These NCERT Notes Class 12 Accountancy Chapter 4 Dissolution of Partnership Firm cover the closing chapter of the Partnership Accounts unit. They centre on the Realisation Account and Section 48 payment order, matching the 6 to 8 mark Long Answer in CBSE Board papers.

- CBSE Weightage: 6 to 8 marks (Part A, Partnership Accounts)

- Notes Length: 18 pages with one solved dissolution problem and the Garner versus Murray application

The notes cover partnership versus firm dissolution, the five modes under Sections 39 to 44, the Realisation Account with its eight entries, unrecorded items, realisation expenses, partner’s loan handling, Section 48 and 49, and the trimmed Garner versus Murray rule.

Chartered Accountants and senior Commerce educators reviewed these Notes, mapped to the 2026-27 NCERT textbook and checked against five years of CBSE Board papers.

Also Check:

- Dissolution of Partnership Firm Class 12 NCERT Solutions

- Retirement of a Partner Class 12 Accountancy Notes

- CBSE Class 12 Accountancy Syllabus 2026-27

NCERT Notes Class 12 Accountancy Chapter 4 Dissolution of Partnership Firm: Section Map

The file has ten focused blocks for a clean revision in about 100 minutes. Exam Yield shows how each idea has appeared in CBSE Board papers from 2021 to 2025.

| Block | What It Covers | Exam Yield |

|---|---|---|

| 1. Partnership vs Firm | Books, court relief, continuity | 3 to 4 marks theory |

| 2. Modes of Dissolution | Sections 39 to 44, five modes | 3 marks theory |

| 3. Realisation Account | Format plus eight journal entries | Core 4-mark machinery |

| 4. Unrecorded Items | Four-case treatment | 2 to 3 marks |

| 5. Realisation Expenses | Four cases: who paid, who bore | 3 to 4 marks |

| 6. Partner’s Loan | Asset side vs liability side | 2 marks |

| 7. Section 48 Order | External, Loans, Capital, Surplus | 3 marks theory |

| 8. Section 49 | Two pools, surplus rule | 2 to 3 marks |

| 9. Deficiency (Garner vs Murray) | Insolvent partner, CBSE-trimmed form | 3 to 4 marks |

| 10. Full Solved Example | Nine-step protocol | 6 marks |

Class 12 Accountancy Chapter 4 Dissolution Of Partnership Firm Notes

Source: Rajat Arora on YouTube

Dissolution of Partnership versus Dissolution of Firm

This is the most repeated theory question in Class 12 Accountancy. A change in the partnership relationship does not always end the firm.

| Basis | Dissolution of Partnership | Dissolution of Firm |

|---|---|---|

| Continuity of business | Continues with a reconstituted firm | Ends; books are closed |

| Closure of books | Not closed; only reconstituted | Closed permanently |

| Settlement of accounts | Not required | Required under Section 48 |

| Court intervention | Not applicable | May be ordered under Section 44 |

| Economic relationship | Only the partners’ contract changes | Firm-outsider relationship ends |

Every dissolution of firm necessarily ends the partnership, but the reverse is not true.

Modes of Dissolution under the Indian Partnership Act, 1932

- Section 40, Agreement: all partners consent.

- Section 41, Compulsory: insolvency of all but one, or an unlawful business.

- Section 42, Contingencies: term expiry, venture completion, death, or insolvency.

- Section 43, By Notice: a partnership at will, by written notice.

- Section 44, Court Order: insanity, incapacity, misconduct, breach, transfer of interest, or losses.

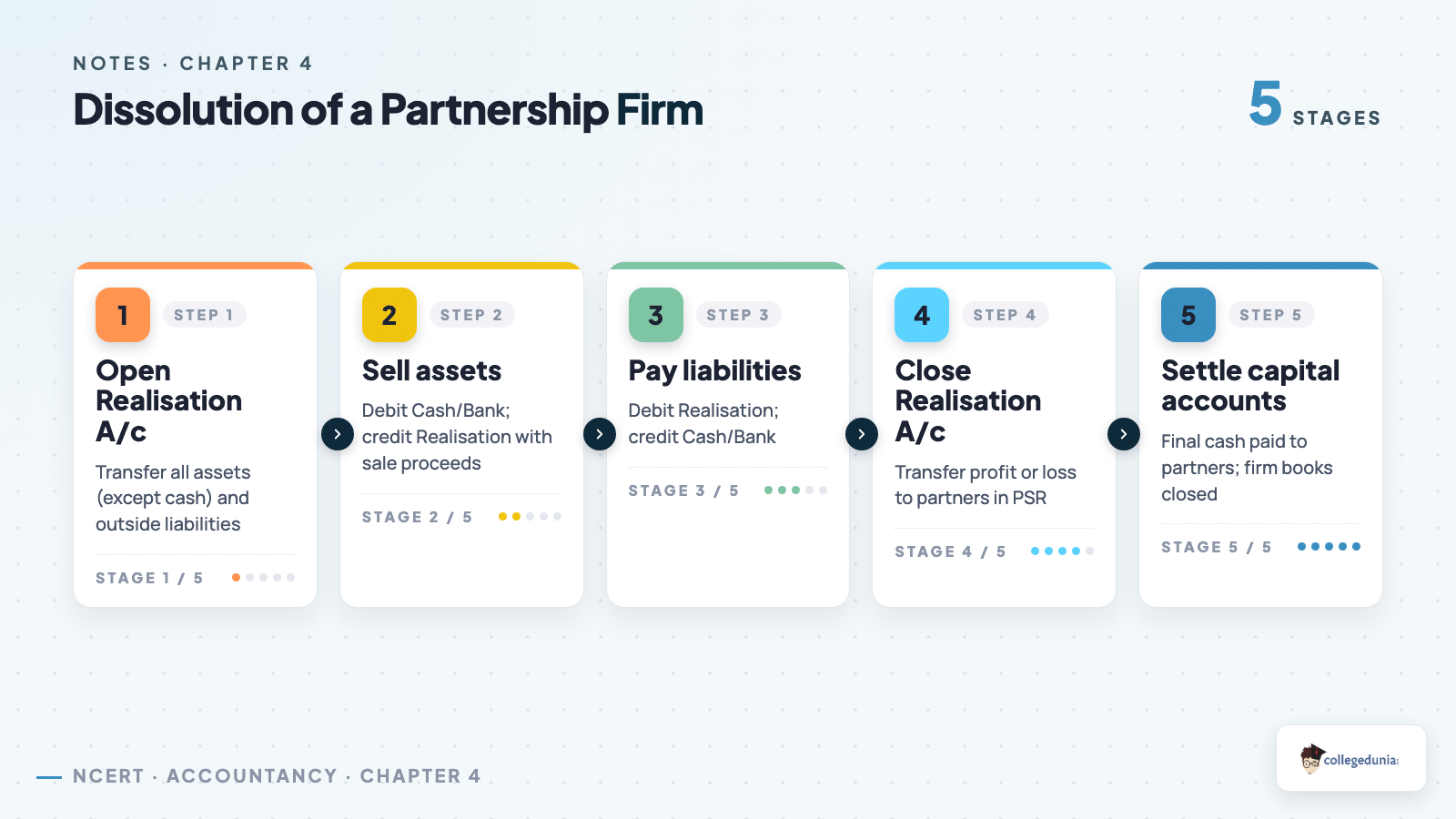

The Realisation Account: Format and the Eight Standard Entries

The Realisation Account is the central ledger of dissolution. Assets, except cash, bank, fictitious assets and partner balances, close to its debit side. Outside liabilities close to its credit side. The balancing figure is profit or loss on realisation, shared in the current PSR.

- Assets at book value: Dr. Realisation A/c.

- External liabilities at book value: Cr. Realisation A/c.

- Sale of assets: Bank A/c Dr. to Realisation A/c.

- Payment of liabilities: Realisation A/c Dr. to Bank A/c.

- Asset taken by partner: Partner’s Capital A/c Dr. to Realisation A/c.

- Liability assumed by partner: Realisation A/c Dr. to Partner’s Capital A/c.

- Expenses paid by firm: Realisation A/c Dr. to Bank A/c.

- Profit or loss: shared in PSR via Partners’ Capital A/cs.

Cash, bank and fictitious balances never go to Realisation A/c; fictitious balances move straight to Partners’ Capital A/cs in PSR. Routing Cash A/c through Realisation A/c is the most common one-mark slip.

Unrecorded Assets and Unrecorded Liabilities

An unrecorded item does not appear on the Balance Sheet but surfaces during winding up:

- Asset sold for cash: Bank A/c Dr. to Realisation A/c.

- Asset taken by partner: Partner’s Capital A/c Dr. to Realisation A/c.

- Liability paid in cash: Realisation A/c Dr. to Bank A/c.

- Liability assumed by partner: Realisation A/c Dr. to Partner’s Capital A/c.

No transfer entry is passed, since there is no opening book value. The gain or loss flows straight through Realisation A/c.

Realisation Expenses: Four Scenarios

| Case | Who Paid | Who Bore | Treatment |

|---|---|---|---|

| 1 | Firm | Firm | Realisation A/c Dr. to Bank A/c |

| 2 | Firm | Partner | Partner’s Capital A/c Dr. to Bank A/c |

| 3 | Partner | Firm | Realisation A/c Dr. to Partner’s Capital A/c |

| 4 | Partner | Partner | No entry in firm’s books |

If a partner takes a fixed remuneration to wind up the business, debit Realisation A/c and credit that Partner’s Capital A/c. Expenses the firm pays after that belong to the partner, so debit his Capital A/c.

Partner’s Loan: Asset Side and Liability Side

- Loan BY the partner (liability side): not transferred to Realisation A/c; settled AFTER creditors, BEFORE Capital. Entry: Partner’s Loan A/c Dr. to Bank A/c.

- Loan BY the firm (asset side): also not transferred; closed against that partner’s Capital A/c. Entry: Partner’s Capital A/c Dr. to Loan to Partner A/c.

Section 48: The Settlement Order of Payment

Section 48 sets a strict order for cash from asset sales, plus any deficiency contributed by partners:

- Dissolution expenses and outside (External) debts.

- Loans and advances from partners to the firm.

- Capital balances due to partners.

- Surplus, distributed in the profit-sharing ratio.

Remember the sequence with the cue ELCS: External, Loans, Capital, Surplus. Writing the Bank A/c strictly in this order earns the full presentation mark.

Section 49: Firm Debts versus Partner’s Private Debts

Section 49 covers two pools. Firm property first pays firm debts; surplus then goes to partners. A partner’s private property first pays private debts; surplus goes to the firm for unsettled debts.

The two pools never mix until each primary obligation is fully met.

Deficiency of Capital: The Garner versus Murray Position

When a partner’s Capital A/c shows a debit balance at dissolution and that partner cannot pay, a deficiency arises. CBSE has trimmed the historical Garner versus Murray treatment: solvent partners now bear the deficiency in the profit-sharing ratio, unless the question says otherwise.

Three classical Garner versus Murray conditions still come up as theory: the deed is silent on insolvency, solvent partners keep fluctuating capitals, and the insolvent partner has a debit balance after closing his accounts.

How Collegedunia’s Notes Help You Score the Full 6 to 8 Marks

- A fixed eight-entry Realisation Account sequence, so a blank sheet never feels intimidating.

- The Section 48 ELCS order reinforced in the Bank A/c walkthrough.

- A four-case unrecorded-item table covering two standard 2-mark variants.

- Garner versus Murray summarised as CBSE marking now expects.

- A nine-step protocol for any 6-mark dissolution question.

Common Mistakes in Dissolution of Partnership Firm

- Transferring Cash or Bank balance to Realisation A/c.

- Routing a partner’s loan through Realisation A/c, not a separate Loan A/c.

- Splitting realisation profit or loss in the old ratio, not PSR.

- Forgetting unrecorded assets and liabilities.

- Treating a creditor’s costlier asset as a loss, not a gain.

- Ignoring fictitious balances (Dr. P&L A/c) at the start.

Other Resources

NCERT Notes for Class 12 Accountancy: All Chapters

The full chapterwise Notes index for Class 12 Accountancy, Parts A and B, aligned to the 2026-27 NCERT.

| Chapter | NCERT Notes Link |

|---|---|

| Chapter 1 | Accounting for Partnership: Basic Concepts Notes |

| Chapter 2 | Admission of a Partner Notes |

| Chapter 3 | Retirement / Death of a Partner Notes |

| Chapter 5 | Accounting for Share Capital Notes |

| Chapter 6 | Issue and Redemption of Debentures Notes |

Other Resources for Dissolution of Partnership Firm

Other resources for this chapter:

| Resource | Link |

|---|---|

| NCERT Solutions | Dissolution of Partnership Firm NCERT Solutions |

| Notes | Dissolution of Partnership Firm Notes |

| NCERT Book PDF | Dissolution of Partnership Firm NCERT Book PDF |

| Handwritten Notes | Dissolution of Partnership Firm Handwritten Notes |

| Previous Year Questions | Dissolution of Partnership Firm Previous Year Questions |

Student Feedback

In a Collegedunia poll of 1,240 Class 12 Commerce students, 76% rated Dissolution of Partnership Firm among the tougher parts of the Accountancy syllabus. After using these revision notes, 4 in 5 said they felt ready for the board questions from this chapter.

Frequently Asked Questions

Ques. What is the difference between dissolution of partnership and dissolution of firm?

Ans.

Dissolution of partnership is a change in the relationship among partners (admission, retirement, death) where the firm continues business with a reconstituted set of partners. Dissolution of firm closes the business itself, settles all accounts under Section 48, and closes the books permanently. Every dissolution of firm involves dissolution of partnership, but not the reverse.

Ques. Why are Cash and Bank not transferred to Realisation A/c?

Ans.

Cash and Bank are the media through which realisation transactions flow. Sale of assets brings cash in; payment of liabilities and expenses takes cash out. If Cash or Bank were closed to Realisation A/c at the start, there would be no live cash account to record those flows. They remain open throughout dissolution and close only when the final Capital balances are paid off.

Ques. What is the Section 48 order of payment?

Ans.

Section 48 of the Indian Partnership Act, 1932 fixes the order as: first pay outside (External) debts and dissolution expenses, then repay partners’ loans and advances, then settle Capital balances, and finally distribute any Surplus in the profit-sharing ratio. The cue ELCS captures the sequence.

Ques. How is the deficiency of an insolvent partner’s capital treated in the current CBSE syllabus?

Ans.

The classical Garner versus Murray rule (deficiency borne by solvent partners in their capital ratio) has been trimmed in the current CBSE prescription. The deficiency is now borne by the solvent partners in the profit-sharing ratio unless the question states otherwise. The three classical conditions of Garner versus Murray remain examinable as a 2 to 3 mark theory question.

Ques. How is a partner’s loan to the firm settled on dissolution?

Ans.

A partner’s loan to the firm is not transferred to Realisation A/c. It is settled through a separate Partner’s Loan A/c after all outside creditors have been paid but before any Capital balance is returned. Entry: Partner’s Loan A/c Dr. to Bank A/c.

Ques. What are unrecorded assets and liabilities, and how are they treated?

Ans.

Unrecorded items do not appear on the Balance Sheet but surface during winding up. Sale of an unrecorded asset is credited to Realisation A/c. Payment of an unrecorded liability is debited to Realisation A/c. If a partner takes the asset or assumes the liability, the corresponding entry routes through that Partner’s Capital A/c. No opening transfer entry is required because the book value is zero.

Comments