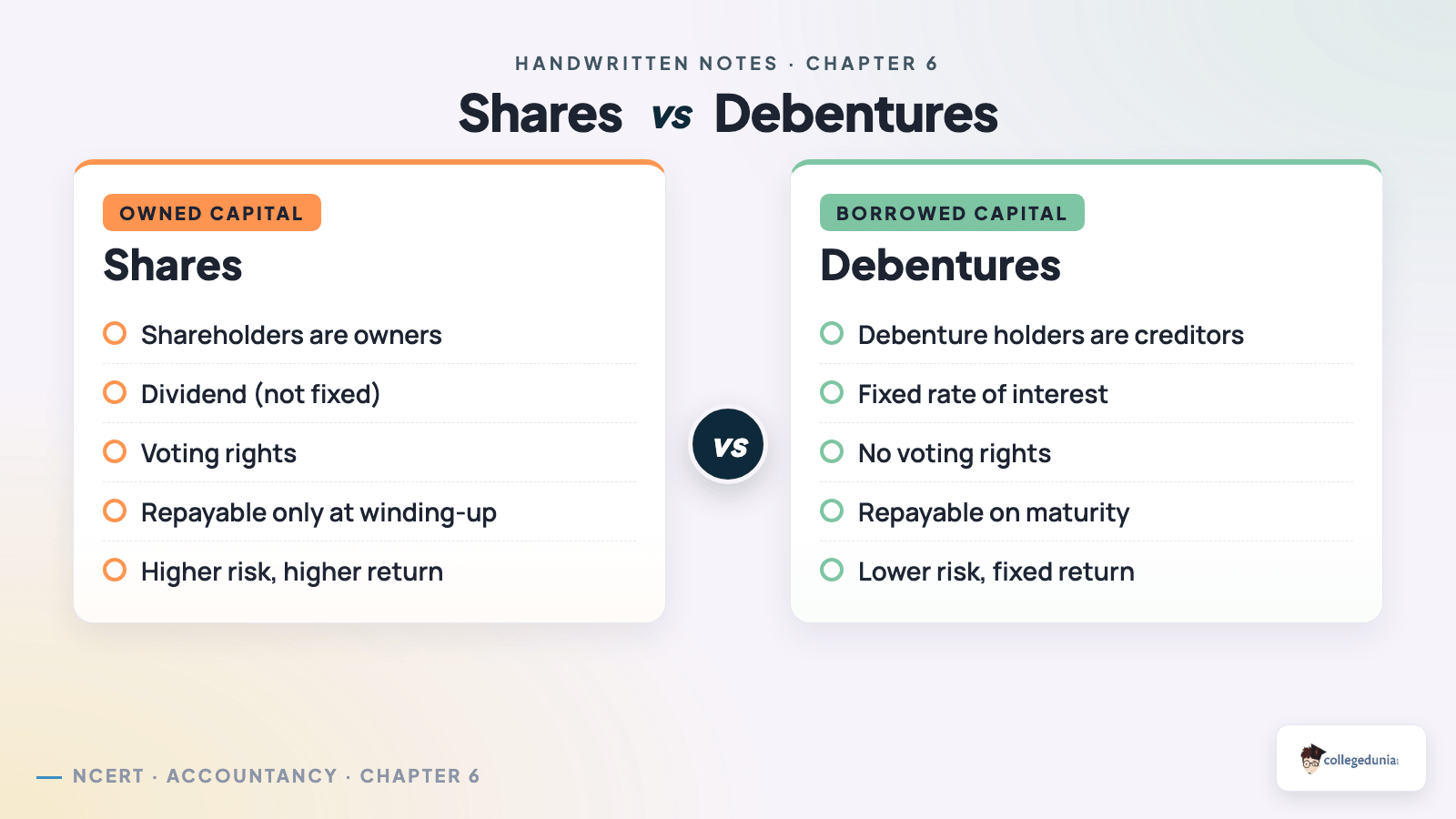

The Issue and Redemption of Debentures class 12 accountancy handwritten notes cover debenture issue at par, premium and discount, interest and TDS, redemption by lump-sum and instalment, and open-market purchase.

- CBSE Weightage: 8 to 10 marks - typically one 6-mark redemption numerical and one 4-mark journal block.

- Entrance exams: CUET and B.Com papers frequently test issue-at-discount with redemption-at-premium and the DRR/DIF rule.

Also Check:

- Issue and Redemption of Debentures Class 12 Notes (Typeset)

- Issue and Redemption of Debentures Class 12 NCERT Solutions

What the 9 Pages of the Issue and Redemption of Debentures Handwritten Notes Cover

The nine pages map one journal pattern per page, each recurring in CBSE Part B questions. Use the table below as your guide.

| Page | Focus | What you copy first |

|---|---|---|

| Page 1 | Debenture definition and issue journal block | Written acknowledgement of debt under a common seal; 3-stage issue entries. |

| Page 2 | Issue-redemption matrix | Six combinations: Par-Par, Par-Premium, Discount-Par, Discount-Premium, Premium-Par, Premium-Premium. |

| Page 3 | Loss on Issue table | Capital loss written off against Securities Premium first, then Statement of P&L. |

| Page 4 | Interest and TDS | Charge against profit, net of TDS at 10% under Section 193. |

| Page 5 | Issue as collateral security | No-entry with footnote, or full entry via Debenture Suspense A/c. |

| Page 6 | DRR and DIF rules | DRR 10% before redemption; DIF 15% invested by 30th April. |

| Page 7 | Lump-sum and instalment redemption | Single-date or equal annual tranches by draw of lots. |

| Page 8 | Open-market purchase | Profit on cancellation routes to Capital Reserve. |

| Page 9 | Seven slip warnings | Red-pen margin arrows: trap, rule, safer entry. |

Class 12 Accountancy Part 2 Chapter 2 Issue And Redemption Of Debentures Handwritten Notes

Source: Magnet Brains on YouTube

Conditions of Issue and Redemption Matrix: The Page-2 Six-Cell Grid

Page 2 shows the six issue-redemption combinations in a 2x3 grid. CBSE almost always picks one cell as the stem of a 4-mark or 6-mark question.

| Issue condition | Redemption condition | Loss on Issue? | Premium leg present? |

|---|---|---|---|

| At Par | At Par | No | No |

| At Par | At Premium | Yes (premium on redemption) | Premium on Redemption A/c Cr |

| At Discount | At Par | Yes (discount only) | Discount on Issue A/c Dr |

| At Discount | At Premium | Yes (discount + premium) | Both legs |

| At Premium | At Par | No | Securities Premium A/c Cr |

| At Premium | At Premium | Yes (premium on redemption) | Both premium legs |

How Collegedunia's Handwritten Notes Help You in the Last 24 Hours

Print and fold the booklet for a pocket-size revision strip. It works because:

- The six-cell grid is the most-asked stem; recall it in under 30 seconds.

- DRR/DIF rules with exact percentages and dates (30th April) prevent one-mark losses.

- Redemption ladders are sequenced as the marker expects, saving 2 minutes per question.

Interest on Debentures and TDS Treatment: The Page-4 P&L Charge

Page 4 shows entries students confuse with dividend treatment. Interest is a profit charge (paid even if the firm has no profit); TDS at 10% (Section 193) is deducted from resident-individual holders.

- Interest due: Debenture Interest A/c Dr (gross), to Debentureholders A/c (net), to TDS Payable A/c (10% of gross).

- Payment and TDS deposit: Debentureholders A/c Dr, to Bank A/c (net cheque); then TDS Payable A/c Dr, to Bank A/c.

- Year-end closure: Statement of P&L Dr, to Debenture Interest A/c.

The margin note reads "deduct TDS only when residency is stated; do not assume it in MCQ stems."

DRR and DIF Rule: The Page-6 Statutory Pair

Page 6 covers the two statutory provisions CBSE always checks: DRR (created from profits before redemption) and DIF (the matching liquid asset the firm must hold).

| Item | Statutory rate | Base | Timing |

|---|---|---|---|

| DRR creation | 10% of nominal value of debentures to be redeemed | Out of profits available for dividend | Before redemption commences |

| DRI / DIF deposit | 15% of nominal value due for redemption in the next FY | Invested in specified securities | By 30th April of the year of redemption |

| DRR transfer on redemption | Full DRR balance | - | Move to General Reserve after all debentures are redeemed |

The 30th April deadline is circled in red because CBSE has used it as a one-mark stem in three of the last five sessions.

Redemption Methods: Lump-Sum, Instalment, and Open-Market Purchase

Pages 7 and 8 cover the standard 6-mark redemption numerical. Each method has different journal entries; the paper rotates between them.

- Lump-sum redemption: Debentures A/c Dr (nominal), Premium on Redemption A/c Dr (if any), to Debentureholders A/c. Then Debentureholders A/c Dr, to Bank A/c.

- Instalment by draw of lots: Equal annual tranches selected by random draw. Each tranche follows the lump-sum entries on the proportional nominal value.

- Purchase from open market: Own Debentures A/c Dr (cost price), to Bank A/c. Then Debentures A/c Dr (nominal), to Own Debentures A/c (cost), to Capital Reserve A/c (profit on cancellation).

Seven Frequent Debentures Slip Warnings: Page 9 Red-Pen Margin Arrows

Page 9 lists seven slip patterns from 200 CBSE answer scripts, marked with red-pen arrows. The notebook uses blue (journals), red (rates/dates), and green underlines (account heads) to distinguish issue-at-par from issue-at-premium scenarios.

| # | Slip pattern | Correct treatment |

|---|---|---|

| 1 | Booking Loss on Issue in the Par-Par cell | No Loss on Issue arises when both issue and redemption are at par. |

| 2 | Writing off Loss on Issue first against P&L | Securities Premium A/c first, balance to Statement of P&L. |

| 3 | Treating debenture interest like dividend | Charge against profit; debit Statement of P&L, not P&L Appropriation. |

| 4 | Creating DRR at 25% (old rule) | Current 2026-27 syllabus uses 10% of nominal value. |

| 5 | Investing DIF after 30th April | 15% investment must be in place by 30th April of the year of redemption. |

| 6 | Routing profit on cancellation to P&L | Capital profit; transfer to Capital Reserve. |

| 7 | Missing the footnote on collateral issue | No-entry method requires a contingent-liability footnote. |

Tick each of these seven boxes and the chapter costs you at most one presentation mark.

Memory Mnemonics for Debentures Quick Recall

- 10-15-30: 10% DRR, 15% DIF, by 30th April.

- SP first, P&L next: Loss on Issue routes through Securities Premium first.

- OPC equals CR: Open-market Profit on Cancellation = Capital Reserve.

Full formula sheet: Issue and Redemption of Debentures Formula Sheet.

Other Resources for Class 12 Accountancy Part 2 Chapter 2

- Issue and Redemption of Debentures Handwritten Notes

- Class 12 Accountancy Part 2 Chapter 2 Notes (Typeset)

- Class 12 Accountancy Part 2 Chapter 2 NCERT Solutions

- Class 12 Accountancy Part 2 Chapter 2 Formula Sheet

- Class 12 Accountancy Part 2 Chapter 2 NCERT Book PDF

NCERT Handwritten Notes for Class 12 Accountancy: All Chapters

Student Feedback

In a Collegedunia poll of 1,240 Class 12 Commerce students, 76% rated Issue and Redemption of Debentures among the tougher parts of the Accountancy syllabus. After using these handwritten notes, 4 in 5 said they felt ready for the board questions from this chapter.

Issue and Redemption of Debentures Class 12 Handwritten Notes FAQs

Ques. What does the Issue and Redemption of Debentures class 12 accountancy handwritten notes PDF contain?

Ans.

Nine ruled pages: debenture issue journal block, the six-cell issue-redemption matrix, Loss on Issue table, interest on debentures and TDS, collateral security, DRR and DIF rules, lump-sum and instalment redemption, open-market purchase and cancellation, and seven red-pen slip warnings. The booklet is sized for last-day revision and assumes you have read the typeset Notes PDF once.

Ques. When is Loss on Issue of Debentures booked?

Ans.

Loss on Issue is booked at the time of issue whenever debentures are issued at a discount, redeemed at a premium, or both. The amount equals discount on issue plus premium on redemption. It is written off first against Securities Premium A/c and then against Statement of P&L if any balance remains.

Ques. What is the DRR percentage required before redemption under the current 2026-27 syllabus?

Ans.

Debenture Redemption Reserve is created at 10% of the nominal value of debentures to be redeemed, out of profits available for dividend, before redemption commences. The earlier 25% requirement no longer applies. Additionally, 15% of the nominal value due for redemption in the next financial year must be invested in specified securities by 30th April of that year as DRI / DIF.

Ques. How is profit on cancellation of own debentures treated?

Ans.

When a firm buys its own debentures from the open market at a price below face value and cancels them, the gap is a capital profit and is transferred to Capital Reserve A/c. It never routes through Statement of P&L. The booklet draws this transfer on page 8 as a single-line ladder.

Ques. Are handwritten notes enough to cover the debentures chapter for CBSE 2026?

Ans.

The handwritten notes are a final-day revision aid, not a first-read resource. Pair them with the Collegedunia typeset Notes PDF and at least 8 solved redemption numericals from the NCERT textbook for a complete 8 to 10 mark coverage of the chapter in the Accountancy Part B paper.

Comments