full year-wise PYQ map: Accounting for Share Capital Class 12 NCERT Solutions

Related Resources

- Accounting for Share Capital Class 12 NCERT Solutions

- Accounting for Share Capital Class 12 Handwritten Notes

- Accounting for Share Capital Class 12 NCERT Book PDF

NCERT Notes for Class 12 Accountancy: All Chapters

| Chapter | Notes |

|---|---|

| Chapter 1 | Accounting for Partnership: Basic Concepts Notes |

| Chapter 2 | Reconstitution of a Partnership Firm: Admission of a Partner Notes |

| Chapter 3 | Reconstitution of a Partnership Firm: Retirement / Death of a Partner Notes |

| Chapter 4 | Dissolution of Partnership Firm Notes |

| Part 2 Chapter 2 | Issue and Redemption of Debentures Notes |

| Part 2 Chapter 3 | Financial Statements of a Company Notes |

| Part 2 Chapter 4 | Analysis of Financial Statements Notes |

| Part 2 Chapter 5 | Accounting Ratios Notes |

| Part 2 Chapter 6 | Cash Flow Statement Notes |

FAQs on Accounting for Share Capital Class 12 Notes

Ques. What is the difference between Reserve Capital and Capital Reserve in Class 12 Accountancy?

Ans.

Reserve Capital is the portion of uncalled subscribed capital that a company resolves, by special resolution under the Companies Act, 2013, to call only at the time of winding up. It is a part of share capital. Capital Reserve, on the other hand, is the residual profit transferred from Share Forfeiture A/c after re-issue of forfeited shares, and it is a reserve under Reserves and Surplus, not part of share capital. Reserve Capital is uncalled; Capital Reserve is fully realised.

Ques. How is the maximum amount of discount on re-issue of forfeited shares calculated?

Ans.

The maximum discount that can be allowed on re-issue of forfeited shares is the amount lying to the credit of Share Forfeiture A/c for those specific shares. If, for example, the original applicant paid Rs 4 per share on a Rs 10 share before forfeiture, then up to Rs 4 per share can be allowed as discount on re-issue. Any discount beyond the credit balance is not legally permitted under the Companies Act, 2013.

Ques. What is pro-rata allotment of shares and why is it used?

Ans.

Pro-rata allotment is used when a share issue is over-subscribed. Instead of refusing the excess applications outright, the company allots shares to every applicant in proportion to the shares applied for. The excess application money is then adjusted against the amount due on allotment, and any further excess against the calls. Pro-rata is the fairest method of handling over-subscription and is the most common CBSE Long Answer pattern in Part 2 Chapter 1.

Ques. Is Securities Premium Reserve part of Share Capital under Schedule III?

Ans.

No. Securities Premium Reserve is not part of Share Capital. It is disclosed under Reserves and Surplus on the Equity and Liabilities side of the Schedule III balance sheet. Section 52 of the Companies Act, 2013 restricts its use to five specific purposes, including bonus issue, writing off preliminary expenses, and providing for premium on redemption of preference shares.

Ques. What rate of interest is allowed on Calls in Advance and Calls in Arrears?

Ans.

Under Table F of Schedule I of the Companies Act, 2013, interest on Calls in Advance is paid at a rate not exceeding 12% per annum, and interest on Calls in Arrears is charged at a rate not exceeding 10% per annum. These default rates apply unless the company's Articles of Association specify a different rate. Both are common 3-mark numerical questions in CBSE Class 12 Accountancy.

Ques. Do these Class 12 Accountancy notes for Part 2 Chapter 1 cover the 2026-27 NCERT syllabus?

Ans.

Yes. The Collegedunia notes for Accounting for Share Capital are mapped section-by-section to the current 2026-27 NCERT Accountancy Part B Reprint and the Companies Act, 2013. Every journal entry, every Schedule III tag, and every section reference (Section 42, 52, 54, 62) is verified against the latest NCERT print and CBSE Class 12 Accountancy curriculum document.

Comments