The ncert class 12 accountancy book pdf chapter 10 Cash Flow Statement carries a guaranteed 6-mark numerical in every CBSE Class 12 Accountancy board session. This is the highest-weightage topic in Part B, making this Reprint 2026-27 chapter essential for exam prep.

- CBSE Weightage (Part B): 6 marks (one long-answer numerical, every session)

- Solved Illustrations: 7 + 11 numerical practice questions

This is the official NCERT source for the CBSE exam. Our Solutions and Notes refer to this PDF by section number, so refer to it while studying.

Also Check:

- Cash Flow Statement Class 12 NCERT Solutions PDF

- Cash Flow Statement Class 12 Accountancy Notes

- Cash Flow Statement Class 12 Handwritten Notes

Why Part 2 Chapter 6 Cash Flow Statement Is the Part B Anchor

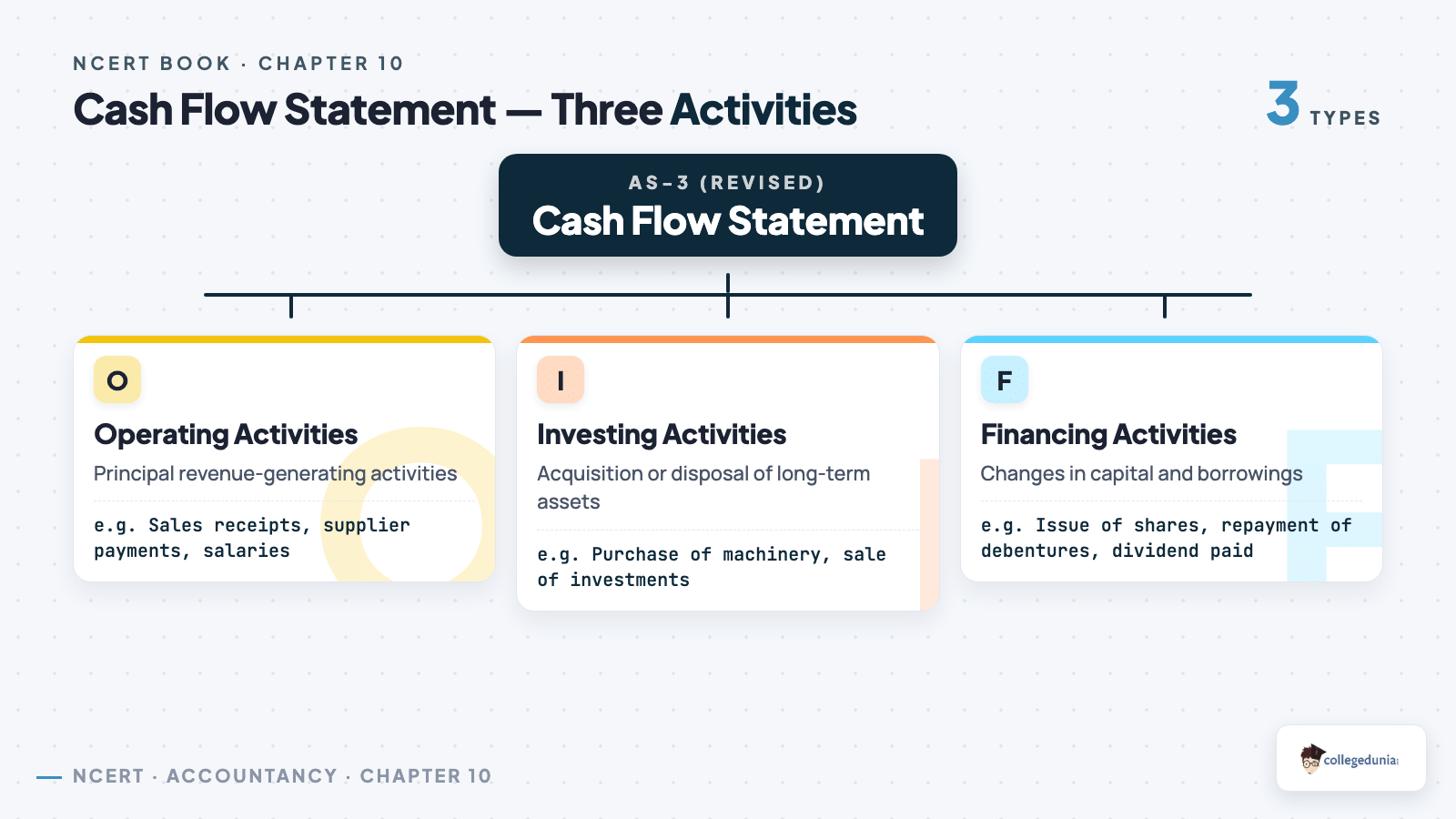

Cash Flow Statement converts the Balance Sheet and Statement of Profit and Loss into three streams: Operating, Investing, and Financing. It's the only chapter requiring a full cash-position reconstruction, which is why a 6-mark numerical appears in every board session. In CBSE 2024, the average was 3.2/6. The chapter rewards procedure over interpretation, so learning the indirect-method format line by line earns full marks.

Cash Flow Statement Video Chapter Walkthrough

Source: Commerce and Fun on YouTube

How Will Collegedunia's NCERT Book PDF for Part 2 Chapter 6 Help You?

The NCERT chapter is the only reference CBSE examiners use, including AS-3 (Revised) rules. We host the 2026-27 PDF plus the matching Cash Flow Statement NCERT Solutions for practice.

- Page-faithful PDF: the chapter appears exactly as printed by NCERT, with original illustration numbers retained.

- Direct download: no sign-up, no paywall, no watermark over the format tables.

- Linked Solutions and Notes: every step in the Collegedunia Solutions cites the section number from this PDF, so cross-checking a treatment item takes one click.

Three Concepts That Carry Almost Every Mark in Part 2 Chapter 6

The 6-mark CBSE numerical tests three ideas in a fixed order. Lock these down before opening any practice question.

2. Indirect method for Operating Activities. Start with Net Profit before Tax and Extraordinary Items. Add non-cash and non-operating charges (depreciation, goodwill written off, loss on sale of fixed asset). Subtract non-operating incomes (profit on sale, interest received, dividend received). Adjust for working-capital changes. Subtract tax paid. The closing figure is Cash from Operating Activities.

3. Treatment of Interest and Dividend. For a non-financing enterprise: Interest paid and Dividend paid go to Financing. Interest received and Dividend received go to Investing. Reversing this is a standard examiner trap.

Class 12 Accountancy Part 2 Chapter 6 PYQ Trends in CBSE Board Exams

Cash Flow Statement is the most predictable 6-mark question in the CBSE Class 12 Accountancy paper. The last six sessions are mapped below, latest first.

| Year | Question Type | Marks | What Was Asked |

|---|---|---|---|

| 2025 | Long answer | 6 | Full Cash Flow Statement, indirect method, with provision for tax |

| 2024 | Long answer | 6 | Cash Flow with extraordinary item and goodwill written off |

| 2023 | Long answer | 6 | Operating activities reconciliation, sale of fixed asset adjustment |

| 2022 | Short + Long | 1+6 | MCQ on classification; full statement with proposed dividend |

| 2021 | Long answer | 6 | Cash Flow Statement with bank overdraft and tax paid |

| 2020 | Long answer | 6 | Indirect method with depreciation and dividend paid |

A 6-mark full Cash Flow Statement has appeared in every one of the last 8 CBSE board sessions without exception. No other Class 12 Accountancy chapter has this kind of question-pattern stability.

Part 2 Chapter 6 Cash Flow Statement Section Sequence

The chapter is organised as a single long workflow, not as separate concepts. Read it strictly in printed order; each section feeds the next.

| Section | Topic | What It Covers |

|---|---|---|

| 6.1 | Objectives of Cash Flow Statement | Why AS-3 mandates the statement; uses for short-term planning |

| 6.2 | Benefits of Cash Flow Statement | Five benefits including liquidity assessment and comparison with budget |

| 6.3 | Cash and Cash Equivalents | Definition; treatment of bank overdraft; short-term investments |

| 6.4 | Cash Flows | Inflows vs outflows; what is excluded |

| 6.5 | Classification of Activities | Operating, Investing, Financing with worked examples |

| 6.6 | Ascertaining Cash Flow from Operating Activities | Indirect method, step-by-step format (the 6-mark question) |

| 6.7 | Ascertainment of Cash Flow from Investing and Financing | Working notes for each line; non-cash transactions |

| 6.8 | Preparation of Cash Flow Statement | Complete format; 7 solved illustrations |

2026-27 Edition Notes for Part 2 Chapter 6

The 2026-27 syllabus keeps Chapter 6 unchanged. The 7 illustrations and AS-3 table carry forward exactly. Only the indirect method is tested in CBSE Class 12 for Operating Activities. Page numbers shift by 1–2 pages due to front-matter changes.

Three-Day Study Plan for Part 2 Chapter 6 Cash Flow Statement

Use this short plan to cover Cash Flow Statement without crowding out Part 2 Chapter 4 Analysis of Financial Statements and Part 2 Chapter 5 Accounting Ratios from the same Part B unit.

| Day | Read | Practice |

|---|---|---|

| Day 1 | Sections 6.1, 6.2, 6.3, 6.4, 6.5 (classification framework) | Illustration 1 and 2; one MCQ set on classification |

| Day 2 | Section 6.6 (Operating Activities, indirect method) | Illustrations 3 to 5; 4 practice questions on indirect method |

| Day 3 | Sections 6.7 and 6.8 (Investing, Financing, full format) | Illustrations 6 and 7; last 3 CBSE 6-mark Cash Flow questions |

Key Features of the Official NCERT Reprint 2026-27

- Publisher: NCERT, Reprint 2026-27 (April 2025 print)

- Book: Class 12 Accountancy Part 2, Part 2 Chapter 2 (the chapter is printed as Part 2 Chapter 2 of Part 2 but appears as Part 2 Chapter 6 in the combined Part A + Part B CBSE syllabus listing)

- Pages: 40 pages (approx)

- Illustrations: 7 solved illustrations covering all three activity streams

- Exercise: 11 numerical questions plus short-answer and long-answer theory questions

- Aligned to: AS-3 (Revised) issued by ICAI

Class 12 Accountancy Chapter Weightage Snapshot

Cash Flow Statement is the final Part B chapter (Financial Statement Analysis, 20 marks total). The three Part B chapters share marks as below.

| Chapter | Topic | CBSE Marks (typical) |

|---|---|---|

| Part 2 Ch 4 | Analysis of Financial Statements | 4 to 5 |

| Part 2 Ch 5 | Accounting Ratios | 8 to 10 |

| Part 2 Ch 6 | Cash Flow Statement | 6 |

Full master table: Class 12 Accountancy Part 2 Chapter 6 Weightage and Trend Notes

Other Resources for Part 2 Chapter 6

- Cash Flow Statement NCERT Book PDF

- Class 12 Accountancy Part 2 Chapter 6 NCERT Solutions

- Class 12 Accountancy Part 2 Chapter 6 Notes

- Class 12 Accountancy Part 2 Chapter 6 Handwritten Notes

NCERT Book PDF for Class 12 Accountancy: All Chapters

The full set of Class 12 Accountancy chapter PDFs, Part 1 and Part 2, sourced from the Reprint 2026-27 NCERT release.

| Chapter | Title |

|---|---|

| Chapter 1 | Accounting for Partnership: Basic Concepts NCERT Book PDF |

| Chapter 2 | Reconstitution: Admission of a Partner NCERT Book PDF |

| Chapter 3 | Reconstitution: Retirement / Death NCERT Book PDF |

| Chapter 4 | Dissolution of Partnership Firm NCERT Book PDF |

| Part 2 Chapter 1 | Accounting for Share Capital NCERT Book PDF |

| Part 2 Chapter 2 | Issue and Redemption of Debentures NCERT Book PDF |

| Part 2 Chapter 3 | Financial Statements of a Company NCERT Book PDF |

| Part 2 Chapter 4 | Analysis of Financial Statements NCERT Book PDF |

| Part 2 Chapter 5 | Accounting Ratios N CERT Book PDF |

Student Feedback

In a Collegedunia poll of 1,240 Class 12 Commerce students, 76% rated Cash Flow Statement among the tougher parts of the Accountancy syllabus. After using these chapter resources, 4 in 5 said they felt ready for the board questions from this chapter.

FAQs on Class 12 Accountancy Part 2 Chapter 6 Cash Flow Statement NCERT Book PDF

Ques. Is this the official NCERT Class 12 Accountancy Part 2 Chapter 6 Cash Flow Statement PDF?

Ans.

Yes. This is the Reprint 2026-27 edition of Class 12 Accountancy Part 2, Part 2 Chapter 2 Cash Flow Statement (listed as Part 2 Chapter 6 in the CBSE syllabus), sourced from ncert.nic.in and aligned to the CBSE 2026-27 syllabus.

Ques. What is a Cash Flow Statement in Class 12 Accountancy?

Ans.

A Cash Flow Statement is a financial statement that shows the inflows and outflows of cash and cash equivalents during an accounting period, classified into Operating, Investing, and Financing activities as required by AS-3 (Revised).

Ques. What weightage does Part 2 Chapter 6 Cash Flow Statement carry in the CBSE Class 12 board exam?

Ans.

Part 2 Chapter 6 carries 6 marks in the CBSE Class 12 Accountancy board exam as a long-answer numerical question. A full Cash Flow Statement of 6 marks has appeared in every one of the last 8 board sessions without exception.

Ques. Which method is tested in CBSE Class 12 Cash Flow Statement, direct or indirect?

Ans.

Only the indirect method is tested in CBSE Class 12 Accountancy. The direct method is mentioned in the NCERT chapter for awareness but is not asked in the board exam.

Ques. How are interest paid and dividend paid treated in Cash Flow Statement?

Ans.

For a non-financing enterprise, interest paid and dividend paid are classified under Financing Activities. Interest received and dividend received are classified under Investing Activities. For a financing enterprise (banks, NBFCs), these are part of Operating Activities.

Ques. How many illustrations and practice questions are in Part 2 Chapter 6?

Ans.

The chapter has 7 solved illustrations covering all three activity streams (Operating, Investing, Financing) and 11 numerical practice questions in the end-of-chapter exercise, along with short-answer and long-answer theory questions.

Ques. Is bank overdraft treated as cash equivalent in Class 12 Cash Flow Statement?

Ans.

Yes. As per the NCERT chapter aligned to AS-3 (Revised), bank overdraft and cash credit are treated as part of cash and cash equivalents for the purpose of preparing the Cash Flow Statement, because they are part of the enterprise's cash management.

Comments