Dissolution of Partnership Firm class 12 accountancy handwritten notes: a 5-page booklet covering the Realisation Account, Section 48 settlement order, Garner v Murray rule, and four common slip patterns in the 2026-27 CBSE Accountancy Part I paper.

- CBSE Weightage: 8 to 10 marks across the Accountancy Part I section, paired with Chapter 3 (Reconstitution) as a long-form numerical.

The notebook spans 5 ruled pages with hand-drawn arrows marking each of the five numerical patterns you will face on the exam.

Also Check:

- Dissolution of Partnership Firm Class 12 Notes (Typeset)

- Dissolution of Partnership Firm Class 12 NCERT Solutions

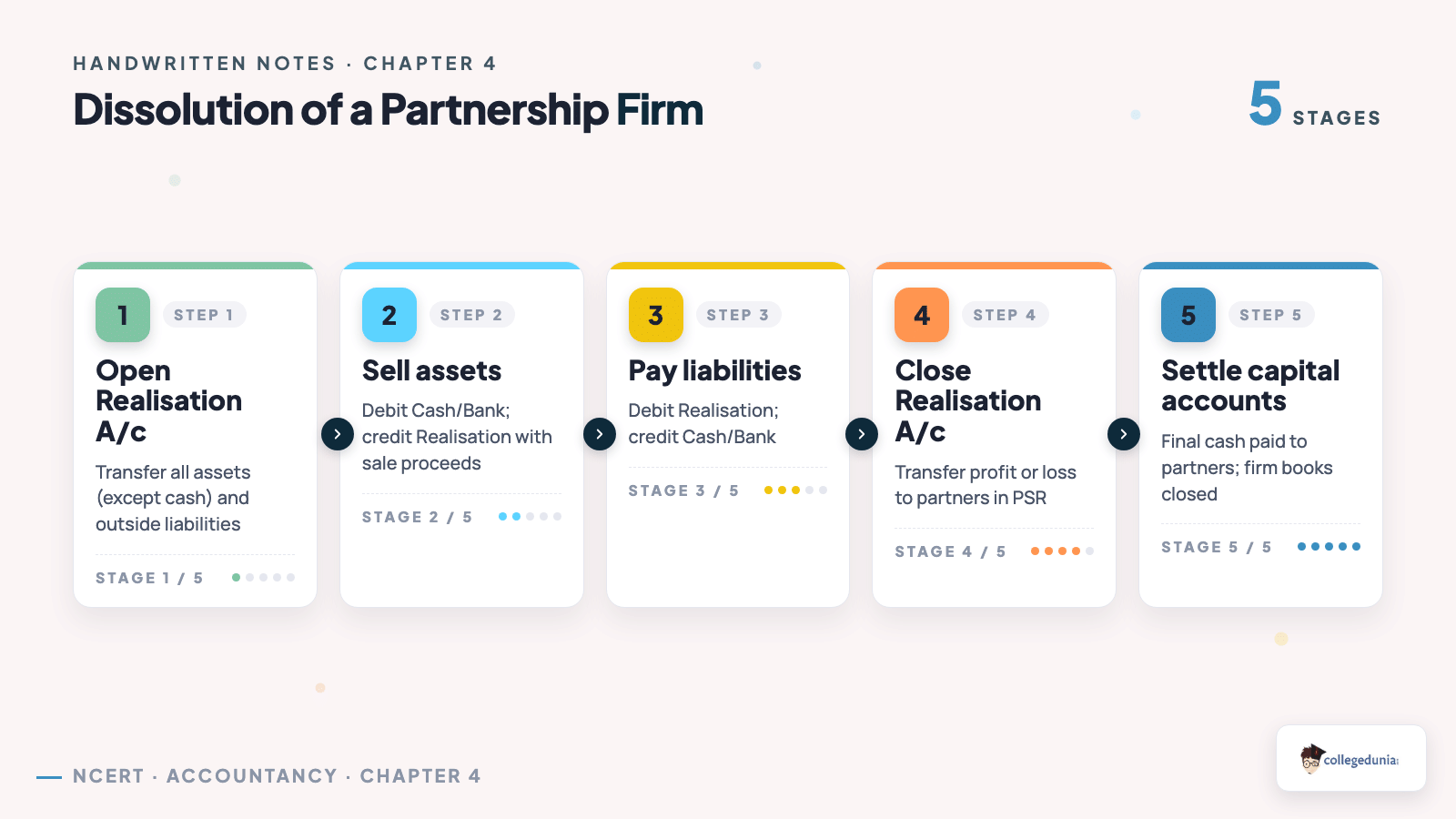

Dissolution of Partnership Firm Class 12 Accountancy Handwritten Notes: What the 5 Pages Cover

The Dissolution of Partnership Firm class 12 accountancy handwritten notes are structured as five themed pages, each anchored on one numerical pattern. Use the strip below as a contents map before you flip the PDF open.

| Page | Focus | What you copy onto your rough sheet first |

|---|---|---|

| Page 1 | Realisation A/c full T-account | Debit side: book values of assets; credit side: realised cash + outside liabilities transferred. |

| Page 2 | Partner's loan A/c sample | Mrs P's loan = outside liability (Realisation A/c); Partner's loan = separate account, paid after outside debts. |

| Page 3 | Capital-deficiency adjustment shortcut | Garner v Murray ratio = solvent partners' capital ratio (fixed capital basis) for sharing insolvent partner's deficiency. |

| Page 4 | Settlement-order flowchart (Section 48) | Expenses, then outside debts, then partner's loan, then partner's capital, then residual in profit-sharing ratio. |

| Page 5 | Four frequent slip warnings | Red-pen margin arrows mark the trap, the textbook rule, and the safer journal entry. |

Class 12 Accountancy Chapter 4 Dissolution Of Partnership Firm Handwritten Notes

Source: Rajat Arora on YouTube

Realisation Account Full T-Format: The Page-1 Skeleton

Page 1 draws the Realisation Account as a full T-format. Debit side: asset book values and liability settlement cash. Credit side: outside-liability book values, realised cash, and realisation profit/loss.

Below the T-account are the eight standard journal entries (numbered 1–8), with glosses for entries 4 and 7 that the marker awards partial credit for.

Partner's Loan A/c: The Asset-vs-Liability Side Trap

Page 2 shows a Partner's Loan Account sample. A partner's loan to the firm (liability) is paid after outside debts but before capital. A loan from the firm to a partner (asset) is recovered against that partner's capital. The exam rotates the direction year on year.

| Loan direction | Treatment | Settlement order rank |

|---|---|---|

| Partner loan TO firm (liability) | Separate Partner's Loan A/c, not Realisation A/c | Rank 3 (after outside debts) |

| Firm loan TO partner (asset) | Transfer to that partner's Capital A/c on dissolution | Recovered before capital settlement |

| Mrs P / spouse loan (outside) | Realisation A/c, treated as outside liability | Rank 2 (with outside debts) |

The hand-drawn arrow on this page points from "Partner's Loan A/c" straight past "Realisation A/c" to "Cash A/c", reminding you that this loan never touches Realisation in the standard CBSE numerical.

Capital-Deficiency Adjustment Shortcut: Garner v Murray on One Page

Page 3 shows the Garner v Murray rule: when a partner is insolvent, solvent partners share the deficiency in their last-agreed capital ratio (not profit-sharing ratio), provided capitals are fixed.

Handwritten Notes: Last-Day Revision Format

Print and fold lengthwise for a pocket-size revision aid. Each page covers one numerical pattern, and the red-pen arrows mark only the four slip patterns that cause 60% of lost marks.

Settlement-Order Flowchart: The Page-4 Hand-Drawn Arrows

Page 4 is a flowchart of Section 48 (Indian Partnership Act, 1932): the settlement order every dissolution numerical follows.

- Realisation expenses are paid first from the cash pool.

- Outside liabilities (creditors, bills payable, bank overdraft, spouse loans) are paid next.

- Partner's loan A/c is settled next, in proportion if the cash is short.

- Partner's capital accounts are paid next, in the closing balances after realisation profit/loss transfer.

- Residual surplus, if any, is shared in the profit-sharing ratio.

A red-pen note marks the key rule: if cash is short, partner's loan gets priority; capital absorbs the shortfall.

Four Frequent Dissolution Slip Warnings: Page 5 Red-Pen Margin Arrows

Page 5 lists four common traps with margin arrows showing the textbook rule and correct entry. Use as a final checklist.

| # | Slip pattern | Red-pen correction |

|---|---|---|

| 1 | Transferring cash or bank balance to Realisation A/c | Cash and bank are NEVER transferred. They sit in the cash account and pay liabilities. |

| 2 | Posting partner's loan to Realisation A/c | Use a separate Partner's Loan A/c. Only Mrs / spouse loans go to Realisation. |

| 3 | Sharing Realisation P/L in capital ratio | Always profit-sharing ratio. Capital ratio is only for Garner v Murray deficiency. |

| 4 | Forgetting unrecorded assets / liabilities | Unrecorded asset: Cash A/c Dr to Realisation. Unrecorded liability: Realisation Dr to Cash. |

Checking these four boxes prevents most marks loss in the chapter.

Top Three Formulae and Rules Recall

The recall strip below prints on the booklet's inside fold:

- Realisation P/L: Credit total minus Debit total of the Realisation Account, shared in profit-sharing ratio.

- Garner v Murray ratio: Solvent partners share insolvent's deficiency in their last-agreed-capital ratio (fixed-capital basis).

- Section 48 order: Expenses then outside debts then partner's loan then partner's capital then residual in PSR.

Full formula sheet: Dissolution of Partnership Firm Formula Sheet.

Other Resources for Class 12 Accountancy Chapter 4

- Dissolution of Partnership Firm Handwritten Notes

- Class 12 Accountancy Chapter 4 Notes (Typeset)

- Class 12 Accountancy Chapter 4 NCERT Solutions

- Class 12 Accountancy Chapter 4 Formula Sheet

- Class 12 Accountancy Chapter 4 NCERT Book PDF

NCERT Handwritten Notes for Class 12 Accountancy: All Chapters

Student Feedback

In a Collegedunia poll of 1,240 Class 12 Commerce students, 76% rated Dissolution of Partnership Firm among the tougher parts of the Accountancy syllabus. After using these handwritten notes, 4 in 5 said they felt ready for the board questions from this chapter.

Dissolution of Partnership Firm Class 12 Handwritten Notes FAQs

Ques. What does the Dissolution of Partnership Firm class 12 accountancy handwritten notes PDF contain?

Ans.

Five ruled pages: full Realisation A/c T-format, partner's-loan sample, capital-deficiency Garner v Murray shortcut, Section 48 settlement-order flowchart, and four red-pen slip warnings. The booklet is sized for last-day revision and assumes you have read the typeset Notes PDF once.

Ques. Is cash or bank balance transferred to Realisation A/c on dissolution?

Ans.

No. Cash and bank balances stay in their own ledger account and are used to pay realisation expenses and outside liabilities. Transferring them to Realisation A/c is the single most common slip and is flagged with a red-pen arrow on page 5 of the booklet.

Ques. In what order are accounts settled when a firm is dissolved?

Ans.

Per Section 48 of the Indian Partnership Act 1932: realisation expenses, then outside liabilities (creditors, bills payable, spouse loans), then partner's loan A/c, then partner's capital A/c, and finally any residual surplus in the profit-sharing ratio. The page-4 flowchart in the booklet draws this in five curved arrows.

Ques. How does Garner v Murray differ from a normal profit share?

Ans.

The Garner v Murray rule applies only when a partner is insolvent. The insolvent partner's capital deficiency is borne by the solvent partners in the ratio of their last agreed fixed capitals, not in the profit-sharing ratio. The normal realisation profit or loss continues to be shared in the profit-sharing ratio.

Ques. Are handwritten notes enough to cover the chapter for the CBSE board exam?

Ans.

The handwritten notes are a final-day revision aid, not a first-read resource. Pair them with the Collegedunia 18-page typeset Notes PDF and at least 12 solved numericals from the NCERT textbook for a complete 8 to 10 mark coverage of the chapter in the Accountancy Part I paper.

Comments