The ncert class 12 accountancy book pdf chapter 6 Issue and Redemption of Debentures covers how a company raises long-term debt by issuing debentures, services the interest cost, and finally repays the principal under SEBI rules and the Companies Act 2013. The Reprint 2026-27 PDF is the official NCERT source aligned to the CBSE 2026-27 Accountancy syllabus.

- CBSE Weightage (Part A): 8 marks typically, 1 long-answer numerical of 6 to 8 marks

- Stream relevance: compulsory for Class 12 Commerce; the only Part A chapter that covers company debt instruments end to end

Part 2 Chapter 2 sits inside Part A (Accounting for Partnership Firms and Companies, 60 marks) and pairs with Part 2 Chapter 1 Accounting for Share Capital to complete the Company Accounts block. It walks through six issue cases (par, premium, discount, consideration other than cash, collateral security, and from the lender's books), the writing-off of Loss on Issue of Debentures, interest on debentures with TDS, and the three redemption routes (lump sum, instalments, purchase in the open market).

This PDF is the source the Collegedunia NCERT Solutions and Handwritten Notes refer to. Read this chapter first, then move to the Solutions for active practice.

Also Check:

- Issue and Redemption of Debentures Class 12 NCERT Solutions PDF

- Issue and Redemption of Debentures Class 12 Accountancy Notes

- Issue and Redemption of Debentures Class 12 Handwritten Notes

Why Class 12 Accountancy Part 2 Chapter 2 Debentures Matters for the Board Exam

Debentures is one of the two chapters that almost guarantees a long-answer question in the CBSE Class 12 Accountancy paper. Examiners use it to test the full journal-entry cycle, the Loss on Issue write-off, and one of the redemption methods in the same numerical, so a single question can pull 6 to 8 marks from this chapter alone.

Across the last 5 board sessions, Part 2 Chapter 2 has carried at least 1 long-answer numerical every year, typically worth 6 marks.

Issue and Redemption of Debentures Video Chapter Walkthrough

Source: Magnet Brains on YouTube

How Will Collegedunia's Class 12 Accountancy Part 2 Chapter 2 NCERT Book PDF Help You?

The official NCERT source is the only book CBSE examiners use to frame Part A questions on debentures. Reading the chapter PDF first builds the legal and accounting framework before you attempt numericals. Collegedunia hosts the same Reprint 2026-27 chapter the board uses, plus the matching Solutions and Notes for cross-reference.

- Page-faithful PDF: the chapter appears exactly as printed by NCERT, with original illustration numbers and journal-entry tables retained.

- Direct download: no sign-up or paywall before the file opens.

- Connected resources: the Solutions and Handwritten Notes on Collegedunia reference this PDF by section number, so cross-checking an entry takes one click.

Class 12 Accountancy Part 2 Chapter 2 PYQ Trends in CBSE Board Exams

The chapter rotates between two examiner favourites: a full issue-of-debentures numerical with a Loss on Issue write-off, and a redemption numerical (lump sum or by purchase in the open market). Short-answer questions usually pick on terms of issue with redemption (issued at par redeemable at premium, and the four similar permutations).

| Year | Question Type | Marks | Sub-topic |

|---|---|---|---|

| 2025 | Long answer | 6 | Issue at discount redeemable at premium with Loss on Issue write-off |

| 2024 | Long answer | 6 | Redemption by purchase in the open market for cancellation |

| 2023 | Short + Long | 3 + 6 | Interest on debentures with TDS; issue for consideration other than cash |

| 2022 | Short answer | 4 | Issue of debentures as collateral security (two methods) |

| 2021 | MCQ + Short | 1 + 3 | Terms of issue permutations; DRR computation |

In 4 of the last 5 sessions, the long-answer question has come from either Issue terms with Loss on Issue or Redemption by purchase in the open market.

What the Class 12 Accountancy Part 2 Chapter 2 NCERT Book PDF Contains

The chapter is built around six numbered sections that move from definition to redemption in a strict order. Each section feeds directly into a journal-entry block that the CBSE board paper asks you to prepare almost every year.

| Section | Topic | Why It Matters |

|---|---|---|

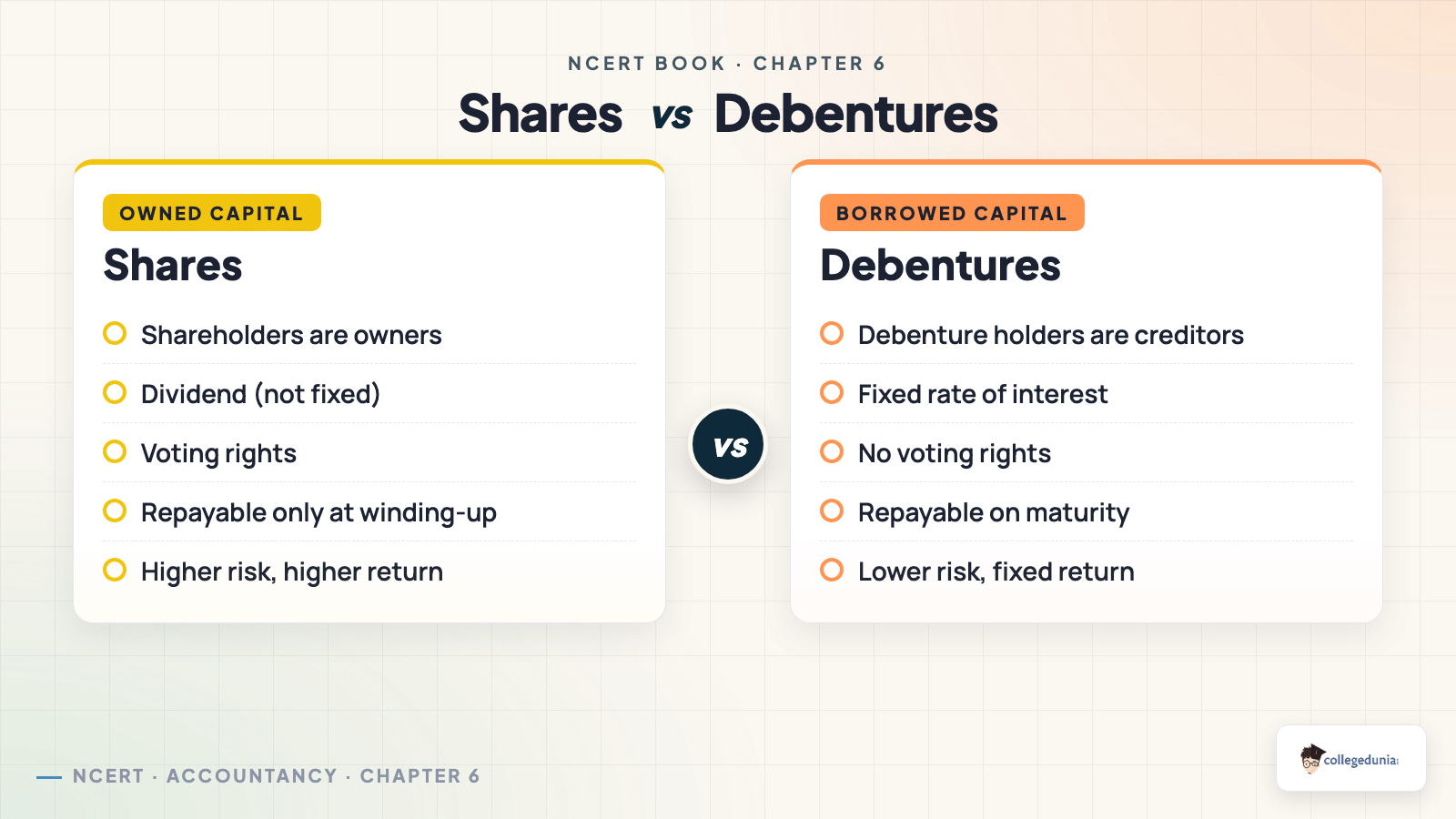

| 6.1 | Meaning of Debenture & Distinction from Shares | 5 fixed distinguishing points; standard 3-mark short-answer trap |

| 6.2 | Types of Debentures | Five classifications by security, tenure, convertibility, registration, priority |

| 6.3 | Issue of Debentures | Six issue cases including the four terms-of-issue-and-redemption permutations |

| 6.4 | Issue for Consideration other than Cash & as Collateral Security | Two methods for collateral security; Debenture Suspense A/c |

| 6.5 | Interest on Debentures | Charge against profits; TDS at 10% (Sec 193, Income Tax Act) |

| 6.6 | Redemption of Debentures | Three methods; DRR + DRI rules under Companies (Amendment) Act 2019 |

Key Journal Entries Every Student Must Memorise from Part 2 Chapter 2

Five entries appear in almost every CBSE long-answer numerical on debentures. Practise them from this chapter PDF in the exact order shown by NCERT, then move to the Solutions PDF for fully worked numericals.

2. Write-off of Loss on Issue: Securities Premium Reserve A/c Dr. (first), then Statement of Profit & Loss Dr. (balance) to Loss on Issue of Debentures A/c.

3. Interest with TDS: Interest on Debentures A/c Dr. to Debenture-holders A/c, TDS Payable A/c.

4. Transfer to DRR: Surplus, i.e., Balance in Statement of P&L A/c Dr. to Debenture Redemption Reserve A/c.

5. Redemption in lump sum: Debentures A/c Dr., Premium on Redemption A/c Dr. to Debenture-holders A/c; then Debenture-holders A/c Dr. to Bank A/c.

2026-27 Edition Notes for Part 2 Chapter 2 Issue and Redemption of Debentures

The current 2026-27 syllabus keeps Part 2 Chapter 2 Issue and Redemption of Debentures structurally unchanged from the previous reprint, but two regulatory updates carry into the chapter content and must be reflected when you answer:

- DRR is no longer compulsory for listed companies and AIFIs; only unlisted companies retain a 10% DRR on the outstanding debentures (Companies Amendment Rules 2019, reflected in the NCERT 2026-27 reprint).

- DRI (Debenture Redemption Investment) at 15% of the debentures maturing during the year must be made on or before 30th April of the year of redemption, under Rule 18(7)(c) of the Companies (Share Capital and Debentures) Rules.

- Redemption by conversion into shares and the related sinking-fund method are NOT in the 2026-27 CBSE Class 12 Accountancy syllabus, although the NCERT chapter retains the brief theory mention.

Three-Day Study Plan for Class 12 Accountancy Part 2 Chapter 2

Use this short plan to cover Issue and Redemption of Debentures without crowding out Part 2 Chapter 1 Accounting for Share Capital, which examiners often pair with it.

| Day | Read | Practice |

|---|---|---|

| Day 1 | Sections 6.1, 6.2, 6.3 (definition, types, six issue cases) | Illustrations 1 to 6 + the four terms-of-issue permutations |

| Day 2 | Sections 6.4, 6.5 (collateral security, interest with TDS) | Illustrations 7 to 12 + 5 practice questions |

| Day 3 | Section 6.6 (redemption methods, DRR, DRI) + revision | Illustrations 13 to 20 + last 3 years CBSE Qs |

Class 12 Accountancy Chapter Weightage Snapshot

Part 2 Chapter 2 sits inside Part A. Within the 24-mark Company Accounts cluster, the Share Capital chapter (Part 2 Ch 1) and Debentures chapter (Part 2 Ch 2) together account for almost the entire Part A weightage outside Partnership.

| Chapter | Topic | CBSE Marks (typical) |

|---|---|---|

| Ch 1 | Accounting for Partnership: Basic Concepts | 8 to 10 |

| Ch 2 | Reconstitution: Admission of a Partner | 8 to 10 |

| Ch 3 | Reconstitution: Retirement / Death | 8 to 10 |

| Ch 4 | Dissolution of Partnership Firm | 6 to 8 |

| Part 2 Ch 1 | Accounting for Share Capital | 8 to 10 |

| Part 2 Ch 2 | Issue and Redemption of Debentures | 6 to 8 |

Full reference table: Class 12 Accountancy Weightage and Trend Notes

Related Resources for Part 2 Chapter 2

- Class 12 Accountancy Part 2 Chapter 2 NCERT Solutions

- Class 12 Accountancy Part 2 Chapter 2 Notes

- Class 12 Accountancy Part 2 Chapter 2 Handwritten Notes

NCERT Book PDF for Class 12 Accountancy: All Chapters

The full set of Class 12 Accountancy chapter PDFs, Part 1 and Part 2, sourced from the Reprint 2026-27 NCERT release.

| Chapter | Title |

|---|---|

| Chapter 1 | Accounting for Partnership: Basic Concepts NCERT Book PDF |

| Chapter 2 | Reconstitution: Admission of a Partner NCERT Book PDF |

| Chapter 3 | Reconstitution: Retirement / Death NCERT Book PDF |

| Chapter 4 | Dissolution of Partnership Firm NCERT Book PDF |

| Part 2 Chapter 1 | Accounting for Share Capital NCERT Book PDF |

| Part 2 Chapter 3 | Financial Statements of a Company NCERT Book PDF |

| Part 2 Chapter 4 | Analysis of Financial Statements NCERT Book PDF |

| Part 2 Chapter 5 | Accounting Ratios NCERT Book PDF |

| Part 2 Chapter 6 | Cash Flow Statement NCERT Book PDF |

FAQs on Class 12 Accountancy Part 2 Chapter 2 NCERT Book PDF

FAQs on Class 12 Accountancy Part 2 Chapter 2 NCERT Book PDF

Ques. Is this the official NCERT Class 12 Accountancy Part 2 Chapter 2 PDF?

Ans.

Yes. This is the Reprint 2026-27 edition of Class 12 Accountancy Part 1, Part 2 Chapter 2 Issue and Redemption of Debentures, sourced from ncert.nic.in and aligned to the CBSE 2026-27 syllabus.

Ques. What is the difference between a debenture and a share?

Ans.

A debenture is borrowed capital that earns a fixed rate of interest as a charge against profits, while a share is owned capital that earns a variable dividend out of distributable profits. Debenture-holders are creditors of the company; shareholders are owners. NCERT lists five such distinguishing points in Section 6.1 of the Class 12 Accountancy Part 2 Chapter 2 PDF.

Ques. What weightage does Part 2 Chapter 2 carry in the CBSE Class 12 Accountancy board exam?

Ans.

Part 2 Chapter 2 contributes 6 to 8 marks to the Part A Company Accounts cluster. Across the last 5 board sessions a long-answer numerical of 6 marks has appeared every year, drawn from either the issue cases with Loss on Issue or one of the redemption methods.

Ques. What are the four terms of issue and redemption of debentures?

Ans.

The four standard permutations are: issued at par redeemable at par, issued at premium redeemable at par, issued at par redeemable at premium, and issued at discount redeemable at premium. Each permutation has a fixed journal entry pattern on issue and a corresponding Loss on Issue write-off when there is a redemption premium.

Ques. Is DRR (Debenture Redemption Reserve) compulsory for all companies in 2026-27?

Ans.

No. After the Companies (Share Capital and Debentures) Amendment Rules 2019, listed companies and All India Financial Institutions are exempt from creating DRR. Only unlisted companies are required to maintain DRR at 10% of the outstanding value of debentures before redemption begins.

Ques. How many illustrations and practice questions are in Part 2 Chapter 2?

Ans.

The chapter has 18 to 20 solved illustrations and more than 25 practice questions across the Test Your Understanding blocks and the end-of-chapter exercise. Together they cover all six issue cases and the three redemption methods.

Ques. Is redemption by conversion into shares part of the 2026-27 syllabus?

Ans.

No. Redemption by conversion into shares and the related sinking-fund method are outside the 2026-27 CBSE Class 12 Accountancy syllabus. The NCERT chapter still mentions both briefly, but CBSE has not asked them for several sessions.

Comments