These cash flow statement notes class 12 condense the final chapter of Accountancy Part-II (Financial Statements of Companies) into an exam-ready revision document built around AS-3 (Revised) and the indirect-method format prescribed under Schedule III of the Companies Act, 2013. The chapter carries a high probability of appearing as a long 6-mark question in the CBSE Board paper, and this revision guide tracks every adjustment a student is expected to handle in a 60-minute writing slot. Aligned to the 2026-27 NCERT (Reprint 2026-27), with a 26-page printable PDF bundled below.

- CBSE Weightage: 6 marks (Part B, Financial Statement Analysis cluster); compulsory question almost every year

- Time to Read: 90 to 110 minutes for full coverage with the solved illustration

These notes are curated by Chartered Accountants and Commerce educators, mapped to the 2026-27 NCERT Accountancy Part-II textbook, and refined against the last seven years of CBSE Class 12 Board papers.

Also Check:

- Cash Flow Statement Class 12 NCERT Solutions

- Accounting Ratios Class 12 Accountancy Notes

- CBSE Class 12 Accountancy Syllabus 2026-27

Cash Flow Statement Notes Class 12: Why This Chapter Decides Your Board Score

The Cash Flow Statement is the single largest standalone question in the Class 12 Accountancy paper, with a guaranteed 6-mark numerical appearing in every CBSE Board paper since 2013. Unlike the Accounting Ratios chapter where partial credit is easy, the cash flow numerical is graded for the closing cash balance reconciling exactly with the figure given in the comparative balance sheet, so the answer is either correct or substantially penalised. The cash flow statement notes class 12 revision PDF below treats every AS-3 classification rule, every non-cash adjustment, and every working note format that the CBSE marking scheme expects to see written down in the answer book.

Class 12 Accountancy Part 2 Chapter 6 Cash Flow Statement Notes

Source: Commerce and Fun on YouTube

How will Collegedunia's NCERT Notes Help with Cash Flow Statement?

- Every AS-3 classification rule is presented as a one-line decision: which activity does this item belong to, and what is the CBSE-accepted reasoning.

- The indirect-method workflow is broken into a fixed 7-step protocol that fits on a single A4 sheet and can be reproduced verbatim under exam pressure.

- Non-cash items (depreciation, goodwill written off, amortisation), non-operating items (interest, dividend, profit/loss on sale of fixed assets), and working-capital adjustments each get their own checklist.

- The treatment of provision for tax and proposed dividend (the two most common errors flagged by CBSE evaluators) is given in both the simplified and the complete formats.

- A complete solved illustration runs from the comparative balance sheet to the final Net Increase/Decrease in Cash, matching the exact layout the CBSE marking scheme rewards.

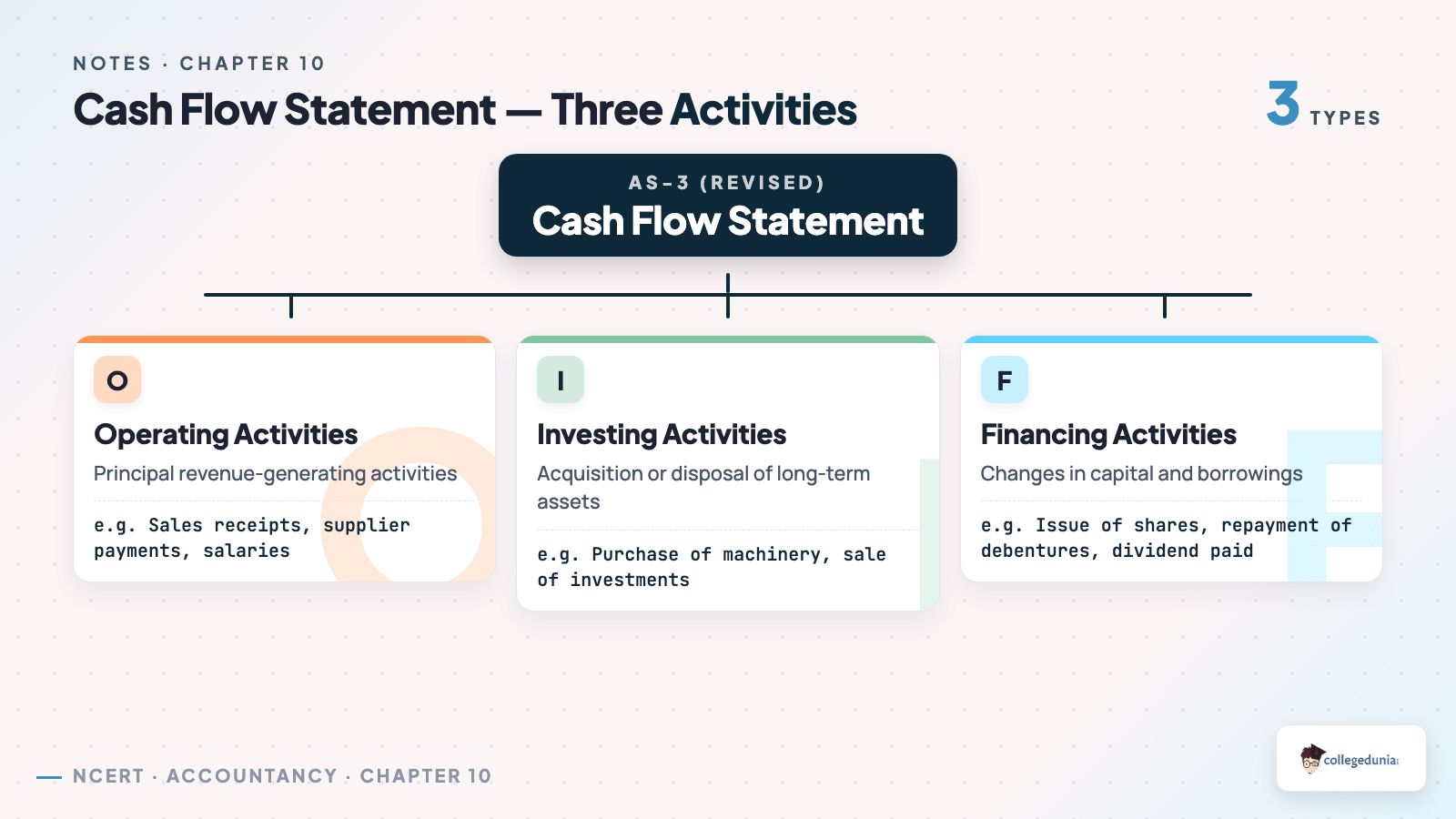

Meaning of Cash Flow Statement and Objectives under AS-3 (Revised)

A Cash Flow Statement is a financial statement that reports the inflows and outflows of Cash and Cash Equivalents during an accounting period, classified under three activities prescribed by Accounting Standard 3 (Revised): Operating, Investing, and Financing. Cash Equivalents are short-term, highly liquid investments readily convertible into known amounts of cash and subject to insignificant risk of change in value (original maturity of three months or less from the date of acquisition).

The objectives the CBSE answer should mention when a 3-mark theory question is asked are summarised below.

| Objective | What it tells the reader |

|---|---|

| Liquidity assessment | Ability of the enterprise to generate cash for short-term obligations |

| Solvency assessment | Long-term repayment capacity, especially for debentures and term loans |

| Reconciling profit with cash | Bridges Net Profit (accrual) with Net Cash from Operations (cash basis) |

| Forecasting | Helps in projecting future cash budgets and dividend capacity |

AS-3 Classification: Operating, Investing, and Financing Activities

The classification of every line item under one of the three activities is the highest-frequency 1-mark or 3-mark theory question in this chapter. The rule of thumb stated in the notes: ask what generated the cash flow, not what it ended up funding. Sale of machinery is investing regardless of whether the proceeds were used to pay creditors.

| Activity | Definition | Typical Items |

|---|---|---|

| Operating | Principal revenue-producing activities; not investing or financing | Cash from customers, payments to suppliers, wages, operating expenses, income tax paid |

| Investing | Acquisition and disposal of long-term assets and other investments not included in cash equivalents | Purchase/sale of fixed assets, purchase/sale of non-current investments, interest received, dividend received (non-finance company) |

| Financing | Activities that change the size and composition of owner's capital and borrowings | Issue of shares, issue/redemption of debentures, long-term loans, dividend paid, interest paid on borrowings |

Cash Flow Statement Indirect Method: The 7-Step Protocol

The indirect method is the only method CBSE asks about. The direct method is excluded from the 2026-27 syllabus. The seven steps below are the spine of every full numerical and should be written as working notes in the answer book, since the marking scheme awards step marks even when the closing figure is wrong.

- Start with Net Profit before Tax and Extraordinary Items. Add back current-year tax provision and proposed dividend (if treated as appropriation).

- Add non-cash items: depreciation, goodwill written off, preliminary expenses written off, loss on sale of fixed assets, provision for doubtful debts created.

- Deduct non-operating gains: profit on sale of fixed assets, profit on sale of investments, interest received, dividend received.

- Adjust for changes in working capital: increase in current assets and decrease in current liabilities are deducted; decrease in current assets and increase in current liabilities are added.

- Deduct income tax paid to arrive at Net Cash from Operating Activities.

- Compute Net Cash from Investing Activities using the fixed assets ledger and the non-current investments ledger (always prepare these working notes).

- Compute Net Cash from Financing Activities, then reconcile total of (A) plus (B) plus (C) with the change in Cash and Cash Equivalents between opening and closing balance sheets.

Cash Flow Statement Class 12 Notes: Treatment of Tricky Items

The four items below account for the majority of evaluator-flagged errors in CBSE Class 12 Accountancy answer books. The notes give the complete ledger format for each, but the summary table is shown here for rapid revision.

| Item | Treatment | Activity |

|---|---|---|

| Provision for Tax | Add back current-year provision to Net Profit; deduct tax paid (prepare Provision for Tax A/c) | Operating |

| Proposed Dividend (current year) | Disclosed as contingent liability under AS-4 (Revised); previous-year proposed dividend paid is treated as Financing outflow | Financing (when paid) |

| Sale of Fixed Asset | Sale proceeds in Investing; profit removed from Operating, loss added back to Operating | Investing |

| Interim Dividend | Already paid during the year; full outflow under Financing | Financing |

What's Inside the Cash Flow Statement Class 12 Revision PDF

- Concept boxes for AS-3 (Revised), Cash, Cash Equivalents, and the three-activity classification.

- Format templates for the indirect method, Provision for Tax A/c, Accumulated Depreciation A/c, and Fixed Assets A/c.

- Comparative chart Operating vs Investing vs Financing for finance and non-finance companies.

- Solved illustration running from the comparative balance sheet to the closing cash reconciliation.

- Quick recall card for the seven-step indirect-method protocol.

- Common mistakes checklist drawn from the 2018 to 2025 CBSE marking schemes.

- Practice problem set with four self-study numericals and an answer key.

Common Mistakes Students Make in Cash Flow Statement Numericals

- Treating depreciation as an investing outflow. It is a non-cash item; add it back to Net Profit under Operating.

- Routing proposed dividend of the current year as an outflow. It is only a contingent liability; only previous-year proposed dividend paid this year is shown as a Financing outflow.

- Forgetting to deduct profit on sale of fixed assets from Operating while also including sale proceeds under Investing (double counting).

- Adjusting working capital changes using closing balances instead of differences between opening and closing.

- Showing interest and dividend received under Operating for a manufacturing or trading company (should be Investing).

- Skipping the Provision for Tax A/c working note and treating the provision figure as tax paid.

Cash Flow Statement Previous Year Trend: Class 12 CBSE Board

The chapter is one of the most stable scoring blocks in the Class 12 paper. The pattern over the last five board sittings is summarised below for revision priority.

| Year | Question Type | Marks |

|---|---|---|

| 2025 | Full CFS by indirect method with proposed dividend treatment | 6 |

| 2024 | Classification of items into three activities; partial CFS | 3 plus 4 |

| 2023 | Full CFS with Provision for Tax and interim dividend | 6 |

| 2022 (Term 2) | Calculation of Cash from Operating Activities only | 5 |

| 2020 | Full CFS with sale of machinery and revaluation reserve | 6 |

Full year-wise PYQ map: Cash Flow Statement Class 12 NCERT Solutions on Collegedunia carries the complete solved board questions from 2018 to 2025.

Related Resources for Cash Flow Statement Class 12 Accountancy

- Cash Flow Statement Class 12 NCERT Solutions

- Cash Flow Statement Class 12 Handwritten Notes

- Cash Flow Statement Class 12 NCERT Book PDF

NCERT Notes for Class 12 Accountancy: All Chapters

| Chapter | Chapter Title and Notes |

|---|---|

| Chapter 1 | Accounting for Partnership: Basic Concepts Notes |

| Chapter 2 | Reconstitution: Admission of a Partner Notes |

| Chapter 3 | Reconstitution: Retirement/Death of a Partner Notes |

| Chapter 4 | Dissolution of Partnership Firm Notes |

| Part 2 Chapter 1 | Accounting for Share Capital Notes |

| Part 2 Chapter 2 | Issue and Redemption of Debentures Notes |

| Part 2 Chapter 3 | Financial Statements of a Company Notes |

| Part 2 Chapter 4 | Analysis of Financial Statements Notes |

| Part 2 Chapter 5 | Accounting Ratios Notes |

FAQs on Cash Flow Statement Class 12 Accountancy Notes

FAQs on Cash Flow Statement Class 12 Accountancy Notes

Ques. Is Cash Flow Statement compulsory in Class 12 Board exam?

Ans. Yes. Part 2 Chapter 6 has carried a compulsory 6-mark numerical in every CBSE Class 12 Accountancy paper since 2013. The 2026-27 syllabus retains the chapter as part of the Part B Financial Statement Analysis cluster.

Ques. What is the difference between Cash Flow and Fund Flow Statement?

Ans. Cash Flow Statement reports changes in Cash and Cash Equivalents during a period; Fund Flow Statement reports changes in Working Capital. CBSE 2026-27 syllabus excludes Fund Flow Statement; only Cash Flow Statement is examinable.

Ques. Why is depreciation added back in the Cash Flow Statement?

Ans. Depreciation is a non-cash expense that has already been deducted while computing Net Profit. Since no actual cash outflow occurred, it is added back to Net Profit before Tax to arrive at cash-basis operating profit under the indirect method.

Ques. How is proposed dividend treated under the 2026-27 syllabus?

Ans. Proposed dividend of the current year is treated as a contingent liability under AS-4 (Revised) and is not shown as an outflow. Only the proposed dividend of the previous year, which has been declared and paid during the current year, is shown as a Financing Activity outflow.

Ques. Where is interest paid on debentures classified?

Ans. For a non-finance company, interest paid on debentures and other borrowings is classified under Financing Activities. For a finance company (bank, NBFC), the same interest paid is classified under Operating Activities because lending and borrowing constitute its principal revenue-producing activity.

Ques. How long should Cash Flow Statement notes take to revise before the board exam?

Ans. A focused revision pass of 90 to 110 minutes is sufficient when the seven-step indirect-method protocol has been internalised. The Collegedunia revision PDF is designed around this timing block and includes a one-page recall card for the final week before the exam.

Comments