The NCERT Class 12 Accountancy Notes Part 2 Chapter 2 Issue and Redemption of Debentures compress the entire long-term-debt segment of the Company Accounts unit into a single revision file built around six issue cases, three redemption routes, and the Companies Act, 2013 framework that the CBSE Class 12 question paper now tests every year through a guaranteed 8-mark Long Answer. The notes are mapped to the current 2026-27 NCERT Reprint.

- CBSE Weightage: 8 marks (Part A, Company Accounts unit), every Board paper since 2019

- Notes Length: 22-page revision PDF covering all six issue cases, DRR / DRI rules, and three redemption routes with worked journal entries

Collegedunia’s notes cover the Section 2(30) definition, debentures versus shares, the six issue cases, Section 52 routing of Securities Premium Reserve, writing off Loss on Issue, the 10% DRR rule, the 15% DRI requirement, and redemption through lump-sum, instalments by draw of lots, and open market purchase.

These Notes are reviewed by Chartered Accountants and senior Commerce educators, mapped to the 2026-27 NCERT Accountancy Part B textbook, and cross-checked against the last seven years of CBSE Class 12 Board papers.

Also Check:

- Issue and Redemption of Debentures Class 12 NCERT Solutions

- Accounting for Share Capital Class 12 Accountancy Notes

- CBSE Class 12 Accountancy Syllabus 2026-27

Why Debentures Matter in the Class 12 Accountancy Board Paper

Debentures test three competencies at once: legal framework recall, journal-entry mechanics, and treatment of premium and discount. Examiners have favoured this chapter for a single 8-mark Long Answer in every CBSE Board paper from 2019 to 2025. An average commerce student loses 4 of those 8 marks by mishandling the “Loss on Issue of Debentures” account.

Class 12 Accountancy Part 2 Chapter 2 Issue And Redemption Of Debentures Notes

Source: Magnet Brains on YouTube

How Collegedunia’s NCERT Notes Help You Score the Full 8 Marks on Debentures

The revision file is engineered for the last two days before the Board exam. The six issue cases are laid out as a single comparison matrix, and the three redemption routes are walked through with the journal entries you will be asked to write. The notes also flag the DRR threshold, the DRI deadline of 30 April, and the listed-company exemption list, all of which CBSE has tested as 3-mark direct-recall questions.

- Six-case Issue Matrix on a single page, no page flips during revision

- Journal-entry templates pre-typed for each issue and redemption case

- Rules summarised against the post-2019 Companies Amendment

NCERT Class 12 Accountancy Part 2 Chapter 2 Issue and Redemption of Debentures: Section Map

The notes are organised into eleven blocks so a student can walk top-to-bottom and finish a clean revision in roughly 110 minutes. The Exam Yield column reflects how each block has surfaced in CBSE Board papers from 2021 to 2025.

| Block | What It Covers | Exam Yield |

|---|---|---|

| 1. Meaning and Section 2(30) Definition | Legal definition under Companies Act, 2013 | 1 mark recall |

| 2. Debentures versus Shares | Six axes of difference | 3 marks theory |

| 3. Types of Debentures | Security, redemption, registration, convertibility, priority | 2 to 3 marks |

| 4. Issue for Cash, Six Cases | Par/Premium/Discount crossed with redemption at Par/Premium | Core 4-mark machinery |

| 5. Issue for Consideration other than Cash | Purchase of assets and vendor settlement | 3 to 4 marks |

| 6. Issue as Collateral Security | Two methods of recording | 2 to 3 marks |

| 7. Interest on Debentures and TDS | Half-yearly accrual entries | 3 marks |

| 8. Writing Off Loss on Issue of Debentures | Capital fund versus revenue route | 3 marks |

| 9. Debenture Redemption Reserve and Investment | 25% DRR plus 15% DRI rules | 3 to 4 marks theory |

| 10. Redemption: Lump-Sum, Instalments, Open Market | Three routes with journal entries | 6 to 8 marks |

| 11. Conversion into Shares or New Debentures | Conversion ratio and accounting | 3 marks |

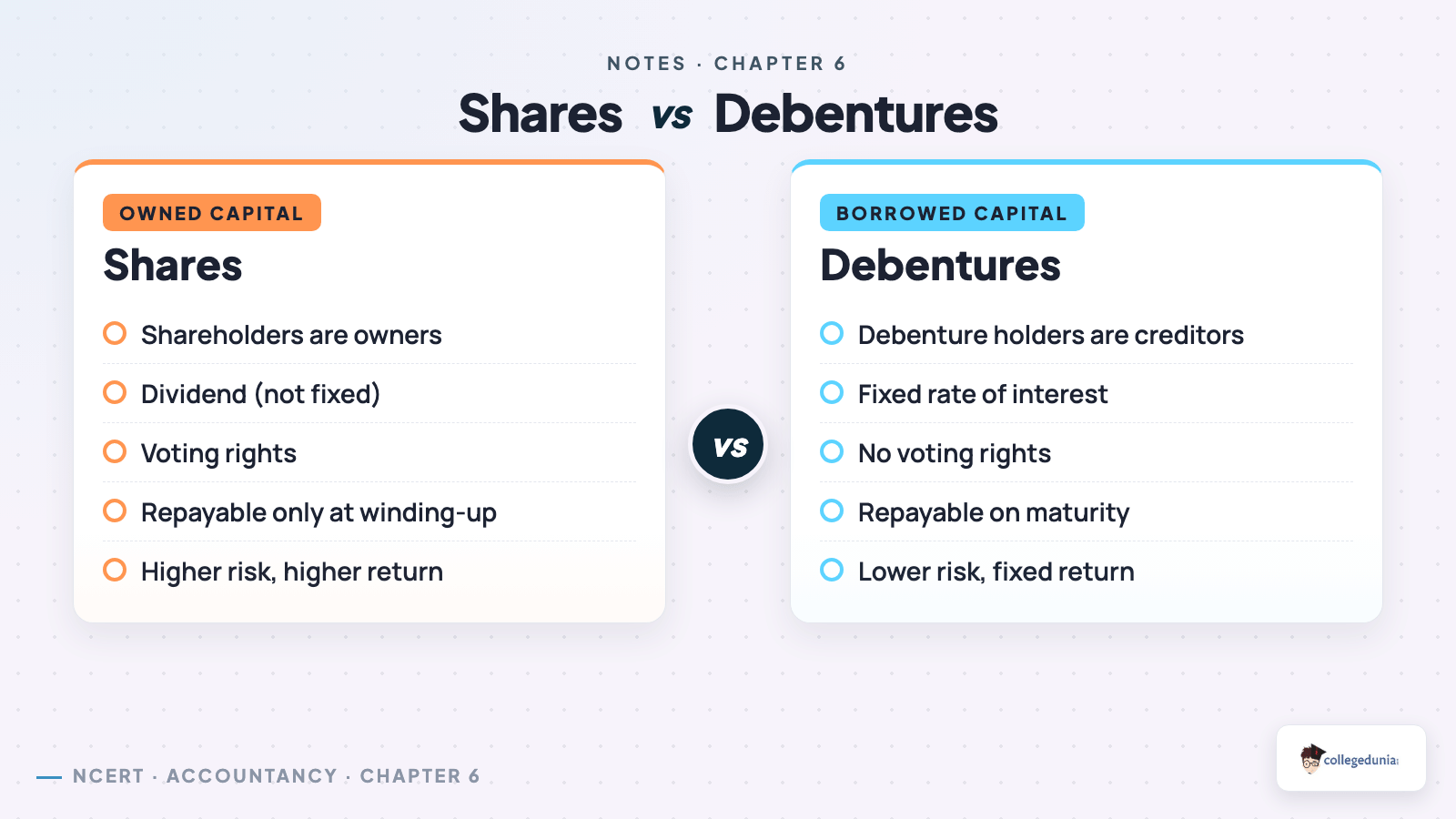

Debentures versus Shares: The Six-Axis Distinction

This comparison is the single most repeated theory question in the Company Accounts unit. It frames why debenture-holders are creditors, not owners, and explains the asymmetric treatment of interest, repayment, and voting rights.

| Basis | Debenture | Share |

|---|---|---|

| Status of Holder | Creditor of the company | Owner of the company |

| Return | Fixed rate of interest, charge against profit | Dividend, appropriation of profit |

| Voting Rights | No voting rights | Voting rights in general meetings |

| Repayment Priority | Repaid before shareholders on winding up | Repaid only after all creditors |

| Issue at Discount | Allowed without restriction | Prohibited under Section 53, except Section 54 Sweat Equity |

| Convertibility | Can be issued as convertible | Equity shares not convertible into debentures |

A debenture-holder is paid even when the company makes a loss; a shareholder is paid only out of distributable profits.

Types of Debentures under the 2026-27 NCERT

- From Security: Secured (charge on assets) and Unsecured (naked).

- From Tenure: Redeemable (specific date) and Irredeemable / Perpetual (no fixed date, rare post-2013).

- From Registration: Registered (name on books) and Bearer (transfer by delivery).

- From Convertibility: Fully Convertible (FCD), Partly Convertible (PCD), Non-Convertible (NCD).

- From Priority: First Mortgage and Second Mortgage debentures.

Issue of Debentures for Cash: The Six-Case Matrix

This matrix is the working heart of the chapter. Every issue problem in the CBSE paper falls into one of these six cases. The pairing of issue terms with redemption terms decides whether Securities Premium or Loss on Issue is debited or credited.

| Case | Issued At | Redeemable At | Special Account Hit |

|---|---|---|---|

| I | Par | Par | None, plain entry |

| II | Premium | Par | Securities Premium Reserve credited |

| III | Discount | Par | Discount on Issue debited |

| IV | Par | Premium | Loss on Issue debited, Premium on Redemption credited |

| V | Premium | Premium | Securities Premium and Loss on Issue both hit |

| VI | Discount | Premium | Discount and Loss on Issue both debited |

- Bank A/c Dr. (with cash received including premium)

- Loss on Issue of Debentures A/c Dr. (with premium payable on redemption)

- To Debentures A/c (with face value)

- To Securities Premium Reserve A/c (with premium received on issue)

- To Premium on Redemption of Debentures A/c (with premium payable on redemption)

Securities Premium Reserve is governed by Section 52 of the Companies Act, 2013, which restricts its use to specific purposes including writing off preliminary expenses, writing off Loss on Issue of Debentures, and providing for the premium payable on redemption.

Issue of Debentures for Consideration other than Cash and as Collateral Security

When a company purchases assets and pays the vendor in debentures, the Vendor A/c is credited at the purchase consideration and the Debentures A/c is credited at face value, with any difference parked in Goodwill, Capital Reserve, Securities Premium Reserve, or Discount on Issue. A purchase consideration of Rs. 9.5 lakh settled by 10,000 debentures of Rs. 100 each at par produces a Rs. 50,000 Discount on Issue.

Collateral security is a secondary security offered to a lender along with the principal security. NCERT recognises two recording methods: no journal entry with a footnote disclosure, or a full journal entry routing through a Debenture Suspense A/c.

Writing Off Loss on Issue of Debentures: The Section 52 Route

Loss on Issue of Debentures arises whenever debentures are issued at a discount or are issued at any price but are redeemable at a premium. It is a capital loss and must be written off in the year of issue itself, against, in this strict order of preference:

- Securities Premium Reserve (Section 52 use);

- Statement of Profit and Loss (if Securities Premium Reserve is insufficient);

The 2026-27 NCERT has dropped the older “deferred amortisation over the life of the debentures” treatment. Loss on Issue is now extinguished in the same financial year. This single change has been a focused 3-mark CBSE question in 2023 and 2024.

Debenture Redemption Reserve and Debenture Redemption Investment

The Companies (Share Capital and Debentures) Amendment Rules, 2019, recast the DRR and DRI framework. The 2026-27 NCERT carries the post-amendment thresholds.

| Company Class | DRR (% of outstanding debentures) | DRI (% of debentures maturing in next FY) |

|---|---|---|

| All India Financial Institutions, Banking Companies | Nil | Nil |

| Listed NBFCs and HFCs | Nil | 15% |

| Other Listed Companies | Nil | 15% |

| Unlisted NBFCs and HFCs | Nil | 15% |

| Unlisted Other Companies | 10% | 15% |

The DRI must be created by 30 April of the year in which the debentures mature. CBSE has asked the “30 April deadline” as a direct 1-mark recall question in 2022 and 2024. Permitted investments are central or state government securities and scheduled-bank deposits.

Redemption of Debentures: The Three Routes

Redemption is the discharge of the company’s liability towards debenture-holders. NCERT recognises three routes, each with a distinct accounting treatment.

The 2026-27 NCERT no longer treats “Redemption by Conversion” as a separate Board-paper route. It is now folded into a 2 to 3 mark theory question on convertibility.

Common Mistakes Class 12 Students Make in Issue and Redemption of Debentures

- Crediting Debentures A/c at the issue price instead of the face value.

- Routing “premium payable on redemption” through Securities Premium Reserve instead of a separate Premium on Redemption of Debentures A/c.

- Forgetting to write off Loss on Issue in the year of issue itself, treating it as a deferred expense in the older NCERT style.

- Confusing DRR (a reserve out of profits) with DRI (an investment in specified securities). The two are independent obligations.

- Missing the 30 April DRI deadline in dated-entry problems.

- Treating a listed company as needing 10% DRR; the post-2019 rules set DRR for listed companies at Nil.

CBSE Class 12 Accountancy Previous Year Question Mapping for Part 2 Chapter 2

The table below tracks the dominant question shape on debentures over the last five CBSE Board cycles. The chapter has carried the 8-mark Long Answer every year, with the issue-redemption six-case matrix as the most frequent anchor.

| Year | Question Shape | Marks |

|---|---|---|

| 2025 | Issue at Premium redeemable at Premium plus DRR computation | 8 |

| 2024 | Issue for consideration other than Cash plus 30 April DRI date | 8 |

| 2023 | Open Market Purchase and cancellation of own debentures | 8 |

| 2022 | Six-case matrix, two cases asked together | 6 |

| 2021 | Loss on Issue, write-off route under Section 52 | 3 |

Full year-wise PYQ map: Issue and Redemption of Debentures Class 12 Solutions.

Related Resources

- NCERT Solutions for Class 12 Accountancy Part 2 Chapter 2 Issue and Redemption of Debentures

- Handwritten Notes for Class 12 Accountancy Part 2 Chapter 2 Issue and Redemption of Debentures

- NCERT Book PDF for Class 12 Accountancy Part 2 Chapter 2 Issue and Redemption of Debentures

NCERT Notes for Class 12 Accountancy: All Chapters

| Chapter | Notes Link |

|---|---|

| Chapter 1 | Accounting for Partnership: Basic Concepts Notes |

| Chapter 2 | Reconstitution of a Partnership Firm: Admission of a Partner Notes |

| Chapter 3 | Reconstitution of a Partnership Firm: Retirement or Death of a Partner Notes |

| Chapter 4 | Dissolution of Partnership Firm Notes |

| Part 2 Chapter 1 | Accounting for Share Capital Notes |

| Part 2 Chapter 3 | Financial Statements of a Company Notes |

| Part 2 Chapter 4 | Financial Statements Analysis Notes |

| Part 2 Chapter 5 | Accounting Ratios Notes |

| Part 2 Chapter 6 | Cash Flow Statement Notes |

FAQs on NCERT Class 12 Accountancy Notes Part 2 Chapter 2 Issue and Redemption of Debentures

Ques. What is the CBSE weightage of Part 2 Chapter 2 Issue and Redemption of Debentures in Class 12 Accountancy?

Ans.

Part 2 Chapter 2 Issue and Redemption of Debentures is part of the Company Accounts unit and carries 8 marks in every CBSE Class 12 Accountancy Board paper since 2019, typically delivered as a single Long Answer question on either issue at premium / discount or redemption by lump-sum or open market.

Comments