The ncert class 12 accountancy book pdf chapter 8 Analysis of Financial Statements opens Part B of the textbook and is the highest-yield commerce-stream topic for the CBSE board paper. The Reprint 2026-27 PDF carries the official NCERT framing for tools of financial analysis that examiners use to build the 12-mark Part B numerical cluster.

| Chapter Length | 23 pages (Part 2, Ch 3 of Part B) |

| CBSE Weightage (Part B) | 4 to 6 marks (tools and limitations) |

| Tools Covered | 5 standard methods plus limitations block |

Part 2 Chapter 4 sits inside the Analysis of Financial Statements unit of Part B and supplies the conceptual scaffolding for Chapters 9 (Accounting Ratios) and 10 (Cash Flow Statement). Examiners pair it with the company balance sheet of Part 2 Chapter 3 to ask 1-mark MCQs on objectives, 3-mark short questions on limitations, and 4 to 6-mark numericals on Comparative and Common Size statements.

This PDF is the source the Collegedunia NCERT Solutions and Handwritten Notes refer to. Read this chapter first, then move to Part 2 Chapter 5 for Ratio practice.

Also Check:

- Analysis of Financial Statements Class 12 NCERT Solutions PDF

- Analysis of Financial Statements Class 12 Accountancy Notes

- Analysis of Financial Statements Class 12 Handwritten Notes

Why Analysis of Financial Statements Carries the Highest Application Weight in Part B

The CBSE Class 12 Accountancy paper splits Part B between this chapter, Accounting Ratios, and Cash Flow Statement. Part 2 Chapter 4 is the conceptual gatekeeper: every 4-mark Comparative Statement and every 6-mark Common Size Statement in the last decade has used the formula framework laid out in Sections 4.4.1 and 4.4.2 of this PDF. The chapter is also the favoured source for 1-mark objective-type MCQs on parties interested in analysis, limitations, and types of analysis.

Comparative Income Statement or Common Size Balance Sheet has appeared in 9 of the last 10 CBSE board sessions for 4 to 6 marks.

Analysis of Financial Statements Video Chapter Walkthrough

Source: takshila learn on YouTube

What the ncert class 12 accountancy book pdf chapter 8 Analysis of Financial Statements Contains

The Part 2 chapter is structured around five numbered sections that move from definitions to tool-by-tool worked treatment. Each section feeds directly into a CBSE question pattern, so a sequential reading order is the safest preparation route.

| Section | Topic | Why It Matters |

|---|---|---|

| 4.1 | Meaning of Analysis of Financial Statements | 1-mark MCQ on definitions and parties interested |

| 4.2 | Significance of Analysis | Distinguishes information needs of seven user groups |

| 4.3 | Objectives of Analysis | 3-mark short-answer staple in 2023 and 2024 papers |

| 4.4 | Tools of Analysis | Houses the five techniques the numerical section uses |

| 4.5 | Limitations of Financial Analysis | Five-point block tested as 3-mark direct theory |

How Will Collegedunia's Class 12 Accountancy Part 2 Chapter 4 NCERT Book PDF Help You?

The official NCERT source is the only book CBSE examiners use to set Part B questions on financial analysis. Reading the chapter PDF first locks the vocabulary (horizontal analysis, vertical analysis, base year, percentage change) that the marking scheme rewards. Collegedunia hosts the same Reprint 2026-27 chapter the board uses, alongside the matching Solutions and Notes for cross-reference.

- Page-faithful PDF: the chapter appears exactly as printed by NCERT, with original illustration numbers and proforma layouts retained.

- Direct download: no sign-up or paywall before the file opens.

- Connected resources: the Solutions and Handwritten Notes reference this PDF by section number, so cross-checking a Comparative Statement format takes one click.

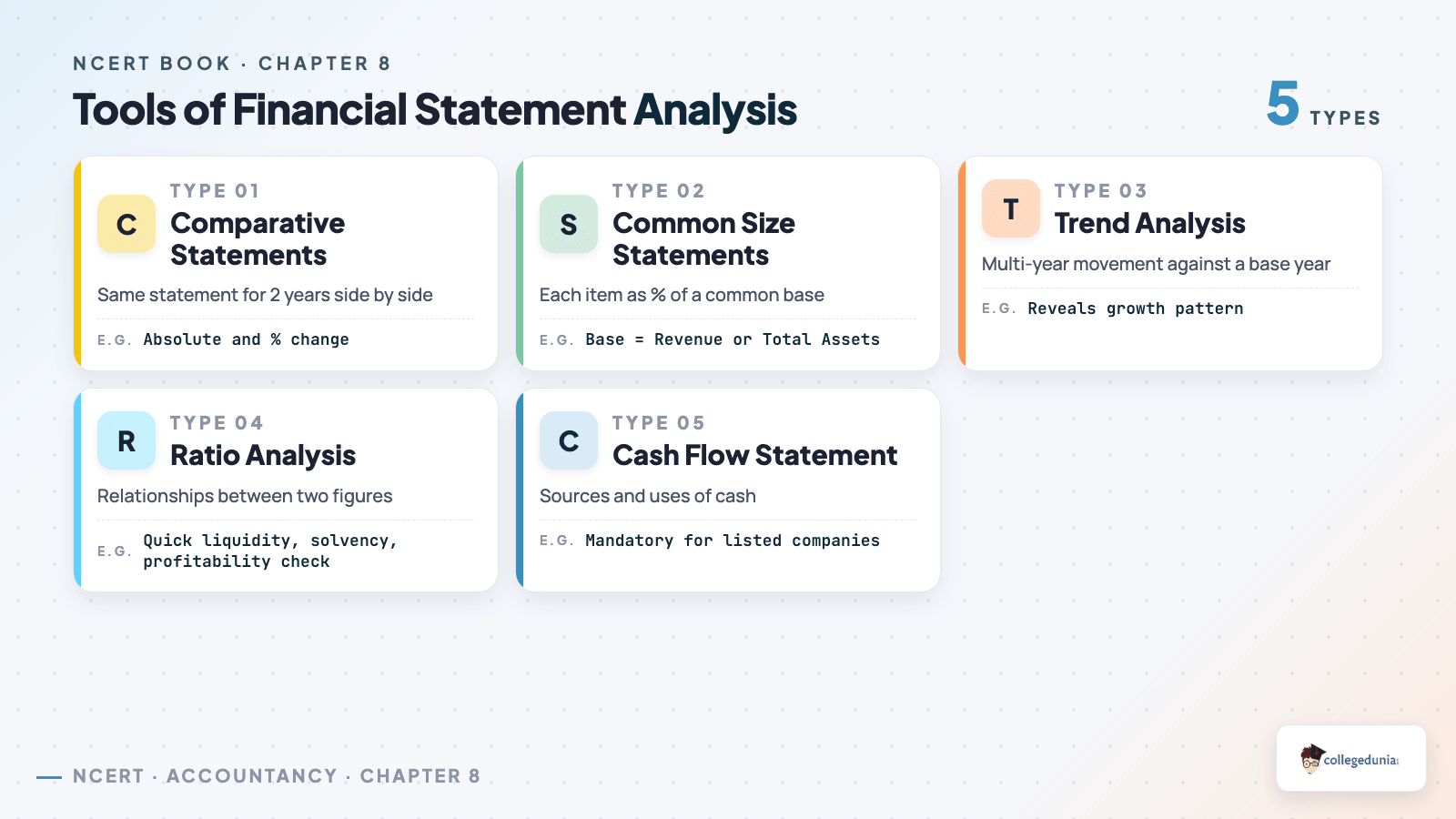

Key Tools of Financial Analysis Inside Part 2 Chapter 4

Section 4.4 lists the five standard tools the CBSE syllabus expects you to apply. Comparative Statements and Common Size Statements are the directly examinable formats; Trend Analysis, Ratio Analysis, and Cash Flow Analysis are introduced here and developed in detail in Chapters 9 and 10.

| Tool | What It Compares | Standard Output |

|---|---|---|

| Comparative Statements | Two or more years, side by side | Absolute change and percentage change columns |

| Common Size Statements | Each item as a percentage of a base figure | Revenue from Operations = 100 for income; Total Assets = 100 for balance sheet |

| Trend Analysis | One item across many years | Indexed values against a chosen base year |

| Ratio Analysis | Numerical relationships between line items | Liquidity, solvency, activity, profitability ratios |

| Cash Flow Analysis | Inflows and outflows of cash and cash equivalents | Operating, investing, financing activities |

Of these five, only Comparative and Common Size Statements are examined as standalone numericals inside this chapter. The remaining three move to Chapters 9 and 10.

Class 12 Accountancy Part 2 Chapter 4 PYQ Trends in CBSE Board Exams

Analysis of Financial Statements is the most repeated source of 1-mark MCQs in the entire Part B block, while the 4-mark and 6-mark numericals rotate predictably between Comparative Income Statement and Common Size Balance Sheet. The chapter rarely sits out a session.

| Year | Question Type | Marks | Sub-topic |

|---|---|---|---|

| 2025 | Long answer | 6 | Common Size Balance Sheet (two years) |

| 2024 | Short answer | 3 | Three objectives of financial analysis |

| 2023 | Long answer | 4 | Comparative Income Statement |

| 2022 | Short answer | 3 | Limitations of financial analysis (any four) |

| 2021 | MCQ + Short | 1+3 | Parties interested; types of analysis |

Full year-wise PYQ map: Analysis of Financial Statements NCERT Solutions Class 12

Important Concepts and Definitions in Part 2 Chapter 4

The NCERT framing keeps the language formal. The five terms below carry the highest 1-mark and 3-mark recall load.

Vertical Analysis: each item in a single year's statement is expressed as a percentage of a base figure (Revenue from Operations for the Statement of Profit and Loss; Total Assets or Total Equity and Liabilities for the Balance Sheet).

Comparative Statement: a four-column document showing absolute figures of two years, absolute change, and percentage change.

Common Size Statement: a vertical analysis output in which every line is shown as a percentage of the selected base. Useful for cross-firm comparison regardless of size.

Trend Percentages: values of a single item across many years indexed to a chosen base year that is set at 100.

Class 12 Accountancy NCERT Book PDF Part 2 Chapter 4: Limitations You Must Quote in 3-Mark Answers

Section 4.5 of the chapter lists the standard limitations of financial analysis that CBSE asks for verbatim recall. Examiners deduct marks when students invent generic limitations instead of quoting the textbook list.

- Historical: based on past data, may not predict the future.

- Ignores price level changes: figures do not adjust for inflation.

- Qualitative elements ignored: management quality, employee morale, brand value are not captured.

- Accounting concepts and conventions: different firms may follow different methods.

- Window dressing: manipulated figures distort the analysis.

CBSE 2024 awarded 3 marks for naming any three of these limitations with one-line explanations.

Related Resources

- Class 12 Accountancy Part 2 Chapter 4 NCERT Solutions PDF

- Class 12 Accountancy Part 2 Chapter 4 Notes

- Class 12 Accountancy Part 2 Chapter 4 Handwritten Notes

- Class 12 Accountancy Part 2 Chapter 4 Formula Sheet

NCERT Book PDF for Class 12 Accountancy: All Chapters

| Chapter | Title |

|---|---|

| Chapter 1 | Accounting for Partnership Basic Concepts NCERT Book PDF |

| Chapter 2 | Reconstitution of a Partnership Firm: Admission of a Partner NCERT Book PDF |

| Chapter 3 | Reconstitution of a Partnership Firm: Retirement or Death of a Partner NCERT Book PDF |

| Chapter 4 | Dissolution of Partnership Firm NCERT Book PDF |

| Part 2 Chapter 1 | Accounting for Share Capital NCERT Book PDF |

| Part 2 Chapter 2 | Issue and Redemption of Debentures NCERT Book PDF |

| Part 2 Chapter 3 | Financial Statements of a Company NCERT Book PDF |

| Part 2 Chapter 5 | Accounting Ratios NCERT Book PDF |

| Part 2 Chapter 6 | Cash Flow Statement NCERT Book PDF |

FAQs on Class 12 Accountancy Part 2 Chapter 4 NCERT Book PDF

Ques. Is the NCERT Class 12 Accountancy Part 2 Chapter 4 PDF available for free download?

Ans.

Yes. Collegedunia hosts the official Reprint 2026-27 release of the Analysis of Financial Statements chapter as a free, no-signup PDF. The download link on this page opens the full 23-page chapter exactly as printed by NCERT.

Ques. What are the five tools of financial analysis listed in NCERT Class 12 Accountancy Part 2 Chapter 4?

Ans.

NCERT lists Comparative Statements, Common Size Statements, Trend Analysis, Ratio Analysis, and Cash Flow Analysis as the five standard tools. Only the first two are examined as standalone numericals inside this chapter; the rest are developed in Chapters 9 and 10.

Ques. Is Part 2 Chapter 4 Analysis of Financial Statements part of the CBSE 2026-27 syllabus?

Ans.

Yes. The chapter is fully retained in the current 2026-27 syllabus and forms the opening chapter of Part B: Analysis of Financial Statements. CBSE allocates 4 to 6 marks to this chapter in the Class 12 Accountancy board paper.

Ques. What is the difference between Comparative and Common Size Statements as per NCERT?

Ans.

A Comparative Statement uses horizontal analysis: it shows absolute figures of two years plus absolute change and percentage change columns. A Common Size Statement uses vertical analysis: it expresses every line as a percentage of a base figure (Revenue from Operations for the income statement; Total Assets for the balance sheet).

Ques. How many marks does Part 2 Chapter 4 carry in the CBSE Class 12 Accountancy board exam?

Ans.

Part 2 Chapter 4 carries 4 to 6 marks in the Part B section. The mark allocation rotates between a 1-mark MCQ on objectives or parties interested, a 3-mark short-answer on limitations or objectives, and a 4 to 6-mark numerical on Comparative or Common Size Statements.

Ques. Which chapters should I read alongside NCERT Class 12 Accountancy Part 2 Chapter 4?

Ans.

Read Part 2 Chapter 3 (Financial Statements of a Company) first, because Part 2 Chapter 4 analyses the same statements. Follow Part 2 Chapter 4 with Part 2 Chapter 5 (Accounting Ratios) and Part 2 Chapter 6 (Cash Flow Statement). The three chapters together form the full Part B block of the CBSE Class 12 Accountancy syllabus.

Comments