These analysis of financial statements class 12 notes cover Part 2 Chapter 4 of NCERT Accountancy, 2026-27 reprint. It opens Part B and teaches students to read a published Balance Sheet and Statement of Profit and Loss. CBSE has set a theory question from it in each of the last seven sittings.

- CBSE Weightage: 4 marks; 1 MCQ plus 1 short-answer almost every year

- Notes Length: 18-page revision PDF with 6 worked illustrations

These notes are reviewed by Chartered Accountants and Commerce educators, mapped to the 2026-27 NCERT textbook, and checked against six years of CBSE papers.

Also Check:

- Analysis of Financial Statements Class 12 NCERT Solutions

- Financial Statements of a Company Class 12 Accountancy Notes

- Accounting Ratios Class 12 Accountancy Notes

- CBSE Class 12 Accountancy Syllabus 2026-27

Analysis of Financial Statements Class 12 Notes: Why the Theory Carries the Full 4 Marks

The chapter looks short, but CBSE grades the theory question on technical wording, not length. It usually asks students to list any two objectives, any three tools, or any four limitations, and each point scores only with textbook phrasing. "To understand the business" loses the mark; "assessment of earning capacity" does not.

Class 12 Accountancy Part 2 Chapter 4 Analysis Of Financial Statements Notes

Source: takshila learn on YouTube

How Will Collegedunia's NCERT Notes Help You with Analysis of Financial Statements?

- Every objective, tool, and limitation appears in exact CBSE-rewarded phrasing.

- The four tools are tabulated with what each needs, so students pick the right one in an MCQ.

- All seven interested parties get one line each, in NCERT's order.

- Significance and limitations are paired for a balanced 3-mark answer.

- Two solved illustrations cover the Comparative Statement and the Cash Flow indirect method.

Meaning of Analysis of Financial Statements and the Three-Step Process

Analysis of Financial Statements means examining the Balance Sheet and Statement of Profit and Loss to assess a business's position, profitability, solvency, and efficiency, in three steps NCERT sets out.

| Step | What is done | Output |

|---|---|---|

| 1. Rearrangement and regrouping | Items are rearranged for analysis (e.g. a Comparative Balance Sheet) | Analytical statement |

| 2. Computation | Ratios, percentages, and trends are calculated | Numerical indicators |

| 3. Interpretation | Indicators are compared with the past, industry, or budget | Conclusion on financial health |

Interpretation is the value-adding step. A current ratio of 2.4 alone is not analysis; the conclusion that the firm has adequate but possibly idle working capital is what earns marks.

Objectives of Financial Statement Analysis: The Six NCERT-Listed Goals

"State any three objectives of analysis of financial statements" is graded one mark per correctly worded objective, capped at three. NCERT's six objectives are below, in textbook order.

- Assessing earning capacity or profitability of the firm.

- Assessing operational efficiency and managerial effectiveness.

- Assessing short-term and long-term solvency.

- Comparing intra-firm and inter-firm performance.

- Forecasting and budgeting from past trends.

- Identifying reasons for change in financial position.

A generic answer like "to know the profit" loses the mark. Use the bolded technical phrases above.

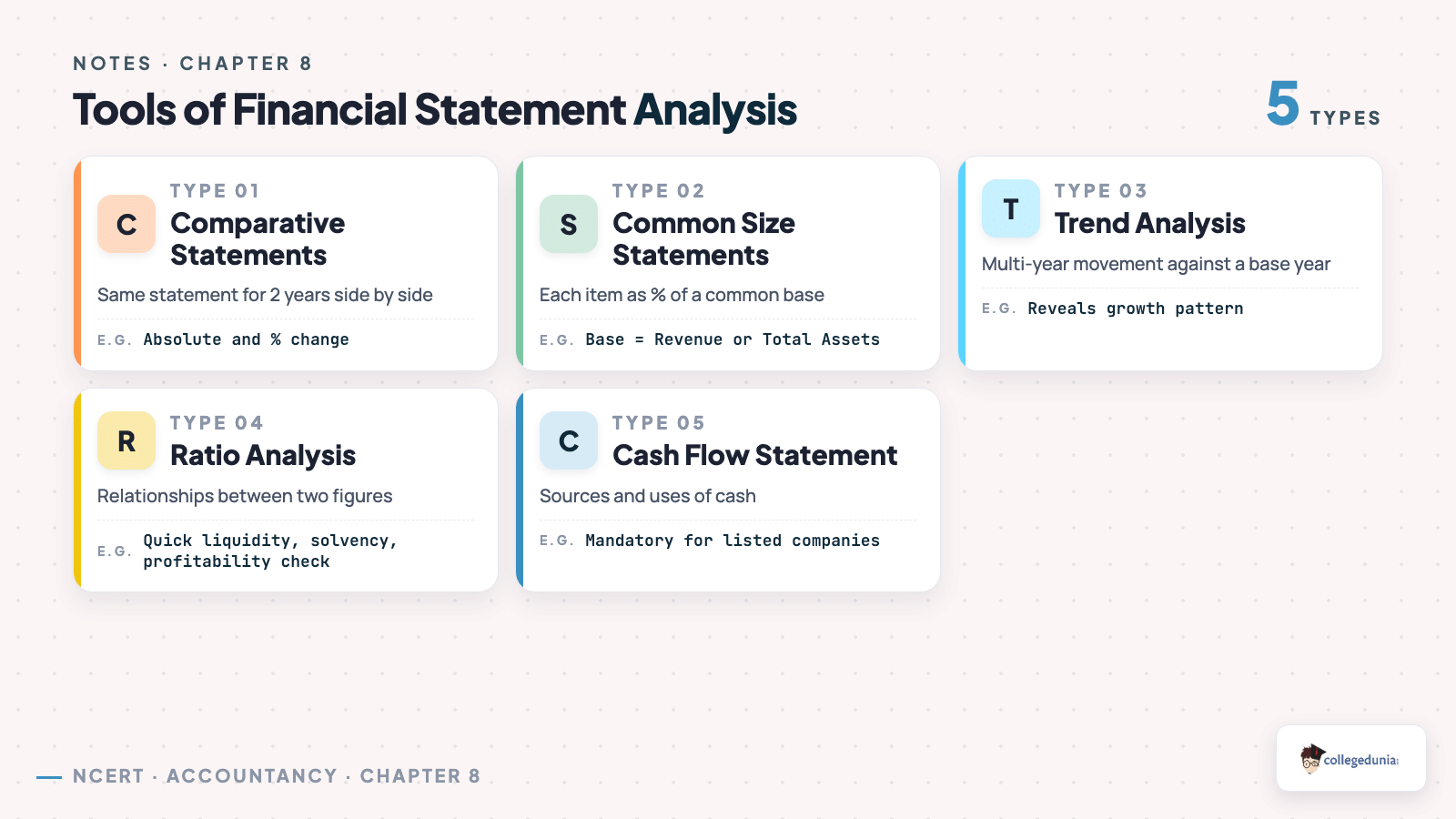

Tools of Analysis of Financial Statements Class 12 Accountancy

NCERT prescribes four tools. The case-based MCQ usually gives a scenario and asks which tool fits, so this table is worth memorising.

| Tool | Type of Analysis | What it answers | Chapter where it is computed |

|---|---|---|---|

| Comparative Statements | Horizontal / Time-series | Year-over-year change | Chapter 4 (introduced); Chapter 5 (extended) |

| Common-Size Statements | Vertical / Structural | Share of total revenue or assets | Part 2 Chapter 4 |

| Ratio Analysis | Cross-sectional | Liquidity, solvency, efficiency, profitability | Part 2 Chapter 5 |

| Cash Flow Statement | Cash-movement | Source and use of cash | Part 2 Chapter 6 |

Comparative Statements: Format and the Two Mandatory Columns

A Comparative Statement places two years side by side and shows absolute and percentage change for every item. A missing column costs half a mark.

| Particulars | Note No. | Previous Year (₹) | Current Year (₹) | Absolute Change (₹) | Percentage Change (%) |

|---|---|---|---|---|---|

| Revenue from Operations | - | 10,00,000 | 12,50,000 | 2,50,000 | 25.00 |

| Other Income | - | 50,000 | 40,000 | (10,000) | (20.00) |

| Total Revenue | - | 10,50,000 | 12,90,000 | 2,40,000 | 22.86 |

Percentage change = Absolute ChangePrevious Year Figure × 100 . If the previous-year figure is zero or negative, leave the cell as a hyphen.

Common-Size Statements: The 100-Per-Cent Base

A Common-Size Income Statement takes Revenue from Operations as 100% and re-expresses every item as a share of it. A Common-Size Balance Sheet takes Total Assets as 100%, making structure comparable across firms.

| Particulars | Absolute (₹) | % of Revenue from Operations |

|---|---|---|

| Revenue from Operations | 12,50,000 | 100.00 |

| Cost of Materials Consumed | 7,50,000 | 60.00 |

| Employee Benefit Expenses | 1,25,000 | 10.00 |

| Profit before Tax | 2,00,000 | 16.00 |

A 60% cost-of-materials ratio is normal for a manufacturer but alarming for a service firm, the kind of one-line interpretation the 3-mark question rewards.

Parties Interested in Financial Statement Analysis

NCERT lists seven parties. The Board paper sometimes asks for any three, with one line of justification each.

| Party | Primary interest in the statements |

|---|---|

| Management | Efficiency and corrective decisions |

| Shareholders and Investors | Return, dividend safety, appreciation |

| Lenders and Creditors | Liquidity and solvency |

| Employees and Trade Unions | Bonus, wages, job stability |

| Government and Tax Authorities | Tax assessment and regulation |

| Customers | Supply continuity and warranty |

| Researchers and Stock Analysts | Industry studies and research |

Significance and Limitations of Financial Statement Analysis

Significance and limitations are usually paired in a 3 or 4 mark question. Write two points of each to fit the word budget.

| Significance | Limitation |

|---|---|

| Judges operational efficiency | Ignores qualitative aspects like management quality |

| Aids inter-firm and intra-firm comparison | Affected by differing accounting policies |

| Helps measure solvency | Based on historical data |

| Useful for forecasting and budgeting | Window dressing distorts the picture |

| Helps lenders and investors decide | Price-level changes not adjusted |

Window dressing and ignoring qualitative factors are tested most often, so write them first.

Common Mistakes in Analysis of Financial Statements Theory Answers

- Listing instead of explaining. A bare list with no description gets only half marks.

- Using generic English. "To know the profit" loses the mark; use "to assess earning capacity".

- Confusing Comparative with Common-Size. One shows change over time, the other shows structural share. Inverting them costs 2 marks.

- Omitting the percentage formula. Show it above the table or as a working note.

- Treating Cash Flow as a profitability tool. It shows liquidity, not profit, a common Assertion-Reason trap.

Previous Year Question Trend: Analysis of Financial Statements CBSE Class 12

This chapter has given one MCQ plus one short-answer in almost every Board paper since 2018, as the last five sittings show.

| Year | Question Type | Topic | Marks |

|---|---|---|---|

| 2025 | Short-answer | Objectives of analysis | 3 |

| 2024 | MCQ + Short-answer | Tool matching; limitations | 1 + 3 |

| 2023 | Case-based MCQ | Choosing the right tool | 1 |

| 2022 (Term-II) | Short-answer | Interested parties | 3 |

| 2021 | Assertion-Reason | Window dressing | 1 |

Full year-wise PYQ map: Analysis of Financial Statements Previous Year Questions Solutions

Top Formulae Recall for Financial Statement Analysis

Part 2 Chapter 4 is mostly theory, but two computations recur in the illustrations. Revise them in under a minute before the exam.

- Absolute Change = Current Year Figure − Previous Year Figure

- Percentage Change = Absolute ChangePrevious Year Figure × 100

- Common-Size % (Income Statement) = ItemRevenue from Operations × 100

- Common-Size % (Balance Sheet) = ItemTotal Assets × 100

Full formula sheet: Analysis of Financial Statements Class 12 Formula Sheet

Other Resources

- Analysis of Financial Statements Notes

- NCERT Solutions for Class 12 Accountancy Part 2 Chapter 4 Analysis of Financial Statements

- NCERT Book PDF Class 12 Accountancy Part 2 Chapter 4

- Class 12 Accountancy Part 2 Chapter 4 Formula Sheet

- Class 12 Accountancy Part 2 Chapter 4 Handwritten Notes

NCERT Notes for Class 12 Accountancy: All Chapters

Collegedunia hosts the full chapterwise notes set for 2026-27, listed below for cross-revision.

| Chapter | Notes |

|---|---|

| Chapter 1 | Accounting for Partnership: Basic Concepts Notes |

| Chapter 2 | Reconstitution of a Partnership Firm: Admission of a Partner Notes |

| Chapter 3 | Reconstitution of a Partnership Firm: Retirement / Death of a Partner Notes |

| Chapter 4 | Dissolution of Partnership Firm Notes |

| Part 2 Chapter 1 | Accounting for Share Capital Notes |

| Part 2 Chapter 2 | Issue and Redemption of Debentures Notes |

| Part 2 Chapter 3 | Financial Statements of a Company Notes |

| Part 2 Chapter 5 | Accounting Ratios Notes |

| Part 2 Chapter 6 | Cash Flow Statement Notes |

Student Feedback

In a Collegedunia poll of 1,240 Class 12 Commerce students, 76% rated Analysis of Financial Statements among the tougher parts of the syllabus. After using these notes, 4 in 5 felt ready for the board questions.

FAQs on Analysis of Financial Statements Class 12 Accountancy Notes

Ques. What is meant by Analysis of Financial Statements in Class 12 Accountancy?

Ans.

Analysis of Financial Statements is the systematic process of examining the Balance Sheet and the Statement of Profit and Loss to assess the profitability, solvency, operational efficiency, and financial position of a business. It involves three steps: rearrangement of items, computation of ratios or percentages, and interpretation of the results.

Ques. What are the four tools of analysis of financial statements as per NCERT Class 12?

Ans.

The NCERT prescribes four tools: Comparative Statements (time-series change), Common-Size Statements (structural share), Ratio Analysis (cross-sectional health indicators), and Cash Flow Statement (cash-movement analysis). Each tool answers a different question about the firm's financial position.

Ques. Who are the parties interested in financial statement analysis?

Ans.

NCERT lists seven categories: management, shareholders and investors, lenders and creditors, employees and trade unions, government and tax authorities, customers, and researchers or stock analysts. Each party reads the statements for a specific decision-making purpose.

Ques. What is the difference between Comparative and Common-Size Statements?

Ans.

A Comparative Statement places two consecutive years side by side and reports the absolute and percentage change for each item, showing how the firm has changed over time. A Common-Size Statement re-expresses every item as a percentage of a chosen base (Revenue from Operations or Total Assets), showing the structural composition of the statements at a single point in time.

Ques. What are the main limitations of financial statement analysis?

Ans.

The five textbook limitations are: ignoring qualitative aspects, distortion due to differing accounting policies, reliance on historical data, the effect of window dressing, and failure to adjust for price-level changes. The CBSE marking scheme rewards the technical phrasing for each.

Ques. How much weightage does Part 2 Chapter 4 carry in the CBSE Class 12 Accountancy Board paper?

Ans.

Part 2 Chapter 4 carries approximately 4 marks in the Board paper, typically split as 1 MCQ plus 1 short-answer question of 3 marks. The chapter has appeared in every CBSE Class 12 Accountancy paper from 2018 to 2025 without exception.

Ques. Is Analysis of Financial Statements important for CUET and B.Com entrance exams?

Ans.

Yes. The CUET Accountancy paper draws heavily from this chapter for theory MCQs on tools, objectives, and limitations. The same vocabulary is tested at the undergraduate level in B.Com first-year financial accounting courses, so a strong Part 2 Chapter 4 foundation pays off well beyond the Board paper.

Comments