The ncert class 12 accountancy book pdf chapter 5 Accounting for Share Capital is the single highest-scoring chapter in the Part B (Company Accounts) cluster of the CBSE Class 12 Accountancy paper, routinely carrying one full 8-mark journal-entry question on issue of shares plus a 3 to 4 mark theory or pro-rata problem in every board session since 2019. The page hosts the unmodified Reprint 2026-27 NCERT chapter, aligned to the current CBSE 2026-27 syllabus.

- CBSE Weightage (Part B): 8 to 10 marks (1 numerical of 8 marks + 1 short answer of 3 to 4 marks)

- NCERT Chapter Length: 88 to 92 pages (Part 2, opening chapter)

This PDF is the official source the Collegedunia NCERT Solutions, Notes and Handwritten Notes for Part 2 Chapter 1 quote from. Download it once, then layer the practice resources on top.

Also Check:

- Accounting for Share Capital Class 12 NCERT Solutions PDF

- Accounting for Share Capital Class 12 Accountancy Notes

- Accounting for Share Capital Class 12 Handwritten Notes

- CBSE Class 12 Accountancy Syllabus 2026-27

Why ncert class 12 accountancy book pdf chapter 5 Accounting for Share Capital Sets the Tone of Company Accounts

Part 2 Chapter 1 is the first chapter of Part 2 of Class 12 Accountancy and the entry point to the Company Accounts unit. Every later topic in Part B (Chapters 6 to 10) assumes you already know the share capital structure, the journal entries for issue, the treatment of calls in arrears and the forfeiture-reissue cycle. A weak Part 2 Chapter 1 directly costs you 4 to 6 marks on the Schedule III balance sheet question in Part 2 Chapter 3.

The CBSE board paper has asked an 8-mark question on issue of shares at premium with pro-rata allotment, calls in arrears and forfeiture in 5 of the last 6 board sessions. The Companies Act 2013 references, especially Section 53 (prohibition on discount issue) and Section 52 (Securities Premium uses), are also directly examinable as 1-mark or 3-mark theory.

Accounting for Share Capital Video Chapter Walkthrough

Source: Next Toppers - 12th Commerce on YouTube

How Will Collegedunia's ncert class 12 accountancy book pdf chapter 5 Accounting for Share Capital Help You?

The official NCERT chapter is the only source the CBSE board paper quotes from. Using the original PDF removes three risks that older editions carry: section numbers from the Companies Act 1956 instead of 2013, outdated Schedule III templates, and the discontinued treatment of issue at discount that NCERT removed when Section 53 came into force.

- Reprint 2026-27, the exact edition CBSE 2026-27 question setters work from

- All 25+ Illustrations are solved in the NCERT recommended Journal, Cash Book and Ledger format that the board marking scheme rewards

- Section 5.5 covers Forfeiture and Re-issue, the highest-scoring 8-mark sub-topic, with three fully worked Illustrations

- The Glossary lists every term (Authorised, Issued, Subscribed, Called-up, Paid-up Capital, Calls in Arrears, Securities Premium) that the 1-mark Assertion-Reason questions test

Collegedunia hosts the file as a direct PDF download plus a page-by-page flipbook so you can jump to a specific Illustration without downloading the full 90-page file.

Class 12 Accountancy Part 2 Chapter 1 PYQ Trends in CBSE Board Exams

The table below is built from the actual CBSE Class 12 Accountancy question papers from 2025 backwards. The 8-mark numerical question on issue of shares with pro-rata allotment and forfeiture has appeared in 5 of the last 6 sessions, making this the single most-tested numerical in the entire Class 12 paper.

| Year | Marks from Part 2 Chapter 1 | Question Pattern |

|---|---|---|

| 2025 | 11 | 8M: Pro-rata allotment, forfeiture, re-issue + 3M: Securities Premium uses (Section 52) |

| 2024 | 9 | 8M: Issue at premium + over-subscription + 1M: Minimum subscription threshold |

| 2023 | 10 | 8M: Forfeiture + re-issue at discount + journal entries + 1M Assertion-Reason on share capital classes |

| 2022 (Term 2) | 8 | 6M: Issue for consideration other than cash + 1M MCQ + 1M MCQ |

| 2021 (Term 1) | 6 | 6 MCQs covering Authorised, Issued, Subscribed Capital and Calls in Arrears |

| 2020 | 8 | 8M: Pro-rata allotment + adjustment of excess against calls in advance |

Full year-wise PYQ map: Accounting for Share Capital NCERT Solutions PDF

What the ncert class 12 accountancy book pdf chapter 5 Accounting for Share Capital Contains

Part 2 Chapter 1 is organised into five numbered sections plus a Glossary, a Summary, and the end-of-chapter question block. Each section feeds directly into the journal-entry sequence the board paper tests.

| Section | Topic | Why It Matters in CBSE 2026-27 |

|---|---|---|

| 5.1 | Features of a Company | 1-mark theory: separate legal entity, perpetual succession, limited liability |

| 5.2 | Kinds of Companies | Public vs Private, One Person Company (Section 2(62) Companies Act 2013) |

| 5.3 | Share Capital of a Company | Authorised, Issued, Subscribed, Called-up, Paid-up, Reserve Capital, Uncalled Capital |

| 5.4 | Nature and Classes of Shares | Equity vs Preference; Section 43 Companies Act 2013 |

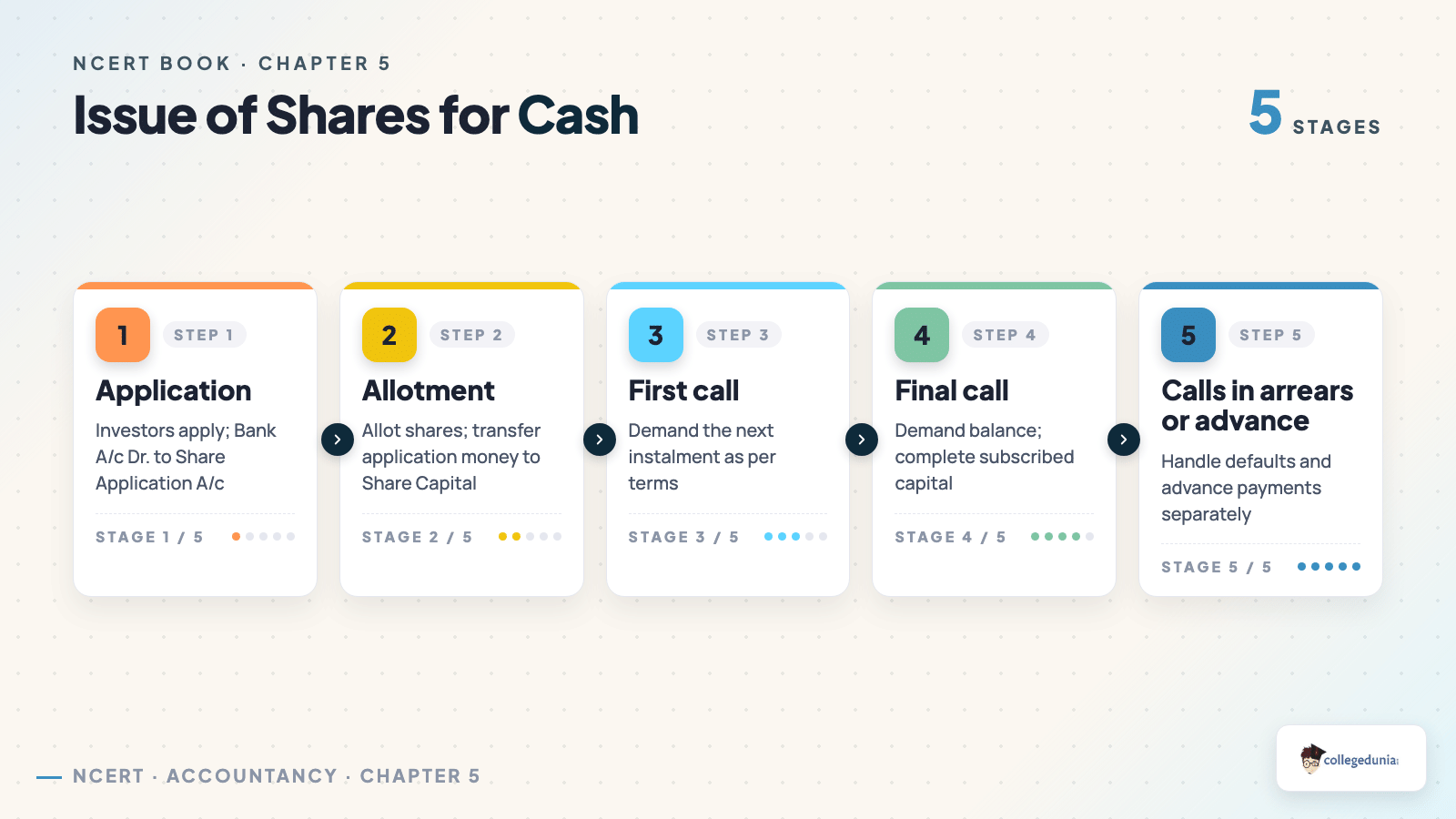

| 5.5 | Issue of Shares (Premium, Par, Consideration other than Cash, Pro-rata, Calls in Arrears / Advance, Over-subscription, Forfeiture, Re-issue) | The 8-mark numerical comes from here, every single year |

| Glossary + Summary | Key terms + Section references | Direct source for Assertion-Reason and 1-mark MCQs |

| Questions for Practice | 12 SA + 18 LA + 40 Numerical | Mirrors CBSE board paper difficulty |

The strongest study tactic is to first work all 25+ Illustrations from section 5.5 in order, because each successive Illustration adds one new complication, premium, then over-subscription, then pro-rata, then calls in arrears, then forfeiture, then re-issue.

Key Concepts and Formulas Inside Part 2 Chapter 1 Accounting for Share Capital

The chapter is journal-entry heavy but does carry three small calculations the CBSE marking scheme rewards. The most common is the pro-rata allotment ratio and the adjustment of excess application money against allotment money due.

- Pro-rata Ratio = Shares Applied : Shares Allotted on the over-subscribed portion only.

- Excess Application Money = (Applied minus Allotted) x Application rate, adjusted first against Allotment due.

- Forfeiture credit to Share Capital A/c = Forfeited shares x Called-up value per share.

- Capital Reserve on Re-issue = Forfeited amount on re-issued shares minus discount allowed on re-issue.

- Max Discount on Re-issue = Amount originally forfeited on those shares.

Full formula recall: Accounting for Share Capital Notes

2026-27 Edition Notes for the Class 12 Accountancy Part 2 Chapter 1 NCERT Book PDF

The Reprint 2026-27 carries the same Section 5.1 to 5.5 structure as the 2023 rationalised edition. Two changes worth flagging:

- Issue of Shares at a Discount has been fully removed in line with Section 53 of the Companies Act 2013. The current print skips straight from issue at premium to issue for consideration other than cash.

- The Glossary now lists 18 key terms (added: Sweat Equity Shares, ESOP, Private Placement, Rights Issue), all of which surface in 1-mark Assertion-Reason questions.

Three-Day Study Plan for Part 2 Chapter 1 Accounting for Share Capital

A focused 3-day plan covers the entire 88 to 92 page chapter at board-exam depth.

| Day | NCERT Sections | Output |

|---|---|---|

| Day 1 (3 hrs) | 5.1 to 5.4 + first 6 Illustrations of 5.5 | One-page summary of share capital classes; 1-mark MCQ drill |

| Day 2 (3 hrs) | Illustrations 7 to 15 (premium, over-subscription, pro-rata, calls in arrears / advance) | 3 journal-entry problems in Cash Book format |

| Day 3 (3 hrs) | Illustrations 16 to 25 (forfeiture, re-issue) + 8 Numerical Questions | Capital Reserve calculation for 5 forfeiture-reissue cases |

Class 12 Accountancy Chapter Weightage Snapshot

Across the 10-chapter Class 12 Accountancy book (4 chapters of Part 1 Partnership + 6 chapters of Part 2 Company Accounts), Part 2 Chapter 1 ties with Chapter 2 for the highest single-chapter weightage. The board paper consistently allocates 8 to 10 marks here.

| Chapter | Title | CBSE Marks |

|---|---|---|

| 1 | Accounting for Partnership: Basic Concepts | 6 to 8 |

| 2 | Reconstitution: Admission of a Partner | 8 to 10 |

| 3 | Reconstitution: Retirement / Death of a Partner | 8 to 10 |

| 4 | Dissolution of Partnership Firm | 6 to 8 |

| 5 | Accounting for Share Capital | 8 to 10 |

| 6 | Issue and Redemption of Debentures | 6 to 8 |

| 7 | Financial Statements of a Company | 6 |

| 8 | Analysis of Financial Statements | 4 to 6 |

| 9 | Accounting Ratios | 6 to 8 |

| 10 | Cash Flow Statement | 6 |

Related Resources for Class 12 Accountancy Part 2 Chapter 1

- Class 12 Accountancy Part 2 Chapter 1 NCERT Solutions PDF

- Class 12 Accountancy Part 2 Chapter 1 Revision Notes

- Class 12 Accountancy Part 2 Chapter 1 Handwritten Notes PDF

- CBSE Class 12 Accountancy Syllabus 2026-27

NCERT Book PDF for Class 12 Accountancy: All Chapters

| Chapter | Title |

|---|---|

| Chapter 1 | Accounting for Partnership: Basic Concepts NCERT Book PDF |

| Chapter 2 | Reconstitution: Admission of a Partner NCERT Book PDF |

| Chapter 3 | Reconstitution: Retirement / Death of a Partner NCERT Book PDF |

| Chapter 4 | Dissolution of Partnership Firm NCERT Book PDF |

| Part 2 Chapter 2 | Issue and Redemption of Debentures NCERT Book PDF |

| Part 2 Chapter 3 | Financial Statements of a Company NCERT Book PDF |

| Part 2 Chapter 4 | Analysis of Financial Statements NCERT Book PDF |

| Part 2 Chapter 5 | Accounting Ratios NCERT Book PDF |

| Part 2 Chapter 6 | Cash Flow Statement NCERT Book PDF |

FAQs on Class 12 Accountancy Part 2 Chapter 1 Accounting for Share Capital NCERT Book PDF

Ques. Is the NCERT Class 12 Accountancy Part 2 Chapter 1 PDF on this page the latest 2026-27 edition?

Ans. Yes. The PDF hosted here is the Reprint 2026-27 of NCERT Accountancy Part 2, downloaded directly from the official NCERT publication. It is aligned to the CBSE 2026-27 Accountancy syllabus and the Companies Act 2013 references match the current statute. Older editions still in private circulation print the discontinued Issue of Shares at a Discount section, which is not valid for the 2026 board paper.

Ques. How many marks does Accounting for Share Capital carry in the CBSE Class 12 board exam?

Ans. Part 2 Chapter 1 typically carries 8 to 10 marks in the 80-mark Class 12 Accountancy board paper. The structure is almost always one 8-mark numerical question on issue of shares (pro-rata allotment, premium, forfeiture or re-issue) plus 1 to 2 marks of theory or Assertion-Reason on share capital classes or Securities Premium.

Ques. What is the difference between Authorised, Issued, Subscribed and Paid-up Capital?

Ans. Authorised Capital is the maximum capital a company can raise per its Memorandum of Association. Issued Capital is the portion the company offers to the public. Subscribed Capital is the part the public actually applies for. Called-up Capital is the portion the company has demanded from shareholders so far, and Paid-up Capital is the part shareholders have actually paid. Part 2 Chapter 1 Section 5.3 of the NCERT PDF gives the full schedule with a numerical Illustration.

Ques. Has Issue of Shares at Discount been removed from the NCERT Class 12 Accountancy Part 2 Chapter 1?

Ans. Yes. Section 53 of the Companies Act 2013 prohibits the issue of shares at a discount, so the NCERT removed that sub-section from Part 2 Chapter 1 starting with the rationalised edition. The Reprint 2026-27 print on this page reflects this removal. The only related concept retained is re-issue of forfeited shares at a discount, which is permitted because the original loss has already been absorbed via the Share Capital A/c.

Ques. How are forfeited shares accounted for when they are re-issued?

Ans. When forfeited shares are re-issued, the discount allowed on re-issue is debited to the Share Forfeiture A/c. The remaining balance in the Share Forfeiture A/c, after writing off the discount, is transferred to Capital Reserve. The board paper tests this calculation almost every year. The detailed worked solution is in Illustrations 22 to 25 of Section 5.5 of the NCERT PDF.

Comments