Financial Management is one of the highest-weightage chapters in the Class 12 Business Studies paper. These NCERT Solutions answer every question on the three financial decisions, the wealth-maximisation objective and capital structure, solved step by step for the 2026-27 CBSE syllabus.

CBSE Weightage: 8 to 12 marks (Unit 3, Business Finance and Marketing)

Sections Covered: 5 Very Short Answer, 7 Short Answer (incl. case), 6 Long Answer NCERT exercise questions

These solutions suit both a first-time reader of the chapter and a board candidate revising in the last week. Each answer gives a clear definition, the ROI vs cost-of-debt rule, the NWC formula, and a one-line takeaway. Quick tips and common-mistake call-outs sit at the exact points where students slip.

Financial Management Class 12 NCERT Solutions: Topic Map

What the Class 12 Business Studies Chapter 9 NCERT Solutions PDF Contains

Question-wise step-by-step answers to all 18 NCERT exercise questions (5 Very Short Answer, 7 Short Answer including case, 6 Long Answer including the steel-industry composite case).

Concept Used block at the start of every long-answer solution naming the rule, definition or model being applied.

Boxed Final Answer at the end of every solution for last-minute revision.

Numerical solutions with line-by-line ROI computation (e.g. ROI = $\frac{8{,}00{,}000}{1{,}00{,}00{,}000} \times 100 = 8\%$ in the Sunrises case).

EPS comparison table showing trading on equity in action (Plan A all-equity vs Plan B 50:50 debt-equity).

Case-study mapping from spotter words to answer (e.g. "financial blueprint" $\Rightarrow$ financial planning; "fixed financial charges raise return to equity" $\Rightarrow$ trading on equity).

Cross-links to Notes, Handwritten Notes and the NCERT Book PDF for the same chapter.

Exam Anchor: In Chapter 9, the must-know rule is "trading on equity works only when ROI > cost of debt". The must-state formula is $\text{NWC} = \text{CA} - \text{CL}$. The must-list trio is the three financial decisions: Investment + Financing + Dividend.

Financial Management Class 12: Related Chapters to Continue Learning

All NCERT Solutions for Financial Management with Step-by-Step Working

Every NCERT textbook question for Class 12 Business Studies Chapter 9 Financial Management is listed below with its full Solution and Expert Solution hidden inside collapsible tabs. Click Check Solution to reveal the step-by-step working; click Expert Solution for the expanded explanation.

Very Short Answer Type Questions

Q 9.1

What is meant by capital structure?

Concept used.Capital structure is the mix of long-term sources of

finance used by a firm. On the basis of ownership, business funds are classified into two

categories – owners' funds (equity, retained earnings) and borrowed funds (debt,

debentures, long-term loans). Capital structure refers to the proportion between these

two – the debt-equity mix.

Definition. Capital structure is the relative proportion of owners' funds

(equity + retained earnings) and borrowed funds (debt + debentures) in the total

long-term capital of the firm.

Two extremes.

All equity, no debt. Low risk, but high cost of capital and missed

trading-on-equity benefit.

Very high debt. Cheap on average but raises financial risk – the firm

must service fixed interest payments out of variable EBIT.

Optimum capital structure. The debt-equity mix at which the firm's overall

cost of capital is minimum and the market value of the share is maximum. Finding it is

one of the central tasks of financial management.

Why it matters. Capital structure affects three things at once – the

firm's cost of capital, its financial risk and its earnings per share (EPS).

Capital structure is the mix of long-term sources of finance used by a

firm – specifically, the proportion between owners' funds (equity + retained earnings)

and borrowed funds (debt + debentures). The optimum capital structure minimises cost of

capital and maximises share price.

AS

Aarav Sharma

M.Com, Delhi University

Verified Expert

Quick reading. Capital structure \(=\) debt-equity mix.

Owners' funds \(+\) Borrowed funds \(=\) total long-term capital.

Capital structure \(=\) proportion between the two.

Capital structure \(=\) mix of equity and debt in long-term capital.

Q 9.2

State the two objectives of financial planning.

Concept used.Financial planning is essentially the preparation of a

financial blueprint of an organisation's future operations – estimating the funds

required, the timing, and the sources from which the funds will come. The NCERT explicitly lists

two twin objectives of financial planning.

Objective 1: To ensure availability of funds whenever they are required.

Estimate the quantum of funds needed – short-term (working capital) and

long-term (fixed capital).

Estimate the timing – when each instalment is needed.

Specify the sources – equity, debentures, banks, retained earnings.

Net effect: no production halt for lack of funds, no missed growth opportunity.

Objective 2: To see that the firm does not raise resources unnecessarily.

Surplus funds are an idle cost (interest on debt, dividend on equity, lost

opportunity).

Excess equity dilutes EPS.

Excess debt raises financial risk.

Financial planning aligns the cash-in with the cash-out so that just-enough

funds, of the right type, are raised at the right time.

The two objectives of financial planning are: (i) to ensure availability of

funds whenever they are required (right quantum, right timing, right source) and (ii)

to see that the firm does not raise resources unnecessarily (avoid idle surplus

funds, avoid dilution and unnecessary financial risk).

PI

Priya Iyer

M.Com, Christ University Bangalore

Verified Expert

Quick reading. Two objectives, exact NCERT wording.

Availability of funds when required.

No unnecessary funds raised.

(i) Availability of funds when required; (ii) No unnecessary fund-raising.

Q 9.3

Name the concept of financial management which increases the return to equity

shareholders due to the presence of fixed financial charges.

Concept used. The concept described is Trading on Equity. When a firm

finances part of its needs through fixed-charge sources (debt, preference shares) and earns a

return on investment (ROI) higher than the cost of those fixed-charge funds, the

surplus benefit accrues entirely to the equity shareholders – raising their earnings per

share (EPS).

Definition. Trading on equity means the increase in profit available to

equity shareholders due to the use of fixed-cost financing (debt or preference shares)

in the capital structure.

How it works. Debt has a fixed cost (interest). If the firm earns more on its

total investment than it pays on its debt, the excess belongs to the equity holders.

Example: Firm earns 15% ROI; pays 10% interest on debt. The 5% spread on the

debt portion goes to equity holders, boosting their EPS.

Condition. Trading on equity is beneficial only when ROI \(>\) cost of

debt. If ROI \(<\) cost of debt, the spread becomes negative and trading on equity

actually reduces EPS – this is the financial risk the firm assumes.

The concept is Trading on Equity. It is the rise in earnings per share for

equity holders when the firm uses fixed-cost finance (debt, preference shares) and earns an ROI

higher than the cost of that finance. The condition for it to be beneficial is

ROI \(>\) cost of debt; otherwise the firm bears a negative spread (financial risk).

VM

Vivaan Mehta

M.Com, Symbiosis Pune

Verified Expert

Quick reading. Use debt \(\to\) boost EPS, but only if ROI \(>\) cost of debt.

Amrit is running a `transport service' and earning good returns by providing this

service to industries. Giving reason, state whether the working capital requirement of the firm

will be `less' or `more'.

Concept used. The nature of business is the primary determinant of working

capital requirement. A trading or service concern (which buys and sells, or sells a

service, with no manufacturing) typically needs less working capital than a manufacturing

concern, because it does not hold large stocks of raw materials, work-in-progress and finished

goods.

Diagnose the business. Amrit runs a transport service – he provides

a service (movement of goods) to industries. There is no manufacturing, no raw

material, no work-in-progress and no finished-goods inventory.

Apply the principle.

Services typically need less working capital than manufacturing because

there is no production cycle to fund.

Cash collection in transport is often quick (industries pay against invoices

in 30-60 days; sometimes advance).

Operating expenses (fuel, driver salaries, maintenance) recur each month but

are predictable.

Conclusion. The working capital requirement of Amrit's transport firm will be

less compared with a manufacturing firm of similar scale.

The working capital requirement of Amrit's transport service firm will be

less, because a service business holds no raw material, no work-in-progress and no

finished-goods inventory; only operating expenses (fuel, salaries, maintenance) need to be

funded, and receivables turn over reasonably fast. Service firms have a shorter operating

cycle than manufacturing firms.

AK

Aanya Kapoor

M.Com, BHU Varanasi

Verified Expert

Quick reading. Service \(=\) no inventory \(=\) less working capital.

Transport is a service.

No raw materials, WIP, finished goods.

Less working capital.

Less working capital.

Q 9.5

Ramnath is into the business of assembling and selling of televisions. Recently he

has adopted a new policy of purchasing the components on three months credit and selling the

complete product in cash. Will it affect the requirement of working capital? Give reason in

support of your answer.

Concept used.Working capital requirement is determined by the

operating cycle: the time between paying for inputs (cash out) and collecting from

customers (cash in). Two key determinants here are credit availed (from suppliers) and

credit allowed (to customers). Both have changed in Ramnath's case.

Identify the two changes.

Credit availed from suppliers has increased from `cash purchase'

(presumably) to 3 months.

Credit allowed to customers has decreased from credit sales

(presumably) to cash sale.

Effect on working capital.

More supplier credit \(\Rightarrow\) Ramnath gets to use the supplier's money for

3 months, reducing his own funding need.

Cash sale to customers \(\Rightarrow\) no debtors; cash returns immediately.

Net effect: the operating cycle is shortened dramatically. Cash flowing in

arrives before cash flowing out is paid.

Conclusion. Working capital requirement will decrease. In fact, the

firm now operates almost on the suppliers' money, holding only inventory and minimal

operating cash.

Yes, the change affects working capital – it decreases the

requirement. Two reasons:

(i) buying on 3 months credit lets Ramnath use the supplier's money for that period,

postponing his cash outflow;

(ii) selling for cash means immediate cash inflow with no debtors. The operating cycle

shrinks, so much less working capital is needed.

KJ

Karan Joshi

M.Com, BHU Varanasi

Verified Expert

Quick reading. Pay later (suppliers) + collect now (customers) \(\Rightarrow\) shorter

cycle \(\Rightarrow\) less working capital.

Credit availed \(\uparrow\): less cash out today.

Credit allowed \(\downarrow\): cash in today.

Cycle shrinks; WC need falls.

Working capital requirement decreases.

Short Answer Type Questions

Q 9.6

What is financial risk? Why does it arise?

Concept used.Financial risk is one of the two main risks of a business – the

other being business risk (operating risk). Financial risk arises from the

financing decisions of the firm, specifically the use of debt in the capital

structure.

Definition. Financial risk is the risk that a firm may not be able to

meet its fixed financial obligations – interest on debt, repayment of principal, and

preference dividend.

Why it arises.

Debt carries a fixed cost (interest) which must be paid whether the firm

earns profits or not.

Operating profits (EBIT) are variable – they rise in good years and

fall in bad years.

When debt is high, even a small fall in EBIT can leave the firm short of cash

to pay interest – triggering default.

Total risk = business risk + financial risk. A firm with low business risk

(stable demand, low operating leverage) can take on more debt – and vice versa.

Utility companies typically use high debt; tech start-ups use low debt.

Managing financial risk. Maintain a balanced debt-equity ratio, build cash

reserves, ensure interest-coverage ratio (ICR) and debt-service coverage ratio (DSCR)

well above 1.

Financial risk is the risk that the firm may fail to meet its fixed

financial obligations – interest, principal repayment and preference dividend. It arises

because debt carries fixed charges, while operating profit (EBIT) is variable; in a bad year

the firm may not have enough EBIT to service its debt. The greater the proportion of debt in

the capital structure, the higher the financial risk.

Definition: risk of not meeting fixed financial obligations.

Cause: debt has fixed cost; EBIT is variable.

More debt \(\Rightarrow\) more financial risk.

Financial risk \(=\) risk of failing to meet fixed financial charges. Arises from use of

debt in the capital structure.

Q 9.7

Define current assets. Give four examples of such assets.

Concept used.Current assets are one of the two broad categories of assets

on the balance sheet (the other being fixed assets). They are at the heart of

working capital management.

Definition. Current assets are assets which, in the normal routine of the

business, get converted into cash or cash equivalents within one year (or one

operating cycle, whichever is longer). They are the firm's short-term, liquid

resources.

Key properties.

High liquidity – convertible to cash quickly.

Lower return than fixed assets – they earn little or no income on their

own.

Support operations – finance the day-to-day operating cycle.

Four examples (in order of liquidity).

Cash in hand / cash at bank – already in liquid form.

Bills receivable / debtors – amounts due from customers, payable

within a year.

Inventories – raw materials, work-in-progress, finished goods.

Prepaid expenses – expenses paid in advance (rent, insurance).

Current assets are assets that get converted into cash or cash equivalents

within one year (or one operating cycle) in the normal routine of the business. Four

examples: (1) cash in hand / cash at bank, (2) marketable securities, (3) bills receivable /

debtors, and (4) inventories of raw materials, work-in-progress and finished goods.

PI

Priya Iyer

M.Com, Christ University Bangalore

Verified Expert

Quick reading. Convertible to cash within 1 year. Four examples.

Cash and bank balances.

Marketable securities.

Debtors / bills receivable.

Inventories.

Current assets \(=\) assets convertible to cash within a year. Examples: cash,

marketable securities, debtors, inventories.

Q 9.8

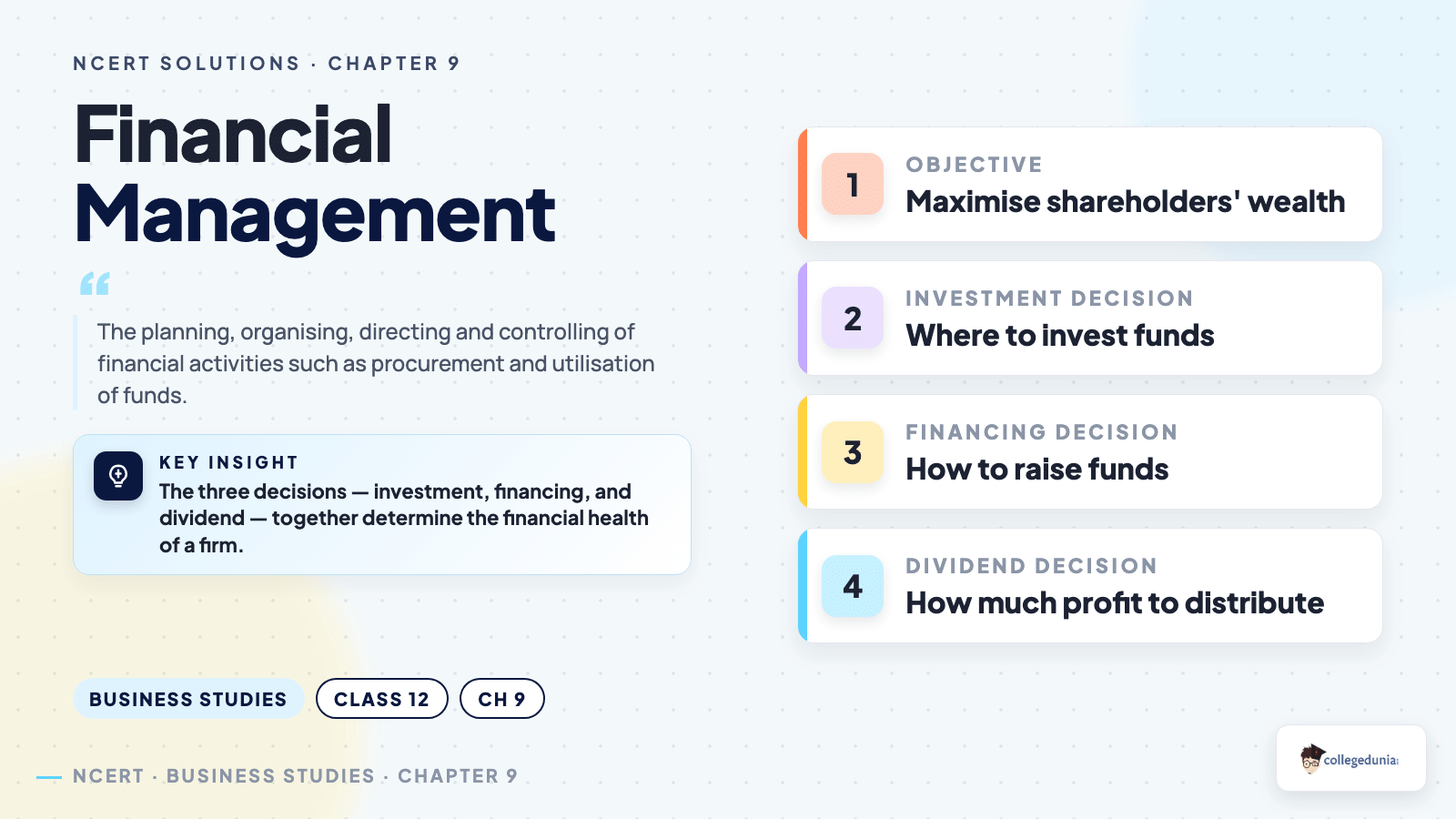

What are the main objectives of financial management? Briefly explain.

Concept used.Financial management is concerned with the optimal

procurement and usage of funds. Its primary objective is wealth maximisation of the

equity shareholders. The NCERT explains the link between wealth maximisation and the firm's

three financial decisions.

Primary objective – Wealth Maximisation.

Meaning. Maximise the market price of the firm's equity share, which

in turn maximises the wealth of equity shareholders.

Why not profit maximisation? Profit is short-term, ignores risk, ignores

the time value of money and is open to accounting manipulation. Share price

discounts future cash flows and reflects long-term value.

Achievement. A financial decision creates wealth only if its NPV

(present value of future cash inflows minus present value of outflows) is

positive at the firm's cost of capital.

Three derived objectives (the financial decisions).

Investment / capital budgeting decisions – choose projects with

positive NPV; allocate funds to fixed and current assets.

Financing decisions – decide the mix of equity and debt that

minimises the cost of capital.

Dividend decision – decide what part of profit to retain (for growth)

and what part to distribute (to shareholders), so as to maximise long-run

share price.

Operational objectives.

Ensure adequate funds at right time.

Ensure reasonable return to shareholders.

Ensure efficient use of funds (no idle funds, no waste).

Maintain liquidity to meet day-to-day obligations.

Manage risk (financial + business).

The primary objective of financial management is wealth maximisation

of the equity shareholders – maximising the market price of the equity share. It is preferred

over profit maximisation because it accounts for risk, time value of money and long-term cash

flows. This primary objective is operationalised through three financial decisions –

investment, financing and dividend – each of which must add to shareholder wealth.

VM

Vivaan Mehta

M.Com, Symbiosis Pune

Verified Expert

Quick reading. Wealth max \(>\) profit max. Operationalised via 3 financial decisions.

Primary: wealth maximisation (max market price of share).

Financial management is based on three broad financial decisions. What are these?

Concept used.Financial management revolves around three broad

financial decisions – each one a separate question the financial manager must

answer to maximise shareholder wealth.

Investment Decision (Capital Budgeting).

Question:Where should the firm invest its funds?

Scope: fixed-asset investment (plant, machinery, building, R&D) is

called capital budgeting; current-asset investment is called

working capital management.

Effect: determines retained earnings, future growth funding and the

signal sent to the stock market.

The three broad financial decisions are: (i) Investment Decision (capital

budgeting + working capital management – where to invest), (ii) Financing Decision

(equity vs debt mix – how to raise funds), and (iii) Dividend Decision (how much to

pay out vs retain). All three are interlinked and together aim at maximising shareholder

wealth.

AK

Aanya Kapoor

M.Com, BHU Varanasi

Verified Expert

Quick reading. Where to invest, how to fund, how much to distribute.

Investment \(=\) capital budgeting.

Financing \(=\) debt/equity mix.

Dividend \(=\) retain vs distribute.

Investment + Financing + Dividend.

Q 9.10

Sunrises Ltd. dealing in readymade garments, is planning to expand its business

operations in order to cater to international market. For this purpose the company needs

additional Rs. 80,00,000 for replacing machines with modern machinery of higher production

capacity. The company wishes to raise the required funds by issuing debentures. The debt can be

issued at an estimated cost of 10%. The EBIT for the previous year of the company was

Rs. 8,00,000 and total capital investment was Rs. 1,00,00,000. Suggest whether issue of

debenture would be considered a rational decision by the company. Give reason to justify your

answer. (Ans: No, Cost of Debt (10%) is more than ROI which is 8%).

Concept used. The decision turns on Return on Investment (ROI) versus the

cost of debt. Trading on equity is beneficial only when ROI \(>\) cost of debt. If ROI

\(<\) cost of debt, raising debt would actually destroy shareholder value.

Apply the rule. For debt to add value, ROI must exceed cost of debt.

Here ROI \(=\) 8% and cost of debt \(=\) 10%, so ROI \(<\) cost of debt.

Consequence of issuing debt.

Every Rs. 100 of debt earns only Rs. 8 of EBIT but costs Rs. 10 of interest.

Net effect \(=\) a loss of Rs. 2 per Rs. 100 of debt, paid out of the existing

equity holders' profits.

EPS of equity holders will fall, not rise.

Financial risk will also rise – the firm has taken on fixed interest

obligations.

Recommendation. The company should not raise the Rs. 80 lakh through

debentures.

Better alternatives: raise funds through equity (rights issue / fresh

equity), retained earnings (if available), or a smaller debt issue once

the new machines start improving ROI.

If debt must be used, negotiate a lower interest rate or wait until projected

ROI on the expansion exceeds 10%.

No, issuing debentures is not a rational decision. ROI is only

\(\frac{8{,}00{,}000}{1{,}00{,}00{,}000} \times 100 = 8\%\), which is less than the cost

of debt of 10%. Trading on equity will work against the firm – every rupee of debt loses 2

paise of shareholder wealth. The company should fund the expansion through equity or retained

earnings, or wait until projected ROI on the modern machines exceeds 10%.

KJ

Karan Joshi

M.Com, BHU Varanasi

Verified Expert

Quick reading. ROI \(=\) 8%; cost of debt \(=\) 10%. Debt destroys value.

ROI \(=\) EBIT/Capital \(\times\) 100 \(=\) 8%.

Cost of debt \(=\) 10%.

ROI \(<\) Cost of debt \(\Rightarrow\) negative spread \(\Rightarrow\) EPS falls.

Recommend equity / retained earnings instead.

No – ROI (8%) is less than cost of debt (10%); debt will hurt shareholder wealth.

Q 9.11

How does working capital affect both the liquidity as well as profitability of a

business?

Concept used.Working capital is the lifeblood of the business – it funds

the day-to-day operating cycle. Working capital affects two seemingly competing things:

liquidity (ability to pay short-term obligations) and profitability (return on

total investment). The trade-off between the two is one of the central tensions in financial

management.

Net Working Capital (NWC).

\[

\text{NWC} = \text{Current Assets} - \text{Current Liabilities}.

\]

Effect on Liquidity.

Higher working capital \(\Rightarrow\) more cash, more inventory, more

debtors \(\Rightarrow\) the firm can pay its bills, salaries and suppliers on

time. Higher liquidity.

Lower working capital \(\Rightarrow\) risk of running out of cash, missing

payments, losing supplier credit and customer trust. Lower liquidity.

Effect on Profitability.

Higher working capital (especially excess inventory and excess debtors)

\(\Rightarrow\) funds blocked in low-return current assets \(\Rightarrow\) the

same money would have earned more in fixed assets or paying down debt

\(\Rightarrow\) lower profitability.

Lower working capital \(\Rightarrow\) more money in productive

investments \(\Rightarrow\) higher return on investment.

The trade-off. Liquidity and profitability move in opposite directions with

working capital level.

Too much WC \(\Rightarrow\) high liquidity, low profitability.

Too little WC \(\Rightarrow\) high profitability on paper, but

risk of liquidity crisis that can stop production altogether.

The financial manager seeks the optimum WC level that keeps liquidity

just adequate and profitability as high as possible.

Working capital simultaneously affects liquidity and profitability

in opposite directions. Higher WC raises liquidity (more ability to pay short-term obligations)

but lowers profitability (funds blocked in low-return current assets). Lower WC raises

profitability (more funds in productive investments) but increases liquidity risk (cannot meet

bills). The financial manager seeks the optimum WC level that balances the two.

AS

Aarav Sharma

M.Com, Delhi University

Verified Expert

Quick reading. More WC \(\Rightarrow\) safer but less profitable; less WC \(\Rightarrow\)

profitable but risky.

NWC \(=\) CA \(-\) CL.

More WC \(\to\) liquidity \(\uparrow\), profitability \(\downarrow\).

Less WC \(\to\) liquidity \(\downarrow\), profitability \(\uparrow\).

Optimum \(=\) balance both.

Working capital is a liquidity-profitability trade-off; the optimum WC level keeps

liquidity adequate while maximising profitability.

Q 9.12

Aval Ltd. is engaged in the business of export of canvas goods and bags. In the

past, the performance of the company had been upto the expectations. In line with the latest

demand in the market, the company decided to venture into leather goods for which it required

specialised machinery. For this, the Finance Manager Prabhu prepared a financial blueprint of

the organisation's future operations to estimate the amount of funds required and the timings

to ensure that enough funds are available at right time. He also collected the relevant data

about the profit estimates in the coming years. By doing this, he wanted to be sure about the

availability of funds from the internal sources of the business. For the remaining funds, he

is trying to find out alternative sources from outside. (a) Identify the financial concept

discussed in the above paragraph. Also, state the objectives to be achieved by the use of

financial concept so identified. (Financial Planning) (b) `There is no restriction on payment

of dividend by a company'. Comment. (Legal & Contractual Constraints).

Concept used. The case-study has two parts. Part (a) asks the student to recognise

the description of financial planning and recall its objectives. Part (b) asks the

student to evaluate the statement that dividend payment is unrestricted – a statement which is

wrong, because of the legal and contractual constraints listed by NCERT.

Part (a) – Financial Planning identified.

Clue 1: ``Prabhu prepared a financial blueprint of the organisation's

future operations'' – the textbook definition of financial planning.

Clue 2: He estimated amount and timing of funds needed.

Clue 3: He looked at internal sources first, then external.

Concept identified: Financial Planning.

Objectives of Financial Planning.

(i) To ensure availability of funds whenever they are required. Right

amount, right timing, right source.

(ii) To see that the firm does not raise resources unnecessarily. No

idle surplus; no unnecessary financial cost.

Other points of importance. Tackles uncertainty about future operations;

helps in coordinating various business functions; reduces wastage; provides

links between investment and financing decisions; ensures smooth functioning;

aids in policy formulation.

Part (b) – ``No restriction on dividend payment'' is INCORRECT.

Dividend payment is restricted by both legal and contractual

constraints.

Legal constraints (Companies Act 2013).

itemize

Dividend can be paid only out of profits – current year's

profit (after depreciation), or accumulated past profits, or both.

Dividend cannot be paid out of capital – this would be a return of

capital, not income.

A specified percentage of profit must be transferred to reserves

before dividend.

Dividend must be declared at the AGM on the recommendation of the

Board; the AGM cannot increase the recommended rate.

Contractual constraints.

Long-term loan agreements (debentures, bank loans) often include

covenants that restrict dividend until the loan is partly or fully

repaid, or require the company to maintain a minimum

debt-service-coverage ratio before declaring dividend.

Such covenants protect lenders.

Conclusion: The statement is wrong; there are several legal and contractual

restrictions on dividend payment.

itemize

(a) The concept is Financial Planning – the preparation of a financial

blueprint of an organisation's future operations. Its two objectives are: (i) ensuring

availability of funds when required, and (ii) ensuring that the firm does not raise resources

unnecessarily. (b) The statement is incorrect. Dividend payment is restricted by

legal constraints under the Companies Act (paid only out of profits, mandatory transfer

to reserves, recommended by Board and declared at AGM) and by contractual constraints

(loan covenants in debenture and bank-loan agreements often restrict dividend until loan is

serviced).

(a) Financial Planning – two objectives = availability of funds and avoidance of

surplus. (b) Statement is wrong – dividend is restricted by legal and contractual constraints.

Long Answer Type Questions

Q 9.13

What is working capital? Discuss five important determinants of working capital

requirement.

Concept used.Working capital is the capital needed to finance the

day-to-day operations of the business – buying raw materials, paying wages, holding inventory,

extending credit to customers – until cash returns from sales.

Meaning. Working capital \(=\) the firm's investment in current assets.

Gross working capital \(=\) total current assets. Net working capital \(=\)

current assets minus current liabilities:

\[

\text{NWC} = \text{CA} - \text{CL}.

\]

Five important determinants of working capital requirement.

(i) Nature of business. Manufacturing firms need more WC (raw materials,

WIP, finished goods); trading and service firms need less.

(ii) Scale of operations. Larger scale \(\Rightarrow\) larger inventory

and debtors \(\Rightarrow\) larger WC.

(iii) Production cycle. Longer cycle (heavy engineering, ship-building)

\(\Rightarrow\) funds locked longer \(\Rightarrow\) more WC. Shorter cycle (FMCG)

\(\Rightarrow\) less WC.

(iv) Credit allowed and credit availed.

itemize

More credit allowed to customers \(\Rightarrow\) higher debtors

\(\Rightarrow\) more WC.

More credit availed from suppliers \(\Rightarrow\) lower payable

cash \(\Rightarrow\) less WC.

(v) Inflation. Rising prices push up the cost of inventory and wages,

so even constant volume needs more WC.

(Other determinants for context.) Operating efficiency, availability of

raw material, seasonal factors, business cycle (boom = more WC; depression =

less), growth prospects, level of competition.

itemize

Working capital is the capital required to finance day-to-day operations

(current assets); NWC \(=\) CA \(-\) CL. Five important determinants: (1) Nature of

business (manufacturing \(>\) service); (2) Scale of operations (large \(>\) small); (3) Production

cycle (longer \(\Rightarrow\) more WC); (4) Credit allowed vs credit availed (more allowed

\(\Rightarrow\) more WC; more availed \(\Rightarrow\) less WC); (5) Inflation (rising prices

\(\Rightarrow\) more WC).

VM

Vivaan Mehta

M.Com, Symbiosis Pune

Verified Expert

Quick reading. Day-to-day capital; five drivers.

Nature of business.

Scale.

Production cycle.

Credit (allowed \(-\) availed).

Inflation.

WC funds the operating cycle. Five determinants: nature, scale, cycle, credit terms,

inflation.

Q 9.14

``Capital structure decision is essentially optimisation of risk-return relationship.'' Comment.

Concept used.Capital structure is the debt-equity mix. The choice of mix

sets up a direct trade-off: debt is cheaper (interest is tax-deductible, lenders

expect a lower return) but riskier (fixed obligations must be paid even in bad years); equity

is costlier but safer. The capital structure decision is, in essence, choosing the point on

this trade-off that maximises shareholder wealth.

Return side of the trade-off.

Debt is cheaper. Interest is tax-deductible:

\[ \text{After-tax cost of debt} = \text{Interest rate} \times (1 - t). \]

For a firm taxed at 30% borrowing at 10%, the after-tax cost is only 7%.

Equity holders, who bear residual risk, expect a higher return than 7%.

Therefore, using more debt lowers the weighted average cost of capital

(WACC) and raises EPS – this is the trading on equity benefit.

Risk side of the trade-off.

Debt carries fixed obligations (interest, principal). Failure to pay can

trigger default and bankruptcy.

Beyond a point, additional debt sharply raises financial risk.

Equity holders, seeing the rising risk, demand a higher return \(\Rightarrow\)

cost of equity rises and share price may fall.

The optimisation problem.

As debt rises from zero, WACC falls (benefit dominates) and EPS rises.

At a certain point, the rising risk premium on equity equals the marginal

tax-saving of debt – WACC bottoms out.

Beyond that point, WACC rises again – additional debt destroys value.

The optimum capital structure is the debt-equity mix at the bottom of

this U-shaped WACC curve.

Factors a manager weighs in this trade-off.

Cash-flow position, interest-coverage ratio, debt-service coverage ratio, ROI vs cost

of debt, tax rate, floatation cost, risk consideration, flexibility, control

considerations, regulatory framework, stock-market conditions, industry capital

structure norms.

The statement is true. The capital structure decision is essentially a

risk-return optimisation. Debt is cheaper (tax-deductible interest) and raises EPS up

to a point (return side), but it also brings fixed financial obligations and raises financial

risk (risk side). The financial manager balances the two by choosing the debt-equity mix at

which the weighted average cost of capital is minimum and the market price of the equity share

is maximum – the optimum capital structure.

True – capital structure choice = risk-return optimisation; optimum mix minimises

WACC and maximises share price.

Q 9.15

``A capital budgeting decision is capable of changing the financial fortunes of a

business.'' Do you agree? Give reasons for your answer.

Concept used.Capital budgeting decisions are decisions on long-term

investment in fixed assets – buying plant, building a factory, launching a new product line,

acquiring a competitor. They commit large funds for long periods and are generally irreversible.

Their impact on the firm's future is therefore unique.

Yes, capital budgeting decisions can change the financial fortunes – four

reasons.

(i) Long-term growth. Capital budgeting decisions determine the firm's

future earning power. A wise investment (modern plant, R&D, new product

line) drives years of growth; a poor one drags earnings down for years.

(ii) Large amount of funds involved. These decisions lock up a

substantial portion of the firm's capital. A single project may absorb crores;

if it fails, the firm may be crippled.

(iii) Risk involved. Capital budgeting commits funds whose returns

stretch into an uncertain future. The risk is high; estimates of future cash

flows are exposed to changes in technology, demand and policy.

(iv) Irreversible decisions. Once a plant is built or a competitor is

acquired, reversing the decision is very costly – selling at a loss, writing

off goodwill, retrenching staff. Most capital budgeting decisions cannot be

undone without heavy loss.

Implication. Because of these four characteristics, capital budgeting

decisions are taken only after careful analysis – NPV, IRR, payback period,

sensitivity analysis, scenario analysis, real-option valuation – and only after the

board and shareholders have considered the long-term strategic fit.

Real-world illustration. Reliance's investment in 4G telecom infrastructure

( Rs. 1.5 lakh crore through Reliance Jio) was a capital budgeting decision that

re-shaped the firm and the entire Indian telecom industry – a textbook example of how

a single capital budgeting decision can change the financial fortunes of a business.

Yes, capital budgeting decisions can change the financial fortunes of a

business. Four reasons: (1) Long-term growth – they determine future earning power;

(2) Large funds involved – they lock up a major share of the firm's capital;

(3) High risk – returns stretch into an uncertain future; (4) Irreversibility

– reversal is very costly. Because of these four characteristics, capital budgeting decisions

are taken only after rigorous NPV/IRR analysis and board scrutiny.

KJ

Karan Joshi

M.Com, BHU Varanasi

Verified Expert

Quick reading. Yes – four reasons: growth, funds, risk, irreversibility.

Long-term growth.

Large funds.

Large risk.

Irreversible.

Yes – capital budgeting decisions reshape financial fortunes because they are big,

long-term, risky and irreversible.

Q 9.16

Explain the factors affecting dividend decision.

Concept used. The dividend decision is the third financial decision – how

much of the profit to distribute as dividend and how much to retain. The decision balances

shareholder expectation (dividend in hand) against growth funding (retained

earnings).

1. Earnings. Dividend is paid out of profits. Higher and more stable

earnings allow higher dividend.

2. Stability of earnings. Companies with stable earnings (utilities,

FMCG) can declare higher and more stable dividends; cyclical companies (steel, auto)

keep dividend conservative.

3. Stability of dividend. Most firms aim to maintain a stable dividend over

time; abrupt cuts send a negative signal. Hence the dividend payout is conservative

even in a good year so it can be sustained in a bad year.

4. Growth opportunities. If the firm has many positive-NPV projects, it

retains more (lower payout); if growth opportunities are few, it can pay out more.

5. Cash-flow position. Profit is an accounting concept; dividend is paid in

cash. Even a profitable firm may declare a low dividend if cash is locked up in

receivables or inventory.

6. Shareholder preference. Some shareholders (retired investors, pension

funds) prefer steady dividend; growth investors prefer retention. The firm reads its

shareholder base.

7. Taxation policy. Tax treatment of dividend vs capital gains influences

payout. (In India, dividend is taxable in the hands of the recipient; capital gains

face long-term/short-term distinction.)

8. Stock market reaction. Investors generally view a dividend rise as

positive and a dividend cut as negative – the so-called signalling effect.

Managers manage payout with the share-price reaction in mind.

9. Access to capital markets. Firms with easy access to capital markets (big,

well-known firms) can afford a higher payout because they can replenish funds by

issuing fresh securities. Smaller firms retain more.

10. Legal constraints. The Companies Act restricts dividends to be paid

only out of current or accumulated profits; a percentage must be transferred to

reserves; dividend cannot be paid out of capital.

11. Contractual constraints. Long-term loan agreements may restrict

dividends until the loan is serviced or until a minimum coverage ratio is

maintained.

Factors affecting the dividend decision include: (1) earnings level, (2) stability

of earnings, (3) stability of dividend (signalling), (4) growth opportunities (retain for

positive-NPV projects), (5) cash-flow position, (6) shareholder preference, (7) taxation

policy, (8) stock market reaction, (9) access to capital markets, (10) legal constraints

(Companies Act), and (11) contractual constraints (loan covenants). The firm balances payout

against retention to maximise long-run share price.

Explain the term `Trading on Equity'. Why, when and how it can be used by company?

Concept used.Trading on Equity is the practice of using fixed-cost

finance (debt and preference shares) in the capital structure to enhance the return to equity

shareholders. It is one of the most-tested concepts in the chapter because it operationalises

the entire risk-return trade-off of capital structure.

Meaning. Trading on equity is the use of borrowed funds (or preference share

funds) in the expectation of earning a return greater than the cost of those funds, so

that the excess accrues to the equity shareholders and their EPS rises.

Why use it – the benefit.

Debt carries a fixed interest cost which is tax-deductible. Effective cost is

even lower than the stated rate:

\[ \text{After-tax cost of debt} = i \times (1 - t). \]

If the firm earns ROI \(>\) after-tax cost of debt, the surplus enriches equity

holders – EPS rises sharply.

Used in moderation, trading on equity lowers the weighted average cost of

capital and raises share price.

When to use it – the condition.

Condition 1: ROI \(>\) cost of debt. Without this, debt destroys value.

Condition 2: Stable EBIT. Firms with stable, predictable operating

earnings (utilities, FMCG) can take more debt; firms with volatile EBIT (auto,

steel) cannot.

Condition 3: Low business risk. The total risk (business \(+\) financial)

should remain manageable.

Condition 4: Interest-coverage ratio (ICR) and debt-service coverage

ratio (DSCR) should comfortably exceed 1.

How to use it – the mechanics.

Step 1. Raise long-term funds through debentures, term loans or

preference shares – all carry fixed cost.

Step 2. Invest in projects whose ROI is comfortably above the cost of

debt.

Step 3. Pay fixed interest / preference dividend from EBIT.

Step 4. The surplus (EBIT minus interest minus tax) belongs to equity

holders, lifting EPS.

Numerical illustration. Suppose total capital is Rs. 1 crore. Compare two

capital structures:

Plan A: 100% equity (1,00,000 shares of Rs. 100).

EBIT \(=\) Rs. 20 lakh, tax 30% \(\Rightarrow\) PAT \(=\) Rs. 14 lakh; EPS \(=\)

Rs. 14.

Same EBIT, different capital structure \(\Rightarrow\) EPS rises from Rs. 14 to

Rs. 21 – a 50% rise. This is trading on equity.

Caution. If EBIT falls – say to Rs. 5 lakh – the same plan B becomes

painful: Interest Rs. 5 lakh swallows entire EBIT, tax-saving disappears, PAT is

zero, EPS is zero. With Plan A (no debt), Plan A would still have EPS of Rs. 3.5.

This is the financial risk of trading on equity.

Trading on equity is the use of fixed-cost finance (debt and preference

shares) to enhance the return to equity shareholders. Why: the spread between ROI and

the after-tax cost of debt accrues entirely to equity holders, lifting EPS. When: only

when ROI \(>\) cost of debt, EBIT is stable, business risk is low, and ICR / DSCR are

comfortably above 1. How: raise long-term debt or preference shares, invest in

positive-spread projects, pay fixed charges out of EBIT, and let the surplus enrich equity

EPS. Used in moderation it lowers WACC; used excessively it raises financial risk and can

destroy value.

PI

Priya Iyer

M.Com, Christ University Bangalore

Verified Expert

Quick reading. Use debt to boost EPS – works only if ROI \(>\) cost of debt.

Why: spread \(=\) ROI \(-\) after-tax cost of debt goes to equity holders.

When: ROI \(>\) cost of debt + stable EBIT + low business risk.

How: raise debt, invest in positive-spread projects, pay fixed charges.

Trading on equity = use debt to lift EPS; safe only when ROI \(>\) cost of debt and

EBIT is stable.

Q 9.18

`S' Limited is manufacturing steel at its plant in India. It is enjoying a buoyant

demand for its products as economic growth is about 7-8 per cent and the demand for steel is

growing. It is planning to set up a new steel plant to cash on the increased demand. It is

estimated that it will require about Rs. 5000 crores to set up and about Rs. 500 crores of

working capital to start the new plant. (a) Describe the role and objectives of financial

management for this company. (b) Explain the importance of having a financial plan for this

company. Give an imaginary plan to support your answer. (c) What are the factors which will

affect the capital structure of this company? (d) Keeping in mind that it is a highly

capital-intensive sector, what factors will affect the fixed and working capital? Give reasons

in support of your answer.

Concept used. A textbook composite case-study. Four sub-parts that knit together the

whole chapter: role/objectives of FM, financial planning, capital structure factors, and

fixed/working capital factors. Steel is heavily capital-intensive with a long

production cycle and stable demand – these properties drive each answer.

Part (a) – Role and objectives of financial management for `S' Ltd.

Role: take the three financial decisions – (i) Investment / capital

budgeting (whether and how to invest Rs. 5000 crore in the new plant);

(ii) Financing (raise the funds through equity, debt or a mix);

(iii) Dividend (how much of future profit to retain to keep funding the

expansion).

Primary objective:wealth maximisation of the equity

shareholders – maximise the market price of `S' Ltd. share.

Operational objectives: ensure availability of Rs. 5500 crore at the

right time; ensure no surplus idle funds; ensure reasonable return to

shareholders; maintain liquidity; manage financial and business risk.

Part (b) – Importance of financial planning for `S' Ltd.

Forecasts the funds required (Rs. 5000 crore fixed \(+\) Rs. 500 crore

working) and the timing of each tranche.

Avoids both shortage of funds (which would stall the project) and excess

(which would be idle cost).

Helps in coordinating purchase, construction, hiring and commissioning

schedules with funding tranches.

Provides links between investment and financing decisions.

Imaginary plan.

itemize

Year 0: Equity issue Rs. 2000 crore (rights / IPO).

Year 0–1: Long-term debt Rs. 2000 crore (debentures, term loans).

Year 1–2: Retained earnings + working-capital loan Rs. 500 crore.

Year 2–3: Additional equity Rs. 1000 crore if needed.

Year 3 onwards: Plant operational; dividend kept low till loans

repaid; surplus reinvested in capacity expansion.

itemize

Part (c) – Factors affecting capital structure of `S' Ltd.

Cash-flow position. Steel demand is buoyant and stable \(\to\) supports

more debt.

ICR / DSCR. Stable EBIT means coverage ratios will be comfortable \(\to\)

debt is feasible.

ROI vs cost of debt. Expected ROI on the new plant must exceed

after-tax cost of debt; if 7-8% growth holds, this is likely.

Tax rate. Higher corporate tax makes debt's tax-shield more valuable.

Cost of equity. Equity is costlier than debt.

Floatation cost. A Rs. 2000 crore equity issue carries large

merchant-banking and listing cost; a debt issue is cheaper to float.

Risk consideration. Steel is cyclical; too much debt is dangerous in a

down-cycle.

Flexibility. Some debt capacity must be kept in reserve for emergencies.

Control. Fresh equity dilutes promoters' control; debt does not.

Regulatory framework. SEBI guidelines for public issue; banking norms

for term loans.

Stock market conditions. A bullish market favours equity; a bearish one

favours debt.

Capital structure of peers. Tata Steel, JSW Steel, SAIL benchmark debt

ratios – `S' Ltd. uses these as a sanity check.

Part (d) – Factors affecting fixed and working capital in this

capital-intensive sector.

Fixed capital – factors.

itemize

Nature of business – steel is capital-intensive (blast

furnace, rolling mill, refractories) \(\Rightarrow\) huge fixed capital.

Scale of operations – a green-field plant means very high

fixed capital.

Choice of technique – automated, capital-intensive technology

\(\Rightarrow\) more fixed capital.

Technology upgradation – modern steel plants need

continuous-casting, blast-furnace upgrades.

Growth prospects – 7-8% growth supports building extra

capacity for the future.

Diversification, financing alternatives, level of

collaboration.

Working capital – factors.

Nature of business – manufacturing \(\Rightarrow\) raw material

(iron ore, coking coal), WIP (heavy and slow), finished goods

\(\Rightarrow\) large working capital. Trading concerns would

need less.

Scale of operations – the larger the plant, the larger the

inventory and debtor balances.

Production cycle – steel-making has a long cycle (weeks)

\(\Rightarrow\) more funds tied up.

Business cycle – the buoyant phase means high inventory and

more debtors \(\Rightarrow\) more working capital.

Seasonal factors – construction season pushes up demand,

raising WC need.

Credit allowed / availed – B2B credit terms in steel are 30-90

days both ways; net effect depends on the gap.

Availability of raw material – erratic iron-ore supply forces

higher stock levels.

Operating efficiency, growth prospects, level of competition,

inflation.

itemize

(a) FM's role for `S' Ltd. = take the three financial decisions (investment,

financing, dividend) with the primary objective of wealth maximisation. (b) Financial planning

ensures Rs. 5500 crore is available on schedule – imaginary plan: Rs. 2000cr equity +

Rs. 2000cr debt + Rs. 500cr WC loan + Rs. 1000cr later equity. (c) Capital-structure

factors: cash-flow, ICR/DSCR, ROI vs cost of debt, tax rate, floatation cost, risk, flexibility,

control, regulatory framework, market conditions, peer structure. (d) In this capital-intensive

sector, fixed capital is driven by nature of business, scale, capital-intensive technology,

technology upgradation and growth prospects; working capital is driven by nature of business

(manufacturing), scale, long production cycle, business cycle (buoyant), credit terms and raw

material availability.

VM

Vivaan Mehta

M.Com, Symbiosis Pune

Verified Expert

Quick reading. Four sub-parts cover the whole chapter.

(c) Capital structure factors: 12 NCERT factors applied to steel.

(d) Capital-intensive sector: nature, scale, tech, cycle all push WC and FC up.

Whole chapter answer in one case: role + plan + capital structure factors + fixed and

working capital factors applied to the steel industry.

Student Feedback

In a Collegedunia poll of 640 Class 12 Commerce students, 78% said the trading-on-equity numerical was the part of Financial Management they most feared before using these solutions. 3 in 4 said the boxed final answers and the ROI vs cost-of-debt rule made the capital-structure questions easier to attempt in the board exam.

Other Resources for Class 12 Business Studies Chapter 9 Financial Management

Financial Management Class 12 - Frequently Asked Questions

Financial Management Class 12 - Frequently Asked Questions

What is financial management in Class 12 Business Studies Chapter 9?

Financial management is concerned with the optimal procurement and usage of funds. Its primary objective is the wealth maximisation of the equity shareholders, operationalised through three financial decisions - investment (capital budgeting), financing (capital structure), and dividend decisions.

What are the three financial decisions?

The three financial decisions are: (1) Investment decision (where to deploy funds - capital budgeting for fixed assets plus working capital management for current assets), (2) Financing decision (how to raise funds - the debt-equity mix in the capital structure), and (3) Dividend decision (how much to pay out as dividend vs how much to retain for growth).

What is trading on equity?

Trading on equity is the use of fixed-cost finance (debt and preference shares) in the capital structure to enhance the return to equity shareholders. It works only when ROI > cost of debt; the surplus between the two accrues to equity holders and lifts EPS. If ROI is less than cost of debt, trading on equity destroys value.

What are the five main determinants of working capital?

The five main determinants are: (1) Nature of business (manufacturing needs more, service needs less), (2) Scale of operations, (3) Production cycle (longer cycle = more WC), (4) Credit allowed to customers vs credit availed from suppliers, and (5) Inflation (rising prices increase WC need).

Where can I download the Class 12 Business Studies Chapter 9 Financial Management NCERT Solutions PDF?

You can download the Collegedunia Class 12 Business Studies Chapter 9 Financial Management NCERT Solutions PDF free of cost from this page. The PDF is aligned to the NCERT Reprint 2026-27 syllabus and includes all 18 exercise questions, the EPS-comparison numerical, the deviation and NWC formulas, and the case-study spotters you need for the board exam.

Comments