These ncert class 12 accountancy notes chapter 3 Reconstitution of a Partnership Firm – Retirement / Death of a Partner are aligned to the current 2026-27 NCERT print and condense the entire 32-page Reconstitution of a Partnership Firm: Retirement / Death of a Partner chapter into an exam-ready revision document. The notes follow a fixed five-pass workflow used by CBSE markers: ratios, goodwill, revaluation, reserves, settlement.

- CBSE Weightage: 8 to 10 marks in the Part A Partnership cluster (typically one full Long Answer plus a 1 mark theory tag)

- Coverage: 19-page revision PDF, 9 conceptual sections, 14 ledger formats, 6 solved problems

These Collegedunia notes are curated by Chartered Accountants and senior commerce educators, mapped section-by-section to the 2026-27 NCERT Accountancy textbook (Part 1), and refined against the last five years of CBSE Class 12 Board papers.

Also Check:

- Retirement of a Partner Class 12 Accountancy NCERT Solutions

- Dissolution of Partnership Firm Class 12 Accountancy Notes

- CBSE Class 12 Accountancy Syllabus 2026-27

ncert class 12 accountancy notes chapter 3 Reconstitution of a Partnership Firm – Retirement / Death of a Partner: What the Chapter Covers

Chapter 3 is part of Unit 1: Accounting for Partnership Firms. It deals with two events that change the partnership constitution without dissolving the firm: voluntary retirement of an existing partner and death of a partner during the accounting year. Both events trigger the same five accounting adjustments, but the death case adds three special workings, namely interest up to date of death, share of profit up to date of death, and the Executor's Loan Account schedule.

| Section | What It Covers | Typical Mark Yield |

|---|---|---|

| 1. Modes of Retirement | Section 32 of the Indian Partnership Act 1932, consent, express agreement, written notice at-will | 1 to 2 marks theory |

| 2. New Ratio and Gaining Ratio | New ratio when agreed or assumed; Gaining ratio = New ratio minus Old ratio | 1 to 2 marks routine |

| 3. Goodwill Treatment | AS-26 compliance, existing goodwill write-off, adjustment through gaining ratio | 3 to 4 marks |

| 4. Revaluation Account | Format, debit and credit rules, net result split in OLD ratio | 4 marks |

| 5. Reserves and Accumulated Profits | General Reserve and P&L A/c balance distributed in OLD ratio to all partners | 2 to 3 marks |

| 6. Modes of Settlement | Cash lump sum, instalments, transfer to Loan A/c, part asset transfer | 2 marks theory |

| 7. Death and Executor's A/c | Capital A/c balance transferred to Executor's A/c; instalment schedule with interest | 6 marks |

| 8. Share of Profit up to Death | Time basis using last year's profit, OR sales basis using sales ratio | 2 to 3 marks |

| 9. Capital Adjustment | Fixed total capital method, or combined-balance method | 3 to 4 marks |

The CBSE Board paper almost always pulls a single 6 to 8 mark Long Answer question from sections 3, 4, 7 or 9, with a 1 mark theory tag from section 1 or 6. The notes prioritise these five sections.

Reconstitution of a Partnership Firm Retirement Death of a Partner...

Source: Rajat Arora on YouTube

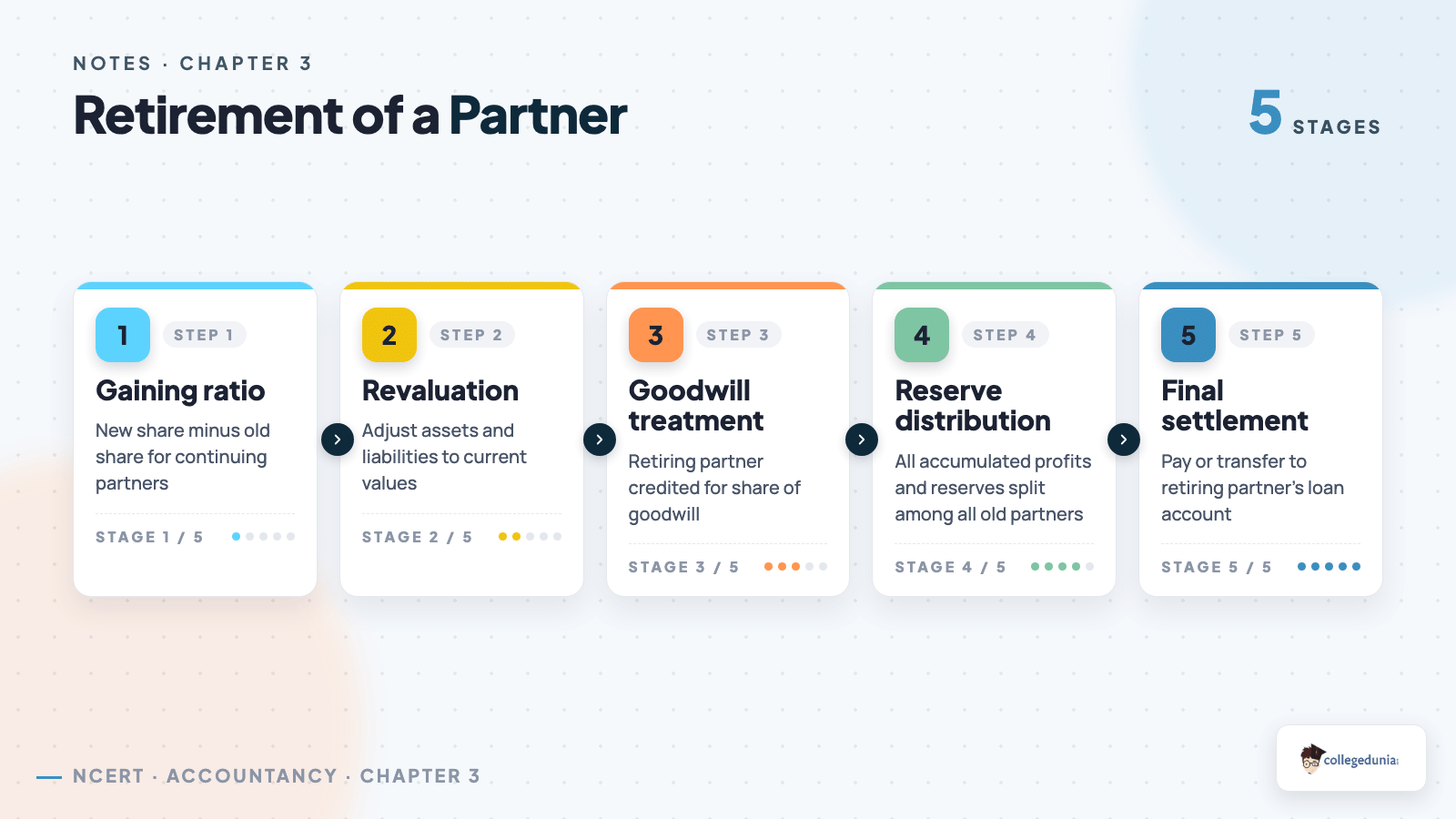

The Five-Pass Framework for Retirement and Death Numericals

Every retirement or death numerical, regardless of phrasing, decomposes into the same five passes. Applying them in fixed order eliminates decision paralysis in the exam hall. The mnemonic is R-G-R-R-S.

- Ratios. Compute the new profit-sharing ratio (NPSR), then the gaining ratio = NPSR minus OPSR. If the question is silent on the new ratio, assume the continuing partners share the outgoing partner's stake in their OLD ratio, which means the gaining ratio equals the old ratio between the continuing partners.

- Goodwill. Step one: write off any existing goodwill in the books by debiting all partners (including the outgoing partner) in their OLD ratio. Step two: pass the new goodwill adjustment entry, debiting the continuing partners in their GAINING ratio and crediting the outgoing partner's Capital A/c with his share of firm goodwill.

- Revaluation. Open a Revaluation A/c. Debit losses (decrease in asset, increase in liability, unrecorded liability), credit gains (increase in asset, decrease in liability, unrecorded asset). Split the net result among ALL partners in the OLD ratio.

- Reserves and accumulated profits. Distribute General Reserve, Workmen Compensation Reserve (excess), Investment Fluctuation Reserve (excess) and the P&L A/c credit balance to all partners in their OLD ratio. P&L debit balance and deferred revenue expenditure are debited similarly.

- Settlement. Compute the outgoing partner's final closing balance after all four passes. Settle by cash, by transfer to Loan A/c (with interest under Section 37 at 6 percent p.a. if the deed is silent), by instalments, or by part-asset transfer, exactly as the question states.

Goodwill Adjustment Through Gaining Ratio, Not Sacrificing Ratio

This is the single most-tested CBSE trap. On admission of a partner, the goodwill adjustment runs through the sacrificing ratio. On retirement or death, the same adjustment runs through the gaining ratio. Mixing these costs students 2 to 3 marks every year.

The journal entry on retirement is:

Continuing Partner B's Capital A/c Dr. (gaining share)

To Retiring Partner's Capital A/c (his share of firm goodwill)

Under AS-26 (Intangible Assets), the firm cannot raise goodwill in the books because it is internally generated. Any existing goodwill in the Balance Sheet must therefore be written off first by debiting all partners in their OLD ratio against the goodwill asset.

Hidden Goodwill, A High-Mark CBSE Variant

When the deed does not disclose the firm's goodwill but specifies the lump-sum amount payable to the retiring partner, hidden goodwill is back-calculated:

$$\text{Hidden Goodwill of Firm} = \frac{\text{Amount Payable} - \text{Closing Capital of Retiring Partner}}{\text{Retiring Partner's Profit Share}}$$

The retiring partner is then credited with his share of this hidden goodwill, debited to the continuing partners in the gaining ratio. This variant carried 4 marks in CBSE 2023.

Share of Profit up to Date of Death: Time Basis vs Sales Basis

For a partner dying during the year, the firm must credit his Capital A/c with his proportionate share of the current year's profit up to the date of death. Two bases are used, dictated by the exact wording of the partnership deed clause.

| Basis | Trigger Phrase in Deed | Formula |

|---|---|---|

| Time Basis | "on the basis of last year's profit" or "average profit" | Last year profit × (months to death ÷ 12) × deceased's share |

| Sales Basis | "in the ratio of sales" or "on the basis of turnover" | Last year profit × (sales to death ÷ last year sales) × deceased's share |

A second method credit option is to debit Profit & Loss Suspense A/c instead of running the entry through the continuing partners' Capital A/cs. The Suspense balance is closed when the next year's profit is determined.

Joint Life Policy and Executor's Loan Account

The Joint Life Policy (JLP) is a survivorship insurance taken by the firm on all partners jointly. On death, the policy amount is received from the insurer and credited to the deceased partner's Capital A/c through the JLP A/c. Three accounting approaches are recognised by NCERT:

- Premium as expense: Premium debited to P&L A/c every year; JLP value not shown in the Balance Sheet.

- Premium as asset: Premium debited to JLP A/c, shown as an asset at surrender value.

- JLP Reserve method: Premium charged to P&L A/c; matching JLP Reserve created on the liabilities side.

After settling all five passes, the deceased partner's closing balance is transferred from his Capital A/c to his Executor's A/c. The executor is then paid as agreed, typically three annual instalments plus 6 percent p.a. interest under Section 37 unless the deed says otherwise.

Capital Adjustment of Continuing Partners

After the retiring partner is paid off, the continuing partners may be required to adjust their capitals so they stand in their new profit-sharing ratio. Two CBSE-tested methods are used:

- Fixed total capital method. The new total capital of the firm is given. Distribute this total in the new ratio to find each partner's required capital, then bring in or withdraw cash to reach that figure.

- Combined-balance method. Add the closing balances of the continuing partners after retirement, then distribute the sum in the new ratio. Differences are settled through Cash A/c or Current A/c (when capitals are fixed).

Common Mistakes Students Make in Reconstitution of a Partnership Firm

- Splitting Revaluation A/c profit or loss in the new ratio instead of the OLD ratio.

- Skipping the existing-goodwill write-off step before adjusting new goodwill.

- Confusing sacrificing ratio (admission) with gaining ratio (retirement).

- Treating a decrease in liabilities as a debit in Revaluation A/c, when it is actually a credit (a gain).

- Forgetting interest on capital up to date of death when the deed provides for it.

- Using the wrong basis (time vs sales) for the deceased partner's share of profit.

- Computing interest on the wrong opening balance in the Executor's A/c instalment schedule (interest accrues on the reducing balance, not the opening lump sum).

How Collegedunia's NCERT Notes Help You Score in Chapter 3

- The R-G-R-R-S framework gives a fixed mental sequence to apply in any retirement or death numerical, removing decision paralysis under exam time pressure.

- Every formula is paired with the exact deed phrase that triggers its use, so the right basis is chosen on first read.

- Hidden goodwill back-calculation is fully derived for the CUET-UG and CA Foundation overlap, where this is a routine tested variant.

- A tabular comparison of Admission, Retirement and Death makes the sign of every goodwill adjustment readable in one glance.

- JLP treatment is covered in all three NCERT-approved accounting approaches, not just the most popular one.

CBSE Class 12 Accountancy Previous Year Question Mapping for Chapter 3

Year-wise CBSE focus areas for Reconstitution of a Partnership Firm: Retirement / Death of a Partner. The 6 to 8 mark Long Answer rotates predictably between goodwill on gaining ratio, the full Revaluation plus Capital Account workings, and the death scenario with Executor's A/c.

| Year | Long Answer Focus | Marks |

|---|---|---|

| 2025 | Revaluation + Capital Adjustment, combined-balance method | 6 |

| 2024 | Death of partner, share of profit on sales basis + Executor's A/c | 8 |

| 2023 | Hidden goodwill back-calculation + gaining ratio entry | 6 |

| 2022 | Retirement with full Revaluation A/c and reserves distribution | 8 |

| 2021 | Goodwill adjustment on retirement in gaining ratio | 4 |

Full PYQ map: Chapter 3 NCERT Solutions with year-wise PYQ workings.

Related Resources for Class 12 Accountancy Chapter 3

- Chapter 3 NCERT Solutions

- Chapter 3 Formula Sheet

- Chapter 3 Handwritten Notes

- Chapter 3 NCERT Book PDF

NCERT Notes for Class 12 Accountancy: All Chapters

| Chapter | Notes Link |

|---|---|

| Chapter 1 | Accounting for Not-for-Profit Organisation Notes |

| Chapter 2 | Accounting for Partnership: Basic Concepts Notes |

| Chapter 4 | Reconstitution: Admission of a Partner Notes |

| Chapter 5 | Dissolution of Partnership Firm Notes |

| Chapter 6 | Accounting for Share Capital Notes |

| Chapter 7 | Issue and Redemption of Debentures Notes |

FAQs on Class 12 Accountancy Chapter 3 Notes

Ques. What is the difference between sacrificing ratio and gaining ratio in partnership accounts?

Ans.

Sacrificing ratio (Old ratio minus New ratio) is used on admission of a new partner and represents the share each old partner gives up. Gaining ratio (New ratio minus Old ratio) is used on retirement or death and represents the share each continuing partner picks up from the outgoing partner. The goodwill journal entry runs through whichever ratio applies to that event.

Ques. Why is the Revaluation Account profit or loss shared in the old ratio?

Ans.

Because the revaluation gain or loss accrued during the period the retiring or deceased partner was still in the firm. He is therefore entitled to (or liable for) his share of the net result in the OLD profit-sharing ratio, alongside the continuing partners.

Ques. When is time basis used for the deceased partner's share of profit?

Ans.

Time basis applies when the deed says "share of profit on the basis of last year's profit" or "average profit". Compute: last year's profit multiplied by the fraction of the year elapsed up to date of death, then multiplied by the deceased partner's profit share. Sales basis is used only when the deed explicitly references sales or turnover.

Ques. What is the rate of interest payable to the retiring partner under Section 37 if the partnership deed is silent?

Ans.

If the deed is silent, the retiring partner is entitled to interest at 6 percent per annum on the unpaid balance, OR a share of profits attributable to the use of his capital, whichever he chooses. This is the default rule under Section 37 of the Indian Partnership Act 1932.

Ques. What is hidden goodwill on retirement of a partner?

Ans.

Hidden goodwill is the firm's implied goodwill, back-calculated when the deed does not disclose goodwill but the agreed amount payable to the retiring partner exceeds his closing capital balance. The formula is: Firm's goodwill equals (Amount Payable minus Closing Capital Balance) divided by the retiring partner's profit share. The retiring partner is then credited with his share, debited to continuing partners in the gaining ratio.

Ques. How is the deceased partner's Capital Account closed?

Ans.

After all five adjustments (ratios, goodwill, revaluation, reserves, share of profit and interest up to date of death) are credited or debited, the final balance is transferred from the deceased partner's Capital A/c to his Executor's A/c. The executor is then paid as per the deed, usually in annual instalments with interest at 6 percent p.a. under Section 37 unless a different rate is agreed.

Comments