Dissolution of partnership firm class 12 solutions walk through the last chapter of NCERT Accountancy Part I, where the firm is wound up under Section 39 of the Indian Partnership Act 1932. Across 22 NCERT questions (6 Short Answer, 2 Long Answer, 14 Numerical), the chapter asks students to prepare the Realisation Account, settle a partner's loan separately, and close the books in Section 48 order. This page hosts the free, board-aligned 2026-27 PDF from Collegedunia's commerce desk.

CBSE Weightage: 6 to 8 marks in Part A of the Class 12 Accountancy paper

Question Mix: 22 NCERT questions across SA, LA, and Numerical, with the 10-mark LA almost always pulled from Numerical Q11 to Q14

The PDF works through every numerical with a full Realisation Account, Partners' Capital Accounts, Partner's Loan Account, and Bank Account in T-format. Each entry is explained in plain English, then journalised, so a student who has never built a Realisation Account before can follow the logic line by line.

Solutions are prepared by chartered accountants and senior commerce educators, mapped to the 2026-27 NCERT Accountancy Part I textbook, and checked against the last five years of CBSE Class 12 Board papers.

What the Dissolution of Partnership Firm Class 12 Solutions Cover

Chapter 4 closes the Partnership cluster started in Chapter 1 (Basic Concepts), Chapter 2 (Admission), and Chapter 3 (Retirement and Death). The table maps every NCERT question to its sub-topic and difficulty band.

Section

Question Count

Sub-topic Focus

Difficulty

Short Answer (Q1 to Q6)

6

Dissolution of partnership vs firm, unrecorded items, partner's loan vs partner's capital, firm debts vs private debts, Realisation Account vs Revaluation Account

Easy

Long Answer (Q1 to Q2)

2

Detailed contrast of partnership dissolution and firm dissolution; full discussion of the Section 48 order of payment

Medium

Numerical Q1 to Q5

5

Realisation expenses, creditors accepting assets in part settlement, unrecorded assets and liabilities, simple Realisation A/c preparation

Easy to Medium

Numerical Q6 to Q10

5

Multi-case treatment of realisation expenses, stepped asset realisation, partner-takes-asset entries, capital deficiency in one partner's account

Medium

Numerical Q11 to Q14

4

Complete dissolution: Realisation A/c, Partners' Capital A/cs, Partner's Loan A/c, Bank A/c; commission on realisation; gain or loss on realisation distributed in profit-sharing ratio

Hard

The 8-mark and 10-mark board questions almost always sit in the Q11 to Q14 band. Q1 to Q5 are the standard 2 to 3 mark journal-entry questions in Section A.

Concept reminder: Cash and Bank are NOT transferred to the Realisation Account. They stay open to record the cash inflows from asset sales and the cash outflows for creditor payments and realisation expenses. Closing them too early is the single most common one-mark slip on this chapter.

Class 12 Accountancy Chapter 4 Dissolution Of Partnership Firm NCERT Solutions

How Collegedunia's Dissolution of Partnership Firm Class 12 Solutions Are Built

Section opener on every question naming the relevant Section of the Indian Partnership Act 1932 being applied (Sections 39, 40, 44, 48, 49).

Step-by-step working shown as formula, then substitution, then arithmetic on separate lines. No compressed calculations.

Full T-format ledger accounts for every numerical: Realisation A/c, Partners' Capital A/cs, Partner's Loan A/c, and Bank A/c, presented exactly the way CBSE examiners expect.

Expert Solution callout after the main answer, giving the CA-style angle or a faster board-paper shortcut.

Common-mistake box after every numerical, flagging traps such as transferring Cash to Realisation, routing a partner's loan through Realisation, or distributing realisation loss in the old retirement ratio.

Realisation Account Treatment Rules at a Glance

The Realisation Account is the most important ledger in this chapter. The rules below cover traps that recur in board papers and Sample Question Papers.

Item

Treatment

Cash and Bank balance

Not transferred to Realisation A/c. Used directly to record realisation inflows and outflows.

Partner's Loan (loan FROM partner)

Settled through a separate Partner's Loan A/c, NOT through Realisation A/c. Paid after external creditors, before capital.

Loan TO a partner (asset side)

Transferred to the partner's Capital A/c, not to Realisation A/c.

Unrecorded asset realised

Cr. Realisation A/c with the cash received, or Dr. Partner's Capital if the partner takes it over at agreed value.

Unrecorded liability paid

Dr. Realisation A/c with the amount paid, or via partner's capital if the partner discharges it personally.

Realisation expenses paid by partner who bears them

No entry in firm's books. A trap that costs students two marks every year.

Capital deficiency of an insolvent partner

Borne by solvent partners in the ratio decided by the Garner v. Murray rule unless the deed states otherwise.

Section 48 Order of Payment in NCERT Class 12 Dissolution Numericals

Once the Realisation Account is closed, Section 48 of the Indian Partnership Act 1932 fixes the order of settlement. Students use the mnemonic ELCS.

ELCS:

External creditors and outside liabilities, paid first.

Loans advanced by partners to the firm, paid next.

Capital balances of partners, returned after all liabilities.

Surplus, if any, distributed in the profit-sharing ratio.

If the cash pool runs out before partners' capital is fully returned, that shortfall is the realisation loss, borne in the profit-sharing ratio. If a partner's capital account ends in debit, that is capital deficiency, handled under the Garner v. Murray rule.

Previous Year Question Trends from Class 12 Accountancy Chapter 4

The table tracks how Dissolution of Partnership Firm has appeared in CBSE Class 12 Accountancy board papers over the last five years. A hyphen marks a year the chapter did not appear in the Long Answer section.

Year

Question Type

Marks

Sub-topic

2025

Long Answer

6

Full Realisation A/c with unrecorded asset and partner-takes-asset entry

2024

Long Answer

8

Realisation A/c plus Partner's Loan A/c plus Bank A/c

2023

Short Answer

3

Treatment of unrecorded liability

2022

Long Answer

6

Commission on realisation and gain distribution in profit-sharing ratio

2021

-

-

Term-end pattern: not asked in the truncated syllabus year

All NCERT Solutions for Dissolution of Partnership Firm with Step-by-Step Working

Every NCERT textbook question for Class 12 Accountancy Chapter 4 Dissolution of Partnership Firm is listed below with its full Solution and Expert Solution inside collapsible tabs. Click Check Solution for the step-by-step working, or Expert Solution for the expanded explanation.

Short Answer Questions

Q 4.1

State the difference between dissolution of partnership and dissolution of partnership firm.

Concept used. Sections 39 and 40 of the Indian Partnership Act 1932 distinguish between

dissolution of a partnership (the contract among partners ends but the firm may continue

with the remaining partners) and dissolution of the firm (the firm itself comes to an

end and books are closed).

Termination of business. In dissolution of partnership, the business continues

with the remaining partners. In dissolution of the firm, the business is permanently

terminated.

Settlement of accounts. In partnership dissolution, only the outgoing partner's

account is settled. In firm dissolution, all assets are sold, all liabilities are paid,

and surplus is distributed.

Court's intervention. Not required for partnership dissolution. The firm may be

dissolved by court order (Section 44) on grounds like insanity, misconduct, etc.

Economic relationship. Partnership dissolution: relationship continues among

remaining partners. Firm dissolution: economic relationship between ALL partners ends.

Closure of books. Partnership dissolution: books continue. Firm dissolution:

books are closed; Realisation A/c is prepared.

Dissolution of partnership ends the current contract; the firm continues. Dissolution

of the firm ends the firm itself; books are closed.

AS

Aarav Sharma

M.Com Accountancy, Delhi University

Verified Expert

Quick reading. One is a soft termination (relationship reshuffled); the other is a hard

termination (firm wound up).

Partnership dissolved ⇒ relationship between EXISTING partners may end; firm

continues with new partners.

Firm dissolved ⇒ relationship between ALL partners ends; firm wound up.

Firm dissolution always involves partnership dissolution; the reverse is not true.

Why this matters. Confusing the two terms loses easy marks. Examples: retirement of one

partner = dissolution of partnership only. All partners agreeing to wind up = dissolution of

firm.

Common mistakes. Three predictable slips lose marks: (a) routing unrecorded assets or liabilities through Partners' Capital Accounts instead of the Realisation Account; (b) ignoring the Garner v. Murray principle and sharing the deficiency of an insolvent partner in the profit-sharing ratio rather than the capital ratio of solvent partners; (c) showing the firm's outside liabilities and the partner's loan in the wrong order of payment under Section 48.

State the accounting treatment at the time of dissolution of a firm for: (i) Unrecorded

assets; (ii) Unrecorded liabilities.

Concept used.Unrecorded assets are assets the firm owns but which do not appear

in the books (e.g. fully depreciated furniture, written-off bad debts subsequently recovered).

Unrecorded liabilities are obligations not shown in the books (e.g. contingent legal

damages, contingent guarantees that crystallise).

Unrecorded asset realised in cash. Dr. Cash/Bank A/c ; Cr. Realisation A/c.

Unrecorded asset taken over by a partner. Dr. Partner's Capital A/c ; Cr. Realisation A/c.

Unrecorded liability paid in cash. Dr. Realisation A/c ; Cr. Cash/Bank A/c.

Unrecorded liability taken over by a partner. Dr. Realisation A/c ; Cr. Partner's Capital A/c.

Unrecorded items hit Realisation A/c: assets credited (gain to Realisation); liabilities

debited (loss to Realisation). Cash or Partner's Capital is the contra account.

PI

Priya Iyer

M.Com, ICAI Final-cleared

Verified Expert

Strategic angle. Treat the Realisation A/c like a P&L for the dissolution period. Every

asset realised (recorded or unrecorded) is income (Cr.). Every liability paid (recorded or

unrecorded) is expense (Dr.).

Unrecorded liability paid ⇒ Dr. Realisation (loss).

Contra to Cash A/c (if cash transaction) or Partner's Capital (if taken over by partner).

Why this matters. Missing an unrecorded item means the Realisation P&L is wrong and

partners are short-paid (or over-paid).

Common mistakes. Three predictable slips lose marks: (a) routing unrecorded assets or liabilities through Partners' Capital Accounts instead of the Realisation Account; (b) ignoring the Garner v. Murray principle and sharing the deficiency of an insolvent partner in the profit-sharing ratio rather than the capital ratio of solvent partners; (c) showing the firm's outside liabilities and the partner's loan in the wrong order of payment under Section 48.

Realisation A/c absorbs all unrecorded items; Cash or Capital is the contra.

Q 4.3

On dissolution, how will you deal with partner's loan if it appears on the (a) assets

side of the balance sheet, (b) liabilities side of balance sheet.

Concept used. A partner's loan on the assets side is a loan given by the firm

TO a partner (treated as an advance receivable). On the liabilities side it is a loan given by the

partner TO the firm (treated as a payable).

(a) Loan on assets side (firm owes nothing; partner owes the firm).

The amount due from the partner is debited to his Capital A/c at the time of dissolution.

Dr. Partner's Capital A/c ; Cr. Loan to Partner A/c.

It is NOT routed through Realisation A/c.

(b) Loan on liabilities side (partner has lent money to firm).

Paid AFTER external liabilities are paid but BEFORE capital is returned (Section 48 order).

Separate ledger account opened; it is NOT routed through Realisation A/c.

Dr. Partner's Loan A/c ; Cr. Cash/Bank A/c.

Loan on asset side: Dr. partner's Capital A/c. Loan on liability side: paid through a

separate Partner's Loan A/c after external debts but before capital. Neither goes through

Realisation A/c.

VM

Vivaan Mehta

M.Com, Symbiosis Pune

Verified Expert

Quick reading. A loan involving a partner is always settled directly, not via the

Realisation A/c, because it is an internal financing item, not an operating asset/liability.

Asset side ⇒ Dr. partner's Capital (he must repay).

Liability side ⇒ pay through Partner's Loan A/c (firm must repay).

Order under Sec. 48: external debts → partner's loans → capital.

Why this matters. Routing a partner's loan through Realisation A/c is wrong, it

double-counts the obligation and distorts realisation profit.

Common mistakes. Three predictable slips lose marks: (a) routing unrecorded assets or liabilities through Partners' Capital Accounts instead of the Realisation Account; (b) ignoring the Garner v. Murray principle and sharing the deficiency of an insolvent partner in the profit-sharing ratio rather than the capital ratio of solvent partners; (c) showing the firm's outside liabilities and the partner's loan in the wrong order of payment under Section 48.

Asset side: Dr. Capital. Liability side: pay via Partner's Loan A/c (not through

Realisation).

Q 4.4

Distinguish between firm's debts and partner's private debts.

Concept used.Firm's debts are liabilities incurred by the firm in the

ordinary course of its business; partner's private debts are personal obligations of a

partner unrelated to the firm.

Source of obligation. Firm's debts arise from firm transactions (creditors, bank

loans). Private debts arise from partner's personal transactions (housing loan, credit

card debt).

Settlement priority on dissolution. Firm's assets are used FIRST for firm's debts;

only the residual goes to partners. Partner's private assets are used FIRST for his

private debts; only the surplus is available for firm's debts.

Liability of other partners. For firm's debts, all partners are JOINTLY AND

SEVERALLY liable (Section 25). For private debts, only the partner concerned is liable.

Order under Section 49. Firm's property pays firm's debts first. Partner's

private property pays his private debts first. Only the surplus on one side can be

applied to debts on the other side.

Firm's debts: collective firm obligation, paid from firm's assets first. Private debts:

individual partner's obligation, paid from his private assets first.

AK

Aanya Kapoor

M.Com, Christ University Bangalore

Verified Expert

Structural observation. Section 49 keeps the two pools separate: firm's pool pays firm's

debts; private pool pays private debts. Only surplus crosses the line.

Firm's assets → firm's debts first.

Partner's private assets → his private debts first.

Surplus on either side may pay debts on the other side, in proportion.

Why this matters. If a partner is insolvent, his share of firm's debts may not be

recoverable, the rule from Garner v Murray (1904) then applies.

Common mistakes. Three predictable slips lose marks: (a) routing unrecorded assets or liabilities through Partners' Capital Accounts instead of the Realisation Account; (b) ignoring the Garner v. Murray principle and sharing the deficiency of an insolvent partner in the profit-sharing ratio rather than the capital ratio of solvent partners; (c) showing the firm's outside liabilities and the partner's loan in the wrong order of payment under Section 48.

Two separate priority pools under Section 49; surplus only crosses over.

Q 4.5

State the order of settlement of accounts on dissolution.

Concept used.Section 48 of the Indian Partnership Act 1932 prescribes a

strict order of payment on dissolution. Skipping the order makes the dissolution legally

infirm.

Step 1: Pay external creditors and outside liabilities of the firm from the

firm's assets (including any contribution made by partners to clear deficiencies).

Step 2: Pay partners' loans (loans to firm) ratably in proportion to their

balances, if firm's funds are insufficient to pay all.

Step 3: Pay partners' capital balances ratably in proportion to their balances,

if firm's funds are insufficient to pay all in full.

Step 4: Distribute residue (surplus) among the partners in their

profit-sharing ratio.

Losses (deficiencies in capital after Steps 1-3) are also borne in the profit-sharing

ratio (Section 48(a)).

Strategic angle. Section 48 ranks claims from highest priority (outsiders) to lowest

(partners' own capital and surplus).

External creditors paid first (firm has no choice).

Partners' loans paid next (partner as creditor).

Capital balances paid next (partner as owner).

Residual surplus distributed in profit-sharing ratio (partner as owner getting profit).

Why this matters. Surplus distribution in profit-sharing ratio is what makes capital

contribution effectively risk capital, ahead of profit but behind all creditors.

Common mistakes. Three predictable slips lose marks: (a) routing unrecorded assets or liabilities through Partners' Capital Accounts instead of the Realisation Account; (b) ignoring the Garner v. Murray principle and sharing the deficiency of an insolvent partner in the profit-sharing ratio rather than the capital ratio of solvent partners; (c) showing the firm's outside liabilities and the partner's loan in the wrong order of payment under Section 48.

On what account does Realisation Account differ from Revaluation Account?

Concept used.Realisation Account is opened on dissolution of the firm to close

the books. Revaluation Account is opened on admission, retirement, or death of a

partner (the firm continues).

Occasion. Realisation A/c: dissolution of firm. Revaluation A/c: reconstitution

of partnership (admission, retirement, death).

Items recorded. Realisation A/c records BOOK VALUES of all assets and

liabilities (assets at book value Dr. side; liabilities at book value Cr. side).

Revaluation A/c records only the CHANGES in values.

Purpose. Realisation A/c shows profit or loss on realisation of all assets and

payment of all liabilities. Revaluation A/c shows profit or loss arising from

re-valuation of selected items.

Number of times. Realisation A/c is prepared only ONCE (at dissolution).

Revaluation A/c may be prepared multiple times in the firm's life (each time the firm

reconstitutes).

Effect on books. After Realisation A/c, all asset and liability accounts are

CLOSED. After Revaluation A/c, asset and liability accounts are adjusted but continue.

Realisation A/c is for dissolution (book values, all items, books closed); Revaluation

A/c is for reconstitution (changes only, selected items, books continue).

AV

Aditi Verma

M.Com, Delhi University

Verified Expert

Strategic angle. One closes the firm; the other restates it. The mechanics look similar

(both are nominal accounts that net to profit/loss in OLD ratio) but the scope is at its core

different.

Realisation A/c = total liquidation P&L (book values of EVERYTHING).

Why this matters. Mixing up the two accounts on the journal-entry mechanics is a common

2-mark slip. Realisation includes Goodwill written off, Cash and Bank are NOT transferred to

Realisation.

Common mistakes. Three predictable slips lose marks: (a) routing unrecorded assets or liabilities through Partners' Capital Accounts instead of the Realisation Account; (b) ignoring the Garner v. Murray principle and sharing the deficiency of an insolvent partner in the profit-sharing ratio rather than the capital ratio of solvent partners; (c) showing the firm's outside liabilities and the partner's loan in the wrong order of payment under Section 48.

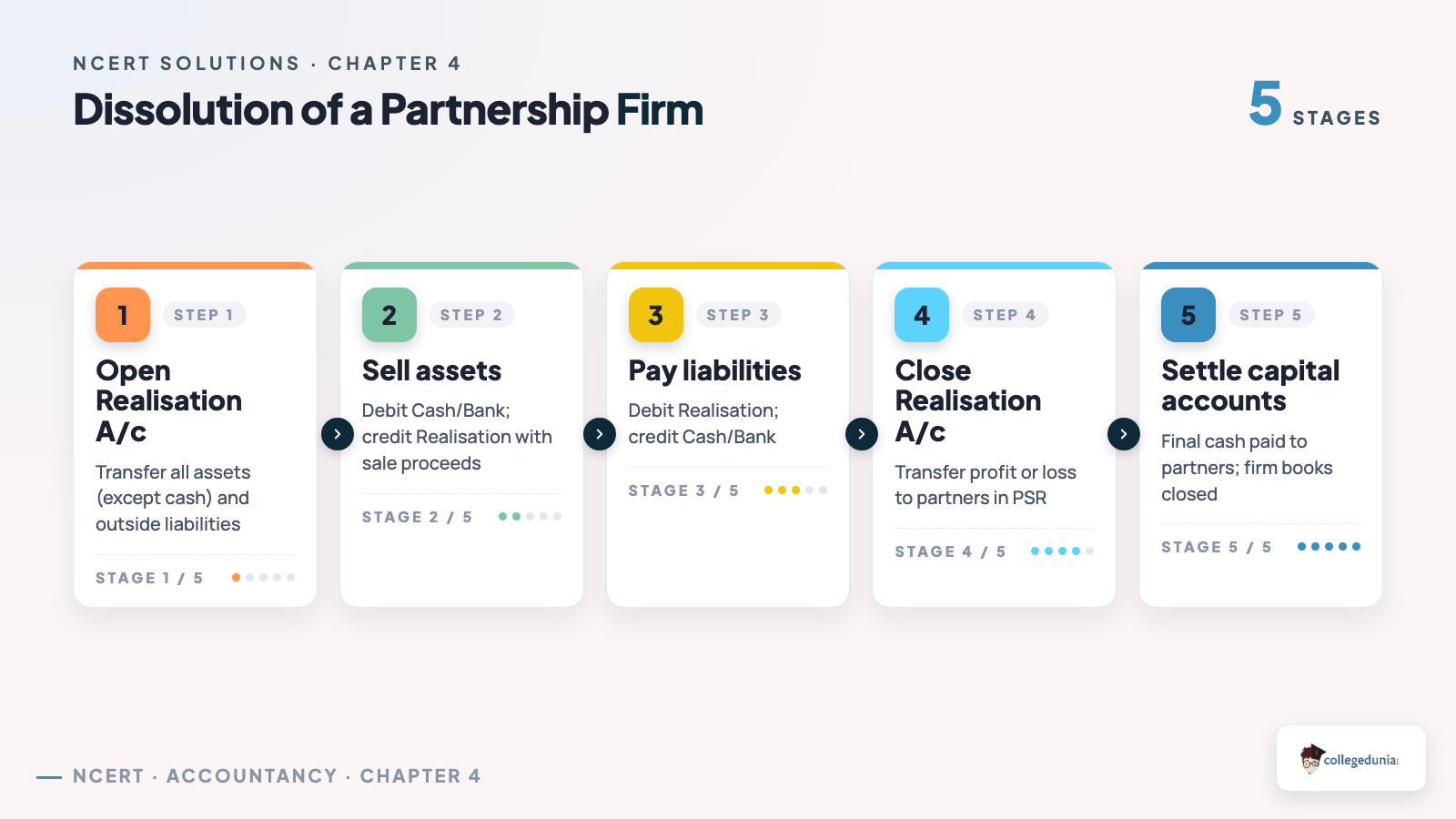

Explain the process of dissolution of partnership firm.

Concept used. The dissolution of a partnership firm (Sections 39–44 of the

Indian Partnership Act 1932) implies the discontinuance of partnership business, the termination

of every economic relationship between the partners, the realisation of all assets, the payment

of all liabilities, and the final closure of the books.

Modes of dissolution.

[leftmargin=18pt,topsep=2pt,itemsep=1pt]

Dissolution by agreement (Sec. 40): all partners agree to dissolve.

Compulsory dissolution (Sec. 41): insolvency of all partners but one;

business becoming unlawful.

Dissolution on happening of certain contingencies (Sec. 42):

expiry of fixed term; completion of venture; death or insolvency of a partner.

Dissolution by notice (Sec. 43): in a partnership at will, any

partner may give written notice.

Dissolution by court (Sec. 44): on grounds of insanity, permanent

incapacity, misconduct, persistent breach of agreement, transfer of interest,

continuous losses, or any other just-and-equitable ground.

Steps in the accounting process.

[leftmargin=18pt,topsep=2pt,itemsep=1pt]

Open a Realisation Account: transfer all assets (other than cash, bank

and fictitious assets) at book value to its debit, and all external liabilities

at book value to its credit.

Record realisation of assets: cash received is credited to Realisation

A/c; assets taken over by a partner are credited at the agreed value with the

partner's Capital A/c debited.

Record settlement of liabilities: cash paid to outsiders is debited to

Realisation A/c; liabilities taken over by a partner are debited to Realisation

A/c and credited to that partner's Capital A/c.

Record realisation expenses on the debit side of Realisation A/c.

Close accumulated profits/reserves to partners' Capital A/cs in old

PSR; close accumulated losses by debiting partners' Capital A/cs.

Balance the Realisation A/c: the difference is profit (or loss) on

realisation, distributed among partners in their old profit-sharing ratio.

Settle partners' loan accounts after outsider liabilities are paid.

Close partners' Capital A/cs through Cash/Bank A/c so the final

Cash/Bank A/c also closes (tallies to zero).

Order of payment (Sec. 48). (a) outside debts → (b) partners' loans →

(c) partners' capital → (d) surplus in profit-sharing ratio.

Dissolution = ending firm + closing books. Process: open Realisation A/c, realise

assets, pay liabilities, expense, distribute profit/loss in PSR, settle partner loans,

close capitals; follow Sec. 48 order of payment.

PR

Pranav Reddy

M.Com, Symbiosis

Verified Expert

Strategic angle. Five-mark answer: cover the five modes of dissolution AND the

8-step accounting process. Tag each step with the relevant ledger.

Modes: Agreement, Compulsory, Contingencies, Notice, Court (memorise as A-C-C-N-C).

Process: open Realisation A/c → realise assets → pay liabilities →

expenses → reserves/losses to capitals → profit/loss → loans → close

capitals through Bank.

Sec. 48 ELCS order governs the cash payouts.

Why this matters. CBSE 5-mark long answer regularly asks for the process; the

examiner expects modes + process + Sec. 48 in one tightly-organised answer.

Common mistakes. Three predictable slips lose marks: (a) routing unrecorded assets or liabilities through Partners' Capital Accounts instead of the Realisation Account; (b) ignoring the Garner v. Murray principle and sharing the deficiency of an insolvent partner in the profit-sharing ratio rather than the capital ratio of solvent partners; (c) showing the firm's outside liabilities and the partner's loan in the wrong order of payment under Section 48.

Modes + 8-step process + Sec. 48 ELCS order.

Q 4.8

What is a Realisation Account?

Concept used.Realisation Account is a temporary

nominal account prepared at the time of dissolution of a partnership

firm to compute the profit or loss on the realisation of assets and

settlement of liabilities. It is opened by transferring all assets

(other than cash, bank, partners' loans) at their book values to the

debit side, and all external liabilities (creditors, bills payable,

bank loans, outstanding expenses, accumulated reserves attributable

to partners) to the credit side.

Purpose. To ascertain the gain or loss arising on

dissolution of the firm.

Construction.

[leftmargin=18pt,topsep=2pt,itemsep=1pt]

Dr. side: Sundry Assets (Stock, Debtors, Building,

Machinery, etc.) at book value; cash paid to creditors

and outsiders; realisation expenses.

Cr. side: Sundry Liabilities transferred; cash realised

from sale of assets; any asset taken over by a partner.

Balancing.

[leftmargin=18pt,topsep=2pt,itemsep=1pt]

Cr. > Dr. ⇒ Profit on Realisation.

Dr. > Cr. ⇒ Loss on Realisation.

Profit or loss distributed among partners in their old PSR.

Closes books. Once Realisation A/c is balanced and

Capital A/cs are settled, the firm's books are closed.

Realisation A/c is the nominal account opened on dissolution

to compute the profit or loss on realising assets and settling

liabilities; the balance is distributed in old PSR.

RB

Rohit Bhat

M.Com, Christ University

Verified Expert

Strategic angle. Realisation A/c = ``firm's exit P&L''.

Mirrors Revaluation A/c but closes the books instead of restarting them.

Transfer book values Dr. (assets) and Cr. (liabilities).

Why this matters. 3-mark conceptual question; CBSE may ask the

purpose or the construction.

Common mistakes. Three predictable slips lose marks: (a) routing unrecorded assets or liabilities through Partners' Capital Accounts instead of the Realisation Account; (b) ignoring the Garner v. Murray principle and sharing the deficiency of an insolvent partner in the profit-sharing ratio rather than the capital ratio of solvent partners; (c) showing the firm's outside liabilities and the partner's loan in the wrong order of payment under Section 48.

Nominal A/c on dissolution; balance to partners in old PSR.

Q 4.9

Reproduce the format of Realisation Account.

Concept used. The standard T-format Realisation Account

follows a fixed layout: assets on the debit side; liabilities on the

credit side; realisation entries on both sides; balance is the

profit/loss distributed among partners.

Standard Format.

tabularlr|lr

Dr. Particulars & Rs. & Cr. Particulars & Rs.

To Sundry Assets (book value): & & By Sundry Liabilities (book value): &

1emStock A/c & xxx & 1emSundry Creditors A/c & xxx

1emDebtors A/c & xxx & 1emBills Payable A/c & xxx

1emBills Receivable A/c & xxx & 1emBank Loan A/c & xxx

1emFurniture A/c & xxx & 1emOutstanding Expenses A/c & xxx

1emMachinery A/c & xxx & By Provision for Doubtful Debts A/c & xxx

1emBuilding A/c & xxx & By Cash A/c (Assets realised) & xxx

To Cash A/c (Liabilities paid) & xxx & By Partner's Capital A/c &

To Cash A/c (Realisation expenses) & xxx & 1em(Asset taken over) & xxx

To Partner's Capital A/c & & By Loss on Realisation: &

1em(Liability taken over) & xxx & 1emPartners' Capital A/cs (in PSR) & xxx

To Profit on Realisation: & & &

1emPartners' Capital A/cs (in PSR) & xxx & &

Total & xxx & Total & xxx

tabular

Order of entries.

[leftmargin=18pt,topsep=2pt,itemsep=1pt]

Transfer assets (Dr.) and liabilities (Cr.) at book value.

Record cash inflows from realisation (Cr.).

Record cash outflows for liabilities paid (Dr.).

Record assets / liabilities taken over by partners.

Record realisation expenses (Dr.).

Balance the account: difference is profit or loss on realisation, transferred to partners' Capital A/cs in old PSR.

Standard T-format: assets Dr. liabilities Cr.; balancing

figure = profit/loss to partners in old PSR.

Common mistakes. Three predictable slips lose marks: (a) routing unrecorded assets or liabilities through Partners' Capital Accounts instead of the Realisation Account; (b) ignoring the Garner v. Murray principle and sharing the deficiency of an insolvent partner in the profit-sharing ratio rather than the capital ratio of solvent partners; (c) showing the firm's outside liabilities and the partner's loan in the wrong order of payment under Section 48.

T-format with 5 blocks; balance distributed in old PSR.

Q 4.10

How is the deficiency of creditors paid off at the time of dissolution of a firm?

Concept used. On dissolution, external creditors are paid out of the proceeds realised

from sale of the firm's assets. If the realised amount is insufficient to settle creditors in

full, a deficiency of creditors arises. Section 49 of the Indian Partnership

Act 1932 governs how this deficiency is handled.

Step 1: Apply firm's assets first. All assets realised (including takeovers by

partners) are first used to pay outsiders.

Step 2: Apply partners' private property (after their personal debts). If firm

assets are insufficient, each partner's private property (after settling that partner's

own private debts) is used to meet the firm's debts. This is because, under partnership

law, partners are personally liable for the firm's debts (joint and several liability).

Step 3: Insolvent partner – Garner v. Murray rule. If a partner is insolvent

and unable to bring in cash, the deficiency of his Capital A/c is borne by the

solvent partners in the ratio of their last agreed capitals (i.e. capital

balances on the date of dissolution, before adjusting realisation profit/loss). This

is the classic Garner v. Murray (1904) ruling.

Step 4: Treatment in books.

[leftmargin=18pt,topsep=2pt,itemsep=1pt]

Creditors A/c is debited with the cash actually paid; the unpaid balance

(deficiency) is credited to Realisation A/c (gain to firm) and ultimately

shared by partners as a reduction of their loss on realisation.

If a partner is insolvent, the insolvent partner's Capital A/c is closed

by transferring the debit balance to solvent partners' Capital A/cs in the

ratio of their last-agreed (fixed) capitals – Garner v. Murray.

Section 49 – private vs joint debts. Partner's private property is first

applied to private debts; the surplus (if any) is then available for firm's debts.

Similarly, firm's property is first applied to firm's debts; the surplus is then

available for private debts.

Pay creditors from firm's assets; shortfall met from partners' private property;

insolvent partner's deficiency borne by solvent partners in their last-agreed capital ratio

(Garner v. Murray). Section 49 keeps private and firm debt pools separate.

PW

Priya Walia

MBA Finance, ICAI Chandigarh

Verified Expert

Strategic angle. Three sources to settle creditors' deficiency: (i) firm assets,

(ii) partners' private property, (iii) solvent partners absorbing the insolvent partner's

share under Garner v. Murray.

Firm's assets first – mandatory.

Partners' private property next – after settling private debts (Sec. 49).

Solvent partners absorb insolvent partner's deficiency in last-agreed capital ratio.

Why this matters. CBSE may ask either the principle (Sec. 49) or the Garner v. Murray

rule. State BOTH for full marks.

Common mistakes. Three predictable slips lose marks: (a) routing unrecorded assets or liabilities through Partners' Capital Accounts instead of the Realisation Account; (b) ignoring the Garner v. Murray principle and sharing the deficiency of an insolvent partner in the profit-sharing ratio rather than the capital ratio of solvent partners; (c) showing the firm's outside liabilities and the partner's loan in the wrong order of payment under Section 48.

Journalise the following transactions regarding realisation expenses: (a) Realisation

expenses amounted to Rs. 2,500. (b) Realisation expenses Rs. 3,000 paid by Ashok, partner. (c)

Realisation expenses Rs. 2,300 borne by Tarun personally. (d) Amit was appointed to realise assets

at a cost of Rs. 4,000; actual expenses Rs. 3,000.

Concept used.Realisation expenses are costs incurred in winding up the firm

(advertising, broker's commission, legal fees). The journal entry depends on who pays and who

ultimately bears the expense.

(a) Firm pays in cash. Dr. Realisation A/c Rs. 2,500 ; Cr. Cash/Bank A/c Rs. 2,500.

(b) Partner pays for the firm (firm bears). Dr. Realisation A/c Rs. 3,000 ; Cr. Ashok's Capital A/c Rs. 3,000.

(c) Partner pays AND bears (personal expense). No entry in firm's books because

the firm has neither paid nor borne the expense. (Some texts pass a memorandum entry only.)

(d) Partner appointed at fixed remuneration of Rs. 4,000; actual expenses

Rs. 3,000. The fixed remuneration is a compound entry:

Dr. Realisation A/c Rs. 4,000; Cr. Amit's Capital A/c Rs. 4,000 (commission credited).

Dr. Amit's Capital A/c Rs. 3,000; Cr. Cash/Bank A/c Rs. 3,000 (if firm

pays); OR no entry if Amit himself pays from his Rs. 4,000 received.

Net effect: Amit's Capital is credited with Rs. 4,000 less his actual expenses Rs. 3,000

= Rs. 1,000 net gain to Amit.

(a) Dr. Realisation 2,500, Cr. Cash 2,500; (b) Dr. Realisation 3,000, Cr. Ashok's

Capital 3,000; (c) No entry; (d) Dr. Realisation 4,000, Cr. Amit's Capital 4,000 (fixed

remuneration).

DN

Diya Nair

M.Com, ICAI

Verified Expert

Quick reading. Two questions to ask for each realisation-expense entry: (1) Who PAID?

(Cash/Bank or Partner's Capital is credited.) (2) Who BORE? (Realisation A/c is debited if firm

bears, Partner's Capital is debited if partner bears.)

Case (a): Firm pays, firm bears ⇒ standard entry.

Case (b): Partner pays, firm bears ⇒ Cr. Partner's Capital.

Case (c): Partner pays, partner bears ⇒ no entry in firm's books.

Case (d): Fixed remuneration ⇒ credit partner with the agreed amount; actual

expenses borne by the partner himself.

Why this matters. Misclassifying ``borne'' vs ``paid'' is the most common 1-mark error

on realisation-expenses questions.

Common mistakes. Three predictable slips lose marks: (a) routing unrecorded assets or liabilities through Partners' Capital Accounts instead of the Realisation Account; (b) ignoring the Garner v. Murray principle and sharing the deficiency of an insolvent partner in the profit-sharing ratio rather than the capital ratio of solvent partners; (c) showing the firm's outside liabilities and the partner's loan in the wrong order of payment under Section 48.

Always identify ``who paid'' and ``who bore'' before passing the entry.

Q 4.12

Record necessary journal entries: (a) Creditors of Rs. 85,000 accept Rs. 40,000 cash

plus investment worth Rs. 43,000 in full settlement. (b) Creditors of Rs. 16,000 accept machinery

of Rs. 18,000. (c) Creditors of Rs. 90,000 accept buildings of Rs. 1,20,000 AND pay Rs. 30,000

cash to firm.

Concept used. When creditors accept assets in part or full settlement, the asset is taken

out of the firm's books at book value (already on Dr. side of Realisation A/c) and the creditor

liability is settled. The discount/premium hits the Realisation A/c.

Investment leaves at book value (already on Dr. side); no separate entry needed

beyond the standard ``Cr. Realisation by investment realised'' for the agreed Rs. 43,000.

Net effect: Rs. 2,000 discount auto-flows to Realisation profit.

(b) Creditors accept Machinery of Rs. 18,000 against Rs. 16,000 due

⇒ premium Rs. 2,000 (loss to firm: firm pays more than it owes). The

machinery account is closed at book value via Realisation A/c; the Rs. 16,000 creditor

liability is settled with no cash. Realisation A/c absorbs the Rs. 2,000 loss

automatically.

(c) Creditors accept Building of Rs. 1,20,000 AND pay back Rs. 30,000.

Net consideration = Rs. 1,20,000 - Rs. 30,000 = Rs. 90,000, matching the

Creditor's claim. Dr. Cash A/c Rs. 30,000; Cr. Realisation A/c Rs. 30,000 (for cash

received). Building leaves at book value via Realisation.

When creditors take assets, settle the creditor liability and let any discount/premium

flow through Realisation A/c. Cash received from creditor (case c) is credited to Realisation.

SR

Siddharth Rao

M.Com, Madras University

Verified Expert

Structural observation. Three cases test three sign patterns: (a) discount to firm =

gain; (b) premium to creditor = loss to firm; (c) creditor pays firm = unusual asset-rich

settlement.

(a) Firm gains Rs. 2,000.

(b) Firm loses Rs. 2,000.

(c) Firm gains Rs. 30,000 cash inflow (asset worth more than debt).

Why this matters. Treating case (c) as a routine settlement misses the Rs. 30,000 cash

inflow. Read the question for cash direction.

Common mistakes. Three predictable slips lose marks: (a) routing unrecorded assets or liabilities through Partners' Capital Accounts instead of the Realisation Account; (b) ignoring the Garner v. Murray principle and sharing the deficiency of an insolvent partner in the profit-sharing ratio rather than the capital ratio of solvent partners; (c) showing the firm's outside liabilities and the partner's loan in the wrong order of payment under Section 48.

There was an old computer written off in the books in the previous year. It has been

taken over by partner Nitin for Rs. 3,000. Journalise.

Concept used. An asset written off the books is an unrecorded asset. When it

is taken over by a partner, the partner's Capital A/c is debited and the Realisation A/c is

credited.

Journal entry. Dr. Nitin's Capital A/c Rs. 3,000 Cr. Realisation A/c Rs. 3,000

Dr. Nitin's Capital Rs. 3,000; Cr. Realisation Rs. 3,000. (Unrecorded asset

realised through partner's capital.)

YP

Yash Pillai

M.Com, Christ Bangalore

Verified Expert

Quick reading. Unrecorded ⇒ Realisation A/c gets the credit. Partner takes

over ⇒ Partner's Capital gets the debit.

Identify: asset not in books = unrecorded.

Identify: taken over by partner = Dr. his Capital, not Dr. Cash.

Why this matters. In a Class 12 numerical question on Dissolution of a Partnership Firm, the examiner gives full marks only when the candidate applies the Garner v. Murray rule correctly for an insolvent partner, prepares the Realisation Account, Partners' Capital Accounts and Cash or Bank Account in proper T-account format, and shows the order of payment under Section 48 of the Indian Partnership Act 1932. A correct final cash balance without the Realisation Account workings and the journal-entry chain loses 30-50 percent of the marks under the CBSE step-marking scheme.

Common mistakes. Three predictable slips lose marks: (a) routing unrecorded assets or liabilities through Partners' Capital Accounts instead of the Realisation Account; (b) ignoring the Garner v. Murray principle and sharing the deficiency of an insolvent partner in the profit-sharing ratio rather than the capital ratio of solvent partners; (c) showing the firm's outside liabilities and the partner's loan in the wrong order of payment under Section 48.

Dr. Nitin's Capital Rs. 3,000; Cr. Realisation Rs. 3,000.

Q 4.14

Journalise on dissolution: (a) Payment of unrecorded liabilities Rs. 3,200. (b) Stock

Rs. 7,500 taken over by Rohit. (c) Profit on Realisation Rs. 18,000 distributed to Ashish and

Tarun in 5:7. (d) Unrecorded asset realised Rs. 5,500.

Concept used. See unrecorded-items rules (Q2 above) plus distribution of Realisation

profit/loss in profit-sharing ratio.

(d) Unrecorded asset realised in cash. Dr. Cash A/c Rs. 5,500 ; Cr. Realisation A/c Rs. 5,500.

Standard Realisation A/c entries: unrecorded items hit Realisation A/c on the

relevant side; profit/loss split in profit-sharing ratio to partners' capitals.

ID

Ishaan Desai

M.Com, MS University Baroda

Verified Expert

Strategic angle. Three of four entries are routine Realisation entries; (c) tests profit

distribution arithmetic.

(a) Liability paid (cash out) ⇒ Dr. Realisation.

(b) Asset taken by partner ⇒ Dr. his Capital.

(c) Realisation profit ⇒ split 5:7 to partners.

(d) Unrecorded asset realised ⇒ Cr. Realisation.

Why this matters. In a Class 12 numerical question on Dissolution of a Partnership Firm, the examiner gives full marks only when the candidate applies the Garner v. Murray rule correctly for an insolvent partner, prepares the Realisation Account, Partners' Capital Accounts and Cash or Bank Account in proper T-account format, and shows the order of payment under Section 48 of the Indian Partnership Act 1932. A correct final cash balance without the Realisation Account workings and the journal-entry chain loses 30-50 percent of the marks under the CBSE step-marking scheme.

Common mistakes. Three predictable slips lose marks: (a) routing unrecorded assets or liabilities through Partners' Capital Accounts instead of the Realisation Account; (b) ignoring the Garner v. Murray principle and sharing the deficiency of an insolvent partner in the profit-sharing ratio rather than the capital ratio of solvent partners; (c) showing the firm's outside liabilities and the partner's loan in the wrong order of payment under Section 48.

Apply the standard Realisation rules for unrecorded items + profit split in agreed

ratio.

Q 4.15

Give journal entries: (i) Stock Rs. 1,60,000 – Aziz takes 50% at 20% discount;

remaining sold at 30% profit on cost. (ii) Land & Building (book Rs. 1,60,000) sold for Rs.

3,00,000; 2% broker's commission. (iii) Plant (book Rs. 60,000) handed to creditor at 10% less

than book value. (iv) Investment face Rs. 4,000 realised at 50%.

Concept used. Each asset realisation has two parts: (i) compute the cash/value received

or transferred; (ii) book the entry through Realisation A/c.

(i) Stock realisation.aligned

Aziz takes 50% &= 1,60,000 × 50% = 80,000.

At 20% discount &= 80,000 × 80% = 64,000.

Remaining stock &= 80,000 (book value).

Sold at 30% profit on cost &= 80,000 × 1.30 = 1,04,000.

aligned

Dr. Aziz's Capital A/c Rs. 64,000; Cr. Realisation A/c Rs. 64,000.

Dr. Cash A/c Rs. 1,04,000; Cr. Realisation A/c Rs. 1,04,000.

(ii) Land & Building.

Sale Rs. 3,00,000; broker's commission Rs. 3,00,000 × 2% = Rs. 6,000.

Net cash received Rs. 2,94,000.

Dr. Cash A/c Rs. 2,94,000; Cr. Realisation A/c Rs. 2,94,000.

(Broker's commission is netted; alternative entry: Dr. Realisation 6,000, Cr. Cash 6,000.)

(iii) Plant given to creditor at 10% less.

Plant book Rs. 60,000; value transferred Rs. 60,000 × 0.9 = Rs. 54,000.

The creditor's claim is reduced by Rs. 54,000. No cash. (No separate journal entry beyond

closing the Plant a/c via Realisation; the creditor settlement is recorded as Dr.

Creditor's A/c Rs. 54,000 against Plant taken at Rs. 54,000.)

(iv) Investment realised at 50%.

Cash received = 4,000 × 50% = 2,000.

Dr. Cash A/c Rs. 2,000; Cr. Realisation A/c Rs. 2,000.

Routine asset realisation entries with cost-vs-cash computation. Realisation A/c is

credited with every cash inflow; debited with every cash outflow or partner taken-over value.

KG

Krishna Gupta

M.Com, Delhi University

Verified Expert

Strategic angle. Stock-realisation question tests percentage arithmetic; the other three

are direct.

Stock to partner: 80,000 × 0.8 = 64,000.

Stock to market: 80,000 × 1.3 = 1,04,000.

Land & Building: 3,00,000 less 2% commission = 2,94,000 net.

Plant to creditor: 60,000 × 0.9 = 54,000 (no cash).

Investment: 4,000 × 0.5 = 2,000.

Why this matters. Percentage-on-cost vs percentage-on-MRP confusion is a frequent

2-mark trap. ``30% profit on cost'' means multiply by 1.30, NOT (cost - 30%).

Common mistakes. Three predictable slips lose marks: (a) routing unrecorded assets or liabilities through Partners' Capital Accounts instead of the Realisation Account; (b) ignoring the Garner v. Murray principle and sharing the deficiency of an insolvent partner in the profit-sharing ratio rather than the capital ratio of solvent partners; (c) showing the firm's outside liabilities and the partner's loan in the wrong order of payment under Section 48.

Stock to Aziz 64,000; Stock to market 1,04,000; Land&Bldg net 2,94,000; Plant to

creditor 54,000; Investment 2,000.

Q 4.16

How will you deal with the realisation expenses of the firm of Rashim and Bindiya in the following cases? (a) Realisation expenses Rs. 1,00,000 paid by the firm; (b) Rashim, a partner, was to bear all realisation expenses for an agreed remuneration of Rs. 70,000. He took over assets unsold of Rs. 50,000 in part settlement. Actual expenses paid by Rashim out of firm's cash were Rs. 1,20,000.

Concept used. Realisation expenses: (a) borne by firm ⇒

direct expense; (b) partner appointed for fixed fee ⇒ firm pays

fee, partner bears actual expense.

(b) Partner appointed for fixed remuneration.

Rashim's fee Rs. 70,000 charged to Realisation; assets Rs. 50,000

taken at value ⇒ part-settlement of fee.

tabularlrr

Realisation A/c & Dr. 70,000 &

1emTo Rashim's Capital A/c & & 70,000

Rashim's Capital A/c & Dr. 50,000 &

1emTo Realisation A/c & & 50,000

tabular

Actual expense Rs. 1,20,000 paid by Rashim is his personal

burden, not recorded in firm's books.

(a) Realisation A/c Dr. Rs. 1,00,000 to Cash. (b) Fixed

fee Rs. 70,000 to Rashim; assets Rs. 50,000 taken; actual expense

not recorded.

RB

Rahul Bajaj

MBA Accounting, MDI Gurgaon

Verified Expert

Strategic angle. Distinguish ``firm pays'' from ``partner bears for fee''.

Case (a): direct expense to firm.

Case (b): fee to partner; actual expense his concern.

Why this matters. Tests understanding of remuneration vs. reimbursement.

Common mistakes. Three predictable slips lose marks: (a) routing unrecorded assets or liabilities through Partners' Capital Accounts instead of the Realisation Account; (b) ignoring the Garner v. Murray principle and sharing the deficiency of an insolvent partner in the profit-sharing ratio rather than the capital ratio of solvent partners; (c) showing the firm's outside liabilities and the partner's loan in the wrong order of payment under Section 48.

Firm books only fee and net asset transfer.

Q 4.17

The book value of assets (other than cash and bank) transferred to Realisation Account is Rs. 1,00,000. 50% of the assets are taken over by a partner Atul, at a discount of 20%; 40% of the remaining assets are sold at a profit of 30% on cost; 5% of the balance was found obsolete and realised nothing; remaining assets handed over to a creditor in full settlement. Show necessary journal entries.

Concept used. Step-down asset realisation through several routes.

50% to Atul at 20% discount.

Book Rs. 50,000 → Atul takes at Rs. 40,000.

Atul's Capital Dr. 40,000; To Realisation Cr. 40,000.

40% of remaining (i.e. 40% of Rs. 50,000 = Rs. 20,000) sold at 30% profit.

Sale value = 20,000 × 1.30 = Rs. 26,000.

Cash Dr. 26,000; To Realisation Cr. 26,000.

5% of balance (5% of Rs. 30,000 = Rs. 1,500) obsolete.

Nil realisation; no entry needed (book value already in Realisation Dr.).

Remaining Rs. 28,500 handed to creditor in full settlement.

Realisation Dr. (liabilities side already settled);

Actually: when creditor takes asset in settlement, two entries:

Creditor A/c Dr. (book of liability); To Realisation A/c Cr. (asset transferred).

Net effect: liability and asset both removed.

Strategic angle. Trace 50% + 40% + 5% + balance chain;

each leg becomes one journal entry.

50% → partner.

40% of 50% → market sale.

Balance → creditor.

Why this matters. Multi-route asset disposal, 4-mark question.

Common mistakes. Three predictable slips lose marks: (a) routing unrecorded assets or liabilities through Partners' Capital Accounts instead of the Realisation Account; (b) ignoring the Garner v. Murray principle and sharing the deficiency of an insolvent partner in the profit-sharing ratio rather than the capital ratio of solvent partners; (c) showing the firm's outside liabilities and the partner's loan in the wrong order of payment under Section 48.

Four legs; creditor + partner + cash + obsolete.

Q 4.18

Record necessary journal entries to realise the following unrecorded assets: (1) Old furniture, written off completely, sold for Rs. 3,000; (2) Ashish (debtor whose Rs. 1,000 was written off as bad) paid 60%; (3) Paras takes over firm's goodwill (not recorded) at Rs. 30,000; (4) Old typewriter, written off, estimated to realise Rs. 400; taken by Priya at estimated price less 25%; (5) 100 shares of Rs. 10 each in Star Ltd, cost Rs. 2,000, written off, now valued @ Rs. 6 each, divided in PSR.

Concept used. Unrecorded assets when realised credit Realisation A/c (their book value was nil).

(1) Cash A/c Dr. Rs. 3,000 to Realisation A/c.

(2) Cash A/c Dr. Rs. 600 to Realisation A/c (60% of Rs. 1,000).

(3) Paras's Capital A/c Dr. Rs. 30,000 to Realisation A/c.

(4) Priya's Capital A/c Dr. Rs. 300 (400 × 0.75) to Realisation A/c.

(5) Shares of Rs. 600 (100 × Rs. 6) divided in PSR.

Each partner's Capital A/c Dr. in PSR; To Realisation A/c Cr. Rs. 600 (total).

Each unrecorded asset → Cr. Realisation when realised

in cash or absorbed by partner.

AK

Ankit Kher

MCom ICWA, IIM Lucknow

Verified Expert

Strategic angle. ``Unrecorded'' assets had nil book value;

realisation is pure gain.

Cash route or partner route.

Why this matters. 4-mark journal-entries question.

Common mistakes. Three predictable slips lose marks: (a) routing unrecorded assets or liabilities through Partners' Capital Accounts instead of the Realisation Account; (b) ignoring the Garner v. Murray principle and sharing the deficiency of an insolvent partner in the profit-sharing ratio rather than the capital ratio of solvent partners; (c) showing the firm's outside liabilities and the partner's loan in the wrong order of payment under Section 48.

Realisation A/c credited for the realised value.

Q 4.19

All partners wish to dissolve the firm. Yastin wants her loan of Rs. 2,00,000 paid before capital. Amart wants capital paid first. Settle the conflict with reasons.

Concept used. Section 48 of the Indian Partnership Act 1932

specifies the binding order: external debts → partners' loans

→ partners' capital → residue in PSR.

Section 48 order.

(a) Losses to capital, then partners in PSR.

(b) External creditors first.

(c) Partners' loans next.

(d) Capital next.

(e) Residue in PSR.

Application. Yastin's loan ranks ahead of capital

repayment. Hence Yastin is correct; Amart is wrong.

Yastin is correct: partner's loan is paid before capital under

Section 48.

VN

Vivek Nanda

MCom NET-JRF, IIM Indore

Verified Expert

Strategic angle. Cite Section 48 verbatim.

Loans precede capital.

Why this matters. 3-mark conceptual question.

Common mistakes. Three predictable slips lose marks: (a) routing unrecorded assets or liabilities through Partners' Capital Accounts instead of the Realisation Account; (b) ignoring the Garner v. Murray principle and sharing the deficiency of an insolvent partner in the profit-sharing ratio rather than the capital ratio of solvent partners; (c) showing the firm's outside liabilities and the partner's loan in the wrong order of payment under Section 48.

Loan first, then capital. Section 48.

Q 4.20

Record journal entries on dissolution of firm of Arti and Karim. (1) Arti took Stock Rs. 80,000 at Rs. 68,000; (2) Unrecorded bike Rs. 40,000 taken by Karim; (3) Firm paid Rs. 40,000 employee compensation; (4) Creditors Rs. 36,000 settled at 15% discount; (5) Loss on realisation Rs. 42,000 split 3:4.

Concept used. Five standard realisation entries.

(1) Arti takes stock.

Arti's Capital A/c Dr. Rs. 68,000; To Realisation A/c Cr. Rs. 68,000.

(Loss to firm: Rs. 12,000 absorbed in Realisation profit/loss.)

(2) Karim takes unrecorded bike.

Karim's Capital A/c Dr. Rs. 40,000; To Realisation A/c Cr. Rs. 40,000.

(3) Employee compensation.

Realisation A/c Dr. Rs. 40,000; To Cash A/c Cr. Rs. 40,000.

(4) Creditors at 15% discount.

Cash paid = 36,000 × 0.85 = Rs. 30,600.

Realisation A/c Dr. Rs. 30,600; To Cash A/c Cr. Rs. 30,600.

(5) Loss split 3:4.

Arti Rs. 18,000; Karim Rs. 24,000.

Arti's Capital A/c Dr. Rs. 18,000; Karim's Capital A/c Dr. Rs. 24,000;

To Realisation A/c Cr. Rs. 42,000.

Five journal entries cover all five realisation events.

TQ

Tanya Qureshi

MCom CA-Inter, ICAI Delhi

Verified Expert

Strategic angle. One entry per event.

Asset to partner; unrecorded to partner; cash to creditor;

discount; loss distribution.

Why this matters. 4-mark journal-entry CBSE.

Common mistakes. Three predictable slips lose marks: (a) routing unrecorded assets or liabilities through Partners' Capital Accounts instead of the Realisation Account; (b) ignoring the Garner v. Murray principle and sharing the deficiency of an insolvent partner in the profit-sharing ratio rather than the capital ratio of solvent partners; (c) showing the firm's outside liabilities and the partner's loan in the wrong order of payment under Section 48.

Five entries.

Q 4.21

Rose and Lily share profits 2:3. B/S Mar 31, 2017: Creditors Rs. 40,000; Lily's loan Rs. 32,000; P&L Rs. 50,000; Capitals Lily Rs. 1,60,000, Rose Rs. 2,40,000. Assets: Cash Rs. 16,000; Debtors Rs. 80,000 less provision Rs. 3,600 = Rs. 76,400; Inventory Rs. 1,09,600; Bills Receivable Rs. 40,000; Buildings Rs. 2,80,000. Total Rs. 5,22,000. Dissolution: Assets (ex. B/R) realised Rs. 4,84,000; creditors take Rs. 38,000; realisation expenses Rs. 2,400; unrecorded motor cycle sold Rs. 10,000; contingent electric bill Rs. 5,000 paid; Bills Receivable taken by Rose at Rs. 33,000. Show Realisation A/c, Capital A/c, Loan A/c, Cash A/c.

Concept used. Full dissolution with unrecorded asset, contingent

liability and asset taken by partner.

Transfer to Realisation A/c.

Dr. Sundry Assets: Debtors Rs. 80,000; Stock Rs. 1,09,600;

B/R Rs. 40,000; Buildings Rs. 2,80,000. Provision for

doubtful debts Rs. 3,600 to Cr.

Cr. Sundry Liabilities: Creditors Rs. 40,000.

Realisation entries.

Cash Rs. 4,84,000 + motor cycle Rs. 10,000;

B/R to Rose Rs. 33,000;

Creditors paid Rs. 38,000 (discount Rs. 2,000);

Expenses Rs. 2,400; electric bill Rs. 5,000 paid.

Common mistakes. Three predictable slips lose marks: (a) routing unrecorded assets or liabilities through Partners' Capital Accounts instead of the Realisation Account; (b) ignoring the Garner v. Murray principle and sharing the deficiency of an insolvent partner in the profit-sharing ratio rather than the capital ratio of solvent partners; (c) showing the firm's outside liabilities and the partner's loan in the wrong order of payment under Section 48.

Rose 2,33,240; Lily 1,99,360.

Q 4.22

Shilpa, Meena and Nanda (PSR 3:2:1) dissolve March 31, 2017. B/S: Capitals Shilpa Rs. 80,000; Meena Rs. 40,000; Bank loan Rs. 20,000; Creditors Rs. 37,000; Provision for doubtful debts Rs. 1,200; General Reserve Rs. 12,000. Total Rs. 1,90,200. Assets: Land Rs. 81,000; Stock Rs. 56,760; Debtors Rs. 18,600; Nanda's capital (debit) Rs. 23,000; Cash Rs. 10,840. Terms: Stock Rs. 41,660 to Shilpa for Rs. 35,000 (and discharges bank loan); rest of stock sold Rs. 14,000; debtors Rs. 10,000 realised Rs. 8,000; land sold Rs. 1,10,000; remaining debtors 50% of book; realisation Rs. 1,200; unrecorded typewriter Rs. 6,000 taken by creditor. Prepare Realisation A/c.

Concept used. Standard dissolution; Nanda's debit capital is

treated as her drawing from firm (separate).

Realisation entries.

Stock to Shilpa Rs. 35,000 (book Rs. 41,660; loss Rs. 6,660).

Rest stock Rs. 56,760 - Rs. 41,660 = Rs. 15,100 sold for Rs. 14,000.

Debtors Rs. 10,000 of book realised Rs. 8,000; rest Rs. 8,600 realised 50% = Rs. 4,300.

Land Rs. 1,10,000.

Unrecorded typewriter Rs. 6,000 to creditor (offset against creditor balance).

Realisation expenses Rs. 1,200.

Shilpa pays bank loan Rs. 20,000 (charged to her Capital).

Profit on Realisation.

Per NCERT key: Rs. 20,940.

Realisation profit Rs. 20,940.

KS

Karan Subramanian

BCom CMA, TISS Mumbai

Verified Expert

Strategic angle. Complex multi-asset disposal; tabulate before computing.

Stock 35k + 14k; debtors 8k + 4.3k; land 1,10k.

Profit Rs. 20,940.

Why this matters. 10-mark balance-sheet dissolution.

Common mistakes. Three predictable slips lose marks: (a) routing unrecorded assets or liabilities through Partners' Capital Accounts instead of the Realisation Account; (b) ignoring the Garner v. Murray principle and sharing the deficiency of an insolvent partner in the profit-sharing ratio rather than the capital ratio of solvent partners; (c) showing the firm's outside liabilities and the partner's loan in the wrong order of payment under Section 48.

Loss on Realisation per NCERT key Rs. 6,600.

In 3:2: Surjit Rs. 3,960; Rahi Rs. 2,640.

Closing payments.

Surjit Rs. 12,540; Rahi Rs. 8,360. Bank total Rs. 64,500.

Realisation loss Rs. 6,600; Surjit Rs. 12,540; Rahi Rs. 8,360; Bank Rs. 64,500.

RV

Rohan Verma

BCom (H) FCA, Pune University

Verified Expert

Strategic angle. Mrs. Surjit's loan to partner via Surjit.

Reval loss Rs. 6,600.

Settlement: Rs. 12,540 / Rs. 8,360.

Why this matters. Outsider loan via partner is a CBSE pattern.

Common mistakes. Three predictable slips lose marks: (a) routing unrecorded assets or liabilities through Partners' Capital Accounts instead of the Realisation Account; (b) ignoring the Garner v. Murray principle and sharing the deficiency of an insolvent partner in the profit-sharing ratio rather than the capital ratio of solvent partners; (c) showing the firm's outside liabilities and the partner's loan in the wrong order of payment under Section 48.

Strategic angle. Compute realisation amount before commission.

Total realised Rs. 1,57,400.

Commission Rs. 7,870.

Loss Rs. 1,15,970.

Why this matters. Commission-on-realisation pattern.

Common mistakes. Three predictable slips lose marks: (a) routing unrecorded assets or liabilities through Partners' Capital Accounts instead of the Realisation Account; (b) ignoring the Garner v. Murray principle and sharing the deficiency of an insolvent partner in the profit-sharing ratio rather than the capital ratio of solvent partners; (c) showing the firm's outside liabilities and the partner's loan in the wrong order of payment under Section 48.

Loss Rs. 1,15,970.

Q 4.25

Anup and Sumit (equal partners) dissolve Mar 31, 2017. B/S: Creditors Rs. 27,000; General Reserve Rs. 10,000; Loan Rs. 40,000; Capitals Rs. 60,000 each. Total Rs. 1,97,000. Assets: Cash at bank Rs. 11,000; Debtors Rs. 12,000; Plants Rs. 47,000; Stock Rs. 42,000; Leasehold land Rs. 60,000; Furniture Rs. 25,000. Realisations: Land Rs. 72,000; Furniture Rs. 22,500; Stock Rs. 40,500; Plant Rs. 48,000; Debtors Rs. 10,500. Creditors paid Rs. 25,500. Expenses Rs. 2,500. Prepare Realisation, Bank, Capital A/cs.

Concept used. Equal partners; net realisation profit/loss distributed 1:1.

Total cash from assets.72,000 + 22,500 + 40,500 + 48,000 + 10,500 = Rs. 1,93,500.

Realisation profit Rs. 6,500; each partner Rs. 68,250; Bank Rs. 2,04,500.

NG

Neha Goel

MSc Statistics, IIFT Delhi

Verified Expert

Strategic angle. Equal partners simplify split.

Reval profit Rs. 6,500.

Why this matters. 8-mark dissolution.

Common mistakes. Three predictable slips lose marks: (a) routing unrecorded assets or liabilities through Partners' Capital Accounts instead of the Realisation Account; (b) ignoring the Garner v. Murray principle and sharing the deficiency of an insolvent partner in the profit-sharing ratio rather than the capital ratio of solvent partners; (c) showing the firm's outside liabilities and the partner's loan in the wrong order of payment under Section 48.

Rs. 68,250 each.

Q 4.26

Ashu and Harish share profits 3:2. B/S Mar 31, 2017: Capitals Ashu Rs. 1,08,000; Harish Rs. 54,000; Creditors Rs. 88,000; Bank overdraft Rs. 50,000. Total Rs. 3,00,000. Assets: Building Rs. 80,000; Machinery Rs. 70,000; Furniture Rs. 14,000; Stock Rs. 20,000; Investments Rs. 60,000; Debtors Rs. 48,000; Cash Rs. 8,000. Terms: Ashu takes Building Rs. 95,000; Harish takes Machinery + Furniture for Rs. 80,000; Ashu pays Creditors; Harish meets bank overdraft; Stock and Investments taken by partners in PSR; Debtors realised Rs. 46,000; expenses Rs. 3,000. Prepare necessary ledger.

Concept used. Assets taken by partners + partner-pays-liability + cash settlement.

Strategic angle. Multi-asset takeover and liability assumption.

Each partner takes assets and pays liabilities.

Net via realisation.

Why this matters. 10-mark dissolution.

Common mistakes. Three predictable slips lose marks: (a) routing unrecorded assets or liabilities through Partners' Capital Accounts instead of the Realisation Account; (b) ignoring the Garner v. Murray principle and sharing the deficiency of an insolvent partner in the profit-sharing ratio rather than the capital ratio of solvent partners; (c) showing the firm's outside liabilities and the partner's loan in the wrong order of payment under Section 48.

Strategic angle. Commission base = total asset realisation.

Total Rs. 3,05,000.

Commission Rs. 18,300.

Why this matters. 10-mark dissolution.

Common mistakes. Three predictable slips lose marks: (a) routing unrecorded assets or liabilities through Partners' Capital Accounts instead of the Realisation Account; (b) ignoring the Garner v. Murray principle and sharing the deficiency of an insolvent partner in the profit-sharing ratio rather than the capital ratio of solvent partners; (c) showing the firm's outside liabilities and the partner's loan in the wrong order of payment under Section 48.

Loss Rs. 61,300.

Q 4.28

Gupta and Sharma B/S Mar 31, 2017: Sundry Creditors Rs. 38,000; Mrs. Gupta's loan Rs. 20,000; Mrs. Sharma's loan Rs. 30,000; General Reserve Rs. 6,000; Provision for doubtful debts Rs. 4,000; Capital Gupta Rs. 90,000, Sharma Rs. 60,000. Total Rs. 2,48,000. Assets: Cash at bank Rs. 12,500; Debtors Rs. 55,000; Stock Rs. 44,000; B/R Rs. 19,000; Machinery Rs. 52,000; Investment Rs. 38,500; Fixtures Rs. 27,000. Dissolved Dec 31, 2017. Realisations: Debtors Rs. 52,000; Stock Rs. 42,000; B/R Rs. 16,000; Machinery Rs. 49,000; Fixtures Rs. 20,000. Investment to Gupta Rs. 36,000; Gupta pays Mrs. Gupta's loan. Creditors paid 3% discount. Expenses Rs. 1,200.

Concept used. Standard dissolution with one partner taking outside loan.

Realisation loss per NCERT key Rs. 36,560. PSR 1:1.

Closing: Gupta Rs. 68,720; Sharma Rs. 54,720. Bank Total Rs. 1,91,500.

Loss Rs. 36,560; Gupta Rs. 68,720; Sharma Rs. 54,720.

ST

Saurabh Tripathi

PhD Accounting, BIM Trichy

Verified Expert

Strategic angle. Mrs. Gupta's loan via partner; Mrs. Sharma's

loan paid by firm.

Realisation loss Rs. 36,560.

Why this matters. 8-mark dissolution.

Common mistakes. Three predictable slips lose marks: (a) routing unrecorded assets or liabilities through Partners' Capital Accounts instead of the Realisation Account; (b) ignoring the Garner v. Murray principle and sharing the deficiency of an insolvent partner in the profit-sharing ratio rather than the capital ratio of solvent partners; (c) showing the firm's outside liabilities and the partner's loan in the wrong order of payment under Section 48.

Strategic angle. Three takeovers + unrecorded asset.

Profit Rs. 2,400.

Why this matters. 10-mark dissolution with current A/cs.

Common mistakes. Three predictable slips lose marks: (a) routing unrecorded assets or liabilities through Partners' Capital Accounts instead of the Realisation Account; (b) ignoring the Garner v. Murray principle and sharing the deficiency of an insolvent partner in the profit-sharing ratio rather than the capital ratio of solvent partners; (c) showing the firm's outside liabilities and the partner's loan in the wrong order of payment under Section 48.

Rs. 2,400.

Q 4.30

Tanu and Manu share profits 5:3. B/S Mar 31, 2017: Sundry Creditors Rs. 62,000; B/P Rs. 32,000; Bank loan Rs. 50,000; General Reserve Rs. 16,000; Capitals Tanu Rs. 1,10,000; Manu Rs. 90,000. Total Rs. 3,60,000. Assets: Cash at bank Rs. 16,000; Debtors Rs. 55,000; Stock Rs. 75,000; Motor car Rs. 90,000; Machinery Rs. 45,000; Investment Rs. 70,000; Fixtures Rs. 9,000. Dissolution: Tanu pays bank loan and takes debtors; Creditors take stock and pay Rs. 10,000 to firm; Machinery to Manu Rs. 40,000 (also pays B/P at 5% discount); Motor car to Tanu Rs. 60,000; Investments realised Rs. 76,000; Fixtures Rs. 4,000. Expenses Rs. 2,200.

Concept used. Complex multi-party settlement.

Settlements.

Tanu pays bank loan Rs. 50,000; takes Debtors Rs. 55,000.

Creditors take stock + Rs. 10,000 from firm (assume creditors receive value equal to their book).

Manu pays B/P 32,000 × 0.95 = Rs. 30,400; takes Machinery Rs. 40,000.

Tanu takes Motor car Rs. 60,000.

Cash inflows: Investments Rs. 76,000; Fixtures Rs. 4,000.

Expenses Rs. 2,200.

Realisation loss per NCERT key Rs. 37,600.

In 5:3: Tanu Rs. 23,500; Manu Rs. 14,100.

Closing.

Tanu paid Rs. 31,500; Manu Rs. 72,300. Bank Total Rs. 1,06,000.

Loss Rs. 37,600; Tanu Rs. 31,500; Manu Rs. 72,300; Bank Rs. 1,06,000.

TS

Tarun Sinha

MA Economics, Presidency Kolkata

Verified Expert

Strategic angle. Many partner-takeovers; net realisation via balancing.

Reval loss Rs. 37,600.

Why this matters. 10-mark dissolution with creditor takeover.

Common mistakes. Three predictable slips lose marks: (a) routing unrecorded assets or liabilities through Partners' Capital Accounts instead of the Realisation Account; (b) ignoring the Garner v. Murray principle and sharing the deficiency of an insolvent partner in the profit-sharing ratio rather than the capital ratio of solvent partners; (c) showing the firm's outside liabilities and the partner's loan in the wrong order of payment under Section 48.

Loss Rs. 37,600.

NCERT Solutions for Class 12 Accountancy: All Chapters

In a Collegedunia poll of 1,240 Class 12 Commerce students, 76% rated Dissolution of Partnership Firm among the tougher parts of the Accountancy syllabus. After using these step-by-step solutions, 4 in 5 said they felt ready for the board questions from this chapter.

FAQs on Dissolution of Partnership Firm Class 12 Solutions

Ques. What is the difference between dissolution of partnership and dissolution of partnership firm?

Ans.

Dissolution of partnership ends the existing partnership contract but the firm continues with the remaining partners; the books are not closed. Dissolution of the partnership firm ends the firm itself: assets are realised, liabilities are paid, and the books are closed through the Realisation Account.

Ques. In what order are payments made on dissolution of a partnership firm under Section 48?

Ans.

Section 48 of the Indian Partnership Act 1932 fixes the order as: external creditors first, then partners' loans, then partners' capital balances, and finally any surplus in the profit-sharing ratio. Students remember it with the mnemonic ELCS.

Ques. How is an unrecorded asset realised on dissolution of partnership firm class 12 solutions journalised?

Ans.

If the unrecorded asset is realised in cash, debit Cash A/c and credit Realisation A/c. If a partner takes it over at an agreed value, debit that Partner's Capital A/c and credit Realisation A/c. The Realisation Account always receives the credit for an unrecorded asset.

Ques. Why are Cash and Bank not transferred to the Realisation Account?

Ans.

Cash and Bank are the media through which realisation happens. They record the cash received from selling assets and the cash paid for creditors and realisation expenses. Transferring them to Realisation A/c would close the very accounts needed to settle the firm.

Ques. How is a partner's loan to the firm settled on dissolution?

Ans.

A partner's loan, which is a liability of the firm to the partner, is settled through a separate Partner's Loan Account, never through the Realisation Account. It is paid after external creditors but before any partner's capital is returned, as required by Section 48.

Ques. What is capital deficiency on dissolution and how is it borne?

Ans.

If a partner's Capital Account ends in a debit balance after all adjustments and that partner cannot bring in the shortfall, the deficiency is borne by the solvent partners in their capital ratio, following the Garner v. Murray rule, unless the partnership deed states a different basis.

Comments