Part 2 Chapter 6 Cash Flow Statement has 24 NCERT questions across Short Answer, Long Answer, and Numerical blocks, closing Part B of Class 12 Accountancy. These Cash Flow Statement NCERT Solutions solve every question using the CBSE-prescribed Indirect Method (AS-3).

CBSE Weightage: 6 to 8 marks, usually one 6-mark numerical plus a 1 to 2 mark theory or classification question

CUET (UG) Relevance: 3 to 5 questions, mostly on activity classification and AS-3 definitions

24 NCERT questions solved

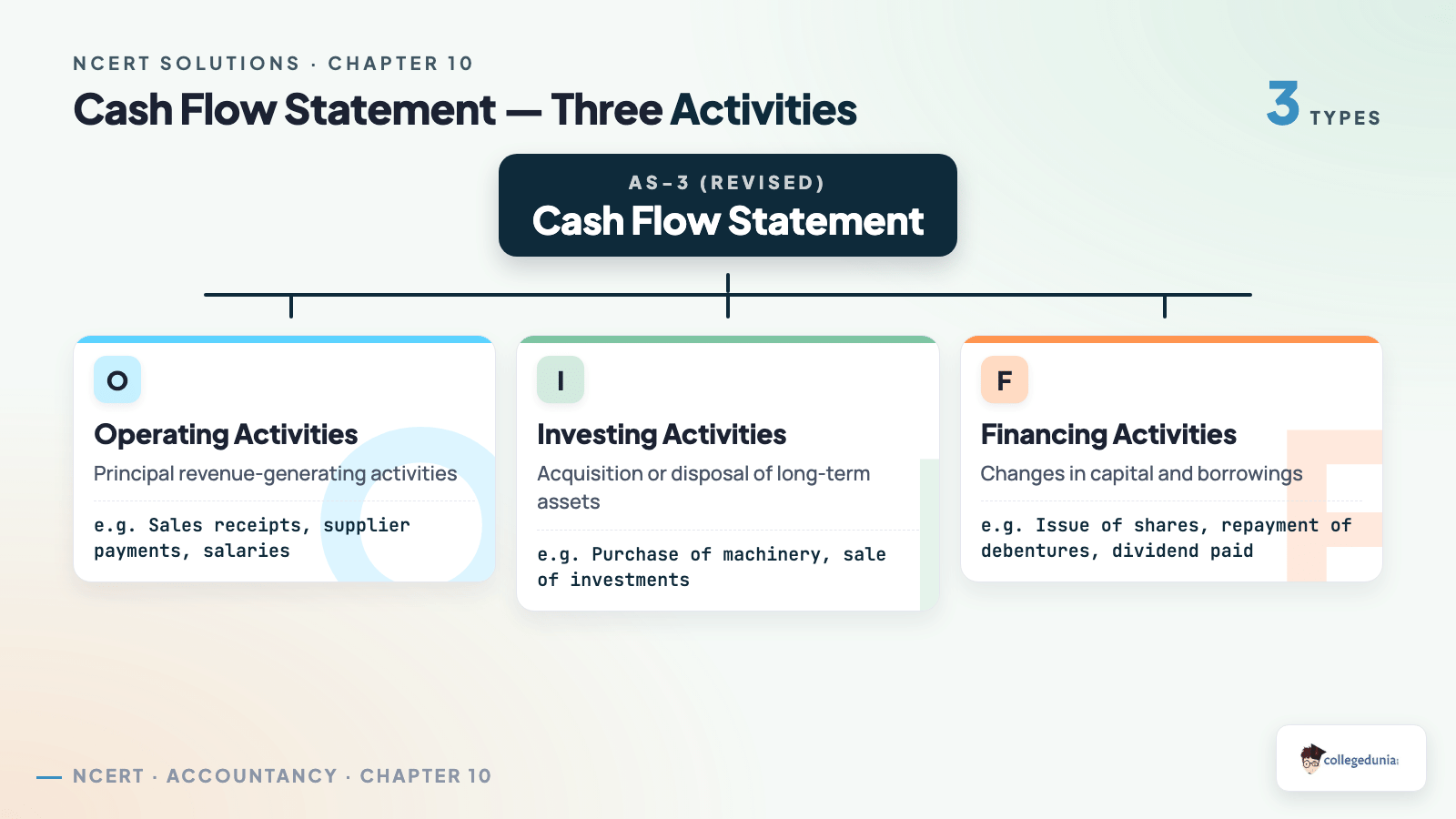

3 activities Operating, Investing, Financing

2026-27 NCERT print aligned

These NCERT Solutions are CA-reviewed, mapped to the 2026-27 print, and checked against five years of CBSE and CUET papers.

Why Cash Flow Statement Class 12 Is the Most Scoring Numerical of Part B

Cash Flow Statement is the highest-marks single question in Part B, with a full 6-mark numerical in every Class 12 Accountancy paper since 2014.

Quick Tip: Start the Indirect Method with Net Profit before Tax and Extraordinary Items, not Net Profit after Tax. Skipping this is the top reason a correct working still scores zero on Operating Activities.

Class 12 Accountancy Part 2 Chapter 6 Cash Flow Statement NCERT Solutions

How will Collegedunia's NCERT Solutions Help You with Cash Flow Statement?

These solutions follow the AS-3 (Revised) format CBSE evaluates against.

2026-27 NCERT Alignment: All 24 questions match the current print, with classification straight from AS-3 wording.

Indirect Method Step Order: Net Profit before Tax, then non-cash items, then working-capital changes.

Activity-Wise Working Notes: Operating, Investing, and Financing sub-totals are worked separately, so one mis-classified item does not cost every mark.

Cash Flow Statement Class 12 TS Grewal Solutions: Common Question Phrasings

CBSE reuses a tight set of phrasings that signal the answer type.

Question Stem

What It Wants

"From the following Balance Sheets of X Ltd., prepare a Cash Flow Statement."

Full statement under three activities using the Indirect Method

"Calculate Cash Flow from Operating Activities."

Start with Net Profit before Tax, add non-cash and non-operating items, adjust working-capital changes

"Classify the following transactions as Operating, Investing or Financing."

One-line classification per item; cite AS-3 for non-financial companies

"State whether Interest received by a Finance Company is Operating or Investing."

Operating, because for a financial enterprise interest income is the principal revenue activity

"Compute Cash Flow from Financing Activities given share issue and dividend paid."

Net of inflows (share issue, debentures) less outflows (redemption, dividend, interest on debentures)

These solutions use the same stems as the paper.

Cash Flow Statement Exercise-by-Exercise Breakdown (NCERT Class 12 Accountancy)

NCERT groups questions by type instead of numbering exercises. The table shows the split so you know which block to drill.

Question Block

Count

Sub-Topic

Short Answer Questions

3

Meaning, AS-3 classification, objectives

Long Answer Questions

8

Cash equivalents, Operating activities format, Indirect Method procedure, treatment of interest and dividend

Numerical Questions

13

Cash from Operating, classification of transactions, full Cash Flow Statement from Balance Sheets

Concept: AS-3 splits cash flows into three activities. Operating = revenue-producing activities. Investing = buying or selling long-term assets. Financing = changes in owners' capital and borrowings.

Sample Fully-Solved Question Walk-Through: Cash from Operating Activities (Indirect Method)

The Anand Ltd. numerical (NCERT Q14) is the template for most Operating Activities questions since 2018.

Particulars

Amount (Rs.)

Net Profit before Tax

5,00,000

Add: Depreciation

50,000

Add: Loss on Sale of Machinery

20,000

Less: Profit on Sale of Investments

(15,000)

Operating Profit before Working Capital Changes

5,55,000

Less: Increase in Trade Receivables

(40,000)

Add: Increase in Trade Payables

30,000

Cash Generated from Operations

5,45,000

Less: Income Tax Paid

(60,000)

Cash Flow from Operating Activities

4,85,000

The PDF shows this working for all 13 numerical questions.

Marks Budget for a 6-Mark Cash Flow Statement Question

CBSE splits a 6-mark Cash Flow Statement question into the same five blocks every year.

Step

Marks

What CBSE Looks For

1. Cash from Operating Activities (Indirect Method)

3

Net Profit before Tax, non-cash adjustments, working-capital changes, tax paid

2. Cash from Investing Activities

1

Sale/purchase of fixed assets, investments, interest received

3. Cash from Financing Activities

1

Share issue, debentures, dividend paid, interest on debentures

4. Net Change in Cash and Cash Equivalents

0.5

Sum of three activities tallied to opening/closing balance

5. Working Notes (Provision for Tax, Proposed Dividend, Fixed Assets account)

0.5

At least two Working Notes shown separately below the statement

Common Mistakes Students Make in Cash Flow Statement Numericals

Most marks lost here are presentation errors, not arithmetic.

Starting with Net Profit after Tax: Start with Profit before Tax; adjust tax at the end.

Treating Interest Paid as Operating: It is Financing for a non-financial company.

Dividend in the wrong activity: Dividend Paid is always Financing, including last year's Proposed Dividend.

Net change does not tally: a missed or double-counted Working Note is usually the cause.

Warning: Bank Overdraft is a Cash Equivalent in some textbooks but a Financing Activity under AS-3 for CBSE. Follow AS-3: it belongs under Financing Activities.

Cash Flow Statement Previous Year Questions Weightage (2026 to 2021)

This chapter has been an anchor numerical in every recent CBSE paper.

Year

Marks

Question Type

2026

6 + 1

Full Cash Flow Statement from two Balance Sheets and Notes; 1-mark classification

2025

6

Full Cash Flow Statement with Provision for Tax and Proposed Dividend Working Notes

2024

6 + 1

Indirect Method statement; classification of interest received by a finance company

2023

6

Cash from Operating Activities + Investing Activities only (4 + 2 marks)

2022

6

Full statement (special term-end paper, AS-3 classification list)

All NCERT Solutions for Cash Flow Statement with Step-by-Step Working

Every NCERT question for Cash Flow Statement is listed below with its Solution and Expert Solution inside collapsible tabs.

Short Answer Questions

Q 10.1

What is a Cash flow statement?

Concept used. A Cash Flow Statement is a financial

statement that reports the inflows (sources) and outflows (uses) of

cash and cash equivalents of an enterprise during a given

accounting period. As per Accounting Standard 3 (Revised)

issued by ICAI, the cash flows are classified into three activities:

Operating, Investing and Financing. The

statement explains the net change in the cash balance between the

opening and the closing Balance Sheet dates.

Cash means cash on hand and demand deposits with

banks.

Cash equivalents are short-term, highly liquid

investments that are readily convertible into known amounts

of cash and are subject to an insignificant risk of change in

value (for example, treasury bills with a maturity of three

months or less).

The statement starts with the opening cash balance, adds (or

deducts) the net cash flows from the three activities, and

arrives at the closing cash balance shown in the latest

Balance Sheet.

In one line

The Cash Flow Statement answers: ``Where did the cash come from and

where did it go during the year?''

A Cash Flow Statement is a statement prepared as per AS-3

(Revised) showing inflows and outflows of cash and cash equivalents

during an accounting period, classified into Operating, Investing

and Financing activities.

AS

Aarav Sharma

M.Com, Shri Ram College of Commerce

Verified Expert

Strategic angle. Think of the three financial statements as

three different cameras pointed at the same business. The Balance

Sheet shows what the firm owns and owes on a single date. The

Statement of Profit and Loss shows revenues earned and expenses

incurred over a period (on the accrual basis). The Cash Flow

Statement adds the third lens: actual cash movement during the same

period.

Why a third statement is needed. Profit and cash are

not the same. A company can report a healthy profit on the

accrual basis (credit sales recorded as revenue) yet face a

cash crunch because the receivables have not been collected.

The Cash Flow Statement separates earned profit from

collected cash.

What it captures. It captures every cash and

cash-equivalent movement: cash received from customers, cash

paid to suppliers, cash spent on machinery, cash raised from

a share issue, cash paid as dividend.

The three buckets. AS-3 (Revised) groups every

movement under exactly one of three activities: Operating

(day-to-day revenue generation), Investing (long-term asset

and investment transactions), Financing (owners' funds and

borrowings).

The bottom line. Net cash flow from the three

activities plus the opening cash balance reconciles to the

closing cash balance shown in the Balance Sheet. This

reconciliation is the proof that the statement is complete.

Why this matters. Lenders use cash flow statements to judge

whether a borrower will have the cash to service interest. Analysts

use them to spot ``profit without cash'' situations that often

precede a corporate distress event.

Common mistakes. Three predictable slips lose marks: (a) treating interest paid on borrowings by a non-finance company as an operating outflow when AS 3 classifies it as a financing outflow; (b) showing the proceeds from issue of shares net of share premium rather than the gross amount under financing activities; (c) omitting the non-cash items such as depreciation, goodwill written off and loss on sale of fixed asset when adjusting Net Profit Before Tax under the indirect method.

A Cash Flow Statement is the AS-3 (Revised) statement

showing how cash and cash equivalents moved through the enterprise

during the year, classified into Operating, Investing and Financing

activities.

Q 10.2

How are the various activities classified (as per AS-3

revised) while preparing cash flow statement?

Concept used. AS-3 (Revised) classifies every cash flow into

exactly one of three activities. The classification depends on the

nature of the transaction, not on the form of the asset or

liability involved.

Operating Activities. These are the principal

revenue-producing activities of the enterprise plus other

activities that are not investing or financing. Examples:

cash received from customers, cash paid to suppliers and

employees, cash payment of income tax (unless specifically

identifiable with investing or financing).

Investing Activities. These are the acquisition and

disposal of long-term assets and other investments that are

not cash equivalents. Examples: cash paid to buy machinery,

cash received from the sale of an old plant, cash paid to

buy shares of another company, dividend or interest received

on those investments (in case of a non-financial enterprise).

Financing Activities. These are activities that

result in changes in the size and composition of the owners'

capital and the borrowings of the enterprise. Examples: cash

received from issue of shares or debentures, cash paid to

redeem debentures or repay a bank loan, dividend paid to

shareholders, interest paid on borrowings.

Test for each item

Ask: does this affect (a) day-to-day operations, (b) long-term

assets and other investments, or (c) the way the business is

financed? The answer points to one of the three activities.

Three activities under AS-3 (Revised): Operating

Activities (principal revenue-producing), Investing Activities

(long-term assets and investments), and Financing Activities

(owners' funds and borrowings).

VI

Vivaan Iyer

M.Com, Christ University Bangalore

Verified Expert

Structural observation. The three buckets are mutually

exclusive and collectively exhaustive: every single cash transaction

of the enterprise must fit into exactly one of them. AS-3 takes a

strict line on this to make cash flow statements comparable across

firms.

Operating = what the business does for a living.

For a manufacturing firm, this is producing and selling

goods. For a hotel, it is renting rooms. For a software

company, it is licensing software. Cash flows tied to those

revenue-generating activities are operating.

Investing = how the business grows its

capacity. Buying machinery, buying patents, buying shares

of other companies as a long-term holding, building a

factory: all investing. Selling any of those same items:

also investing (cash inflow this time).

Financing = how the business is funded. Issuing

new shares, raising a debenture loan, taking a long-term

bank loan: financing inflows. Buying back shares, redeeming

debentures, repaying loans, paying dividends, paying

interest on borrowings: financing outflows.

Comparability follows from consistency. Because

every firm uses the same three buckets in the same order,

analysts can compare ``Cash from Operations'' across

companies as a clean measure of operating health.

Why this matters. A negative Cash from Operations is a

warning signal in almost any non-financial firm. A negative Cash

from Investing in a growing firm is usually a healthy sign (the

firm is buying assets). A positive Cash from Financing means the

firm is raising more money than it is returning.

Common mistakes. Three predictable slips lose marks: (a) treating interest paid on borrowings by a non-finance company as an operating outflow when AS 3 classifies it as a financing outflow; (b) showing the proceeds from issue of shares net of share premium rather than the gross amount under financing activities; (c) omitting the non-cash items such as depreciation, goodwill written off and loss on sale of fixed asset when adjusting Net Profit Before Tax under the indirect method.

Operating, Investing and Financing = the three buckets

under AS-3 (Revised), distinguished by whether the cash flow

relates to running the business, growing the business, or funding

the business.

Q 10.3

State the objectives of cash flow statement.

Concept used. The Cash Flow Statement supplements the

Balance Sheet and Statement of Profit and Loss with information that

neither of them shows directly: the actual cash inflow and outflow

over the year. Its objectives flow from this distinct role.

To assess the ability to generate cash. The

statement tells stakeholders how much cash the firm generated from

its principal operations, helping judge whether the firm can

fund its own activities without external help.

To explain the change in cash balance. The opening

and closing cash balances appear in the two Balance Sheets.

The Cash Flow Statement explains exactly where that

difference came from: how much from operations, how much

from investing, how much from financing.

To assess liquidity and solvency. A firm may report

a large profit but have very little cash. The cash flow

statement reveals that ``profit≠cash'' gap, helping

stakeholders assess short-term liquidity.

To help in planning and control. The statement is a

basis for preparing the next year's cash budget. Trends in

operating cash flows guide working-capital decisions.

To compare across firms and across time. Because the

AS-3 format is uniform, two firms can be compared on Cash

from Operations as cleanly as on profit, and one firm's CFO

across years shows the trend in operating health.

Objectives: assess ability to generate cash, explain

change in cash balance, assess liquidity and solvency, aid planning

and control, and enable inter-firm and trend comparison.

AP

Arjun Patel

M.Com, Symbiosis Pune

Verified Expert

Strategic angle. The objectives of any financial statement

follow from who reads it and why. List the user groups, list

their decisions, and the objectives follow.

Management reads the Cash Flow Statement to plan

working capital, budget capital expenditure, and decide

dividend policy. Objective → planning and control.

Lenders and bankers want to know whether the firm

will generate enough cash to repay loans and pay interest.

Objective → assess debt-servicing ability and solvency.

Investors compare ``earnings'' with ``cash from

operations'' to test the quality of reported profit.

Objective → assess earnings quality and liquidity.

Suppliers and short-term creditors want to know

whether the firm will pay its bills on time. Objective →

assess short-term liquidity.

Regulators and tax authorities want a reconciliation

between opening and closing cash. Objective → explain

change in cash balance.

Why this matters. Each objective listed above is invoked

by a specific user. The cash flow statement is the most

multi-purpose of the three statements precisely because it speaks

the simplest language: cash in, cash out.

Common mistakes. Three predictable slips lose marks: (a) treating interest paid on borrowings by a non-finance company as an operating outflow when AS 3 classifies it as a financing outflow; (b) showing the proceeds from issue of shares net of share premium rather than the gross amount under financing activities; (c) omitting the non-cash items such as depreciation, goodwill written off and loss on sale of fixed asset when adjusting Net Profit Before Tax under the indirect method.

The cash flow statement exists to assess cash generation,

explain the change in cash balance, judge liquidity, support

planning and control, and make firms comparable on a cash basis.

Q 10.4

What are the objectives of preparing cash flow statement?

Concept used. Question 3 already covered the broad

objectives. This phrasing emphasises the preparer's side

(i.e., why the management/accountant prepares the statement).

The core objectives are unchanged; here we frame them as goals

that the preparation process is designed to achieve.

To provide cash-based information. Profit and Loss

Account is on the accrual basis. The Cash Flow Statement

adjusts the same data to a cash basis so stakeholders see what

actually entered and left the cash book.

To identify the sources and uses of cash. The

statement classifies every cash movement under Operating,

Investing or Financing, so a user can see which activities

generated cash and which absorbed it.

To assess the company's cash-generation capacity.

By isolating Cash from Operations, the statement tells the

reader whether the firm's core business throws off enough

cash to fund its growth and pay its dividends.

To reconcile profit with cash. The opening section

starts with Net Profit before Tax and walks step by step to

Cash from Operations, making explicit every adjustment

(depreciation, working-capital changes, non-operating

items).

To facilitate decision-making. By showing how the

firm has actually used its cash, the statement supports

decisions about dividend declaration, capital expenditure

approval, loan applications, and credit policy.

Objectives of preparation: convert accrual data to a cash

basis, identify sources and uses of cash, assess cash-generation

capacity, reconcile profit with cash, and aid decision-making.

PM

Pranav Mehta

M.Com, Hindu College Delhi

Verified Expert

Quick reading. This question is almost a paraphrase of the

previous one. In the exam, the safe move is to repeat the five

points but reframe each one so the answer does not look identical

to Q3.

Cash-basis information. Re-state P&L items on a

cash basis.

Classification. Sort cash flows into three buckets.

Operating cash-generation. Highlight Cash from

Operations as the prime measure of internal cash strength.

Reconciliation. Bridge from Net Profit before Tax

to net cash from operations.

Decision support. Provide a basis for management,

investors, lenders and tax authorities.

Why this matters. The exam often pairs Q3 and Q4 to test

whether the student can keep the answer crisp. Treat them as a

matched pair and answer slightly differently to score full marks on

both.

Common mistakes. Three predictable slips lose marks: (a) treating interest paid on borrowings by a non-finance company as an operating outflow when AS 3 classifies it as a financing outflow; (b) showing the proceeds from issue of shares net of share premium rather than the gross amount under financing activities; (c) omitting the non-cash items such as depreciation, goodwill written off and loss on sale of fixed asset when adjusting Net Profit Before Tax under the indirect method.

Same five objectives as Q3, framed from the preparer's

side: cash-basis data, classification, operating cash measurement,

reconciliation, and decision support.

Q 10.5

State the meaning of the terms: (i) Cash Equivalents,

(ii) Cash flows.

Concept used. AS-3 (Revised) defines both terms precisely

because the rest of the standard is built on them.

(i) Cash Equivalents. These are short-term, highly

liquid investments that are

readily convertible into known amounts of cash, and

subject to an insignificant risk of change in value.

As a rule of thumb, an investment qualifies as a cash

equivalent only when it has a short maturity, say, three

months or less from the date of acquisition. Examples:

treasury bills with maturity less than three months,

commercial paper with maturity less than three months, money

market funds. Equity shares are not cash

equivalents because their market value can change

significantly.

(ii) Cash flows. These are the inflows and

outflows of cash and cash equivalents during an

accounting period. An inflow increases the cash balance

(cash sales, sale of fixed assets, fresh issue of shares);

an outflow decreases it (purchase of inventory, purchase of

machinery, redemption of debentures).

Quick rule

Movement between two items that are both cash or both

cash equivalents (e.g. moving Rs. 50,000 from the current account

to a 60-day treasury bill) is not a cash flow.

Cash Equivalents = short-term, highly liquid investments

(≤ 3 months) with insignificant risk; Cash flows = inflows and

outflows of cash and cash equivalents during a period.

KG

Karan Gupta

M.Com, Loyola College Chennai

Verified Expert

Strategic angle. Definitions are most clearly written by

stating (a) the test, (b) the conditions, and (c) two contrasting

examples (one that qualifies, one that does not).

Cash Equivalents, the test. An item is a cash

equivalent if it is held to meet short-term cash commitments

rather than for investment or other purposes.

Conditions. Short maturity (three months or less)

and negligible risk of value change.

Qualifies: 91-day treasury bill. Does not

qualify: an equity share, even of a blue-chip firm,

because its price is not stable.

Cash Flows, the test. A transaction is a cash

flow if it changes the combined balance of cash plus cash

equivalents.

Qualifies: cash sale of Rs. 1,00,000 (inflow);

purchase of machinery for cash (outflow). Does not

qualify: transferring Rs. 50,000 from a current account

into a 60-day treasury bill (cash to cash equivalent, net

change zero).

Why this matters. In a Class 12 numerical question on Cash Flow Statement, the examiner gives full marks only when the candidate classifies every change correctly as Operating, Investing or Financing as per AS 3 (Revised) and Indian Accounting Standard 7, starts the Operating section with Net Profit Before Tax and Extraordinary Items, and presents the closing cash and cash equivalents reconciled to the Balance Sheet. A correct closing cash figure without the three-way classification and the reconciliation loses 30-50 percent of the marks under the CBSE step-marking scheme.

Common mistakes. Three predictable slips lose marks: (a) treating interest paid on borrowings by a non-finance company as an operating outflow when AS 3 classifies it as a financing outflow; (b) showing the proceeds from issue of shares net of share premium rather than the gross amount under financing activities; (c) omitting the non-cash items such as depreciation, goodwill written off and loss on sale of fixed asset when adjusting Net Profit Before Tax under the indirect method.

Cash Equivalents = short-term, highly liquid, low-risk

investments; Cash flows = changes in the combined balance of cash

and cash equivalents.

Q 10.6

Prepare a format of cash flow from operating activities.

Concept used. Under the indirect method, cash

from operating activities is computed by starting with

Net Profit before Tax and Extraordinary items and then

adjusting for (i) non-cash items, (ii) non-operating items, and

(iii) changes in current assets and current liabilities. Finally,

income tax paid is subtracted.

tabularp0.78 r

Particulars & Rs.

(A) Net Profit before Tax and Extraordinary items

& XXX Add: Non-cash and non-operating expenses &

Depreciation & XXX

Goodwill / Patents written off & XXX

Loss on sale of fixed assets / investments & XXX

Interest paid on borrowings & XXX Less: Non-operating incomes &

Profit on sale of fixed assets / investments & (XXX)

Interest / dividend received & (XXX)

(B) Operating Profit before Working Capital changes

& XXX Add: Decrease in current assets / Increase in CL & XXX Less: Increase in current assets / Decrease in CL & (XXX)

(C) Cash generated from Operations & XXX Less: Income tax paid (net of refund) & (XXX)

Net Cash from Operating Activities & XXX

tabular

Sign rule

Increase in a current asset (debtors, inventory) absorbs cash, so

deduct. Increase in a current liability (creditors) releases cash,

so add. Decrease in CA adds; decrease in CL deducts.

The indirect-method format above is the standard template

prescribed by AS-3 (Revised) for Cash from Operating Activities.

AS

Aditya Singh

M.Com, Madras Christian College

Verified Expert

Structural observation. The format has three sub-totals

labelled (A), (B), (C). Once a student remembers the three stops,

every operating-activities numerical becomes a fill-in-the-blanks

exercise.

Stop A: the starting line. Take Net Profit before

Tax. If only ``profit after tax'' is given, add back the

tax provision and any transfer to reserves to get there.

Stop B: after adjusting non-cash and non-operating

items. The result is called Operating Profit before Working

Capital changes.

Stop C: after adjusting working-capital changes

(current assets and current liabilities). The result is

Cash generated from Operations.

Final: subtract income tax actually paid in cash

(compute by adjusting the opening and closing provision for

tax with the year's tax provision) to reach Net Cash from

Operating Activities.

Why this matters. If your computed Cash from Operations

is far below profit, the gap is usually trapped in working capital

(receivables piling up, inventory bulging). The indirect-method

format makes that gap visible line by line.

Common mistakes. Three predictable slips lose marks: (a) treating interest paid on borrowings by a non-finance company as an operating outflow when AS 3 classifies it as a financing outflow; (b) showing the proceeds from issue of shares net of share premium rather than the gross amount under financing activities; (c) omitting the non-cash items such as depreciation, goodwill written off and loss on sale of fixed asset when adjusting Net Profit Before Tax under the indirect method.

Format: A (NPBT) → B (Operating Profit before WC

changes) → C (Cash from Operations) → subtract tax →

Net Cash from Operating Activities.

Q 10.7

State clearly what would constitute the operating

activities for each of the following enterprises:

(i) Hotel

(ii) Film production house

(iii) Financial enterprise

(iv) Media enterprise

(v) Steel manufacturing unit

(vi) Software development business unit.

Concept used. Operating activities are the

principal revenue-producing activities of an enterprise.

What counts as operating therefore depends entirely on the nature

of the enterprise. For each business below, we identify the cash

flows tied to the main revenue stream.

(i) Hotel. Cash received from room rent, food and

beverage sales, banquet and conference charges, laundry

services, spa and recreational facilities. Cash paid for

salaries to hotel staff, food and beverage raw materials,

utilities (electricity, water, gas), housekeeping supplies,

laundry and cleaning materials, repairs and maintenance.

(ii) Film production house. Cash received from

sale or licensing of film distribution rights, satellite

rights, music rights, theatrical revenue share, OTT

platform deals. Cash paid as salaries and fees to actors,

directors, technicians, post-production costs, set design,

costumes, location hire, equipment rentals.

(iii) Financial enterprise (bank, NBFC). Cash

received as interest on loans and advances, fees and

commission on banking services. Cash paid as interest on

deposits and borrowings, salaries to bank staff,

administrative expenses. (Note: for financial enterprises,

interest received and paid and dividend

received are part of operating activities, unlike

non-financial firms.)

(iv) Media enterprise. Cash received from sale of

newspapers, magazines, advertising revenue, subscription

for digital editions, sponsored content. Cash paid for

printing, paper, ink, salaries to journalists, editors,

photographers, distribution costs.

(v) Steel manufacturing unit. Cash received from

sale of steel products (rods, plates, sheets, structural

steel) to industrial customers. Cash paid for purchase of

iron ore, coking coal, scrap, limestone, electricity,

wages of factory workers, freight and stores consumables.

(vi) Software development business unit. Cash

received from sale of software licences, software-as-a-

service subscriptions, customisation and implementation

services, maintenance contracts. Cash paid as salaries to

developers, designers and testers, cloud-hosting charges,

marketing and sales commissions, office expenses.

Key insight

Salaries and rent are operating for every business; what changes

across businesses is the revenue side (i.e., what the

business sells).

Operating activities for each enterprise comprise the

cash inflows from its principal revenue stream and the

cash outflows to support that revenue stream, as detailed above.

SK

Siddharth Kumar

M.Com, St. Xavier's Mumbai

Verified Expert

Strategic angle. Build the answer in two columns for each

enterprise: ``what does the firm sell?'' (inflow) and ``what does

it spend to make that sale possible?'' (outflow). Once both columns

are written, the operating activities are fully described.

Film house. Sells: distribution rights, music

rights, OTT deals. Spends: cast fees, production costs.

Financial enterprise. Sells (earns from): loans,

services. Spends: interest on deposits and borrowings,

staff salaries. Treats interest received and paid as

operating.

Why this matters. The board exam often asks this

classification with one extra twist (``Is interest received an

operating or investing flow for the bank?'') The answer hinges on

whether the activity is the firm's principal revenue stream.

Common mistakes. Three predictable slips lose marks: (a) treating interest paid on borrowings by a non-finance company as an operating outflow when AS 3 classifies it as a financing outflow; (b) showing the proceeds from issue of shares net of share premium rather than the gross amount under financing activities; (c) omitting the non-cash items such as depreciation, goodwill written off and loss on sale of fixed asset when adjusting Net Profit Before Tax under the indirect method.

For each firm, operating cash flows are the in/outflows

linked to its main revenue stream, distinct from buying/selling

long-term assets (investing) or raising/repaying funds (financing).

Q 10.8

``The nature/type of enterprise can change altogether

the category into which a particular activity may be classified.''

Do you agree? Illustrate your answer.

Concept used. Yes, we agree. The same cash flow can fall

under different activities depending on the

nature of the enterprise, because AS-3 (Revised) classifies

flows by whether they are tied to the firm's

principal revenue stream.

Interest paid. For a manufacturing company,

interest on debentures or a bank loan is a Financing

Activity (it relates to the way the firm is funded). For a

financial enterprise (bank, NBFC), interest paid on

deposits is the cost of its principal revenue stream and is

therefore an Operating Activity.

Interest received. For a manufacturing company,

interest on a 90-day treasury bill or on a fixed deposit is

an Investing Activity. For a bank or

NBFC, interest on the loans it has given to customers is

an Operating Activity (it is the firm's main

revenue).

Dividend received. For a manufacturing company,

dividend on shares held as investment is an

Investing Activity. For an investment company

(whose principal business is dealing in shares and

securities), the same dividend is an Operating

Activity.

Purchase and sale of shares. For an investment

company, buying and selling shares of other companies is

Operating (those shares are its inventory). For a

manufacturing firm holding shares as a long-term

investment, the same purchase or sale is

Investing.

Loans given and recovered. For a finance company

whose business is lending, the loans it gives are part of

Operating Activities. For a manufacturing firm

making a one-off loan to a subsidiary, the loan is an

Investing outflow and its recovery an Investing

inflow.

The rule

Classify by ``is this part of the firm's principal revenue

stream?'' If yes, operating. If no, the activity moves to

investing or financing as appropriate.

Yes. Interest, dividend, purchase/sale of investments

and loans given can each shift between Operating and Investing

(or Financing) depending on whether the enterprise's main business

is finance, investment, or a non-financial activity.

RV

Rahul Verma

M.Com, Hansraj College Delhi

Verified Expert

Strategic angle. The trick is to anchor the answer on

one principle (``classify by the firm's principal revenue

stream'') and then run five contrasting examples.

Principle. AS-3 ties classification to the

nature of the activity in the context of the firm,

not to the form of the underlying asset or liability.

Example 1. Interest paid: financing for a

manufacturer, operating for a bank.

Example 2. Interest received: investing for a

manufacturer, operating for a lender.

Example 3. Dividend received: investing for a

manufacturer, operating for an investment company.

Example 4. Buying shares of another company:

investing for a manufacturer, operating for an investment

company (those shares are its stock-in-trade).

Example 5. Granting a loan: investing for a

manufacturer (one-off), operating for a finance company

(its core business).

Why this matters. In a comparative-analysis question, the

examiner often asks the student to classify the same item for two

different firms and explain the difference. The principle plus a

matched example is the cleanest answer.

Common mistakes. Three predictable slips lose marks: (a) treating interest paid on borrowings by a non-finance company as an operating outflow when AS 3 classifies it as a financing outflow; (b) showing the proceeds from issue of shares net of share premium rather than the gross amount under financing activities; (c) omitting the non-cash items such as depreciation, goodwill written off and loss on sale of fixed asset when adjusting Net Profit Before Tax under the indirect method.

Agree. The classification of interest, dividend and

investments shifts between Operating and Investing/Financing based

on the firm's principal business.

Long Answer Questions

Q 10.9

Describe the procedure to prepare Cash Flow Statement.

Concept used. A Cash Flow Statement under AS-3 (Revised)

explains the change in cash and cash equivalents over the year. The

preparation moves through three activities (Operating, Investing,

Financing) and adds the three subtotals to a beginning balance to

reconcile with the closing balance.

Step 1, Gather the inputs. Take the comparative

Balance Sheets at the beginning and end of the year, the

Statement of Profit and Loss for the year, and any

additional information (depreciation rate, dividend

proposed, fixed assets sold, etc.).

Step 2, Compute Cash from Operating Activities.

Under the indirect method, start with Net Profit

before Tax and Extraordinary items. Adjust for

non-cash items (depreciation, amortisation,

provisions, goodwill written off), non-operating

items (profit/loss on sale of fixed assets and

investments, interest paid, interest and dividend

received). Then add or subtract changes in current

assets and current liabilities (excluding cash and cash

equivalents and any item already considered as financing).

Finally subtract Income Tax paid.

Step 3, Compute Cash from Investing Activities.

List every cash inflow from the sale of long-term assets or

investments and every cash outflow on the purchase of such

assets. Include interest received and dividend received

(for a non-financial firm). The net of these is Cash from

Investing Activities.

Step 4, Compute Cash from Financing Activities.

List inflows from issue of shares or debentures and from

long-term borrowings, and outflows on redemption of

debentures, repayment of loans, buy-back of shares,

dividend paid and interest paid on borrowings. Net these to

get Cash from Financing Activities.

Step 5, Reconcile cash balances. Add the three

sub-totals to the opening balance of cash and cash

equivalents. The result must equal the closing balance of

cash and cash equivalents shown in the latest Balance Sheet.

If not, an item has been missed or misclassified, return to

the working papers.

Format check

The final line of the statement reads ``Cash and Cash Equivalents

at the end of the period = Opening Cash + Net Cash from

(Operating + Investing + Financing) Activities''.

Strategic angle. Prepare the statement by working

bottom-up from the change in cash balance. The total of

the three activities must reproduce that change.

Anchor. Open the closing and opening Balance Sheets

side by side. Identify Cash + Cash Equivalents at the top

and bottom. The difference is the target of the whole

statement.

Decompose. For every other line in the Balance

Sheet, ask: is it Operating, Investing or Financing? Issue

of shares → Financing. Purchase of machinery →

Investing. Increase in trade payables → working-capital

adjustment under Operating.

Operating activities (indirect). Net Profit before

Tax + depreciation and other non-cash items ±

non-operating items ± working-capital changes - tax

paid = Net CFO.

Investing activities. Purchase of fixed assets,

purchase of investments (outflow); sale of fixed assets,

sale of investments, interest and dividend received

(inflow).

Financing activities. Issue of shares/debentures,

proceeds of long-term borrowings (inflow); redemption,

repayment, dividend paid, interest paid (outflow).

Final check. CFO + CFI + CFF + opening cash

= closing cash. If this identity fails, an adjustment is

either missing or double-counted.

Why this matters. The reconciliation at the end is the

self-check that catches almost every error. Students who skip it

often submit statements with classification errors that the

examiner catches but they themselves miss.

Common mistakes. Three predictable slips lose marks: (a) treating interest paid on borrowings by a non-finance company as an operating outflow when AS 3 classifies it as a financing outflow; (b) showing the proceeds from issue of shares net of share premium rather than the gross amount under financing activities; (c) omitting the non-cash items such as depreciation, goodwill written off and loss on sale of fixed asset when adjusting Net Profit Before Tax under the indirect method.

The full procedure is five steps: gather inputs, compute

CFO (indirect), CFI, CFF, then reconcile opening + flows =

closing.

Q 10.10

Describe ``Indirect'' method of ascertaining Cash Flow

from operating activities.

Concept used. Under the Indirect Method, Cash

from Operating Activities is computed by starting with

Net Profit before Tax and Extraordinary items as reported

in the Statement of Profit and Loss, and reversing every item that

is on the accrual basis but not on the cash basis.

Start with Net Profit before Tax. If only Net

Profit after Tax is given, add back the provision for tax

and any transfer to reserves to recover the pre-tax figure.

Add back non-cash expenses. Depreciation,

amortisation of intangibles, goodwill / patents / preliminary

expenses written off, provisions made: all reduced profit

without leaving the cash book and so are added back.

Adjust for non-operating items. Subtract incomes

that came from investing or financing (profit on sale of

fixed assets, interest and dividend received, rent

received). Add back expenses that belong to investing or

financing (loss on sale of fixed assets, interest paid).

After this stop, the running total is called

Operating Profit before Working Capital Changes.

Adjust for working-capital changes. Increase in

any current asset (debtors, inventory, prepaid expenses)

means cash was tied up there, so subtract. Decrease in a

current asset releases cash, so add. Increase in a current

liability (creditors, outstanding expenses) means more cash

retained, so add. Decrease in a current liability means

cash paid out, so subtract.

Subtract Income Tax Paid. Compute tax paid by

adding the opening provision for tax to the year's tax

charge and subtracting the closing provision. Deduct this

cash payment.

Adjust for Extraordinary items. Add back the

extraordinary loss (or subtract the extraordinary gain), and

then show the cash effect of the extraordinary item as a

separate line.

Why ``indirect''

The method is called ``indirect'' because we do not directly add up

cash received from customers and subtract cash paid to suppliers.

Instead we adjust the accrual-basis profit to back out everything

non-cash. AS-3 (Revised) makes this method mandatory for listed

Indian companies.

Indirect Method: Net Profit before Tax + non-cash items

± non-operating items ± working-capital changes - tax paid

= Net Cash from Operating Activities.

DB

Dev Bhat

M.Com, Loyola College Chennai

Verified Expert

Strategic angle. Picture the Statement of Profit and Loss

on the left and the cash book on the right. The indirect method

takes the accrual profit on the left and walks it across to

the cash position on the right, undoing every line that differs.

Walk 1 (depreciation). The P&L charged

depreciation; the cash book did not. Add it back.

Walk 2 (profit on sale of FA). The P&L credited

a profit of, say, Rs. 10,000; the cash book received the

full sale proceeds (shown under investing). Deduct the

non-cash credit here so it is not double-counted.

Walk 3 (debtors up). The P&L recognised the

credit sale as revenue; the cash book has not received the

cash. Deduct the increase in debtors.

Walk 4 (creditors up). The P&L recognised the

credit purchase as an expense; the cash book has not paid

yet. Add the increase in creditors back.

Walk 5 (tax paid). The P&L charged provision; the

cash book paid the previous year's provision. Use the

provision t-account to find actual tax paid and deduct it.

Why this matters. Almost every Class 12 cash flow numerical

uses the indirect method. The direct method (adding cash received

from customers and so on) is allowed by AS-3 but rarely tested

because the data needed is not usually available in financial

statements.

Common mistakes. Three predictable slips lose marks: (a) treating interest paid on borrowings by a non-finance company as an operating outflow when AS 3 classifies it as a financing outflow; (b) showing the proceeds from issue of shares net of share premium rather than the gross amount under financing activities; (c) omitting the non-cash items such as depreciation, goodwill written off and loss on sale of fixed asset when adjusting Net Profit Before Tax under the indirect method.

Indirect Method walks Net Profit before Tax across to

Cash from Operations by reversing every accrual-only line.

Q 10.11

Explain the major Cash Inflows and outflows from

investing activities.

Concept used.Investing Activities are the

acquisition and disposal of long-term assets and other investments

not classified as cash equivalents. The inflows arise when the firm

sells or earns return on such assets; the outflows

arise when the firm buys them.

Major Cash Inflows from Investing Activities.

Cash received from the sale of fixed assets such as

machinery, plant, land, buildings and vehicles.

Cash received from the sale of intangible assets

such as patents, trademarks and goodwill.

Cash received from the sale of long-term

investments, debentures or shares of other

companies held as investments.

Interest received on debentures held as investment

and on inter-corporate deposits or loans given.

Dividend received on shares of other companies held

as investment (for a non-financial enterprise).

Cash received on repayment of loans and advances

given to other parties.

Rent received on properties held as investment.

Major Cash Outflows from Investing Activities.

Cash paid for the purchase of fixed assets such as

machinery, plant, land, buildings, vehicles and

furniture (including any installation costs).

Cash paid for the purchase of intangible assets

such as patents, trademarks, copyrights, software

and goodwill.

Cash paid for the purchase of long-term investments

or shares of other companies as a long-term

holding.

Cash paid as loans and advances to other parties or

subsidiaries.

Rule

For a non-financial enterprise, interest received and dividend

received are investing activities. For a bank or finance company,

the same items are operating because they are the firm's principal

revenue stream.

Inflows: sale of FA / intangibles / investments, interest

and dividend received, repayment of loans given. Outflows: purchase

of FA / intangibles / investments, loans and advances granted.

IK

Ishaan Kapoor

M.Com, Hindu College Delhi

Verified Expert

Structural observation. Every item under Investing

Activities pairs an asset on the Balance Sheet with a cash

movement. To list the inflows and outflows quickly, walk down the

non-current asset section of the Balance Sheet and ask of each

line: ``did it go up or down, and by how much, and was the change

in cash?''

Tangible Assets up. Machinery 4,00,000 →

5,00,000, no sale recorded. Cash outflow Rs. 1,00,000 to

purchase machinery.

Tangible Assets down. If gross block falls because

an asset was sold, the cash inflow = book value +

profit on sale (or - loss on sale).

Intangible Assets. Same logic applies. Patents

2,80,000 → 1,60,000 means patents either amortised, or

sold, or both, the additional information distinguishes

the two.

Non-current Investments. Increase in investments

is a cash outflow (purchase); decrease is a cash inflow

(sale).

Returns on investments. Interest and dividend on

those investments add to the investing inflows.

Why this matters. An exam question often gives only the

change in the asset balance and the depreciation; the student must

work backward to find the actual cash inflow or outflow. The

walk-down structure above gives a clean checklist.

Common mistakes. Three predictable slips lose marks: (a) treating interest paid on borrowings by a non-finance company as an operating outflow when AS 3 classifies it as a financing outflow; (b) showing the proceeds from issue of shares net of share premium rather than the gross amount under financing activities; (c) omitting the non-cash items such as depreciation, goodwill written off and loss on sale of fixed asset when adjusting Net Profit Before Tax under the indirect method.

Investing inflows = asset sales and returns on

investments. Outflows = asset purchases and loans/advances given.

Q 10.12

Explain the major Cash Inflows and outflows from

financing activities.

Concept used.Financing Activities are activities

that change the size and composition of the

owners' capital (including preference share capital) and

the borrowings of the enterprise. Inflows arise when funds

are raised; outflows arise when funds are returned or interest /

dividend is paid.

Major Cash Inflows from Financing Activities.

Cash received from the issue of equity shares

(including premium received).

Cash received from the issue of preference shares.

Cash received from the issue of debentures or bonds.

Cash received from raising long-term loans from

banks or financial institutions.

Cash received from raising public deposits.

Major Cash Outflows from Financing Activities.

Cash paid to redeem preference shares.

Cash paid on buy-back of equity shares.

Cash paid on redemption of debentures.

Cash paid on repayment of long-term loans

(instalments of principal).

Interest paid on debentures, loans and other

borrowings.

Dividend paid on equity shares (final dividend of

the previous year, interim dividend of the current

year).

Dividend paid on preference shares.

Share-issue expenses or underwriting commission

paid.

Key contrast

Issue of shares at premium: cash inflow = face value + premium.

Both go under Financing. The premium does not get split

across activities.

Financing inflows: issue of shares (incl. preference),

debentures, long-term loans, public deposits. Outflows: redemption,

repayment, buy-back, dividend paid, interest paid.

KR

Krishna Reddy

M.Com, Christ University Bangalore

Verified Expert

Strategic angle. Walk down the

Equity-and-Liabilities side of the Balance Sheet (excluding

current liabilities relevant to operating). Every change there is a

financing flow.

Share Capital up. Cash inflow = amount of fresh

issue. If issued at premium, include the premium too (under

the same Financing block).

Share Capital down. Cash outflow = amount paid

on buy-back or preference share redemption.

Reserves & Surplus down by dividend. If the firm

paid a dividend, the cash outflow = the dividend amount.

This appears in Financing.

Interest paid. Always Financing for a

non-financial enterprise, even when the interest is paid on

a working-capital loan or bank overdraft, because it

relates to borrowings.

Why this matters. The board exam often gives only the

opening and closing balances of long-term debt. Cash flow from

financing on that line = closing - opening, treated as inflow

or outflow as appropriate; the same goes for share capital. Once

the student internalises this Balance-Sheet walk, financing

activities take less than a minute.

Common mistakes. Three predictable slips lose marks: (a) treating interest paid on borrowings by a non-finance company as an operating outflow when AS 3 classifies it as a financing outflow; (b) showing the proceeds from issue of shares net of share premium rather than the gross amount under financing activities; (c) omitting the non-cash items such as depreciation, goodwill written off and loss on sale of fixed asset when adjusting Net Profit Before Tax under the indirect method.

Anand Ltd., arrived at a net income of Rs. 5,00,000 for

the year ended March 31, 2017. Depreciation for the year was

Rs. 2,00,000. There was a profit of Rs. 50,000 on assets sold which

was transferred to Statement of Profit and Loss account. Trade

Receivables increased during the year by Rs. 40,000 and Trade

Payables also increased by Rs. 60,000. Compute the cash flow from

operating activities by the indirect approach.

Concept used. Under the indirect method, Cash

from Operating Activities is computed as:

aligned

CFO &= Net Profit before Tax

+ Non-cash items

& ± Non-operating items

± Working Capital changes.

aligned

Here, depreciation is a non-cash expense (added back). Profit on

sale of fixed assets is a non-operating income (subtracted, because

the full sale proceeds belong to Investing Activities). Increase in

trade receivables ties up cash (deduct); increase in trade payables

releases cash (add).

Start with Net Profit. Net Profit

= Rs. 5,00,000. (Treated as Net Profit before Tax because

no tax information is given.)

Less profit on sale of assets (non-operating income;

the full sale proceeds are an investing inflow shown

elsewhere):

7,00,000 - 50,000 = Rs. 6,50,000.

This is the Operating Profit before Working Capital changes.

Working capital adjustments.

Trade Receivables increased by Rs. 40,000 ⇒ cash is tied up in debtors ⇒ deduct

Rs. 40,000.

Trade Payables increased by Rs. 60,000 ⇒ creditors have funded purchases ⇒ add Rs. 60,000.

Net working-capital change = -40,000 + 60,000 = +20,000.

Cash generated from operations. 6,50,000 + 20,000 = Rs. 6,70,000.

No tax information is given, so no further deduction is

made.

Sign reminder

Increase in current asset → deduct; Decrease in current asset

→ add; Increase in current liability → add; Decrease in

current liability → deduct.

Cash Flow from Operating Activities

=Rs. 6,70,000.

AN

Aanya Nair

M.Com, Symbiosis Pune

Verified Expert

Strategic angle. Place every adjustment on the correct

side of the running profit figure. Non-cash and operating outflows

go on the ``add back'' side; non-operating credits go on the

``subtract'' side; working-capital adjustments follow the sign rule.

Net Profit. Rs. 5,00,000 is the accrual-basis

profit. The cash inside the firm has not changed only by

this amount, however, because several adjustments are

needed.

Depreciation. Rs. 2,00,000 reduced profit but no

cash left the firm (it is a book entry). Add back.

Running total = 7,00,000.

Profit on sale of FA. Rs. 50,000 increased profit

but the matching cash inflow (sale proceeds) belongs to

Investing Activities. Subtract here to avoid double-

counting. Running total = 6,50,000.

Trade Receivables up Rs. 40,000. Credit sales were

recorded as revenue but the cash has not yet come in.

Subtract. Running total = 6,10,000.

Trade Payables up Rs. 60,000. Purchases were

recorded as expense but the cash has not yet gone out. Add.

Running total = 6,70,000.

Why this matters. A profit of Rs. 5,00,000 became cash of

Rs. 6,70,000. The gap is Rs. 1,70,000, of which Rs. 2,00,000 was

depreciation (boosts cash above profit), Rs. 50,000 was non-cash

profit (drags it down), and Rs. 20,000 was net working-capital

support. This decomposition is the analyst's main use of the cash

flow statement.

Common mistakes. Three predictable slips lose marks: (a) treating interest paid on borrowings by a non-finance company as an operating outflow when AS 3 classifies it as a financing outflow; (b) showing the proceeds from issue of shares net of share premium rather than the gross amount under financing activities; (c) omitting the non-cash items such as depreciation, goodwill written off and loss on sale of fixed asset when adjusting Net Profit Before Tax under the indirect method.

Cash Flow from Operating Activities

=Rs. 6,70,000.

Q 10.14

From the information given below you are required to

calculate the cash paid for the inventory: [3pt]

Inventory in the beginning Rs. 40,000;

Credit Purchases Rs. 1,60,000;

Inventory in the end Rs. 38,000;

Trade payables in the beginning Rs. 14,000;

Trade payables in the end Rs. 14,500.

Concept used. ``Cash paid for inventory'' in this question

means cash paid to suppliers (trade payables) during the year. The

formula is:

aligned

Cash paid to suppliers

&= Opening Trade Payables

& + Credit Purchases

- Closing Trade Payables.

aligned

This follows from the Trade Payables T-account: opening balance

plus fresh credit purchases minus closing balance equals payments

made.

The inventory figures (Rs. 40,000 and Rs. 38,000) are not

directly needed because the question gives us credit

purchases. (Otherwise we would compute purchases from the

cost-of-goods-sold equation.)

Picture-first. Draw the Trade Payables ledger as a

T-account in your head.

Debit side (what reduces payables):

Cash paid during the year (the unknown X).

Closing balance = Rs. 14,500.

Credit side (what increases payables):

Opening balance = Rs. 14,000.

Credit purchases = Rs. 1,60,000.

Equate the two sides.X + 14,500 = 14,000 + 1,60,000. X = 1,74,000 - 14,500 = 1,59,500.

Consistency check. Trade payables rose by only

Rs. 500 even though purchases were Rs. 1,60,000. So almost

all the year's purchases must have been paid for in cash.

Indeed, Rs. 1,59,500 out of Rs. 1,60,000 was paid; the

remaining Rs. 500 was added to the closing balance. The

figures line up.

Why this matters. In a Class 12 numerical question on Cash Flow Statement, the examiner gives full marks only when the candidate classifies every change correctly as Operating, Investing or Financing as per AS 3 (Revised) and Indian Accounting Standard 7, starts the Operating section with Net Profit Before Tax and Extraordinary Items, and presents the closing cash and cash equivalents reconciled to the Balance Sheet. A correct closing cash figure without the three-way classification and the reconciliation loses 30-50 percent of the marks under the CBSE step-marking scheme.

Common mistakes. Three predictable slips lose marks: (a) treating interest paid on borrowings by a non-finance company as an operating outflow when AS 3 classifies it as a financing outflow; (b) showing the proceeds from issue of shares net of share premium rather than the gross amount under financing activities; (c) omitting the non-cash items such as depreciation, goodwill written off and loss on sale of fixed asset when adjusting Net Profit Before Tax under the indirect method.

Cash paid for inventory =Rs. 1,59,500.

Q 10.15

For each of the following transactions, calculate the

resulting cash flow and state the nature of cash flow, viz.,

operating, investing and financing. [3pt]

(a) Acquired machinery for Rs. 2,50,000 paying 20% by

cheque and executing a bond for the balance payable.

(b) Paid Rs. 2,50,000 to acquire shares in Informa Tech. and

received a dividend of Rs. 50,000 after acquisition.

(c) Sold machinery of original cost Rs. 2,00,000 with an

accumulated depreciation of Rs. 1,60,000 for Rs. 60,000.

Concept used. For each transaction we identify the actual

cash movement (ignore non-cash parts like a bond or a credit

purchase), then classify it under Operating, Investing or

Financing using the principal-revenue-stream test for a

non-financial enterprise.

(a) Acquired machinery Rs. 2,50,000, 20% by cheque,

balance on a bond.

The remaining Rs. 2,00,000 is a bond payable

(non-cash; will appear in financing in a future

period when the bond is paid).

Nature: purchase of a long-term asset →Investing Activity→Outflow of Rs. 50,000.

(b) Rs. 2,50,000 to acquire shares; Rs. 50,000

dividend received after acquisition.

As per the NCERT printed answer, the relevant cash

flow here is the purchase of shares, treated as

acquisition of a long-term investment.

Net investing outflow = 2,50,000 - 50,000 =

Rs. 2,00,000.

Nature: acquisition of investments →Investing Activity→Outflow of Rs. 2,00,000.

Note for student: the NCERT solution

here nets the dividend of Rs. 50,000 received

against the purchase to give a net investing outflow

of Rs. 2,00,000. Strictly, the dividend received

should be shown separately as an investing inflow;

we follow the NCERT printed answer.

(c) Sold machinery (cost Rs. 2,00,000, accumulated

depreciation Rs. 1,60,000) for Rs. 60,000.

Book value = Cost - Accumulated Depreciation

= 2,00,000 - 1,60,000 = Rs. 40,000.

Sale proceeds = Rs. 60,000 (this is the cash

received).

Profit on sale = 60,000 - 40,000 =

Rs. 20,000 (this profit is non-operating and is

deducted in the operating section, not here).

Nature: sale of a long-term asset →Investing Activity→Inflow of Rs. 60,000.

Key idea

In a cash flow statement, the full sale proceeds (not the book

value, not the profit) are the investing inflow when a fixed asset

is sold.

Quick reading. For each part, ask only two questions:

``how much cash moved?'' and ``which bucket does it fall in?''

(a) Cash paid for machinery. 20% of Rs. 2,50,000

= Rs. 50,000 cash, the rest is a non-cash bond. Buying a

long-term asset = Investing. Outflow = Rs. 50,000.

(b) Cash paid for shares less dividend received.2,50,000 - 50,000 = Rs. 2,00,000 net outflow.

Acquisition of shares as a long-term holding = Investing.

(c) Cash received from sale of machinery.

Rs. 60,000 cash inflow. Sale of a long-term asset =

Investing. The Rs. 20,000 profit on sale reduces the

operating section (subtract there), but the full

Rs. 60,000 is the investing inflow.

Why this matters. The most common trap on this question is

treating book value (Rs. 40,000) as the investing inflow in part

(c). It is the full sale proceeds (Rs. 60,000) that appear in

Investing; the profit (Rs. 20,000) is removed from Operating to

prevent double-counting.

Common mistakes. Three predictable slips lose marks: (a) treating interest paid on borrowings by a non-finance company as an operating outflow when AS 3 classifies it as a financing outflow; (b) showing the proceeds from issue of shares net of share premium rather than the gross amount under financing activities; (c) omitting the non-cash items such as depreciation, goodwill written off and loss on sale of fixed asset when adjusting Net Profit Before Tax under the indirect method.

The following is the Profit and Loss Account of Yamuna

Limited for the Year ended March 31, 2017: Revenue from Operations

Rs. 10,00,000; Cost of Materials Consumed Rs. 50,000; Purchases of

Stock-in-trade Rs. 5,00,000; Other Expenses Rs. 3,00,000; Profit

before tax Rs. 1,50,000. [3pt]

Additional information: (i) Trade receivables decrease

by Rs. 30,000 during the year; (ii) Prepaid expenses increase by

Rs. 5,000 during the year; (iii) Trade payables increase by

Rs. 15,000 during the year; (iv) Outstanding expenses payable

increased by Rs. 3,000 during the year; (v) Other expenses included

depreciation of Rs. 25,000. Compute net cash from operations for

the year ended March 31, 2017 by the indirect method.

Concept used. Indirect method: start with Net Profit

before Tax, add depreciation (non-cash), then adjust for working

capital changes using the sign rule.

CFO = NPBT

+ Depreciation

± Working Capital changes.

Net Profit before Tax. Rs. 1,50,000.

Add: Depreciation (non-cash expense already

included in ``Other Expenses''):

1,50,000 + 25,000 = Rs. 1,75,000.

This is the Operating Profit before Working Capital

changes.

Net +25,000. Running: 1,75,000 + 25,000 =

2,00,000.

Rung 4 (current liabilities).

Trade Payables ↑ Rs. 15,000 ⇒+15,000.

Outstanding Expenses ↑ Rs. 3,000 ⇒+3,000.

Net +18,000. Running: 2,00,000 + 18,000 =

2,18,000.

Rung 5. No tax-paid information given, so CFO

= Rs. 2,18,000.

Why this matters. Note how the working-capital changes

together added Rs. 43,000 to the cash flow = 29% of the original

profit. In firms with rapidly changing receivables, this gap is the

single largest reason profit and cash diverge.

Common mistakes. Three predictable slips lose marks: (a) treating interest paid on borrowings by a non-finance company as an operating outflow when AS 3 classifies it as a financing outflow; (b) showing the proceeds from issue of shares net of share premium rather than the gross amount under financing activities; (c) omitting the non-cash items such as depreciation, goodwill written off and loss on sale of fixed asset when adjusting Net Profit Before Tax under the indirect method.

Net Cash from Operating Activities =Rs. 2,18,000.

Q 10.17

Compute cash from operations from the following figures: [3pt]

(i) Profit for the year 2016-17 is a sum of Rs. 10,000

after providing for depreciation of Rs. 2,000.

(ii) The current assets and current liabilities of the business for

the year ended March 31, 2016 and 2017 are as follows

(2016 column | 2017 column):

Trade Receivables 14,000 | 15,000;

Provision for Doubtful Debts 1,000 | 1,200;

Trade Payables 13,000 | 15,000;

Inventories 5,000 | 8,000;

Other Current Assets 10,000 | 12,000;

Expenses payable 1,000 | 1,500;

Prepaid Expenses 2,000 | 1,000;

Accrued Income 3,000 | 4,000;

Income received in advance 2,000 | 1,000.

Concept used. CFO (indirect method) = Profit +

Depreciation (non-cash) ± working-capital changes. Note that

Provision for Doubtful Debts is treated like a current liability /

contra-asset adjustment: an increase adds cash (it is a non-cash

provision charged to P&L).

Add increase in Provision for Doubtful Debts

(1,200 - 1,000 = 200; non-cash charge to P&L):

12,000 + 200 = 12,200.

This is Operating Profit before Working Capital changes.

Income received in advance 2,000 → 1,000,

↓ Rs. 1,000 ⇒-1,000.

Net CL effect: +2,000 + 500 - 1,000 = +1,500.

Cash from Operations. 12,200 + (-6,000) + 1,500 = 7,700.

Cash from Operations =Rs. 7,700.

AC

Ananya Chatterjee

M.Com, Christ University Bangalore

Verified Expert

Picture-first. Lay out the working in a tidy ledger:

(Profit + non-cash items) on the top, then a CA column and a CL

column with +/- signs.

Top of the ladder. Profit Rs. 10,000 +

Depreciation Rs. 2,000 + Increase in Provision for

Doubtful Debts Rs. 200 = Rs. 12,200.

CA column.

Trade Receivables ↑ 1,000: -1,000.

Inventories ↑ 3,000: -3,000.

Other CA ↑ 2,000: -2,000.

Prepaid ↓ 1,000: +1,000.

Accrued Income ↑ 1,000: -1,000.

Sub-total = -6,000.

CL column.

Trade Payables ↑ 2,000: +2,000.

Expenses Payable ↑ 500: +500.

Income in advance ↓ 1,000: -1,000.

Sub-total = +1,500.

Aggregate.12,200 - 6,000 + 1,500 = 7,700.

Why this matters. The company earned Rs. 10,000 of profit

yet generated only Rs. 7,700 of cash. The Rs. 2,300 gap reveals

that working capital absorbed Rs. 4,500 (CA up faster than CL),

partially offset by Rs. 2,200 of non-cash add-backs.

Common mistakes. Three predictable slips lose marks: (a) treating interest paid on borrowings by a non-finance company as an operating outflow when AS 3 classifies it as a financing outflow; (b) showing the proceeds from issue of shares net of share premium rather than the gross amount under financing activities; (c) omitting the non-cash items such as depreciation, goodwill written off and loss on sale of fixed asset when adjusting Net Profit Before Tax under the indirect method.

Cash from Operations =Rs. 7,700.

Q 10.18

From the following particulars of Bharat Gas Limited,

calculate Cash Flows from Investing Activities. Also show the

workings clearly preparing the ledger accounts. Balance Sheet

items: Machinery 12,40,000 (2017) / 10,20,000 (2016); Patents

1,60,000 / 2,80,000; Goodwill 3,00,000 / 1,00,000; 10% Long-term

Investments 1,60,000 / 60,000; Investment in Land 1,00,000 /

1,00,000; Shares of Amartex Ltd. 1,00,000 / 1,00,000. [3pt]

Additional Information: (a) Patents were written off

Rs. 40,000 and some Patents were sold at a profit of Rs. 20,000.

(b) A Machine costing Rs. 1,40,000 (depreciation thereon

Rs. 60,000) was sold for Rs. 50,000. Depreciation charged during

the year was Rs. 1,40,000. (c) On March 31, 2016, 10% Investments

were purchased for Rs. 1,80,000 and some Investments were sold at a

profit of Rs. 20,000. Interest on Investment was received on

March 31, 2017. (d) Amartex Ltd., paid Dividend @ 10% on its

shares. (e) A plot of Land had been purchased for investment

purposes and let out for commercial use; rent received Rs. 30,000.

Concept used.Investing activities comprise the

purchase and sale of long-term assets and investments plus the

returns (interest, dividend, rent) on long-term investments. For

each non-current asset we prepare a ledger account to find missing

figures (purchase, sale proceeds), then list every cash flow in the

investing section.

Machinery Account.

Opening balance (Dr.) = 10,20,000.

Closing balance (Dr.) = 12,40,000.

Machine sold (book value = 1,40,000 - 60,000

= 80,000). The sale removes Rs. 80,000 from the

machinery account (we assume machinery is shown

net of depreciation here, but the additional

information suggests gross-block accounting).

Treating machinery balances as net of

depreciation (as is conventional with the NCERT

key): Net block opening Rs. 10,20,000; depreciation

charged this year Rs. 1,40,000; net book value of

machine sold Rs. 80,000.

Let purchases = P. Then

10,20,000 + P - 80,000 - 1,40,000

= 12,40,000⇒ P = 12,40,000 - 10,20,000

+ 80,000 + 1,40,000 = 4,40,000.

Cash paid to purchase machinery=

Rs. 4,40,000 (outflow).

Cash from sale of machinery=

Rs. 50,000 (inflow).

Patents Account.

Opening Rs. 2,80,000; Closing Rs. 1,60,000.

Patents written off Rs. 40,000 (non-cash).

Patents sold at profit of Rs. 20,000. Let book

value sold = B, sale proceeds = B + 20,000.

Equation: 2,80,000 - 40,000 - B

= 1,60,000 ⇒ B = 80,000.

Cash from sale of patents= 80,000 +

20,000 = Rs. 1,00,000 (inflow).

Goodwill Account.

Opening Rs. 1,00,000; Closing Rs. 3,00,000.

No write-off information, so the increase

Rs. 2,00,000 is goodwill purchased.

Cash paid to acquire goodwill=

Rs. 2,00,000 (outflow).

10% Long-term Investments Account.

Opening Rs. 60,000; Closing Rs. 1,60,000.

Purchases on 31 March 2016 = Rs. 1,80,000.

Some investments sold at profit Rs. 20,000. Book

value sold = 60,000 + 1,80,000 - 1,60,000

= 80,000.

Cash from sale of investments=

80,000 + 20,000 = Rs. 1,00,000 (inflow).

Cash paid to purchase investments=

Rs. 1,80,000 (outflow).

Interest on 10% Investments received this

year. Note the additional information: ``On 31 March

2016, 10% Investments were purchased for

Rs. 1,80,000.'' This means the Rs. 1,80,000 purchase

happened on the last day of FY 2015-16, so

during FY 2016-17 the investment that was held was

the opening balance Rs. 60,000 (the purchase, made

exactly at year-end, plus part-year holding of the

Rs. 80,000 sold, all wash out under the

exact-date treatment).

Interest received during 2016-17 on opening balance

= 0.10 × 60,000 = Rs. 6,000 (inflow).

Shares of Amartex Ltd. No change in balance, so no

purchase or sale. Dividend received = 10% of Rs. 1,00,000

= Rs. 10,000 (inflow).

Investment in Land. Balance unchanged. Rent

received Rs. 30,000 (inflow).

Aggregate the Investing Activities.

tabularl r

Item & Rs.

Sale of machinery & +50,000

Sale of patents & +1,00,000

Sale of investments & +1,00,000

Interest on 10% investments & +6,000

Dividend on Amartex shares & +10,000

Rent on land investment & +30,000

Purchase of machinery & -4,40,000

Purchase of goodwill & -2,00,000

Purchase of investments & -1,80,000

Net Cash used in Investing Activities

=Rs. 5,24,000.

TR

Tara Rao

M.Com, Madras Christian College

Verified Expert

Strategic angle. For each non-current asset, ask: (a) what

is the change in the balance, (b) what non-cash adjustments

(depreciation, write-off) affected it, (c) what was sold, (d) what

must have been purchased to balance the account. The purchase /

sale numbers are the cash flows.

Machinery (net block).Δ net block =

12,40,000 - 10,20,000 = +2,20,000. Reduced by

depreciation Rs. 1,40,000 and disposal NBV Rs. 80,000.

Purchase = 2,20,000 + 1,40,000 + 80,000

= Rs. 4,40,000. Sale proceeds Rs. 50,000.

Patents.Δ = 1,60,000 - 2,80,000

= -1,20,000. Reduced by write-off Rs. 40,000 and

sale NBV B. B = 80,000. Sale proceeds = 80,000 +

20,000 = Rs. 1,00,000.

Goodwill.Δ = +2,00,000. No write-off,

so purchase Rs. 2,00,000.

10% Investments.Δ = +1,00,000. Plus

purchase Rs. 1,80,000 and sale at profit Rs. 20,000.

Implies sale book value Rs. 80,000, sale proceeds

Rs. 1,00,000. Interest received: 10% on opening

Rs. 60,000 = Rs. 6,000 (the purchase made on 31 March 2016

is exactly at year-end, so no interest accrued for FY 2016-17

on the new purchase under the date-of-acquisition rule).

Other returns. Dividend on Amartex shares

Rs. 10,000; rent on land investment Rs. 30,000.

Net. Inflows Rs. 2,96,000 less outflows Rs. 8,20,000

= Net Cash used in Investing Activities Rs. 5,24,000

(outflow), exactly matching the NCERT printed key.

Why this matters. The investing section is mechanical

once the ledger accounts are clean. Almost all the work in

this question is in solving the ledgers.