The 2026-27 NCERT keeps Part 2 Chapter 4 Analysis of Financial Statements intact in Part B, covering financial analysis, its tools, and Comparative and Common Size Statements. These NCERT Solutions solve every question in textbook order.

CBSE Weightage: 4 to 6 marks, usually one 6-mark statement question plus a 1-mark objective question

CUET Relevance: 3 to 5 questions in the Accountancy paper, mostly on tools of analysis and statement format

These NCERT Solutions are reviewed by Chartered Accountants and CBSE Commerce educators, mapped to the 2026-27 print, and checked against five years of CBSE and CUET papers.

Part 2 Chapter 4 sits in Part B: Financial Statements Analysis, between Chapter 3 and Chapters 5-6.

Why Class 12 Accountancy Part 2 Chapter 4 Solutions Are Worth the Practice

Analysis of Financial Statements is high-return: CBSE almost always sets one full Comparative or Common Size Statement. Students often lose 2 to 3 marks on presentation, not calculation. These solutions train you to write the CBSE-accepted format.

Quick Tip: In a Comparative Statement, the percentage change always uses the previous year (base) figure, not the current year. Reversing the base is the top reason a correct calculation still loses the percentage-column mark.

Class 12 Accountancy Part 2 Chapter 4 Analysis Of Financial Statements NCERT Solutions

Full Working: Each Statement solved column by column.

Expert Verification: CAs checked every percentage and sub-total.

Answer-Writing Cues: Each solution flags where step marks sit.

NCERT Solutions for Class 12 Accountancy Part 2 Chapter 4: Common Question Phrasings

CBSE recycles a small set of phrasings. Recognising the wording tells you instantly which statement format to use.

Question Stem

What It Wants

"Prepare a Comparative Statement of Profit and Loss..."

Two-year columns plus absolute and percentage change

"Prepare a Common Size Balance Sheet..."

Each item as % of Total Assets or Total Equity and Liabilities

"State any two objectives / limitations of financial analysis."

1 to 3 mark theory answer in points

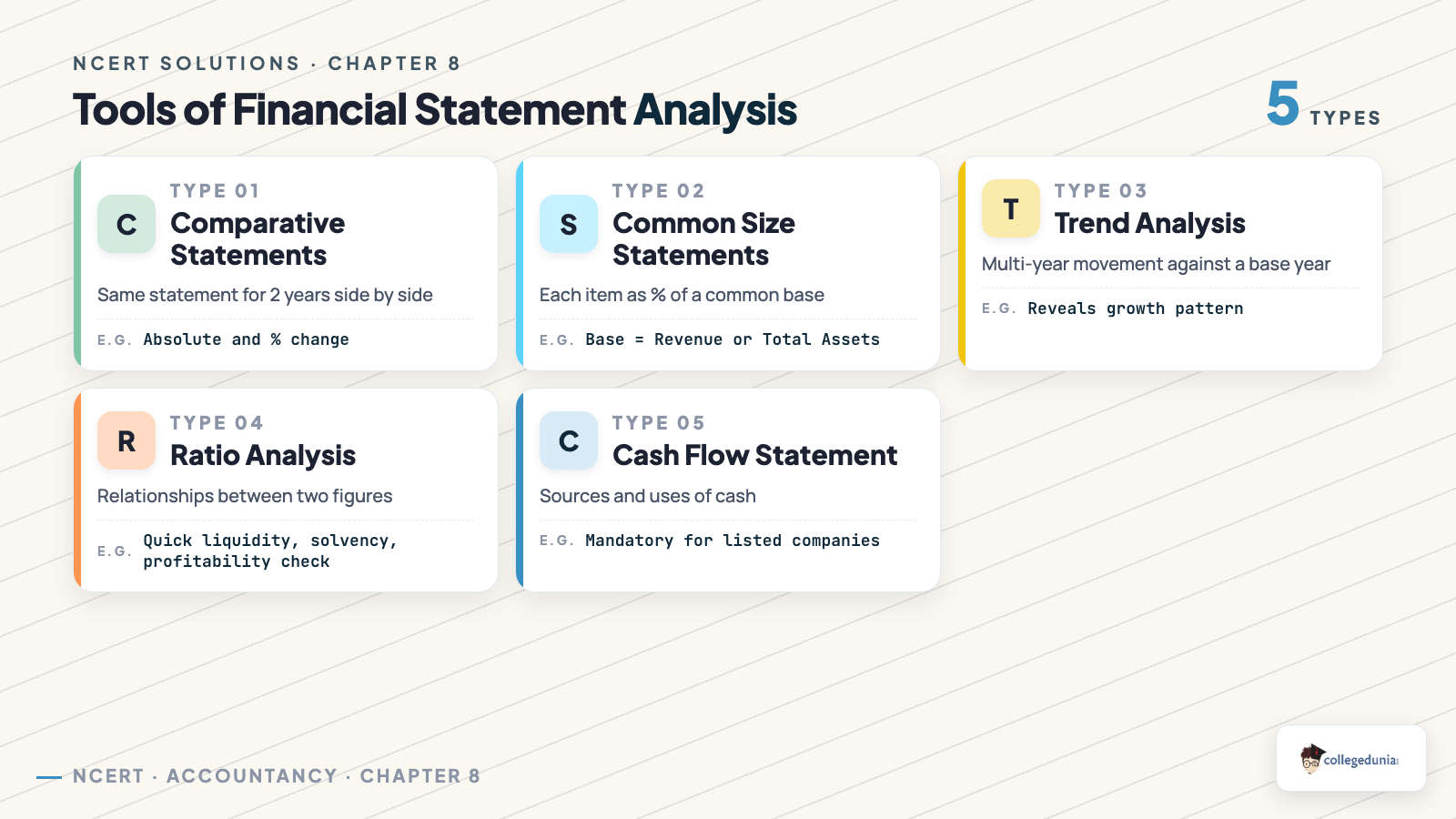

"List the tools of analysis of financial statements."

Comparative, Common Size, Ratio Analysis, Cash Flow

"From the following Statement of Profit and Loss, prepare..."

Numerical with given Revenue, Expenses and Tax

Analysis of Financial Statements Exercise-by-Exercise Breakdown (NCERT Class 12 Accountancy)

The chapter has no numbered exercises; questions are grouped by type. The table shows how many of each type the NCERT print carries.

Question Block

Count

Sub-Topic

Test Your Understanding (Objective)

6+

Meaning, tools, parties interested

Short Answer Questions

5

Objectives, limitations, types of analysis

Long Answer Questions

4

Tools of analysis, significance of analysis

Numerical Questions

12+

Comparative Statement, Common Size Statement

Concept: Comparative Statements show horizontal analysis (change over two years); Common Size Statements show vertical analysis (each item as a percentage of a base). Name the type when CBSE asks.

Sample Fully-Solved Question Walk-Through: Comparative Statement of Profit and Loss

A typical 6-mark CBSE numerical: Revenue from Operations was Rs 8,00,000 in 2023-24 and Rs 10,00,000 in 2024-25; Total Expenses were Rs 5,00,000 and Rs 6,50,000; tax is 50%. The percentage change uses the base-year figure:

$$\text{Percentage Change} = \frac{\text{Absolute Change}}{\text{Previous Year Figure}} \times 100$$

Particulars

2023-24 (Rs)

2024-25 (Rs)

Absolute Change (Rs)

% Change

Revenue from Operations

8,00,000

10,00,000

2,00,000

25.00

Total Expenses

5,00,000

6,50,000

1,50,000

30.00

Profit before Tax

3,00,000

3,50,000

50,000

16.67

Less: Tax @ 50%

1,50,000

1,75,000

25,000

16.67

Profit after Tax

1,50,000

1,75,000

25,000

16.67

Percentage change for Revenue from Operations: 2,00,0008,00,000 × 100 = 25% . Full marks need the four-column layout, correct sub-totals, and two-decimal rounding.

Marks Budget for a 6-Mark Analysis of Financial Statements Question

Knowing where each mark sits tells you what you must not skip under exam pressure.

Step

Marks

What Earns It

Correct format and column headings

1

Four-column layout with title and sub-headings

Current and previous year figures placed correctly

1.5

Right items under right years, with sub-totals

Absolute change column

1.5

Current year minus previous year, every line

Percentage change column

1.5

Change over base year, two-decimal rounding

Profit before / after tax line

0.5

Tax adjustment and final profit shown

Common Mistakes Students Make in Analysis of Financial Statements

Most lost marks come from presentation slips, not arithmetic. Watch for these.

Computing the percentage change on the current year instead of the previous (base) year.

Using a Comparative format when Common Size was asked, or the reverse.

Forgetting the Tax line, so Profit after Tax is missing.

In a Common Size Balance Sheet, using the wrong base (Total Assets or Total Equity and Liabilities).

Watch Out:A Common Size Statement always sums to 100% on its base. If your column does not total 100, a figure is wrong, and the examiner will spot it.

How to Study Analysis of Financial Statements for Class 12 Accountancy Boards

This is a format-driven chapter, so practice beats re-reading. Budget about 6 to 7 hours, spread over four short sessions.

Day 1 (1.5 hours): Read the meaning, objectives, and limitations; learn the four tools by name.

Day 2 (2 hours): Solve Comparative Statement numericals until the layout is automatic.

Day 3 (2 hours): Solve Common Size numericals for both Profit and Loss and Balance Sheet.

Day 4 (1 hour): Revise theory questions and attempt one past-paper question, timed.

Analysis of Financial Statements Previous Year Questions Weightage (2021–2026)

The table shows how the chapter has appeared in recent CBSE and CUET papers. The full list is on the Notes page.

Year

CBSE Board

CUET (Accountancy)

2026

-

-

2025

Comparative Statement of Profit and Loss (6 marks)

Important Formulae for Analysis of Financial Statements

Two formulae drive this chapter: Percentage Change = (Absolute Change / Previous Year Figure) × 100, and Common Size % = (Item / Base) × 100. Base: Revenue from Operations for Profit and Loss; Total Assets for the Balance Sheet.

All NCERT Solutions for Analysis of Financial Statements with Step-by-Step Working

Every NCERT question for this chapter is listed below with a full Solution and Expert Solution in collapsible tabs.

Short Answer Questions

Q 8.1

List the techniques of Financial Statement Analysis.

Concept used.Financial Statement Analysis is the

process of critically evaluating the information in the financial

statements (Balance Sheet, Statement of Profit and Loss, Cash Flow

Statement) to judge a firm's profitability, solvency and operational

efficiency. A technique (or tool) is a standard method used to

turn raw figures into a comparison that means something.

The NCERT chapter lists five commonly used techniques.

Comparative Statements. Statements that show the

profitability and financial position for two or more periods

side by side, with the absolute and percentage change. Also

called horizontal analysis.

Common Size Statements. Statements in which every

item is expressed as a percentage of a common base (revenue

from operations for the Statement of Profit and Loss; total

assets or total of equity and liabilities for the Balance

Sheet). Also called vertical analysis.

Trend Analysis. Studying operational results and

financial position over a series of years by expressing each

year's figure as a percentage of a chosen base year.

Ratio Analysis. Establishing the relationship

between two items of the Balance Sheet and/or the Statement

of Profit and Loss as a ratio, to measure profitability,

solvency and efficiency.

Cash Flow Analysis. Analysing the actual movement

of cash into and out of the business (inflows, outflows and

net cash flow) during an accounting year.

The five techniques are: Comparative Statements, Common Size

Statements, Trend Analysis, Ratio Analysis and Cash Flow Analysis.

AS

Aarav Sharma

M.Com Accounting and Finance, Delhi University

Verified Expert

Quick reading. A "list" question wants a clean enumeration,

not paragraphs, but the marks come from never missing one. The

reliable trick is to remember the five tools by what each one

compares, because every tool is just a different kind of comparison

of the same statement figures.

The five comparisons map one-to-one onto the five tools:

One item, this year vs last year ⇒ Comparative

Statements.

One item, many years vs a fixed base year ⇒

Trend Analysis.

One item vs a common base in the same statement

⇒ Common Size Statements.

One item vs another related item, as a ratio ⇒

Ratio Analysis.

Cash coming in vs cash going out ⇒ Cash Flow

Analysis.

Across time, same firm. Comparative Statements

compare period with period (absolute and percentage change);

Trend Analysis compares many years against one base year

fixed at 100.

Within one statement, structure. Common Size

Statements express each item as a percentage of a common

base (revenue for the P&L, total assets for the Balance

Sheet).

Between two items, relationship. Ratio Analysis

relates one figure to another as a ratio to measure

profitability, solvency and efficiency.

Cash movement. Cash Flow Analysis nets cash

inflows against cash outflows to find the change in cash

position between two balance-sheet dates.

Why this matters. Examiners often follow "list" with

"classify": Comparative and Trend are horizontal analysis;

Common Size and Ratio are vertical analysis; Cash Flow stands

apart as a movement analysis. Knowing this grouping lets you answer

the follow-up without re-reading the chapter.

Common mistakes. Three predictable slips lose marks: (a) computing percentage change on the current-year base rather than the previous-year base in a comparative statement; (b) confusing common-size analysis (each item as a percent of a common base such as Revenue from Operations or Total Assets) with trend analysis (each item as a percent of a chosen base year); (c) discussing limitations in general terms without naming the specific limitation such as ignoring price-level changes or window dressing.

Comparative Statements, Common Size Statements, Trend

Analysis, Ratio Analysis, Cash Flow Analysis.

Q 8.2

Distinguish between Vertical and Horizontal Analysis of financial data.

Concept used.Horizontal analysis compares a single

item across two or more periods to see how it changed over time.

Vertical analysis compares each item within one period

against a common base in that same period, to see its relative size.

The names come from the direction in which the eye moves: across

columns (horizontal) versus down a single column (vertical).

Basis of comparison. Horizontal analysis compares

figures of the current year with those of one or more

previous years. Vertical analysis compares each item with a

common base figure of the same year.

Tools that use it. Horizontal analysis is done

through Comparative Statements and Trend Analysis. Vertical

analysis is done through Common Size Statements and Ratio

Analysis.

Purpose. Horizontal analysis shows the direction and

rate of change over time (is the item growing or shrinking).

Vertical analysis shows the internal structure or proportion

of each item within the statement.

Usefulness. Horizontal analysis suits intra-firm

study over years. Vertical analysis suits inter-firm

comparison even between firms of very different sizes,

because everything is reduced to a percentage.

Horizontal analysis = time-wise comparison of one item

across years (Comparative & Trend). Vertical analysis = same-year

comparison of each item with a common base (Common Size & Ratio).

PM

Priya Mehta

M.Com, Banaras Hindu University

Verified Expert

Structural observation. Picture a financial statement as a

grid of figures. Horizontal analysis reads the grid across

(the same item over several year-columns). Vertical analysis reads

the grid down a single column (each item measured against

that column's base). The whole distinction follows from which

direction the eye moves, which is why the names "horizontal" and

"vertical" were chosen.

A four-line contrast captures everything an exam answer needs:

Basis: horizontal compares across years; vertical

compares within one year against a base.

Tools: horizontal uses Comparative Statements and

Trend Analysis; vertical uses Common Size Statements and

Ratio Analysis.

Output: horizontal yields absolute change and

percentage change; vertical yields a component percentage.

Best use: horizontal tracks one firm's growth over

time; vertical compares firms of unequal size on a common

100 base.

Direction. Row-wise across year-columns

⇒ horizontal. Column-wise top to bottom within

one year ⇒ vertical.

Output. Horizontal gives absolute and percentage

change of each item over time. Vertical gives each item as a

percentage of the period's common base.

Best use. Horizontal is for intra-firm growth

tracking; vertical is for inter-firm comparison even between

firms of very different sizes.

Reconcile the pair. Both analyse the very same

statement figures; they differ only in the direction of

comparison, so a complete analysis usually uses both.

Why this matters. Two firms of unequal size can be laid

side by side only after a common size statement scales both to 100;

a raw comparative statement of unequal firms cannot be compared

directly. That single practical consequence is the point the

examiner is testing.

Common mistakes. Three predictable slips lose marks: (a) computing percentage change on the current-year base rather than the previous-year base in a comparative statement; (b) confusing common-size analysis (each item as a percent of a common base such as Revenue from Operations or Total Assets) with trend analysis (each item as a percent of a chosen base year); (c) discussing limitations in general terms without naming the specific limitation such as ignoring price-level changes or window dressing.

Horizontal = across-time, row-wise (change, via

Comparative and Trend). Vertical = within-year, column-wise

(proportion, via Common Size and Ratio).

Q 8.3

State the meaning of Analysis and Interpretation.

Concept used. The term financial analysis has two

inseparable parts: analysis and interpretation. Analysis

prepares the data; interpretation explains what the prepared data

means. One is useless without the other.

Analysis. Analysis means the simplification of

financial data by a methodical classification of the figures

given in the financial statements. It regroups and rearranges

the raw figures (for example, into comparative or common size

form) so that relationships become visible.

Interpretation. Interpretation means explaining the

meaning and significance of the data so simplified. It draws

conclusions: whether profitability is rising or falling,

whether the firm is becoming more or less solvent, and what

this implies for decision-making.

Why both are needed. Analysis without

interpretation is useless, because numbers alone do not tell

a story. Interpretation without analysis is difficult or even

impossible, because there is nothing organised to interpret.

The two are complementary.

Analysis = methodical simplification and classification of

financial data. Interpretation = explaining the meaning and

significance of that data. They are complementary.

RV

Rohit Verma

M.Com Accountancy, University of Mumbai

Verified Expert

Quick reading. The two words name two stages in a fixed

order: first you do the analysis (arrange the numbers), then

you say the interpretation (explain what the arrangement

means). Answering in that order, and stressing that they are

complementary, is the complete answer.

It helps to map each term to a plain question it answers:

Analysis answers "What do the numbers look like once

organised?" It is mechanical: reclassify, regroup, simplify.

Interpretation answers "So what does that organised

picture mean for the firm?" It is judgemental: strength,

weakness, trend, prospect.

Analysis = the "what". Methodically reclassify and

simplify the statement figures (for example into comparative

or common size form) so patterns and relationships surface.

Interpretation = the "so what". State the

significance of those patterns: is profitability rising,

is solvency improving, what does it predict.

Show the dependence. Analysis without

interpretation is useless (numbers alone tell no story);

interpretation without analysis is impossible (nothing

organised to explain).

Conclude they are complementary. Together they form

the judgemental process that estimates the past, reads the

present and predicts the future.

Why this matters. In a board exam, a comparative statement

submitted with no concluding remark loses every interpretation mark,

because the "interpretation" half of the term was skipped. Always

close a numerical with a one-line "the firm's profitability

improved / declined because ..." comment.

Common mistakes. Three predictable slips lose marks: (a) computing percentage change on the current-year base rather than the previous-year base in a comparative statement; (b) confusing common-size analysis (each item as a percent of a common base such as Revenue from Operations or Total Assets) with trend analysis (each item as a percent of a chosen base year); (c) discussing limitations in general terms without naming the specific limitation such as ignoring price-level changes or window dressing.

Analysis simplifies and classifies the data;

interpretation explains its meaning and significance. They are

complementary and must be done together.

Q 8.4

State the importance of Financial Analysis?

Concept used.Financial analysis identifies the

financial strengths and weaknesses of a firm by establishing

relationships between items of the Balance Sheet and the Statement of

Profit and Loss. Its importance is judged by how many different stakeholders

it serves and the decisions it supports.

Judging operational efficiency. It measures the

success of operations and appraises managerial performance,

helping the finance manager and top management take rational

decisions and exercise financial control.

Assessing short-term solvency. Trade payables use it

to judge the firm's ability to meet short-term obligations,

that is, its liquidity position.

Assessing long-term solvency. Lenders use it to

judge the firm's long-term solvency and survival, its ability

to generate cash, pay interest and repay the principal.

Guiding investment decisions. Investors use it to

analyse present and future profitability and the capital

structure, to decide whether to buy, sell or hold shares.

Other stakeholders. Labour unions use it to support wage

demands; economists, researchers and government agencies use

it for price regulation, taxation and policy.

Financial analysis is important because it reveals strengths

and weaknesses and serves managers, trade payables, lenders,

investors, labour unions and the government in their respective

decisions.

AI

Aditi Iyer

M.Com Finance, University of Madras

Verified Expert

Strategic angle. The cleanest way to answer "importance" is

user by user, because the NCERT explains significance through the

needs of each user group.

Lenders: long-term solvency, interest and principal

repayment.

Investors: profitability and risk for buy / sell /

hold.

Labour unions, economists, government: wage

capacity, economic study, regulation and taxation.

Name the user. Start with the user group (finance

manager, trade payable, lender, investor, labour union,

government).

State the decision. For each, write the single

decision the analysis supports: control and efficiency for

management, short-term liquidity for trade payables,

long-term solvency and repayment ability for lenders,

profitability and risk for investors, wage capacity for

labour unions, regulation and taxation for the government.

Link to the statements. Note that every user reads

the same Balance Sheet and Statement of Profit and Loss; the

analysis differs only because the purpose differs.

Repeat across all groups. Cover every group so no

importance mark is left on the table.

Why this matters. Framing the answer user by user proves to

the examiner that you understand why the same statements are

analysed differently by different parties: the technique chosen

serves the interest of the analyst, so a lender's solvency focus and

an investor's profitability focus draw different conclusions from

identical figures.

Common mistakes. Three predictable slips lose marks: (a) computing percentage change on the current-year base rather than the previous-year base in a comparative statement; (b) confusing common-size analysis (each item as a percent of a common base such as Revenue from Operations or Total Assets) with trend analysis (each item as a percent of a chosen base year); (c) discussing limitations in general terms without naming the specific limitation such as ignoring price-level changes or window dressing.

It supports decisions of every stakeholder: management,

trade payables, lenders, investors, labour unions and government.

Q 8.5

What are Comparative Financial Statements?

Concept used.Comparative Financial Statements are

the Statement of Profit and Loss and the Balance Sheet prepared with

separate columns for the current year, the previous year, and the

change during the year shown both in absolute money terms and in

percentage terms.

What they contain. For each item there are four

figures: the previous year's amount, the current year's

amount, the absolute change, and the percentage change.

How the change is found. The absolute change is the

current year figure minus the previous year figure. The

percentage change is

% change

= Absolute changePrevious year figure× 100 .

Purpose. They show not only the balances on

different dates but also the extent of increase or decrease

between those dates, revealing the direction and trend of

performance.

Other name. Because they compare the same item

across periods, this is a form of horizontal analysis.

Comparative Financial Statements are the Statement of Profit

and Loss and Balance Sheet shown for two periods side by side, with

the absolute and percentage change for every item (horizontal

analysis).

KG

Karan Gupta

M.Com, University of Calcutta

Verified Expert

Picture-first. The fastest way to "define" a comparative

statement is to draw its skeleton. It is always a five-column grid:

Particulars, Previous Year, Current Year, Absolute Change, Percentage

Change. That grid is the comparative statement, and every

exam question simply asks you to fill it.

The two derived columns follow one rule each:

Absolute change= Current Year - Previous Year.

Its sign (or a bracket) shows whether the item rose or fell.

Percentage change=

Absolute changePrevious Year× 100.

The base is always the earlier year.

Columns 2 and 3. Enter the two years' absolute

figures for every item of the Statement of Profit and Loss

or Balance Sheet.

Column 4. Subtract: Column 3 - Column 2, keeping

the sign so a decrease shows as negative or in brackets.

Column 5. Divide Column 4 by Column 2 and multiply

by 100 to get the percentage change.

Read the result. The filled grid shows not just the

balances but the direction and rate of change, which is the

purpose of a comparative statement.

Why this matters. Knowing the five-column layout by heart

means you can build any comparative statement in the exam without

re-deriving the format, and you will never forget the

interpretation column (Column 5) that carries the analysis marks.

Common mistakes. Three predictable slips lose marks: (a) computing percentage change on the current-year base rather than the previous-year base in a comparative statement; (b) confusing common-size analysis (each item as a percent of a common base such as Revenue from Operations or Total Assets) with trend analysis (each item as a percent of a chosen base year); (c) discussing limitations in general terms without naming the specific limitation such as ignoring price-level changes or window dressing.

A two-period side-by-side five-column statement with

absolute and percentage change for each item (horizontal analysis).

Q 8.6

What do you mean by Common Size Statements?

Concept used. A Common Size Statement (also called

a component percentage statement) is a financial statement in which

every item is expressed as a percentage of a common base, so that

statements of different sizes can be compared on a level footing.

The common base. For the Statement of Profit and

Loss the base is revenue from operations, taken as 100. For

the Balance Sheet the base is total assets (or total of

equity and liabilities), taken as 100.

How each item is shown. Each item is converted using

Component %

= Individual itemCommon base× 100 .

Purpose. Because every figure is reduced to a

percentage of a common 100, firms that differ greatly in size

can be compared, and the internal structure of the statements

becomes visible.

Other name. Since each item is compared down the

column against a base of the same year, this is

vertical analysis.

A Common Size Statement expresses each item as a percentage

of a common base (revenue from operations for the P&L; total assets

or total equity and liabilities for the Balance Sheet) to allow

comparison across firms of any size.

SR

Sneha Reddy

M.Com Accountancy, Osmania University

Verified Expert

Strategic angle. The single defining feature of a common

size statement is the common base set to 100. If you state

the correct base for each statement and the conversion formula, the

definition is complete and the purpose follows naturally.

Two facts carry the answer, and both are about the base:

The base is not arbitrary: it is revenue from operations for

the Statement of Profit and Loss, and total assets (equal to

total of equity and liabilities) for the Balance Sheet.

Because every figure is divided by the same base and

multiplied by 100, two firms of very different sizes are

reduced to the same scale and become directly comparable.

P&L base. Revenue from operations = 100; every

expense and profit line is shown as a percentage of it.

Balance Sheet base. Total assets (or total equity

and liabilities) = 100; every asset and liability is shown

as a percentage of it.

Conversion. Each item

= itemcommon base× 100.

Purpose. The resulting percentages reveal the

internal structure of the statement and allow inter-firm and

industry comparison regardless of size (vertical analysis).

Why this matters. The base choice is the single most

examined point in this topic: revenue for the P&L and total assets

for the Balance Sheet, never the other way round. Swapping them is

the most common reason marks are lost here.

Common mistakes. Three predictable slips lose marks: (a) computing percentage change on the current-year base rather than the previous-year base in a comparative statement; (b) confusing common-size analysis (each item as a percent of a common base such as Revenue from Operations or Total Assets) with trend analysis (each item as a percent of a chosen base year); (c) discussing limitations in general terms without naming the specific limitation such as ignoring price-level changes or window dressing.

A statement expressing every item as a % of a common base

(revenue for the P&L; total assets for the Balance Sheet), enabling

size-independent comparison (vertical analysis).

Long Answer Questions

Q 8.7

Describe the different techniques of financial analysis and explain the limitations of financial analysis.

Concept used.Financial analysis uses standard

techniques to convert raw statement figures into meaningful

comparisons; but because it relies entirely on the financial

statements, it inherits their limitations. A full answer has

two parts: the five techniques, then the limitations.

Comparative Statements. Profitability and position

for two or more periods shown side by side with absolute and

percentage change. Reveals the direction and trend of

performance (horizontal analysis).

Common Size Statements. Each item expressed as a

percentage of a common base, allowing comparison of firms of

different sizes (vertical analysis).

Trend Analysis. Each year's figure expressed as a

percentage of a base year over a series of years, to spot

long-run rising, falling or steady patterns.

Ratio Analysis. Relationship between two statement

items expressed as a ratio, measuring profitability, solvency

and efficiency.

Cash Flow Analysis. Study of the actual inflow and

outflow of cash to find the net change in cash position

between two balance sheet dates.

Limitations checklist

Price levels ignored • accounting-policy changes mislead

• only a study of reports • non-monetary factors

ignored • historical, not current, position.

Limitations of financial analysis.

Ignores price level changes. It does not adjust for

inflation, so figures of different years are not strictly

comparable.

Affected by accounting changes. Results can mislead

if the firm changes its accounting procedures and the change

is not known.

Only a study of reports. It analyses only what the

company reports; it cannot reveal what is left out.

Ignores non-monetary factors. Only monetary

information is considered; quality of management, labour

relations and similar factors are not captured.

Based on accounting concepts. Statements rest on

accounting concepts and conventions, so they do not reflect

the current (market) position.

Techniques: Comparative, Common Size, Trend, Ratio and Cash

Flow Analysis. Limitations: ignores price levels, misled by

accounting changes, only a study of reports, ignores non-monetary

factors, and does not show the current position.

VJ

Vivaan Joshi

M.Com Finance, Symbiosis Pune

Verified Expert

Strategic angle. Treat this as two short lists glued

together. Each technique gets one defining sentence; each limitation

gets one cause-and-effect sentence.

Techniques (what they do): Comparative (period vs period),

Common Size (item vs base), Trend (year vs base year), Ratio

(item vs item), Cash Flow (inflow vs outflow).

Limitations (why they weaken the analysis): inflation

ignored, policy changes mislead, only reported data, only

monetary data, historical not current.

List the five techniques. Comparative Statements

(period vs period, with absolute and % change), Common Size

Statements (each item as a % of a common base), Trend

Analysis (each year vs a fixed base year), Ratio Analysis

(one item related to another as a ratio), Cash Flow Analysis

(inflows netted against outflows).

State the five limitations as cause and effect.

Price-level changes ignored, so cross-year figures are not

truly comparable; accounting-policy changes can mislead if

not disclosed; only reported data is analysed; only monetary

information is captured; statements are historical, not

current.

Connect the halves. Point out that the limitations

exist because the techniques operate only on the

reported, historical, monetary statements.

Close. Conclude that financial analysis is helpful

but must always be read with these limitations in mind.

Why this matters. Examiners reward the student who connects

the two halves rather than listing them in isolation: the

limitations are not a separate topic, they are the direct

consequence of the very data the techniques are confined to.

Common mistakes. Three predictable slips lose marks: (a) computing percentage change on the current-year base rather than the previous-year base in a comparative statement; (b) confusing common-size analysis (each item as a percent of a common base such as Revenue from Operations or Total Assets) with trend analysis (each item as a percent of a chosen base year); (c) discussing limitations in general terms without naming the specific limitation such as ignoring price-level changes or window dressing.

Five techniques (Comparative, Common Size, Trend, Ratio,

Cash Flow) and five limitations (price levels, accounting changes,

report-only, non-monetary ignored, not current position).

Q 8.8

Explain the usefulness of trend percentages in interpretation of financial performance of a company.

Concept used.Trend analysis studies operational

results and financial position over a series of years. A

trend percentage expresses each year's figure of an item as

a percentage of that same item in a chosen base year, computed

as

Trend %

= Figure of the given yearFigure of the base year× 100 .

The base year itself is therefore always 100.

Long-run view. By looking at many years at once,

trend percentages take a long-run view that may point to

basic changes in the nature of the business that a single

year cannot show.

Direction of change. By watching a particular item

or ratio, one can see whether it is rising, falling or

staying relatively constant over time.

Early signals. From this direction a problem can be

detected early, or the sign of good or poor management can be

read, before it shows up sharply in absolute figures.

Simple comparison. Because every year is scaled

against the base year's 100, comparing performance across

many years becomes simple and quick.

Forecasting aid. A consistent trend supports a

reasonable forecast of future performance, useful for

planning and for investors.

Trend percentages give a long-run, base-year-scaled view

that shows the direction of change, gives early signals of good or

poor management, makes multi-year comparison simple, and supports

forecasting.

AN

Ananya Nair

M.Com Accountancy, University of Kerala

Verified Expert

Picture-first. Imagine plotting one item, say sales, for ten

years with the first year fixed at 100. The shape of that line, its

slope and its turning points, is exactly what trend analysis reads.

Everything useful about trend percentages follows from that mental

graph.

The graph metaphor unpacks into four concrete benefits:

A long line shows the long-run direction that a single

year's figure cannot reveal.

The slope tells whether the item is rising, falling or flat.

A change in slope is an early signal of good or poor

management, well before absolute figures react sharply.

Because every point is scaled to the base 100, comparing ten

years is as easy as comparing two.

Fix the base year at 100. Choose a representative

year as the base; its trend percentage is always 100.

Scale every later year. Compute

that year's figurebase year figure× 100

for each subsequent year.

Read the slope. Rising, falling or flat tells the

story of the business over the long run.

Use it to forecast. A consistent slope supports a

reasonable projection of the next period, which is the

planning value of the tool.

Why this matters. A rising sales trend paired with a

faster-rising cost trend warns of shrinking margins long before

profit actually turns negative. That early-warning property, read

straight off the scaled line, is the interpretation value examiners

want you to state explicitly.

Common mistakes. Three predictable slips lose marks: (a) computing percentage change on the current-year base rather than the previous-year base in a comparative statement; (b) confusing common-size analysis (each item as a percent of a common base such as Revenue from Operations or Total Assets) with trend analysis (each item as a percent of a chosen base year); (c) discussing limitations in general terms without naming the specific limitation such as ignoring price-level changes or window dressing.

Trend percentages reveal long-run direction, give early

warnings of good or poor management, simplify multi-year comparison

and support forecasting.

Q 8.9

What is the importance of comparative statements? Illustrate your answer with particular reference to comparative income statement.

Concept used. A Comparative Statement shows each

item for two periods together with its absolute and percentage change.

A Comparative Income Statement (comparative Statement of

Profit and Loss) applies this to revenue, expenses and profit.

Shows change clearly. It shows not just the balances

of two years but the exact increase or decrease between them,

in both rupees and percentage.

Reveals direction and trend. It tells whether

revenue, expenses and profit are moving up or down and how

fast, indicating the direction of performance.

Helps in interpretation. By comparing the

percentage change in revenue with the percentage change in

expenses, one can judge whether profitability is improving.

Aids decision-making. Management, investors and

lenders use the visible changes to take operating, investment

and lending decisions.

Illustration (Comparative Income Statement).

1.35

tabularlrrrr

Particulars & Year 1 & Year 2 & Abs. change & % change

Here revenue rose 25% while expenses rose only 10%, so profit before

tax jumped 50%. The comparative income statement makes this

favourable structural change immediately visible: a result no single

year's statement could show.

Comparative statements show the absolute and percentage

change between two periods, reveal direction and trend, support

interpretation and decision-making; a comparative income statement

shows, for example, profit rising 50% because revenue grew faster

(25%) than expenses (10%).

ID

Ishaan Desai

M.Com Finance, Gujarat University

Verified Expert

Strategic angle. The word "illustrate" is the instruction

that matters. State the importance in crisp points, then immediately

prove each point with a tiny three-line income statement so

the examiner sees the concept applied, not merely defined.

The importance reduces to four points, each of which the

illustration must visibly demonstrate:

It shows the exact change between two years in rupees and

percentage.

It reveals the direction and trend of revenue, expenses and

profit.

It supports interpretation by letting you compare the %

change in revenue with the % change in expenses.

It aids decisions of management, investors and lenders.

State the importance. Visible change, direction and

trend, interpretation support, decision support.

Set up the illustration. Take revenue

16,00,000 → 20,00,000 and expenses

10,00,000 → 11,00,000 for two years.

Compute the changes. Revenue

4,00,00016,00,000× 100 = +25%;

expenses

1,00,00010,00,000× 100 = +10%;

profit before tax

3,00,0006,00,000× 100 = +50%.

Read the story. Revenue grew faster than expenses,

so profit jumped 50%, a structural improvement no single

year's statement could show.

Why this matters. A worded definition with no numbers caps

your marks on an "illustrate" question; the small worked example

that turns the definition into a visible 50% profit jump is exactly

what secures full credit.

Common mistakes. Three predictable slips lose marks: (a) computing percentage change on the current-year base rather than the previous-year base in a comparative statement; (b) confusing common-size analysis (each item as a percent of a common base such as Revenue from Operations or Total Assets) with trend analysis (each item as a percent of a chosen base year); (c) discussing limitations in general terms without naming the specific limitation such as ignoring price-level changes or window dressing.

Importance: visible change, trend, interpretation and

decision support, illustrated by profit before tax rising 50% when

revenue (+25%) outgrew expenses (+10%).

Q 8.10

What do you understand by analysis and interpretation of financial statements? Discuss its importance.

Concept used.Analysis and interpretation of

financial statements is the process of critically evaluating the

information in the financial statements to understand the firm and

make decisions about its operations. Analysis simplifies and

classifies the data; interpretation explains its meaning.

Meaning of analysis. It is the methodical

classification and simplification of the figures in the

financial statements so that relationships between them

become clear.

Meaning of interpretation. It is explaining the

meaning and significance of the simplified data: judging

profitability, solvency and operational efficiency, and the

firm's future prospects.

They are complementary. Analysis without

interpretation is useless; interpretation without analysis is

almost impossible. Together they form a judgemental process

that estimates past and present position and predicts the

future.

Importance.

Assesses current profitability and operational efficiency of

the firm and its departments, so the financial health can be

judged.

Ascertains the relative importance of the different

components of the financial position.

Identifies the reasons for changes in profitability or

financial position.

Judges the firm's ability to repay debt and assesses

short-term and long-term liquidity.

Serves owners, lenders, investors, trade payables, employees

and government in their respective decisions.

Analysis = simplifying and classifying statement data;

interpretation = explaining its significance. Together they assess

profitability, the structure of the financial position, reasons for

change, debt-paying ability and serve every user's decisions.

DB

Diya Banerjee

M.Com Accountancy, Jadavpur University

Verified Expert

Quick reading. This is a two-part question hiding in one

sentence: first define the analysis-interpretation pair, then

discuss its importance. The discussion half carries most of

the marks, so keep the definition tight and spend the rest on the

objectives.

The importance is best given as the four NCERT objectives plus the

user dimension:

Assess current profitability and operational efficiency to

judge financial health.

Ascertain the relative importance of the components of the

financial position.

Identify the reasons for changes in profitability or

position.

Judge debt-paying ability and short- and long-term

liquidity, serving owners, lenders, investors and others.

Define the pair. Analysis simplifies and classifies

the figures; interpretation explains their significance;

they are complementary.

List the four objectives.

profitability/efficiency, relative importance of components,

reasons for change, debt-paying ability.

Add the user dimension. Note that owners, lenders,

investors, trade payables and government each rely on this

analysis for their own decisions.

Conclude. The pair together forms the judgemental

process that reads the past and present and predicts the

future.

Why this matters. The verb "discuss" expects the objectives

spelled out, not just the meaning of the two words. Stopping at the

definition is the single most common reason marks are lost on this

question.

Common mistakes. Three predictable slips lose marks: (a) computing percentage change on the current-year base rather than the previous-year base in a comparative statement; (b) confusing common-size analysis (each item as a percent of a common base such as Revenue from Operations or Total Assets) with trend analysis (each item as a percent of a chosen base year); (c) discussing limitations in general terms without naming the specific limitation such as ignoring price-level changes or window dressing.

Definition of the complementary pair plus the four NCERT

objectives and the multi-user importance.

Q 8.11

Explain how common size statements are prepared giving an example.

Concept used. A Common Size Statement expresses

each item as a percentage of a common base. The base is revenue from

operations for the Statement of Profit and Loss, and total assets (or

total of equity and liabilities) for the Balance Sheet. The

conversion is

Component %

= Individual itemCommon base× 100 .

List absolute figures. Write the absolute rupee

figures of all items for the period(s) under study.

Choose the common base as 100. Revenue from

operations for the P&L; total assets or total equity and

liabilities for the Balance Sheet.

Work out each percentage. For every item, divide it

by the base and multiply by 100, and record the percentage

in a separate column.

Example (Common Size Statement of Profit and Loss).

Let revenue from operations be 10,00,000 and cost of

revenue from operations be 6,00,000.

Base = revenue from operations = 10,00,000 = 100%.

Cost of revenue from operations

= 6,00,00010,00,000× 100 = 60%.

Revenue from operations & 10,00,000 & 100

Less: Cost of revenue from operations & 6,00,000 & 60

Gross profit & 4,00,000 & 40

tabular

Steps: list absolute figures, fix the common base as 100,

express each item as a % of that base. Example: with revenue

10,00,000 (100%) and cost 6,00,000 (60%),

gross profit is 4,00,000 (40%).

YK

Yash Kapoor

M.Com Finance, University of Pune

Verified Expert

Strategic angle. A "how to prepare, with an example"

question is graded in two halves: the procedure and the worked

illustration. State the three preparation steps crisply, then build

a two or three line table so each step is visibly applied to real

numbers.

The procedure is exactly three steps, and the example must show all

three in action:

List the absolute figures for the period.

Fix the common base at 100 (revenue for the P&L; total

assets for the Balance Sheet).

Convert every item using

itembase× 100.

State the three steps. List absolute figures, set

the common base to 100, compute each item as

item/base× 100.

Choose the base. Take revenue from operations

= 10,00,000 as the base (= 100%).

Apply to cost.6,00,00010,00,000× 100 = 60%, so

cost of revenue is 60% of revenue.

Apply to gross profit.10,00,000 - 6,00,000 = 4,00,000, i.e.

4,00,00010,00,000× 100 = 40%, and

present the three lines as a small common size table.

Why this matters. The example is what separates a 4-mark

and a 6-mark answer here: a procedure stated without a worked table

is treated as incomplete, because the question explicitly asked for

an illustration.

Common mistakes. Three predictable slips lose marks: (a) computing percentage change on the current-year base rather than the previous-year base in a comparative statement; (b) confusing common-size analysis (each item as a percent of a common base such as Revenue from Operations or Total Assets) with trend analysis (each item as a percent of a chosen base year); (c) discussing limitations in general terms without naming the specific limitation such as ignoring price-level changes or window dressing.

Three steps plus a worked table: cost 60%, gross profit

40% on a revenue base of 100%.

Numerical Questions

Q 8.12

Following are the balance sheets of Alpha Ltd., as at March 31, 2016 and 2017. You are required to prepare a Comparative Balance Sheet. [3pt]

Equity & Liabilities: Share Capital 2,00,000 / 4,00,000; Reserve & Surplus 1,00,000 / 1,50,000; Long Term Borrowings 2,00,000 / 3,00,000; Short term borrowings 50,000 / 70,000; Trade Payables 30,000 / 60,000; Other Current Liabilities 20,000 / 10,000; Short Term Provisions 20,000 / 20,000; Total 6,20,000 / 10,20,000. Assets: Fixed Assets 2,00,000 / 5,00,000; Non-Current Investments 1,00,000 / 1,25,000; Current Investments 60,000 / 80,000; Inventories 1,35,000 / 1,55,000; Trade Receivables 60,000 / 90,000; Cash and Cash Equivalents 25,000 / 10,000; Short term Loans & Advances 40,000 / 60,000; Total 6,20,000 / 10,20,000.

Concept used. A Comparative Balance Sheet shows

each item for both years with the absolute change and the percentage

change. For every line:

Absolute change = Figure2017 - Figure2016,

% change

= Absolute changeFigure2016× 100 .

A bracket or minus sign denotes a decrease.

Sign rule

Increase ⇒ positive. Decrease ⇒ shown with a

minus sign or in brackets. The base of the percentage is always the

earlier year (2016).

Note for editor: The 2017 Equity & Liabilities column of the

NCERT question adds to 10,10,000, while the textbook

prints the total as 10,20,000 (a known textbook

misprint, consistent across Shaalaa, learncbse and BYJU'S). The

NCERT-printed total of 10,20,000 has been retained, as

the asset side independently totals 10,20,000.

Comparative Balance Sheet prepared. Total of equity and

liabilities (and of assets) rises from 6,20,000 to

10,20,000, an increase of 4,00,000

(+64.52%). Fixed assets show the steepest rise (+150%); cash

falls 60%.

PS

Pranav Singh

M.Com Accountancy, University of Delhi

Verified Expert

Strategic angle. Instead of treating fifteen lines as

fifteen unrelated sums, group them into four economic blocks:

owners' funds, borrowed funds, fixed-side assets and working-capital

assets. Apply the same two formulas to every line, and read each

block as a story. The two formulas are, for every line,

Abs.=Figure2017-Figure2016 and

%=Abs.Figure2016× 100.

Owners' funds block. Share capital:

4,00,000 - 2,00,000 = +2,00,000, so

2,00,0002,00,000× 100 = +100%.

Reserve & surplus:

1,50,000 - 1,00,000 = +50,000, so

50,0001,00,000× 100 = +50%.

Total owners' funds rose from 3,00,000 to

5,50,000: the owners injected fresh money.

Borrowed funds block. Long-term borrowings

3,00,000 - 2,00,000 = +1,00,000 (+50%);

short-term borrowings 70,000 - 50,000 = +20,000

(+40%); trade payables

60,000 - 30,000 = +30,000 (+100%); other current

liabilities 10,000 - 20,000 = -10,000 (-50%);

provisions unchanged (0%). Borrowing rose but less than

owners' funds.

Fixed-side assets block. Fixed assets

5,00,000 - 2,00,000 = +3,00,000

(3,00,0002,00,000× 100 = +150%);

non-current investments

1,25,000 - 1,00,000 = +25,000 (+25%). Most of

the new money went into fixed assets.

Working-capital assets block. Current investments

+20,000 (+33.33%); inventories +20,000

(20,0001,35,000× 100 = +14.81%);

trade receivables +30,000 (+50%); cash

10,000 - 25,000 = -15,000 (-60%); short-term

loans & advances +20,000 (+50%). Cash is the only

line that fell sharply.

Reconcile the totals. Add the figures: the

NCERT-printed totals are 6,20,000 and 10,20,000,

giving +4,00,000 and

4,00,0006,20,000× 100 = +64.52% on

each side, so the statement balances. (The 2017 liability

column's arithmetic slip to 10,10,000 is the known

textbook misprint noted above.)

Why this matters. The structure tells the real story: a

+150% jump in fixed assets was financed mainly by fresh owners'

funds and long-term debt, not by squeezing cash or short-term

sources. That is a healthy, well-funded expansion, the one-line

interpretation an examiner rewards.

Common mistakes. Three predictable slips lose marks: (a) computing percentage change on the current-year base rather than the previous-year base in a comparative statement; (b) confusing common-size analysis (each item as a percent of a common base such as Revenue from Operations or Total Assets) with trend analysis (each item as a percent of a chosen base year); (c) discussing limitations in general terms without naming the specific limitation such as ignoring price-level changes or window dressing.

Same Comparative Balance Sheet; both totals

6,20,000 → 10,20,000, +64.52%, expansion led by fixed

assets (+150%) funded by capital (+100%) and long-term debt

(+50%); cash the only sharp fall (-60%).

Q 8.13

Following are the Balance Sheets of Beta Ltd., as at March 31, 2016 and 2017. Prepare comparative Balance Sheet. [3pt]

Equity & Liabilities: Share Capital 4,00,000 / 3,00,000; Reserves and surplus 1,50,000 / 1,00,000; Long term borrowings (IDBI) 3,00,000 / 1,00,000; Short term borrowings 70,000 / 50,000; Trade payables 60,000 / 30,000; Other current liabilities 1,10,000 / 1,00,000; Short term provisions 10,000 / 20,000; Total 11,00,000 / 7,00,000. Assets: Fixed Assets 4,00,000 / 2,20,000; Non-current Investments 2,25,000 / 1,00,000; Current Investments 80,000 / 60,000; Inventories 1,05,000 / 90,000; Trade Receivables 90,000 / 60,000; Cash and Cash Equivalents 1,00,000 / 85,000; Short term loans & Advances 1,00,000 / 85,000; Total 11,00,000 / 7,00,000.

Concept used. Same as the previous question. For every line,

absolute change = Figure2017 - Figure2016 and

% change = Absolute changeFigure2016× 100.

Here almost every figure falls, so most signs are negative.

Note for editor: The NCERT prints the 2016 total of equity

and liabilities as 1,10,000; this is a typographical

slip for 11,00,000 (the asset side and the 2017 column

both confirm 11,00,000). The corrected

11,00,000 has been used so both sides reconcile.

Comparative Balance Sheet prepared. Almost every item

contracted: the total fell from 11,00,000 to

7,00,000, a decrease of 4,00,000

(-36.36%). Only short-term provisions rose (+100%).

MC

Meera Chatterjee

M.Com Finance, University of Calcutta

Verified Expert

Structural observation. This is the mirror image of Alpha

Ltd: nearly every line shrinks, so the discipline is to carry the

minus sign consistently and always divide by the larger 2016 base.

Read it block by block, computing each figure in full so no sign

slips.

Owners' funds block. Share capital:

3,00,000 - 4,00,000 = -1,00,000, so

-1,00,0004,00,000× 100 = -25%.

Reserves and surplus:

1,00,000 - 1,50,000 = -50,000, so

-50,0001,50,000× 100 = -33.33%.

Owners' funds fell from 5,50,000 to 4,00,000.

The lone increase. Short-term provisions

20,000 - 10,000 = +10,000, so

10,00010,000× 100 = +100%: the only

line that grew.

Fixed-side assets block. Fixed assets

2,20,000 - 4,00,000 = -1,80,000 (-45%);

non-current investments

1,00,000 - 2,25,000 = -1,25,000

(-1,25,0002,25,000× 100 = -55.56%):

the deepest cuts, meaning assets were sold off.

Working-capital assets block. Current investments

-20,000 (-25%); inventories -15,000

(-14.29%); trade receivables -30,000 (-33.33%);

cash -15,000 (-15%); short-term loans & advances

-15,000 (-15%). Every working-capital line also

shrank.

Reconcile the totals. Both sides move

11,00,000 → 7,00,000, so absolute change

= -4,00,000 and

-4,00,00011,00,000× 100 = -36.36%.

The corrected 2016 figure of 11,00,000 (not the

misprinted 1,10,000) makes both sides tie.

Why this matters. A balance sheet that contracts on every

front, with long-term borrowings down two-thirds and fixed assets

down nearly half, points to a firm winding down or sharply

downsizing operations. Stating that single interpretation, backed by

the -66.67% debt figure, is what secures the analysis mark.

Common mistakes. Three predictable slips lose marks: (a) computing percentage change on the current-year base rather than the previous-year base in a comparative statement; (b) confusing common-size analysis (each item as a percent of a common base such as Revenue from Operations or Total Assets) with trend analysis (each item as a percent of a chosen base year); (c) discussing limitations in general terms without naming the specific limitation such as ignoring price-level changes or window dressing.

Same Comparative Balance Sheet; total contracts

11,00,000 → 7,00,000 (-36.36%); owners' funds, debt

and all assets fall, only short-term provisions rise (+100%).

Q 8.14

Prepare Comparative Statement of profit and loss from the following information. [3pt]

2015-16 / 2016-17: Freight Outward 20,000 / 10,000; Wages (office) 10,000 / 5,000; Manufacturing Expenses 50,000 / 20,000; Stock adjustment (60,000) / 30,000; Cash purchases 80,000 / 60,000; Credit purchases 60,000 / 20,000; Return inward 8,000 / 4,000; Gross profit (30,000) / 90,000; Carriage outward 20,000 / 10,000; Machinery 3,00,000 / 2,00,000; 10% depreciation on machinery 10,000 / 5,000; Interest on short-term loans 20,000 / 20,000; 10% debentures 20,000 / 10,000; Profit on sale of furniture 20,000 / 10,000; Loss on sale of office car 90,000 / 60,000; Tax rate 40% / 50%.

Concept used. A Comparative Statement of Profit and

Loss (in the NCERT/Schedule III format) lists every item under

Revenue, Expenses, Profit before tax and Profit after tax with an

absolute change and a percentage change column. The data are scattered,

so we must first derive Revenue from Operations and classify every item.

The two key relations are:

Revenue from Operations (Net Sales)= Purchases + Manufacturing Expenses + Change in

Inventory + Gross Profit - Sales Return.

Profit before tax= Total Revenue - Total

Expenses (Total Revenue = Revenue from Operations + Other

Income).

Machinery is a balance sheet item (not a P&L line); the depreciation

figure is given directly ( 10,000/ 5,000), so we

use it as printed. Freight outward, carriage outward and loss on sale

of office car are grouped under Other Expenses.

Change in Inventories. The "stock adjustment" line

is the closing-less-opening change (a positive figure reduces

cost, a negative figure raises it). 2015-16: (60,000);

2016-17: 30,000. Change = +90,000 (base is negative,

so the percentage is n/a).

Profit before Tax= Total Revenue - Total

Expenses.

2015-16: 1,12,000 - 2,52,000 = -1,40,000 (loss).

2016-17: 2,26,000 - 2,21,000 = +5,000.

Change = +1,45,000 (turnaround from loss to profit).

Tax. 2015-16 PBT is a loss, so tax is nil.

2016-17: 50% × 5,000 = 2,500.

Change = +2,500.

1. Revenue from Operations & 92,000 & 2,16,000 & +1,24,000 & +134.78

2. Other Income & 20,000 & 10,000 & -10,000 & -50.00 3. Total Revenue (1+2) & 1,12,000 & 2,26,000 & +1,14,000 & +101.79

5l4. Expenses

a. Purchases of Stock-in-Trade & 1,40,000 & 80,000 & -60,000 & -42.86

b. Change in Inventories & (60,000) & 30,000 & +90,000 & n/a

c. Employee Benefit Expenses & 10,000 & 5,000 & -5,000 & -50.00

d. Finance Costs & 22,000 & 21,000 & -1,000 & -4.55

e. Depreciation & Amort. & 10,000 & 5,000 & -5,000 & -50.00

f. Other Expenses & 1,30,000 & 80,000 & -50,000 & -38.46 Total Expenses & 2,52,000 & 2,21,000 & -31,000 & -12.30 5. Profit before Tax (3-4) & (1,40,000) & 5,000 & +1,45,000 & n/a

Less: Income Tax & nil & 2,500 & +2,500 & n/a 6. Profit after Tax & (1,40,000) & 2,500 & +1,42,500 & n/a

tabular

Comparative Statement of Profit and Loss prepared. Revenue

from operations rose 92,000 → 2,16,000

(+134.78%). The firm turned around from a loss after tax of

(1,40,000) in 2015-16 to a profit of 2,500 in

2016-17, an improvement of 1,42,500.

SR

Siddharth Rao

M.Com Accountancy, University of Hyderabad

Verified Expert

Strategic angle. The figures are scattered on purpose to

test classification. The safe method is to first derive Revenue from

Operations using the trading-account identity, then build the

Statement of Profit and Loss in the Schedule III ladder

(Revenue → Other income → Total revenue → Expenses by

nature → PBT → Tax → PAT), computing each figure fully

before attaching the change columns.

Classify the stray items. Wages (office) →

Employee Benefit Expenses (10,000 / 5,000). Freight

Outward + Carriage Outward + Loss on sale of office car

→ Other Expenses (1,30,000 / 80,000). Profit on

sale of furniture → Other Income (20,000 / 10,000).

Interest on short-term loans + 10% debenture interest

(2,000 / 1,000) → Finance Costs (22,000 /

21,000). Depreciation given directly (10,000 / 5,000);

Machinery is a balance-sheet item, not a P&L line.

Total Revenue and Total Expenses.

Total revenue: 1,12,000 / 2,26,000. Total expenses

= Purchases + Stock-adj inventory change + Wages +

Finance + Dep + Other.

2015-16: 1,40,000 + (-60,000) + 10,000 + 22,000 +

10,000 + 1,30,000 = 2,52,000.

2016-17: 80,000 + 30,000 + 5,000 + 21,000 + 5,000

+ 80,000 = 2,21,000.

Stack to PAT. PBT = Total Revenue - Total

Expenses.

2015-16: 1,12,000 - 2,52,000 = -1,40,000 (loss,

so tax nil; PAT = -1,40,000).

2016-17: 2,26,000 - 2,21,000 = +5,000; tax =

50% × 5,000 = 2,500; PAT = 5,000 - 2,500 =

2,500. Change in PAT = +1,42,500 (turnaround from

loss to profit).

Change column rule. Use absolute change everywhere;

mark PBT, PAT and the Change-in-Inventories lines "n/a" for

percentage because their 2015-16 base is negative or signed

(a percentage on a negative or zero base is undefined).

Cross-check the turnaround. Revenue more than

doubled (92,000 → 2,16,000, +134.78%); other

expenses fell sharply ( 1,30,000→80,000, -38.46%); together they flipped the

bottom line from a 1,40,000 loss to a small

profit of 2,500, an exact 1,42,500

swing, confirming the statement is internally consistent.

Why this matters. The two single most common errors are

(i) putting the loss on sale of the office car above gross profit

when it is a non-operating "Other Expense", and (ii) forgetting to

subtract Returns Inward ( 8,000 / 4,000) when deriving

Net Sales. Either slip collapses every downstream figure, so the

classification step is where the marks are won or lost.

Common mistakes. Three predictable slips lose marks: (a) computing percentage change on the current-year base rather than the previous-year base in a comparative statement; (b) confusing common-size analysis (each item as a percent of a common base such as Revenue from Operations or Total Assets) with trend analysis (each item as a percent of a chosen base year); (c) discussing limitations in general terms without naming the specific limitation such as ignoring price-level changes or window dressing.

Same comparative statement: Revenue from Operations

92,000 → 2,16,000 (+134.78%); PAT swings

from (1,40,000) to 2,500, a

1,42,500 improvement; tax 2,500 only in

2016-17.

Q 8.15

Prepare Comparative Statement of Profit and Loss from the following information: [3pt]

2015-16 / 2016-17: Manufacturing expenses 35,000 / 80,000; Opening stock 30,000 / (60% of closing stock); Sales 9,60,000 / 4,50,000; Returns outward 4,000 (out of credit purchase) / 6,000 (out of cash purchase); Closing stock 150% of opening / 1,00,000; Credit purchases 1,50,000 / 150% of cash purchase; Cash purchases 80% of credit purchases / 40,000; Carriage outward 10,000 / 30,000; Depreciation on building 20% / 10% (building 1,00,000 / 2,00,000); Interest on bank overdraft 5,000 / nil; 10% debentures 2,00,000 / 20,00,000; Profit on sale of copyright 10,000 / 20,000; Loss on sale of personal car 10,000 / 20,000; Other operating expenses 20,000 / 10,000; Tax rate 50% / 40%.

Concept used. As in Q14, first resolve every relational

clue into a number, build the Statement of Profit and Loss, then add

the change columns. Key relations:

Net purchases= (cash + credit purchases) -

returns outward.

Cost of revenue from operations= opening stock

+ net purchases + manufacturing expenses - closing

stock.

Loss on sale of a personal car is a personal (not

business) item and is excluded from the company's

Statement of Profit and Loss.

Indirect / operating expenses= carriage outward + depreciation on building + other

operating expenses.

Depreciation: 2015-16 = 20% of 1,00,000 = 20,000;

2016-17 = 10% of 2,00,000 = 20,000.

Total: 2015-16 = 10,000 + 20,000 + 20,000 = 50,000;

2016-17 = 30,000 + 20,000 + 10,000 = 60,000.

Add other income, less finance cost.

Other income = profit on sale of copyright

(10,000 / 20,000). Finance cost = interest on bank

overdraft (5,000 / 0) + interest on 10% debentures

(10% of 2,00,000 / 20,00,000 = 20,000 /

2,00,000). Loss on sale of personal car is

excluded.

Comparative Statement of Profit and Loss prepared. Sales

fell 9,60,000 → 4,50,000 (-53.13%)

and profit after tax fell 3,04,500 →

45,600 (-85.02%), worsened by a sharp rise in finance

cost on the enlarged 10% debentures.

TP

Tara Pillai

M.Com Finance, University of Kerala

Verified Expert

Strategic angle. Every "X% of Y" clue must be converted

into a rupee figure before any statement can be built. Resolve the

stock and purchase relations first, then feed them into the standard

ladder, computing each line in full.

Open the stock relations.

2015-16 closing stock = 150% of opening

= 1.5 × 30,000 = 45,000.

2016-17 opening stock = 60% of closing

= 0.6 × 1,00,000 = 60,000 (closing given as

1,00,000).

Open the purchase relations.

2015-16: credit = 1,50,000, cash = 80% of credit

= 0.8 × 1,50,000 = 1,20,000.

2016-17: cash = 40,000, credit = 150% of cash

= 1.5 × 40,000 = 60,000.

Drop the personal car loss. Loss on sale of a

personal car is not a business expense (business

entity concept); exclude it entirely before computing PBT.

Stack to PAT. Indirect expenses

50,000 / 60,000; other income 10,000 / 20,000;

finance cost 25,000 / 2,00,000 (bank overdraft

interest plus 10% debenture interest, which is

20,000 / 2,00,000). PBT

= 6,09,000 / 76,000; tax at 50% / 40%= 3,04,500 / 30,400; PAT

= 3,04,500 / 45,600. Change in PAT

= -2,58,900,

-2,58,9003,04,500× 100 = -85.02%.

Cross-check the collapse. Confirm the figures

cohere: sales fell roughly 53%, which alone would cut

profit, but profit fell far more steeply (85%). The extra

damage is the finance cost rising from 25,000 to

2,00,000, an 1,75,000 jump that

almost exactly equals the missing profit. This sanity check

confirms the debenture expansion, not just lower sales,

drove the result.

Why this matters. The 10% debentures balloon from

2,00,000 to 20,00,000, so debenture

interest jumps from 20,000 to 2,00,000.

That single finance-cost surge is why profit collapsed even though

the firm stayed profitable: stating this is the interpretation mark.

Common mistakes. Three predictable slips lose marks: (a) computing percentage change on the current-year base rather than the previous-year base in a comparative statement; (b) confusing common-size analysis (each item as a percent of a common base such as Revenue from Operations or Total Assets) with trend analysis (each item as a percent of a chosen base year); (c) discussing limitations in general terms without naming the specific limitation such as ignoring price-level changes or window dressing.

Same statement: sales -53.13%; PAT

3,04,500 → 45,600 (-85.02%), driven by

a tenfold rise in debenture interest; personal car loss excluded.

Q 8.16

Prepare a Common size statement of profit and loss of Shefali Ltd. with the help of following information: [3pt]

2015-16 / 2016-17: Revenue from operations 6,00,000 / 8,00,000; Cost of revenue from operations 4,28,000 / 7,28,000; Indirect expense 25% of gross profit / 25% of gross profit; Other incomes 10,000 / 12,000; Income tax 30% / 30%.

Concept used. In a Common Size Statement of Profit

and Loss, revenue from operations is the common base, taken as

100%, and every other item is shown as

% of revenue

= ItemRevenue from operations× 100 .

Convert each to % of revenue (base

6,00,000 and 8,00,000). For example, cost of

revenue 2015-16:

4,28,0006,00,000× 100 = 71.33%;

2016-17:

7,28,0008,00,000× 100 = 91.00%.

Common Size Statement of Profit and Loss prepared. Profit

after tax fell from 16.22% of revenue (2015-16) to 5.78%

(2016-17), mainly because cost of revenue rose from 71.33% to

91.00% of revenue.

AB

Aditya Bhat

M.Com Accountancy, University of Mumbai

Verified Expert

Picture-first. Treat each year's revenue as a fixed bar of

length 100. The whole question is: how much of that bar does cost

eat, and how much survives as profit? Build every figure first, then

scale.

Tax and PAT. Tax = 30% of PBT

= 41,700 / 19,800; PAT

= 1,39,000 - 41,700 = 97,300 and

66,000 - 19,800 = 46,200.

Scale every line to revenue. Divide each figure by

its year's revenue and multiply by 100. Cost of revenue:

4,28,0006,00,000× 100 = 71.33% and

7,28,0008,00,000× 100 = 91.00%.

PAT: 97,3006,00,000× 100 = 16.22% and

46,2008,00,000× 100 = 5.78%.

Why this matters. Revenue grew in rupees, yet the

cost-to-revenue ratio leapt from 71.33% to 91%, crushing the

profit margin from 16.22% to 5.78%. Common size analysis

exposes this structural slide where a comparative statement might

hide it behind a rising rupee revenue; stating that contrast is the

interpretation mark.

Common mistakes. Three predictable slips lose marks: (a) computing percentage change on the current-year base rather than the previous-year base in a comparative statement; (b) confusing common-size analysis (each item as a percent of a common base such as Revenue from Operations or Total Assets) with trend analysis (each item as a percent of a chosen base year); (c) discussing limitations in general terms without naming the specific limitation such as ignoring price-level changes or window dressing.

Same common size statement: PAT margin slides

16.22% → 5.78% because cost-to-revenue climbs

71.33% → 91%.

Q 8.17

Prepare a Common Size balance sheet from the following balance sheet of Aditya Ltd., and Anjali Ltd.: [3pt]

Aditya Ltd. / Anjali Ltd.: Equity share capital 6,00,000 / 8,00,000; Reserves and surplus 3,00,000 / 2,50,000; Current liabilities 1,00,000 / 1,50,000; Total 10,00,000 / 12,00,000. Fixed assets 4,00,000 / 7,00,000; Current assets 6,00,000 / 5,00,000; Total 10,00,000 / 12,00,000.

Concept used. In a Common Size Balance Sheet, the

total of the balance sheet (total of equity and liabilities, equal to

total assets) is the common base, taken as 100%, and every item is

shown as

% of total

= ItemBalance sheet total× 100 .

Here it is an inter-firm comparison, so Aditya Ltd is scaled

on its own total ( 10,00,000) and Anjali Ltd on its own

total ( 12,00,000).

Common Size Balance Sheet prepared. Aditya Ltd is

current-asset heavy (60% of total) while Anjali Ltd is fixed-asset

heavy (58.33%); Anjali relies more on share capital (66.67% vs

60%).

SK

Sanya Kapoor

M.Com Finance, University of Pune

Verified Expert

Structural observation. Two firms of unequal size can be

compared only after both are scaled to a common 100. The base for

each firm is its own balance-sheet total, so divide every line by

that firm's total and the two structures line up directly.

Fix the bases. Aditya's total

= 10,00,000; Anjali's total = 12,00,000. Each

firm is scaled against its own total, never the

other's.

Liabilities side. Equity share capital:

6,00,00010,00,000× 100 = 60% vs

8,00,00012,00,000× 100 = 66.67%.

Reserves: 3,00,00010,00,000× 100 = 30%

vs 2,50,00012,00,000× 100 = 20.83%.

Current liabilities:

1,00,00010,00,000× 100 = 10% vs

1,50,00012,00,000× 100 = 12.50%.

Assets side. Fixed assets:

4,00,00010,00,000× 100 = 40% vs

7,00,00012,00,000× 100 = 58.33%.

Current assets:

6,00,00010,00,000× 100 = 60% vs

5,00,00012,00,000× 100 = 41.67%.

Confirm each column sums to 100%. Aditya

liabilities 60 + 30 + 10 = 100; Anjali assets

58.33 + 41.67 = 100, so the scaling is internally

consistent.

Why this matters. Once scaled, the contrast is sharp:

Aditya is liquidity-rich (current assets 60% of its total) while

Anjali is capacity-rich (fixed assets 58.33%) and leans more on

equity (66.67% vs 60%). Drawing that structural comparison is

exactly what common size analysis is built to deliver, and is the

interpretation an examiner rewards.

Common mistakes. Three predictable slips lose marks: (a) computing percentage change on the current-year base rather than the previous-year base in a comparative statement; (b) confusing common-size analysis (each item as a percent of a common base such as Revenue from Operations or Total Assets) with trend analysis (each item as a percent of a chosen base year); (c) discussing limitations in general terms without naming the specific limitation such as ignoring price-level changes or window dressing.

Same common size balance sheet: Aditya is current-asset

heavy (60%), Anjali is fixed-asset heavy (58.33%) and more

equity-financed (66.67%); bases 10,00,000 and

12,00,000.

More Analysis of Financial Statements Accountancy Class 12 Resources

Analysis of Financial Statements Class 12 Accountancy NCERT Solutions FAQs

Ques. Where can I download Analysis of Financial Statements Class 12 Accountancy NCERT Solutions PDF?

Ans. You can download the Analysis of Financial Statements Class 12 Accountancy NCERT Solutions PDF directly from this page. Both the Normal and HD versions are available, and both are free.

Ques. Are these Class 12 Accountancy Part 2 Chapter 4 NCERT Solutions aligned with the 2026-27 syllabus?

Ans. Yes. The solutions reflect the current 2026-27 NCERT edition. Part 2 Chapter 4 was kept intact, so all questions on Comparative Statements, Common Size Statements, and tools of analysis are in scope.

Ques. How many pages is the Class 12th Accountancy Analysis of Financial Statements NCERT Solutions PDF?

Ans. The solutions PDF runs approximately 25 to 30 pages and covers every Short Answer, Long Answer, and numerical question, including full Comparative and Common Size Statements.

Ques. What is the difference between a Comparative Statement and a Common Size Statement?