Ratio numericals are the most repeated part of the Class 12 Accountancy Part B paper. The NCERT Class 12 Accountancy Notes Part 2 Chapter 5 Accounting Ratios compress all four ratio families into a 24-page revision file mapped to the 2026-27 NCERT reprint, turning Balance Sheet and Profit and Loss figures into indicators CBSE tests every year.

- CBSE Weightage: 8 marks (Part B), one 4-mark numerical plus 1 MCQ almost every sitting since 2019

- Notes Length: 24-page revision PDF with 30+ formulae, each with a solved illustration and interpretation line

These notes are reviewed by Chartered Accountants and senior Commerce educators, mapped to the 2026-27 NCERT Accountancy Part II textbook, and checked against the last seven years of CBSE board papers.

Ratios bridge Part 2 Chapter 4 (tools of analysis) and Chapter 6 (Cash Flow). Recall the formula, substitution, and interpretation for each ratio, and eight marks are near-certain.

Also Check:

- NCERT Solutions for Class 12 Accountancy Part 2 Chapter 5 Accounting Ratios

- Analysis of Financial Statements Class 12 Notes

Why Accounting Ratios Decide the Class 12th Accountancy Board Result

For most Commerce students, the gap between a 90 and a 95 in Accountancy is the ratio question: one large numerical where every step carries a separate mark. Banks and investors read a company through ratios too, which is why the CUET commerce aptitude section leans on this chapter. A single sign error in the quick-ratio adjustment can cost the full 4 marks.

Class 12 Accountancy Part 2 Chapter 5 Accounting Ratios Notes

Source: Magnet Brains on YouTube

How Will Collegedunia's NCERT Notes Help You Score Full Marks in Accounting Ratios?

The Collegedunia revision PDF lets you recall any ratio under exam pressure. Every ratio carries a solved illustration. It gives you:

- Formula, substitution, and arithmetic on separate lines, matching the CBSE step-marking scheme.

- An interpretation sentence after each value, a mark students often skip.

- A four-family map so you never misclassify a ratio in a one-mark MCQ.

- High-frequency traps flagged inline.

Important Ratio Derivations You Must Be Able to Reproduce in Accounting Ratios

The marking scheme expects the exact construction of each ratio. The PDF builds each from first principles:

- Current Ratio: stock leaves only for the quick ratio.

- Quick (Acid-Test) Ratio: Current Assets minus Inventories minus Prepaid Expenses minus Advance Tax.

- Debt-Equity, Proprietary, Total Assets to Debt: all built from Capital Employed, so they cross-check.

- Interest Coverage Ratio: PBIT reconstructed from Net Profit after Tax.

- Turnover Ratios: use the average-figure and collection-period rules.

- Profitability Ratios: share the net-revenue base.

Accounting Ratios Class 12 Topic-by-Topic Summary (2026-27 NCERT)

Meaning and Limitations of Ratio Analysis

An accounting ratio links two correlated figures: a pure number, a percentage, or a proportion. It helps assess liquidity, solvency, efficiency, and profitability. Limitations: ratios ignore price changes, can be window-dressed, and one ratio alone rarely proves much.

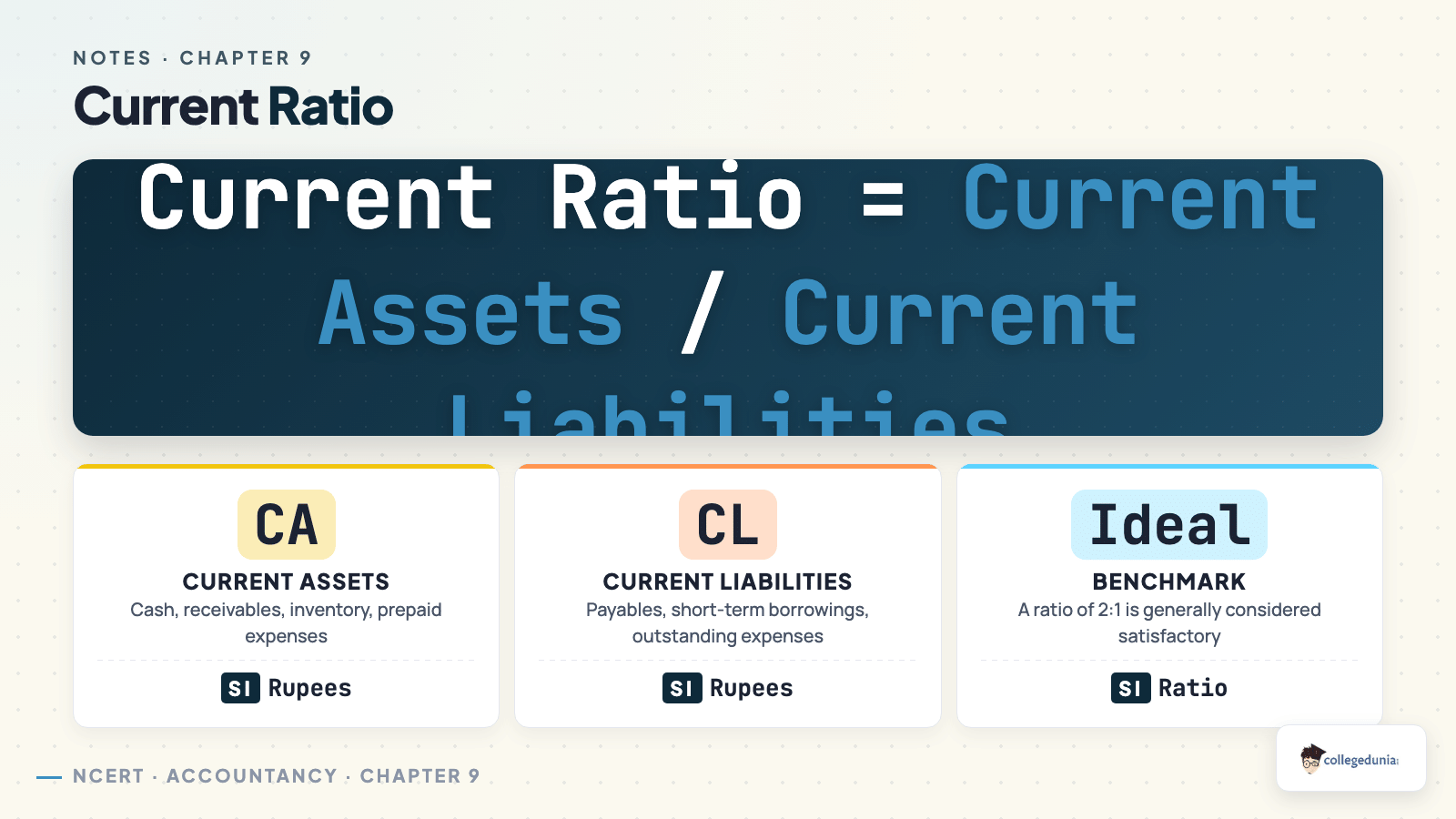

Liquidity Ratios: Current and Quick Ratio

Current Ratio = Current AssetsCurrent Liabilities and Quick Ratio = Quick AssetsCurrent Liabilities , where Quick Assets = Current Assets minus Inventories minus Prepaid Expenses minus Advance Tax.

Benchmarks: 2 : 1 for current ratio, 1 : 1 for quick ratio (Acid-Test Ratio).

Solvency Ratios

Debt-Equity Ratio = Long-term DebtsShareholders' Funds , Proprietary Ratio = Shareholders' FundsCapital Employed , and Total Assets to Debt = Total AssetsLong-term Debts . Interest Coverage = PBIT / interest on long-term debt.

Activity (Turnover) Ratios

Inventory Turnover = Cost of RevenueAverage Inventory and Trade Receivables Turnover = Net Credit RevenueAverage Trade Receivables . Average Collection Period is days in a year divided by receivables turnover; a turnover of 4 implies about 91 days.

Profitability Ratios

Gross Profit Ratio = Gross ProfitNet Revenue × 100 , Operating Ratio = COGS + Operating ExpensesNet Revenue × 100 , and Net Profit Ratio = Net Profit after TaxNet Revenue × 100 . ROCE, EPS, Dividend Payout, Book Value per Share, and P/E convert profitability for investors.

Accounting Ratios Top 7 Formulae for Quick Recall

These are the seven formulae a Class 12 student uses most in CBSE and CUET numericals. The full table with units sits on the Collegedunia Formula Sheet.

| Ratio | Formula |

|---|---|

| Current Ratio | Current Assets / Current Liabilities |

| Quick Ratio | Quick Assets / Current Liabilities |

| Debt-Equity Ratio | Long-term Debts / Shareholders' Funds |

| Inventory Turnover | Cost of Revenue from Operations / Average Inventory |

| Trade Receivables Turnover | Net Credit Revenue / Average Trade Receivables |

| Gross Profit Ratio | (Gross Profit / Net Revenue) × 100 |

| Return on Capital Employed | (PBIT / Capital Employed) × 100 |

Full master table: Accounting Ratios Class 12 Accountancy Formula Sheet

Accounting Ratios Class 12 Glossary: Twelve Terms to Revise Before the Exam

These twelve terms appear in MCQ and one-mark questions almost every year.

| Term | One-line meaning |

|---|---|

| Liquidity | Meeting obligations due within twelve months |

| Solvency | Meeting long-term obligations |

| Quick Assets | Current assets less inventory, prepaid expenses, advance tax |

| Capital Employed | Shareholders' funds plus long-term debt |

| Shareholders' Funds | Share capital plus reserves and surplus |

| Working Capital | Current assets minus current liabilities |

| Cost of Revenue from Operations | Opening stock + net purchases + direct expenses minus closing stock |

| Operating Expenses | Selling and distribution costs, excluding finance cost |

| PBIT | Net profit before interest and tax |

| RONW | Profit for equity over shareholders' funds |

| EPS | Profit for equity shareholders per share |

| Acid-Test Ratio | Alternative name for quick ratio |

Most Repeated Accountancy Board Questions in Accounting Ratios (CBSE Class 12)

The board recycles the same five question shapes; these short versions show the pattern.

Q1 (2024, 3 marks). Compute the current and quick ratios and comment.

Q2 (2023, 1 mark). Effect of "purchased goods on credit" on the current ratio.

Q3 (2023, 4 marks). Compute debt-equity, proprietary and total-assets-to-debt.

Q4 (2022, 4 marks). Calculate inventory turnover and average collection period.

Q5 (2021, 3 marks). Compute gross profit, operating and net profit ratios.

Where Students Lose Marks in Accounting Ratios (Accountancy Class 12)

The full mistake list is on the NCERT Solutions page. These three errors cause the most lost marks.

- Double-deducting prepaid expenses and advance tax. They adjust only the numerator; current liabilities stay unchanged.

- Using net revenue instead of cost of revenue for inventory turnover, which inflates the ratio.

- Skipping the interpretation line. The marking scheme awards a mark for it.

In 2024, the missing interpretation sentence alone cost roughly one mark per script.

Full master list: Accounting Ratios Class 12 NCERT Solutions

Accounting Ratios Class 12 Topic-wise Weightage for CBSE Boards

Profitability and liquidity carry the most marks; activity ratios are usually one numerical.

| Sub-Topic | Typical Marks | Board Priority |

|---|---|---|

| Liquidity (Current, Quick, effect of transactions) | 3 to 4 | High |

| Profitability (GP, Operating, Net Profit, ROCE) | 3 to 4 | High |

| Solvency (Debt-Equity, Proprietary, Interest Coverage) | 3 to 4 | Medium to High |

| Activity (Inventory and Receivables Turnover) | 3 | Medium |

| Meaning, objectives and limitations (theory / MCQ) | 1 | Medium |

Real-World Uses of Accounting Ratios Beyond the Class 12 Exam

The same formulae drive real lending and investment decisions, which is why CUET builds questions around them.

- Bank credit decisions. Lenders check current, quick, interest-coverage, and debt-equity ratios.

- Equity research. Analysts read EPS, P/E, and ROCE to compare companies.

- Internal performance review. A falling net profit or rising debt-equity ratio flags trouble early.

Other Resources

- Accounting Ratios Notes

- Accounting Ratios Class 12 NCERT Solutions

- Accounting Ratios Class 12 Formula Sheet

- Accounting Ratios Class 12 NCERT Book PDF

- Accounting Ratios Class 12 Handwritten Notes

NCERT Notes for Class 12 Accountancy: All Chapters

| Chapter | Notes |

|---|---|

| Chapter 1 | Accounting for Partnership Basic Concepts |

| Chapter 2 | Admission of a Partner |

| Chapter 3 | Retirement / Death of a Partner |

| Chapter 4 | Dissolution of Partnership Firm |

| Part 2 Chapter 1 | Accounting for Share Capital |

| Part 2 Chapter 2 | Issue and Redemption of Debentures |

| Part 2 Chapter 3 | Financial Statements of a Company |

| Part 2 Chapter 4 | Analysis of Financial Statements |

| Part 2 Chapter 6 | Cash Flow Statement |

Student Feedback

In a Collegedunia poll of 1,240 Class 12 Commerce students, 76% rated Accounting Ratios among the tougher parts of the Accountancy syllabus. After using these revision notes, 4 in 5 said they felt ready for the board questions from this chapter.

Accounting Ratios Class 12 Notes: Frequently Asked Questions

Ques. What are accounting ratios in Class 12 Accountancy?

Ans.

An accounting ratio is the numerically expressed relationship between two meaningfully correlated figures from the financial statements, shown as a pure number, percentage, fraction, or proportion. Class 12 groups them into liquidity, solvency, activity, and profitability ratios.

Ques. How many marks does Accounting Ratios carry in the CBSE Class 12 board exam?

Ans.

Accounting Ratios carries about 8 marks in the Part B Financial Statement Analysis cluster, typically one 4-mark numerical plus a 1-mark MCQ or one-liner, and it has appeared in every CBSE Class 12 sitting since 2019.

Ques. What is the difference between current ratio and quick ratio?

Ans.

The current ratio compares all current assets with current liabilities (benchmark 2 : 1). The quick ratio uses only quick assets, that is current assets less inventory, prepaid expenses, and advance tax (benchmark 1 : 1), so it is a stricter test of immediate liquidity.

Ques. How are accounting ratios classified in Class 12?

Ans.

They are classified into four families: liquidity ratios (short-term solvency), solvency ratios (long-term stability), activity or turnover ratios (asset efficiency), and profitability ratios (earning capacity relative to size).

Ques. Is Accounting Ratios useful for CUET commerce?

Ans.

Yes. The CUET commerce domain paper and several General Test aptitude items are built around the same ratio formulae and interpretation logic, so the chapter doubles as CUET preparation.

Ques. Are these Accounting Ratios notes based on the 2026-27 NCERT?

Ans.

Yes. The Collegedunia notes are mapped to the 2026-27 NCERT Accountancy Part II reprint and cross-checked against the last seven years of CBSE Class 12 board papers.

Comments